Defense Electro-Optical And Infrared (EOIR) Systems Market Overview

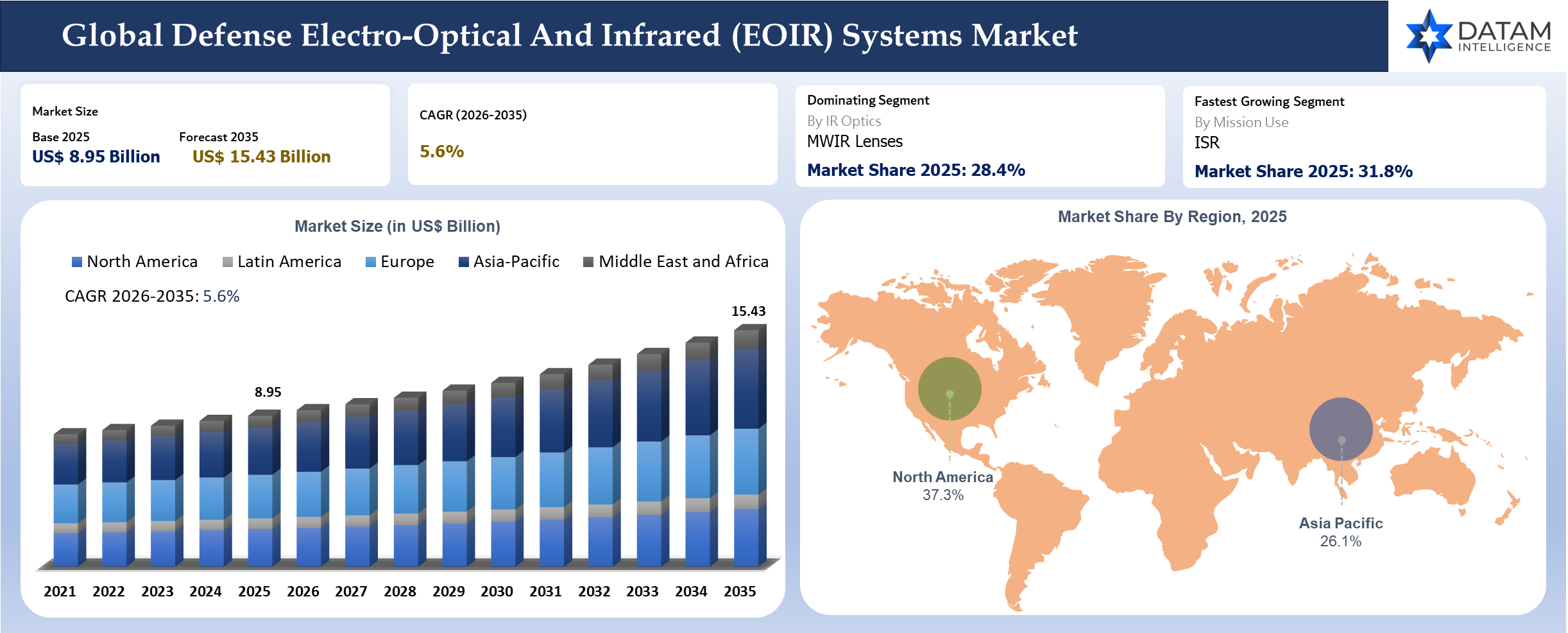

The global defense electro-optical and infrared (EOIR) systems market reached US$ 8.95 billion in 2025 and is expected to reach US$ 15.43 billion by 2035, growing with a CAGR of 5.6% during the forecast period 2026-2035. Growth is being pulled by two procurement realities. Armed forces need persistent visibility against small UAVs, loitering munitions, low-flying missiles, fast boats, infantry teams and camouflaged vehicles. Suppliers also face a deeper optical content requirement because higher resolution sensors need better cooled lenses, thermal coatings, stabilization and edge processing to make imagery usable in real combat conditions. Investment is not translating only into ships, aircraft and land vehicles. A meaningful share is moving into sensor payloads, counter-drone systems, night operations equipment and ISR upgrades because recent conflicts showed that platforms without passive detection and thermal awareness become vulnerable very quickly.

Optics have become a strategic supply chain rather than a commodity input. Germanium, gallium-based detector materials, special glass, chalcogenide compounds and high-precision coatings are exposed to export controls, dual-use licensing and limited refining capacity. China’s restrictions on gallium- and germanium-related exports changed the buying behavior of U.S., European, Israeli, Indian, Japanese and South Korean buyers. Procurement teams now ask for second-source optics, domestic polishing capacity, coating redundancy and inventory commitments before qualifying new EO IR systems. Airborne systems remain the strongest revenue pool because targeting pods, stabilized ISR turrets, drone payloads and missile warning systems carry high optical value per unit. Land and naval adoption are accelerating faster because counter-UAV missions require passive detection, thermal tracking and operator confirmation without emitting radar energy. Border agencies and coastal forces are also moving from single thermal cameras to integrated day-night thermal laser systems that can share tracks with command networks.

Defense Electro-Optical and Infrared (EOIR) Systems Industry Trends and Strategic Insights

- Counter-UAV fire control is pushing compact thermal imagers from observation roles into engagement chains where frame rate, latency and target handoff matter as much as detection distance.

- Open architecture payloads are gaining priority because defense ministries want to refresh detectors, processors and software without replacing the full turret or aircraft integration kit.

- Germanium supply risk is encouraging suppliers to qualify chalcogenide glass and hybrid lens designs for selected LWIR optics where performance requirements allow substitution.

- AI-assisted target recognition is increasing demand for stable image quality, accurate calibration and edge processing inside the sensor head rather than delayed processing at a remote station.

- Uncooled thermal cores are moving into more soldier, vehicle and small UAV roles while cooled MWIR systems remain preferred for long-range targeting, shipborne search and high altitude ISR.

- European and Asian defense buyers are asking for local maintenance, repair and optical alignment capability because depot bottlenecks now influence operational readiness during high-tempo deployments.

Market Scope

| Metrics | Details | |

| 2025 Market Size | US$ 8.95 Billion | |

| 2035 Projected Market Size | US$ 15.43 Billion | |

| CAGR (2026-2035) | 5.6% | |

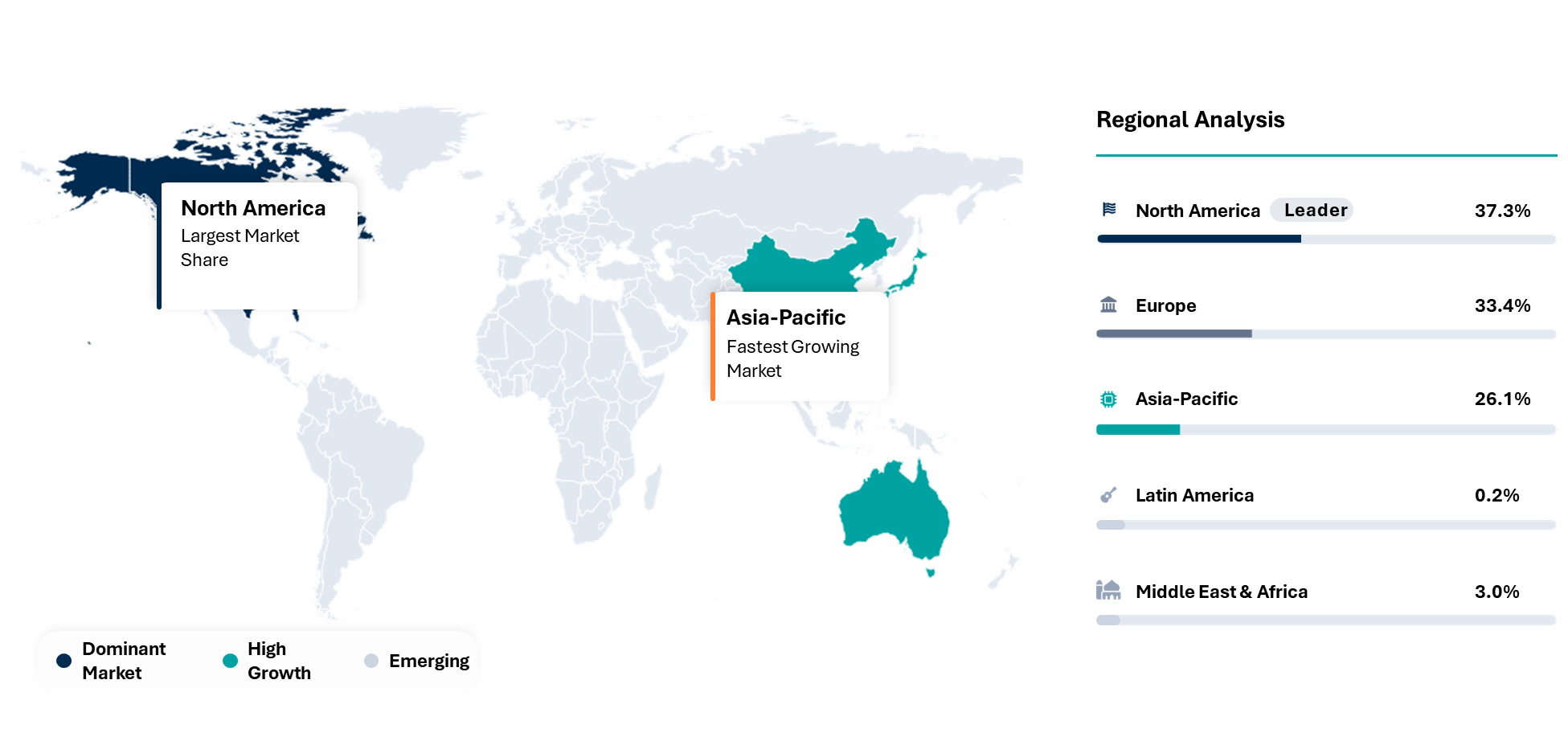

| Largest Market | North America | |

| Fastest Growing Market | Asia-Pacific | |

| By IR Optics | MWIR Lenses, LWIR Lenses, SWIR Optics, Germanium Optics, Chalcogenide Glass Optics, Optical Domes And Windows, Filters And Coatings, Others | |

| By Night Vision Optics EO | Image Intensifier Compatible Optics, Digital Low Light Optics, Visible And NIR Day Night Optics, Helmet Mounted And Weapon Sight Optics, Laser Rangefinder Integrated Optics, Others | |

| By Microlens Fabrication | Wafer Level Microlens Arrays, CMOS And InGaAs Sensor Microlenses, Uncooled Microbolometer Microlenses, Detector Coupling Microlenses, Custom Military Sensor Microlens Arrays, Others | |

| By IR Thermography Optics | Calibrated Thermal Camera Optics, Maintenance And Condition Monitoring Optics, Target Heat Signature Imaging Optics, Uncooled Thermography Lens Assemblies, Cooled Thermography Lens Assemblies, Others | |

| By Spectral Band | Visible, NIR, SWIR, MWIR, LWIR, Multispectral, Hyperspectral | |

| By Cooling Architecture | Cooled, Uncooled, Hybrid Cooled and Uncooled | |

| By System Format | Stabilized Turrets, Targeting Pods, Handheld Imagers, Weapon Sights, Vehicle Sights, Shipborne Sensors, Fixed Surveillance Towers, Space Payload Optics | |

| By Platform | Fixed Wing Aircraft, Rotary Wing Aircraft, UAVs, Armored Vehicles, Air Defense Systems, Naval Vessels, Ground Robots, Soldier Systems, Border Towers | |

| By Mission Use | ISR, Target Acquisition, Fire Control, Missile Warning, Counter UAV, Border Surveillance, Maritime Domain Awareness, Search and Rescue, Maintenance Thermography | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

Strategic Indicators For Defense Electro-Optical and Infrared (EOIR) Systems

High Regulation Impact

Regulation has a high impact because many defenses optical components sit inside dual use export control regimes. Thermal cameras, infrared lenses, cooled detectors, image intensifier components, lasers and stabilized payloads can serve military and civilian roles. Export approvals therefore affect lead times, customer eligibility, after sales servicing and re-export permissions. U.S. International Traffic in Arms Regulations, Export Administration Regulations, EU dual use rules and national licensing frameworks can restrict movement of complete systems and sensitive subcomponents. China’s gallium and germanium controls also show how raw material policy can influence optical supply. Suppliers with strong compliance teams, country specific product variants and documented end user controls gain an advantage. Smaller optics manufacturers often face slower approvals and higher legal cost when defense customers request customized performance.

High Investment Activity

Investment activity is high because armies, navies and air forces are adding passive sensing to counter drone, air defense and ISR networks. Radar remains essential, but optical confirmation is now required to classify small targets, reduce false alarms and support rules of engagement. Funding is visible in aircraft targeting pod upgrades, naval panoramic sensing, border towers, land vehicle sights and compact payloads for tactical UAVs. Japan’s defense buildup, India’s capital procurement push and European investment growth all support demand for survivable night and thermal vision. Capital is moving into both prime integrators and upstream optics. Microlens fabrication, wafer-level packaging, low SWaP optics, cryogenic cooler reliability and AI-ready calibration have become attractive investment themes for strategic buyers and defense-focused private capital.

Supply Chain Disruption

Supply disruption is concentrated in germanium, gallium, optical coatings, cooled detector packaging and precision gimbal components. Military buyers cannot easily substitute these parts after qualification because changes affect calibration, environmental testing, export classification and platform integration.

China’s export controls on gallium and germanium-related products increased the perceived risk around infrared optics. Even when material remains available through licensing, buyers may hold more inventory or redesign lenses to reduce dependence on a single source. Supply chain resilience now shapes vendor selection. Companies with in-house detector assembly, optics polishing, coating, software and MRO capacity can make stronger readiness claims than assemblers dependent on external bottlenecks.

Pricing Volatility

Pricing volatility is high because the bill of materials contains scarce optical materials and precision electromechanical parts. Germanium lenses, diamond-like carbon coatings, cryocoolers, high-sensitivity detectors and stabilized housings can represent a large share of payload cost. Thermal optics pricing also moves with qualification burden. A lens that performs in commercial thermography may not meet shock, vibration, humidity, salt fog and transmission stability requirements for military platforms. Defense-grade testing adds cost and extends production cycles. Vendors are responding through multiyear purchase agreements, alternative lens materials, modular upgrades and service bundles. Price competition exists but buyers usually avoid the cheapest qualified bid when failure would reduce mission readiness.

Procurement Pressure

Procurement pressure is rising because small drones, loitering munitions and low signature targets evolve faster than traditional defense qualification cycles. Forces need new optical payloads quickly yet platform integration, environmental testing and export approvals can take years. Military customers increasingly ask suppliers to prove rapid delivery, field upgrade paths and software refresh capability. Payloads must also connect to existing command networks without expensive vehicle or aircraft rewiring. The pressure favors open systems, modular turrets and common optical cores that can be adapted across platforms. Suppliers unable to shorten qualification or support urgent spares may lose share even when core optics are technically strong.

New Technology Adoption

New technology adoption is strongest around AI-ready image processing, multispectral fusion, digital stabilization, wafer-level microlenses and compact high-precision optics. Smaller unmanned platforms need lighter payloads without sacrificing identification performance. Microlens fabrication is becoming more important because high-density focal plane arrays and miniaturized sensors need precise light collection across small pixels. Uniformity and low defect rates matter because AI models depend on consistent imagery. Adoption will not be uniform. Premium cooled MWIR systems will lead long-range targeting while uncooled LWIR and digital night vision will expand in soldier, vehicle and fixed surveillance roles were cost and power consumption matter more.

Regional Expansion Opportunity

Regional expansion opportunity is strongest where defense budgets are rising, but local optical repair capacity remains thin. India, Japan, Türkiye, Saudi Arabia, UAE, Poland and South Korea are good examples because each is trying to deepen domestic defense production. Suppliers can win by establishing lens cleaning, calibration, turret repair, gimbal alignment and software support inside the customer region. Local support reduces downtime and helps ministries justify premium systems in readiness terms. Partnership models must be carefully designed because many optical designs are export-controlled. Successful expansion will use tiered technology transfer, licensed assembly and controlled access to sensitive calibration procedures.

Government Policy Support

Government policy support is visible through rising defense investment, domestic procurement quotas and national security rules around critical materials. India allocated Rs 6,81,210.27 crore to the Ministry of Defense for FY 2025 to 2026 and earmarked Rs 1.12 lakh crore for procurement from domestic industries. European defense investment exceeded EUR 100 billion in 2024 according to EDA reporting and Japan’s FY2025 budget document frames spending around the country’s most severe and complex security environment since World War II. Policy support does not only mean higher budgets.

Defense ministries are also shaping how systems are sourced. Local content, trusted foundries, secure software, maintenance sovereignty and allied supply chains are becoming decision factors. Optical suppliers that can prove trusted production and repair capability gain a stronger position in tenders. A practical opportunity sits in national optical centers of excellence. Canada, Türkiye, India, Japan and several European states are trying to localize enough capability to support deployed fleets. Joint ventures around coatings, gimbals, optics assembly and depot repair can create durable market access without transferring the most controlled detector or algorithm content.

Import Export And Pricing Intelligence

A single customs code does not cleanly capture defense EO IR systems because finished payloads may ship as cameras, optical instruments, aircraft parts or weapon system components depending on configuration and destination. Practical trade screening should therefore track HS 9002 for mounted lenses, prisms, mirrors and optical elements, HS 9001 for optical fibers and unmounted optical elements, HS 8525 for television cameras and imaging equipment and HS 9013 for liquid crystal devices, lasers and other optical appliances where relevant.

UN Comtrade describes its database as a global platform for detailed annual and monthly trade statistics by product and trading partner. For optical elements under HS 9002, the Observatory of Economic Complexity identifies China, the U.S. and the Netherlands among the leading importers. Defense analysts should treat such data as directional rather than a direct market proxy because military payloads can be classified or bundled inside larger platform deliveries.

| HS Code | Reporter | Trade Flow | 2025 Trade Value | Interpretation |

| HS 902750 | United States | Export | USD 2.4 Billion | Strong export leadership in advanced infrared imaging, military optics and sensing assemblies |

| HS 902750 | Israel | Export | USD 0.75 Billion | Israel's precision electro-optics manufacturing hub supporting NATO defense supply chains |

| HS 902750 | UK | Export | USD 0.61 Billion | One of the key suppliers of optics-related electronic assemblies and infrared component inputs |

| HS 902750 | Japan | Export | USD 0.51 Billion | High-value exporter of precision optical elements and defense-grade infrared materials |

| HS 902750 | USA | Import | USD 1.5 Billion | Rising imports linked to indigenous defense modernization and ISR procurement expansion |

Pricing intelligence should combine customs data with material risk indicators. Germanium export licensing, detector lead times, cryocooler availability and coating capacity can shift price faster than finished system demand. Contracts with local assembly or long-term spares also carry higher upfront prices but often lower downtime risk for defense forces.

Company Coverage Preview

L3Harris Technologies Inc. has one of the strongest visible positions in the global defense EO IR market through its WESCAM MX family. The company benefits from a broad installed base across airborne, land and maritime platforms and a product architecture that has become familiar to military operators, integrators and procurement teams. WESCAM MX systems are promoted as multi-sensor and multispectral payloads for ISR, surveillance, targeting and target acquisition missions across several domains.

The company reached a dominant position by combining optical performance with platform integration and mission software. Stabilized turrets require more than lenses and cameras. Customers need gimbal reliability, image processing, software tools, laser options, platform mounting, export documentation and training. L3Harris has built credibility by serving manned aircraft, unmanned aircraft, helicopters, land vehicles and maritime assets, which supports reuse of technology across programs.

Key USPs include broad mission fit, modular payload families, advanced image processing, global support and compatibility with allied procurement patterns. Recent positioning around WESCAM mission software and counter-unmanned systems integration shows that the company is moving beyond hardware refresh cycles toward operational workflow value.

AI Impact Analysis

AI is shifting the market from operator-interpreted imagery toward assisted recognition, tracking and prioritization. Optical payloads now need clean metadata, stable calibration, low-latency video and consistent image quality so algorithms can detect small drones, vehicles, people, muzzle flashes or missile plumes with fewer false alarms. The sensor head is becoming a computing node instead of a passive camera. Edge AI changes hardware priorities. Processors inside turrets must survive heat, vibration and power limits while running detection models near real time.

Optical quality becomes more valuable because AI cannot fully compensate for poor focus, lens distortion, thermal nonuniformity or unstable gimbal motion. Microlens fabrication and detector uniformity, therefore, influence algorithm performance even when they are not visible to procurement teams. Human oversight remains central in lethal and politically sensitive missions. Defense buyers are likely to use AI first for cueing, prioritizing and reducing operator workload rather than fully autonomous target engagement. Vendors that can show audit trails, explainable detections, cyber hardening and controlled software updates will be better positioned for regulated deployments.

Disruption Analysis

Small UAV warfare has disrupted the traditional hierarchy of defense optics. High-end aircraft targeting pods still command premium pricing but ground forces now need many more affordable thermal and night systems at platoon, vehicle, base and air defense levels. Quantity requirements are moving faster than legacy procurement cycles and are forcing ministries to balance exquisite long-range performance with deployable volume. Material geopolitics is the second disruption. Germanium and gallium controls, semiconductor restrictions and sanctions risk have made supply chain origin a technical procurement criterion.

Military customers want to understand where lenses are grown, polished, coated, assembled and serviced. A high-performance system can lose preference if its critical optical material or detector source looks vulnerable during a crisis. Software-defined sensing creates another disruption. RTX’s RAIVEN positioning around hyperspectral sensing, lidar and AI, L3Harris’ software enabled WESCAM messaging and HENSOLDT’s AI-powered surveillance claims point toward payloads that improve after deployment. Procurement models may evolve from fixed hardware purchases to capability upgrades, algorithm refreshes and mission-specific software licenses.

BCG Matrix: Company Evaluation

STAR

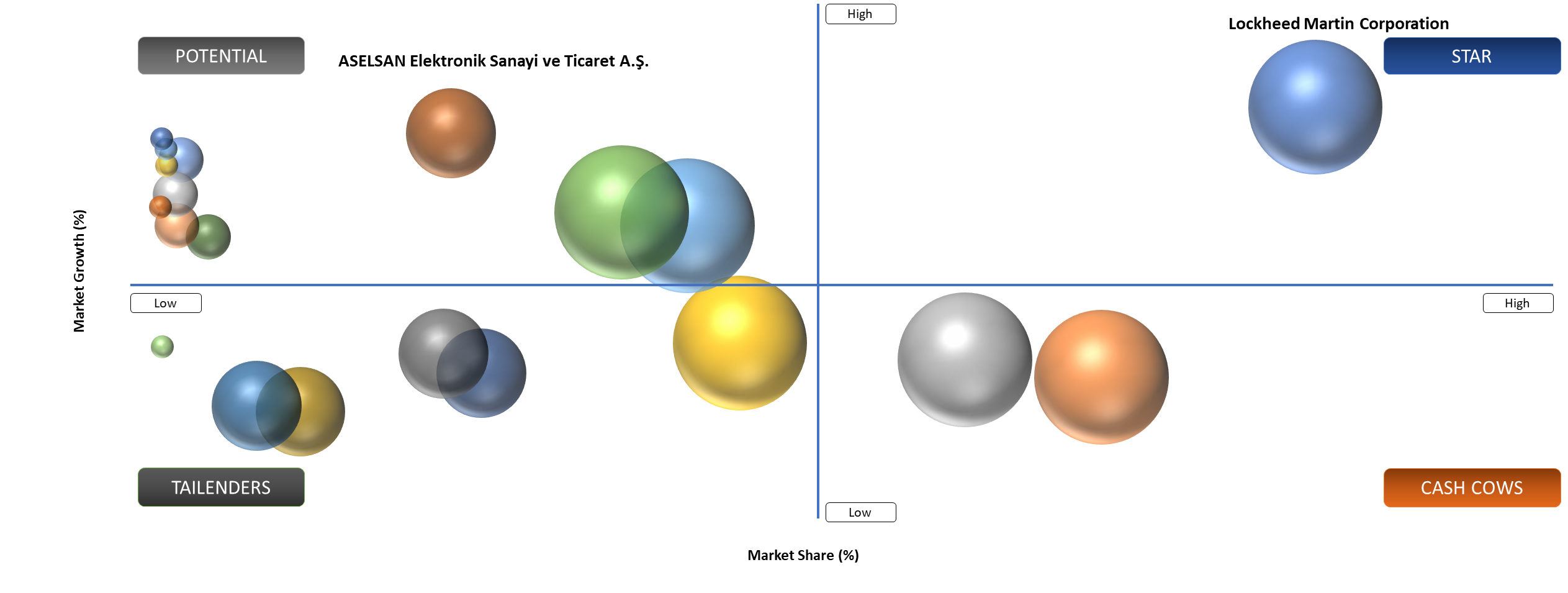

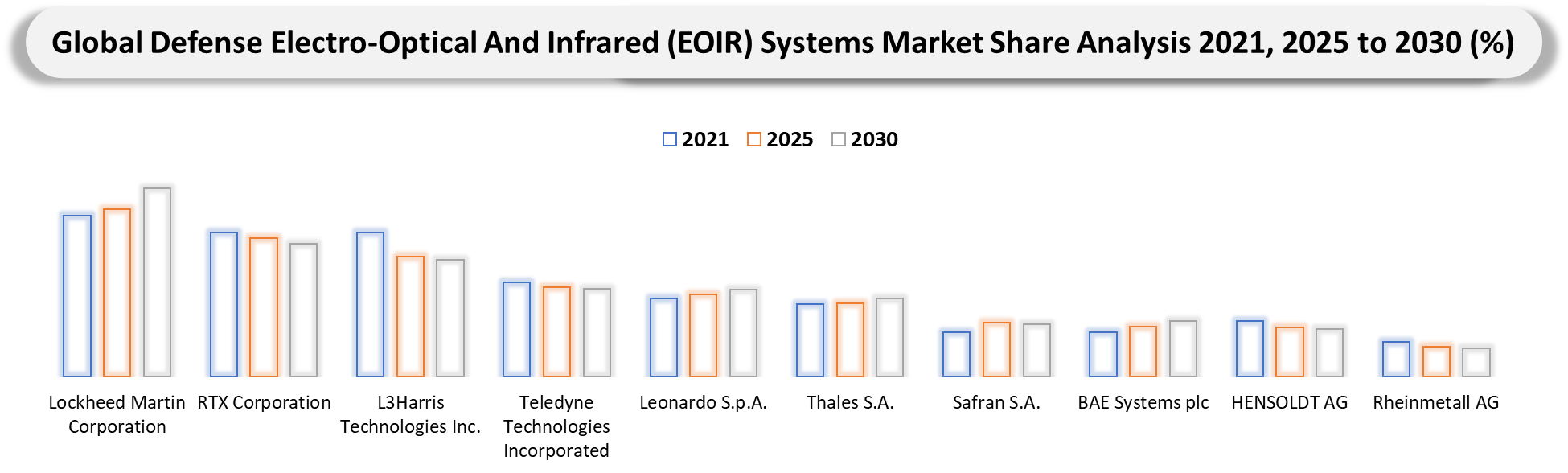

L3Harris Technologies Inc., RTX Corporation, Lockheed Martin Corporation, Teledyne Technologies Incorporated and Leonardo S.p.A. sit in the Stars quadrant because they combine proven defense programs, wide platform integration, strong optical engineering and large installed bases. L3Harris has clear visibility through WESCAM MX systems across air, land and maritime missions. RTX is pushing RAIVEN into next-generation sensing with AI and multi-phenomenology. Lockheed Martin retains major relevance through F-35 infrared sensor systems and broader targeting architecture. Teledyne FLIR is strong in thermal modules and defense imaging scale. Leonardo benefits from detectors, optronics and land platform integration. The strategic pattern across these companies is not just market share. Each controls a mix of hardware, software, qualification history and customer trust that is difficult for smaller payload providers to replace quickly.

POTENTIAL

ASELSAN Elektronik Sanayi ve Ticaret A.Ş., HENSOLDT AG, Elbit Systems Ltd., Israel Aerospace Industries Ltd., CONTROP Precision Technologies Ltd. and Kongsberg Gruppen ASA sit in the Potential quadrant because they are benefiting from faster regional defense modernization, UAV payload demand and counter-UAV adoption. ASELSAN is scaling ASELFLIR systems through Türkiye’s fast-growing drone ecosystem. HENSOLDT benefits from European sensing sovereignty and optronics depth. Elbit and IAI have strong compact payload portfolios for UAV, maritime and land roles. CONTROP has a focused EO payload niche across defense and homeland security. Kongsberg’s NASAMS-linked EO sensor relevance improves as passive confirmation becomes more important in air defense networks. Growth depends on export permissions, production scaling and the ability to offer local support outside home markets.

Market Dynamics

Counter UAV Warfare Is Turning Passive Thermal Tracking Into A Frontline Requirement

Small drones have changed the value of passive sensing. Radar can detect many threats but optical confirmation is essential when commanders need to classify a quadcopter, fixed-wing UAV, bird, decoy or loitering munition before engagement. Thermal imaging and daylight cameras also provide visual evidence after an interception or failed intercept.

Counter UAV missions create demand across several optical layers. Fixed towers need wide area thermal surveillance. Vehicles need stabilized sights. Air defense teams need sensors linked to fire control. Soldiers need handheld thermal devices for local awareness. Naval forces need passive tracking for low-flying drones and fast boats that can appear inside crowded coastal backgrounds.

It is especially strong because low-cost UAV threats multiply faster than premium air defense assets. Defense forces, therefore, need scalable EO IR coverage around bases, convoys, depots, ships and border posts. Optical systems that combine low-latency tracking, AI cueing, laser range finding and network handoff will capture a larger share of urgent procurement.

Critical Infrared Materials And Export Licensing Create Uncomfortable Lead Time Risk

Infrared optics relies on materials and processes that cannot be rapidly expanded. Germanium, chalcogenide glass, precision diamond turning, coating chambers, cooled detector packaging and cryocooler production all require specialized capacity. Shortages can delay finished payload delivery even when system integrators have a strong demand.

Export licensing can also slow cross-border delivery. A customer may approve a system technically but final shipment still depends on end-user documentation, re-export rules and national security reviews. After-sales repair can face similar hurdles when a controlled component must return to the manufacturer. The restraint is not a simple cost issue. Defense users must keep fleets operational during periods when trade policy may change suddenly. Procurement teams are therefore demanding alternate sources, local MRO and larger spares packages. Suppliers unable to provide supply assurance will face tougher negotiations and longer qualification cycles.

Segment Analysis

The global defense electro-optical and infrared (EOIR) systems market is segmented based on the IR optics, night vision optics EO, microlens fabrication, IR thermography optics, spectral band, cooling architecture, system format, platform, mission use and region.

Cooled MWIR And LWIR Assemblies for Long-Range Targeting

Cooled MWIR and LWIR assemblies are the backbone of long-range target acquisition, maritime surveillance and aircraft ISR. Cooled detectors provide higher sensitivity and better performance against small temperature differences, which matters when identifying vehicles or boats at long distances.

Airborne targeting pods, shipborne search systems and vehicle commander sights often justify cooled optics despite higher cost because mission failure is expensive. Lens materials, cryogenic stability, gimbal pointing accuracy and embedded image processing need to work as a system.

Growth is strongest where forces are upgrading aircraft, drones and air defense networks. Long-range stand-off missions require imagery that can support classification, coordinates and engagement decisions without exposing the platform.

Uncooled LWIR Optics For High Volume Tactical Deployment

Uncooled LWIR optics are expanding because they fit the cost and weight limits of small drones, soldier devices, remote weapon stations and perimeter cameras. Lower power draw and simpler maintenance make them practical for distributed deployment.

Performance has improved enough for many tactical missions, although cooled systems still dominate long-range identification. Defense buyers increasingly use uncooled devices to create wide coverage and reserve cooled payloads for critical identification or targeting tasks. Suppliers that can manufacture rugged molded chalcogenide lenses, athermalized optics and compact assemblies will benefit from volume demand. Scale matters because tactical users may need hundreds or thousands of devices rather than a small number of premium payloads.

Geographical Penetration

U.S. Defense Electro-Optical and Infrared (EO-IR) Systems Market Landscape

The United States remains the global technology leader in defense electro-optical and infrared systems due to sustained Pentagon investments in ISR modernization, counter-UAS systems, missile warning architectures and multi-domain battlefield awareness. The U.S. Department of Defense is accelerating deployment of advanced EOIR payloads across airborne, naval and land-based platforms as geopolitical tensions in the Indo-Pacific and Eastern Europe intensify. In 2025, the U.S. Navy continued procurement activity for MX-15 EO/IR sensor systems through the Naval Air Warfare Center to support airborne surveillance operations, reflecting continued demand for high-performance targeting and reconnaissance payloads.

Simultaneously, the Defense Innovation Unit expanded counter-UAS sensing initiatives focused on homeland and mobile defense applications, highlighting growing operational dependence on AI-enabled infrared detection and persistent surveillance technologies. U.S. defense contractors, including L3Harris Technologies, RTX Corporation and Lockheed Martin, are integrating thermal imaging, multispectral targeting and long-range IR sensors into next-generation missile defense and autonomous combat systems.

Japan Defense Electro-Optical and Infrared (EOIR) Systems Market Outlook

Japan is rapidly expanding its defense EOIR capabilities as part of its historic military modernization strategy aimed at countering regional threats from China, North Korea and maritime incursions in the East China Sea. The Japanese Ministry of Defense has significantly increased investments in ISR systems, autonomous surveillance platforms, coastal monitoring sensors and integrated missile defense architectures.

The SHIELD defense initiative specifically prioritizes networks of unmanned air, sea and underwater systems equipped with advanced electro-optical and infrared payloads for persistent island monitoring and rapid threat identification. Japanese defense manufacturers such as Mitsubishi Electric and NEC Corporation are expanding development of infrared seekers, thermal imaging systems and long-range optical surveillance technologies for missile interception and maritime reconnaissance missions.

North America And U.S. Defense Optical Modernization

North America remains the largest market because the U.S. funds a broad mix of aircraft targeting pods, missile warning systems, naval sensors, counter UAV systems, soldier devices and space sensing programs. U.S. procurement also influences allied buying because many systems need interoperability with American platforms and command networks.

U.S. demand is shifting toward multi-sensor architecture. Targeting pods are being upgraded for higher resolution, unmanned systems require lighter payloads and bases need counter-drone surveillance. The FY2026 U.S. defense budget materials and service budget documents show continued emphasis on sensors, unmanned systems, aerospace capabilities and Pacific deterrence priorities.

Industrial depth gives the U.S. a strong base in detectors, cooled sensors, thermal modules, gimbals and software. Supply risk remains real because germanium and gallium chains are globally exposed. U.S. agencies and contractors are therefore paying more attention to trusted foundries, domestic optics and allied sourcing.

Canada is important through Arctic surveillance, naval modernization and industrial participation linked to allied defense programs. Mexico is smaller, but border security and critical infrastructure protection create limited demand for thermal surveillance systems.

Europe Defense Optical Rebuild Around Readiness And Local Sovereignty

Europe is moving from low inventory peacetime procurement to readiness-centered buying. Higher defense investment across EU members is translating into air defense, land systems, ammunition, drones and surveillance. EO IR systems are benefiting because every modern platform needs passive sensing and night operation capability.

Germany, France, UK, Italy and Poland are especially relevant. Germany has strong optronics capability through HENSOLDT, Rheinmetall and Jenoptik. France has Thales and Safran. UK demand is shaped by land modernization, naval systems and aircraft upgrades. Poland is building ground force capacity at speed and will need sights, thermals and sensor sustainment.

European buyers also want resilience within the region. The European Critical Raw Materials Act and defense industrial policy are encouraging domestic processing, recycling and strategic projects for critical materials. Germanium and advanced optics are part of the broader security discussion, even when procurement documents do not always name them directly.

Local MRO will become a decisive commercial lever. European armed forces are trying to avoid long overseas repair cycles and are likely to reward suppliers that can calibrate, align and repair sensor heads close to operational units.

Asia Pacific Expansion Led By Japan, India, China And South Korea

Asia Pacific is the fastest growing region because maritime disputes, border tensions, missile threats and drone adoption are driving rapid modernization. The region has large platform fleets and rising domestic manufacturing ambitions, which create demand for both complete EO systems and upstream optics.

Japan deserves separate attention. The Ministry of Defense FY2025 budget states that Japan faces its most severe and complex security environment since the end of World War II. Spending priorities around unmanned systems, stand-off defense, maritime awareness and island defense support demand for passive sensors, thermal payloads and optical repair capacity.

India is building domestic defense production while maintaining strong import demand for advanced sensors. The FY2025 to 2026 defense allocation and domestic procurement earmark support local supply chains. EO IR demand spans UAVs, helicopters, armored vehicles, border surveillance and naval platforms. Indian buyers will favor suppliers that can localize assembly or create qualified Indian partners. China has strong domestic production in optics, drones, cameras and military electronics. It is both a major supply source and a strategic competitor in advanced sensing. South Korea, Australia, Indonesia and Malaysia provide additional growth through naval, border and air defense modernization.

Competitive Landscape

The competitive landscape is concentrated at the prime and tier one level but fragmented across optical components. Lockheed Martin, RTX, L3Harris, Teledyne FLIR, Leonardo, Thales, Safran, Northrop Grumman and BAE Systems compete around major programs and platform integrations. HENSOLDT, Rheinmetall, ASELSAN, Elbit, IAI, Rafael, CONTROP, Kongsberg, Bertin and Jenoptik add regional strength and specialist capability.

- Differentiation is built around range performance, image quality, stabilization, SWaP, software, integration history and service network. Product pages from L3Harris, RTX, Leonardo, Thales, HENSOLDT, Rheinmetall and Elbit show similar language around multi-sensor payloads, real-time imagery, laser integration and day-night operation. Real competitive separation often comes from exportability, upgrade path and field support rather than a single optical metric.

Upstream optics companies are gaining more strategic value. Lens fabricators, coating houses, microlens specialists and detector packagers influence the performance of finished systems and the resilience of military supply chains. Acquisition interest is likely to remain high where a component supplier provides controlled know-how, qualified production capacity or access to restricted materials.

MAJOR PAIN POINTS

- Critical Material Exposure: Germanium, gallium compounds and specialty glasses create cost and continuity risk for infrared optics suppliers.

- Qualification Bottlenecks: Military environmental testing can slow product refreshes even when commercial optics evolve quickly.

- Export Control Complexity: Every controlled detector, laser, lens or payload may need country-specific licensing and end-user checks.

- Repair Cycle Pressure: Deployed forces need fast calibration, window replacement and gimbal repair, but local MRO capacity is often limited.

- Software Integration Burden: Customers increasingly expect sensors to connect with C2 networks, AI tools and weapon systems.

- Counterfeit And Grey Market Parts: Low-quality optical components can damage brand trust and create mission risk.

- Skilled Labor Shortage: Precision polishing, coating, alignment and cryogenic integration require hard-to-replace technicians.

- Thermal Calibration Drift: Field performance can degrade when optics face heat, vibration and harsh weather over long deployments.

- Demand Spikes From Conflict: Urgent procurement creates capacity strain and can crowd out smaller customers.

Price Pressure In Tactical Systems: High volume soldier and drone optics face stronger cost pressure than premium aircraft payloads.

KEY DEVELOPMENTS

- May 2026: Lockheed Martin Corporation secured U.S. Space Force layered missile-defense contracts supporting advanced space-based EOIR interceptor capabilities and homeland defense modernization.

- April 2026: L3Harris Technologies Inc. reported increased international defense-program volumes, accelerating deployment of advanced EOIR payloads, ISR sensors and mission-system integration capabilities.

- April 2026: RTX Corporation completed first RAIVEN EOIR sensing-system Black Hawk flight-test, enhancing battlefield situational-awareness, autonomous target-tracking and survivability performance.

- August 2025: ASELSAN Elektronik Sanayi ve Ticaret A.Ş. expanded indigenous EOIR targeting-system production, supporting Türkiye’s UAV modernization, border-surveillance and precision-guided defense mission requirements domestically.

- December 2025: Northrop Grumman Corporation advanced distributed EOIR sensing technologies supporting missile-warning architectures, space-based tracking and integrated multi-domain defense-surveillance modernization programs globally.

- November 2025: Rheinmetall AG strengthened battlefield electro-optical reconnaissance capabilities through integrated soldier-systems, vehicle-vision technologies and next-generation thermal-imaging modernization programs internationally.

- October 2025: HENSOLDT AG advanced passive-radar and optronic sensor integration capabilities supporting European air-defense modernization and multi-sensor battlefield situational-awareness enhancement initiatives.

- September 2025: General Atomics integrated upgraded EOIR payloads into unmanned aerial platforms, improving persistent ISR, autonomous tracking and precision-strike operational effectiveness worldwide.

- September 2025: BAE Systems plc expanded infrared countermeasure and multispectral targeting technologies supporting next-generation combat-aircraft survivability and precision-targeting modernization requirements globally.

July 2025: Elbit Systems Ltd. enhanced airborne EOIR payload offerings supporting autonomous ISR operations, precision-targeting missions and next-generation tactical reconnaissance deployments across allied militaries.

ANALYST VIEW / OPINION

- The market is moving from a platform accessory mindset to a battlefield visibility infrastructure mindset. Optical payloads now sit inside counter-drone, air defense, naval protection, border surveillance and autonomous system workflows. Buyers will not simply purchase more cameras. It will provide faster detection, better classification, lower false alarms and higher availability.

- DMI opinion is that supply assurance will become as important as sensor range by 2030. A vendor with a slightly lower range but reliable materials, local repair and export clarity may beat a technically superior product that depends on fragile critical minerals or overseas depot repair. It is especially true for land and fixed surveillance users who need many systems operating every day.

- DMI's opinion is also that microlens fabrication and IR optics deserve deeper coverage than most broad EO IR studies provide. The next wave of AI-enabled sensing will depend on uniform, machine-readable imagery. Upstream optical quality will therefore shape downstream software performance, making component suppliers more strategically relevant to primes, investors and defense ministries.

TARGET AUDIENCE

| INDUSTRY | WHO SHOULD BUY THIS REPORT? | REASON TO BUY THIS REPORT |

| Defense Prime Contractors | Strategy, capture, product management and partnerships teams | Benchmark EO IR portfolios, target regional partners and assess optical supply risks. |

| Optics And Lens Manufacturers | Commercial leaders, R&D heads and export compliance teams | Identify demand pockets for IR optics, night vision optics, microlenses and thermography optics. |

| Thermal Camera And Detector Suppliers | Product strategy, sales and program teams | Understand platform demand, cooling choices and long-term procurement direction. |

| Defense Ministries And Procurement Agencies | Capability planners, acquisition teams and sustainment offices | Evaluate supplier readiness, localization opportunities and life cycle support requirements. |

| UAV And Counter UAV Integrators | Payload engineers, business development teams and systems architects | Map sensor requirements for passive detection, tracking and engagement support. |

| Naval And Border Security Agencies | Technology evaluation, operations and procurement teams | Assess thermal surveillance, maritime tracking and coastal monitoring options. |

| Private Equity And Strategic Investors | Industrial technology investors and M&A teams | Screen acquisition opportunities in optics, coatings, gimbals, detectors and MRO. |

| Consulting And Advisory Firms | Defense, aerospace and industrial consultants | Support market entry, competitive benchmarking and investment due diligence. |

| Critical Material Suppliers | Commercial and supply chain teams | Understand how germanium, gallium and specialty glass risk affects optical demand. |

| MRO And Calibration Providers | Service network leaders and regional operators | Identify local depot opportunities for high-value sensor fleets. |

WHY CHOOSE DATAM?

- Data-Driven insights: Dive into detailed analyses with granular insights such as pricing, market shares and value chain evaluations, enriched by interviews with industry leaders and disruptors.

- Post-Purchase Support and Expert Analyst Consultations: As a valued client, gain direct access to our expert analysts for personalized advice and strategic guidance, tailored to your specific needs and challenges.

- White Papers and Case Studies: Benefit quarterly from our in-depth studies related to your purchased titles, tailored to refine your operational and marketing strategies for maximum impact.

- Annual Updates on Purchased Reports: As an existing customer, enjoy the privilege of annual updates to your reports, ensuring you stay abreast of the latest market insights and technological advancements. Terms and conditions apply.

- Specialized Focus on Emerging Markets: DataM differentiates itself by delivering in-depth, specialized insights specifically for emerging markets, rather than offering generalized geographic overviews. The approach equips our clients with a nuanced understanding and actionable intelligence that are essential for navigating and succeeding in high-growth regions.

- Value of DataM Reports: Our reports offer specialized insights tailored to the latest trends and specific business inquiries. The personalized approach provides a deeper, strategic perspective, ensuring you receive the precise information necessary to make informed decisions. The insights complement and go beyond what is typically available in generic databases.

WHAT DATAM UNIQUELY PROVIDES

- DataM can provide a market view that links optical scope, platform procurement and upstream supply risk in one model. Standard market reports often describe EO IR systems as a single category. A more useful client view separates IR optics, night vision optics, microlens fabrication and IR thermography optics because each has different suppliers, lead time risk and pricing behavior.

- DataM can also map product-level evidence from official manufacturer pages to defense procurement logic. That means connecting WESCAM, RAIVEN, LITENING, SOPHIE, ARGOS, SEOSS, ASELFLIR, MOSP and Micro Compass style products with mission roles, optical bands, cooling choices and service requirements. Such mapping helps clients identify where a company truly competes instead of relying on broad corporate descriptions.

- DataM’s differentiated value sits in sizing feasibility and commercial usability. The study can combine customs proxies, defense budget signals, source country risk, platform counts, product launches and local MRO opportunities. Buyers can use the report for market entry, partner identification, competitor benchmarking, procurement planning and investment screening.