Deep-Sea Mining Market Size

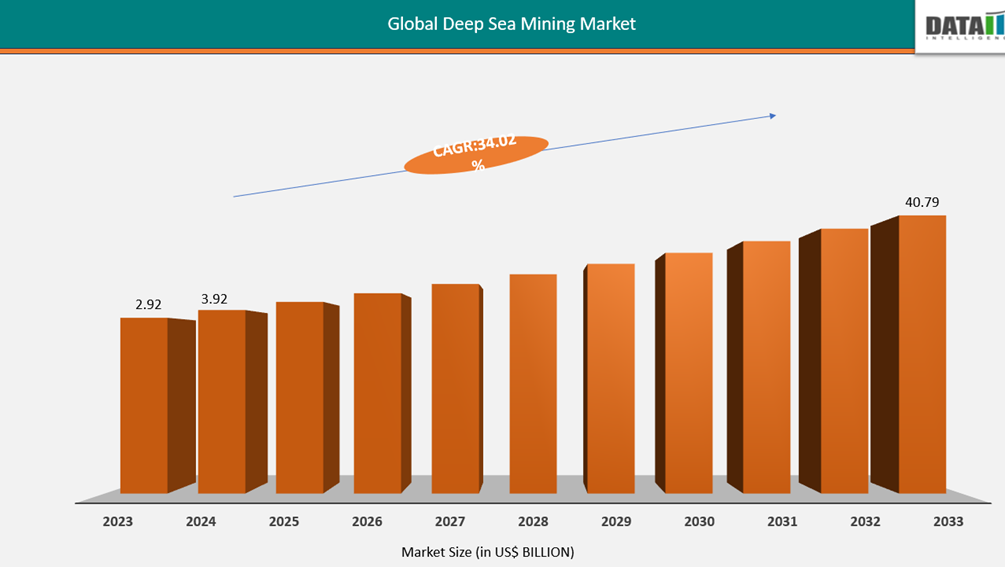

The global deep-sea mining market recorded a valuation of US$1.043 billion in 2025 and is projected to reach US$40.79 billion by 2032, reflecting a compound annual growth rate of 34.02% from 2026 to 2033.

The global deep-sea mining sector stands at a critical inflection point, driven by unprecedented demand for critical minerals essential to energy transition and technological advancement. The International Seabed Authority (ISA) has issued 31 exploration contracts covering approximately 1.5 million square kilometers of international seabed as of 2024, representing a substantial increase from just 8 contracts in 2010. These contracts span across the Clarion-Clipperton Zone in the Pacific Ocean, the Indian Ocean, and the Mid-Atlantic Ridge, signaling intensifying commercial interest in subsea mineral resources.

The industry's momentum derives primarily from the acute shortage of battery-grade metals critical to electric vehicle manufacturing and renewable energy storage systems. According to the International Energy Agency's 2023 Critical Minerals Market Review, global demand for lithium is projected to increase by over 400 percent by 2040 under stated policy scenarios, while cobalt demand is expected to rise by 350 percent during the same period.

Deep-sea polymetallic nodules contain approximately 29 percent manganese, 1.3 percent nickel, 1.1 percent copper, and 0.2 percent cobalt by weight, according to geological surveys conducted by the U.S. Geological Survey in 2023, positioning these resources as strategically significant for meeting future mineral requirements.

Investment activity reflects this strategic importance. The Metals Company, a leading deep-sea mining developer, announced in 2023 that it had secured over $200 million in funding for its NORI-D project in the Clarion-Clipperton Zone. Similarly, China's deep-sea mining initiatives have received substantial state backing, with the China Ocean Mineral Resources Research and Development Association reportedly investing over $300 million in exploration technologies between 2020 and 2023, according to statements from the Ministry of Natural Resources.

Regulatory frameworks are simultaneously evolving to govern this emerging sector. The ISA's ongoing negotiations regarding the Mining Code have intensified following Nauru's sponsorship of The Metals Company's application to commence commercial mining in 2021, triggering the two-year rule that compelled the ISA to expedite regulatory development. As of 2024, over 20 nations have called for precautionary approaches or moratoriums, while an approximately equal number support regulated commercial exploitation, reflecting significant geopolitical divisions on industry development.

Deep- Sea Mining Industry Trends and Strategic Insights

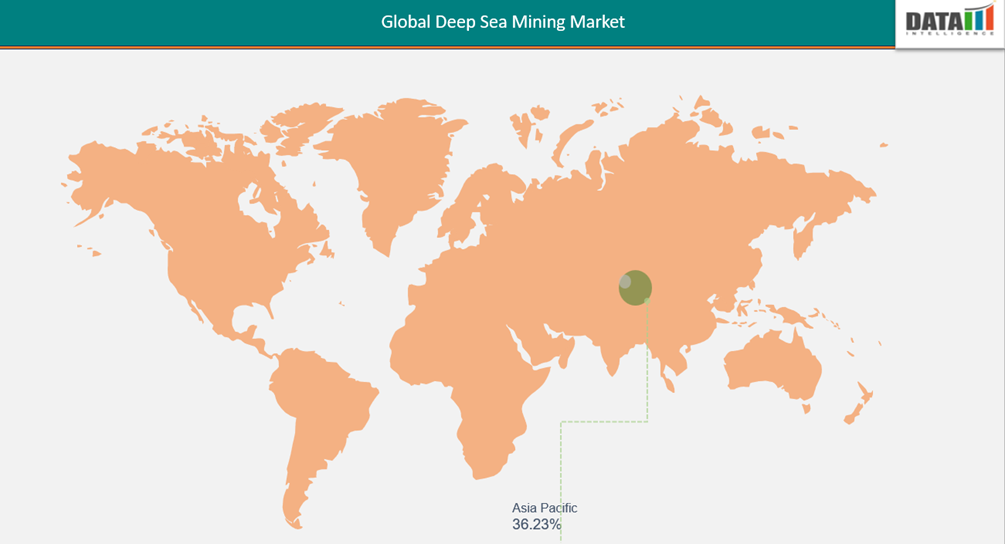

- The Asia-Pacific region leads the global Deep- Sea Mining Market, capturing the largest revenue share of 36.23 % in 2024.

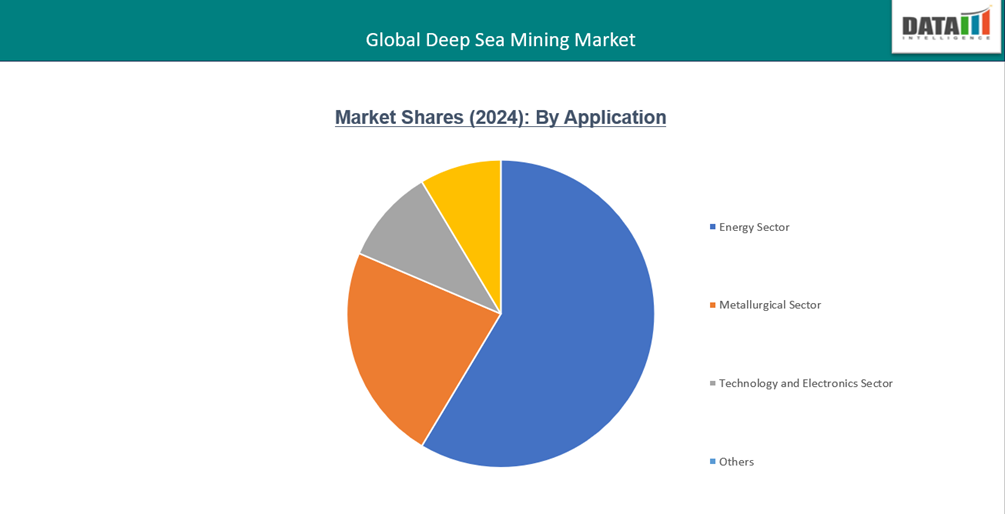

- By end-user, the Metallurgical sector dominates by largest share in the global Deep- Sea mining market

Market Size and Future Outlook

- 2024 Market Size: US$ 3.92 Billion

- 2032 Projected Market Size: US$ 40.79 billion

- CAGR (2025-2032): 34.02%

- Largest Market: Asia-Pacific

- Fastest Market: North America

Market Scope

| Metrics | Details |

By Resource Type

| Polymetallic Nodules, Polymetallic Sulphides, Cobalt-rich Ferromanganese Crusts, Others

|

| By Technology | Remote Operated Vehicles, Autonomous Underwater Vehicles, Seafloor Mining Systems, Exploration, Extraction & Collection, Others. |

| By End User | Energy Sector, Metallurgical Sector, Technology and Electronics Sector, Construction Sector, Aerospace sector

|

| By Region | North America, South America, Europe, Asia-Pacific, Middle East and Africa |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth |

Market Dynamics

Surging Demand for Battery Metals from Electric Vehicle Revolution

The global deep-sea mining market is experiencing unprecedented momentum driven fundamentally by the exponential growth trajectory of the electric vehicle industry and its insatiable appetite for critical battery metals. This transformative shift represents arguably the most significant demand catalyst the mining sector has witnessed in decades, as automotive electrification progresses from a niche segment to mainstream adoption across major economies worldwide.

The electric vehicle revolution has fundamentally altered the demand-supply equilibrium for specific metals including cobalt, nickel, manganese, and increasingly rare earth elements. Contemporary lithium-ion battery chemistries require substantial quantities of these materials, with a single electric vehicle battery pack containing approximately 8 kilograms of cobalt, 40 kilograms of nickel, and varying amounts of manganese depending on battery architecture.

As global electric vehicle sales accelerated past 14 million units in 2023 and continue projecting toward 30-40 million units annually by 2030, the multiplicative effect on battery metal requirements becomes extraordinarily pronounced. This demand trajectory is further amplified by parallel growth in stationary energy storage systems supporting renewable energy infrastructure, creating compounding pressure on mineral supply chains.

Terrestrial mining operations are demonstrably struggling to meet this escalating demand through conventional extraction methods. Existing land-based deposits face multiple constraining factors including declining ore grades, geopolitical concentration risks with over 70% of cobalt production originating from the Democratic Republic of Congo, and increasingly stringent environmental regulations in major mining jurisdictions. The expansion of new terrestrial mining operations typically requires 10-15 years from discovery to production, creating inherent supply inflexibility that cannot adequately respond to the accelerated electric vehicle adoption timelines being pursued by automotive manufacturers and policymakers alike.

Government policy frameworks are providing additional tailwinds through electric vehicle adoption mandates, internal combustion engine phase-out regulations, and critical mineral security strategies. The European Union's Critical Raw Materials Act, the United States' Inflation Reduction Act, and similar initiatives across Asia explicitly recognize the strategic importance of securing battery metal supply chains, potentially extending to supporting alternative sources including deep-sea resources as part of broader resource security objectives.

Net-Zero Goals Accelerate Deep-Sea Mineral Rush

The global shift toward clean energy is driving unprecedented demand for critical minerals like nickel, cobalt, copper, and manganese. These elements are essential for manufacturing batteries, solar panels, semiconductors, and power transmission systems. As land-based sources become strained, attention is turning to the ocean floor, where vast mineral reserves lie untapped. Deep- Sea mining offers access to these resources, positioning itself as a strategic solution for securing long-term supply. This growing interest is reshaping the market with governments and companies investing in marine exploration to meet future energy needs.

As per the instance, in 2023, the International Maritime Organization set targets to cut emissions by 40% by 2030 and achieve net-zero by 2050. As clean energy adoption accelerates, the need for critical minerals like nickel, cobalt, and copper grows sharply. These minerals are vital for low-emission technologies, making stable supply chains a global priority. Deep- Sea mining is emerging as a key source to meet this rising demand.

Uncertain Impact of Deep-Sea Mining

Deep- Sea mining poses serious risks to marine ecosystems that are still largely unknown. Areas like hydrothermal vents host rare species adapted to extreme conditions, and disturbing these zones could lead to irreversible loss. Many organisms may vanish before they’re even discovered. The long recovery time of deep-sea habitats adds to the concern. Without careful regulation, mining could permanently damage biodiversity in some of the planet’s most fragile environments

Segmentation Analysis

The global deep-sea mining market is segmented based on resource type ,technology,end-user and region

Metallurgical Sector Leads the Deep-Sea Mining Race

Metallurgical industry holds a dominant position in the deep-sea mining market, largely because of its consistent demand for metals such as nickel, copper, and cobalt. These elements are crucial in producing alloys and refining processes that support large-scale industrial operations. Their presence in seabed deposits makes ocean mining an attractive source for meeting the sector’s material needs.

For instance, in 2025, Cobalt Seabed Resources is advancing Deep- Sea exploration in the Cook Islands, targeting seabed nodules rich in cobalt, nickel, and copper. These metals are vital for metallurgical processes like alloy production, steelmaking, and non-ferrous refining. By tapping high-density deposits, CSR supports the sector’s dominance in securing long-term mineral supply amid growing global demand.

Energy Sector Drives Deep- Sea Mining Growth

Energy sector is emerging as the second fastest-growing segment. With global efforts to expand renewable energy infrastructure, demand for critical minerals used in solar panels, wind turbines, and battery storage systems is accelerating. This shift is driving increased interest in Deep- Sea mining as a strategic source for securing long-term mineral supply.

For instance, in 2025, Bahrain backed Impossible Metals in applying for an ISA exploration license in the Clarion Clipperton Zone. The project targets seabed nodules rich in cobalt, nickel, and copper key minerals for clean energy systems and metallurgical refining.

Geographical Penetration

North America

North America's engagement with deep-sea mining reflects a complex interplay of strategic resource security imperatives, technological leadership aspirations, environmental considerations, and regulatory positioning that collectively shape a distinctive regional market dynamic. The United States, Canada, and Mexico each demonstrate varying levels of commitment and activity in this emerging sector, driven by critical mineral supply chain vulnerabilities exposed during recent geopolitical disruptions and energy transition acceleration.

The United States Department of Energy's 2023 Critical Materials Assessment identified cobalt, nickel, and manganese among materials with high supply risk and high importance to clean energy technologies. This designation has catalyzed renewed American interest in deep-sea resources, particularly given that the United States currently imports 100 percent of its cobalt requirements and 47 percent of nickel consumption, according to the U.S. Geological Survey's 2024 Mineral Commodity Summaries. The strategic vulnerability became acutely apparent when cobalt prices surged 128 percent between January 2021 and May 2022 during supply chain disruptions, according to London Metal Exchange historical data.

Technological development capabilities position North America advantageously. The Massachusetts Institute of Technology's Department of Mechanical Engineering successfully tested autonomous underwater vehicle prototypes in 2023 capable of nodule identification and collection path optimization at depths exceeding 5,000 meters. The Woods Hole Oceanographic Institution deployed advanced sensor arrays in 2024 that can detect mineral deposits and simultaneously monitor sediment plume dispersion in real-time, representing critical dual-purpose technology for commercial operations. These innovations received approximately $8.5 million in combined funding from the National Science Foundation and Department of Energy between 2022 and 2024.

The regulatory environment presents both opportunities and constraints. The United States is among 36 nations party to the United Nations Convention on the Law of the Sea framework governing deep-sea mining, yet has not ratified the treaty itself, creating jurisdictional complexities. However, American companies can participate through subsidiary entities registered in signatory nations. The U.S. National Environmental Policy Act requirements would apply to any American-flagged vessels engaged in mining operations, establishing potentially stringent environmental oversight.

Asia-Pacific Powers Deep-Sea Exploration

Asia-Pacific region leads the global Deep- Sea mining market, driven by rising demand for minerals like cobalt, nickel, and copper. Countries such as China, India, Japan, and South Korea are actively investing in seabed exploration to support renewable energy, electronics, and industrial growth. The region’s focus includes polymetallic nodules, cobalt-rich crusts, and seafloor sulphides, with exploration zones spanning the Pacific and Indian Oceans.

China Deep- Sea Mining Market Outlook

China leads the deep-sea mining market with strong institutional backing, including multiple exploration contracts from the International Seabed Authority and support from state-owned enterprises and national research programs. Its focus on securing cobalt, nickel, and copper aligns with long-term industrial and energy strategies.

As per instance, by 2025, China has emerged as the top player in Deep- Sea mining. It holds the most exploration licenses from the International Seabed Authority, mainly through state-owned companies. Backed by government support, China is targeting key minerals like cobalt, nickel, and copper vital for batteries, clean energy, and industry. This push helps secure its long-term energy and resource needs while reducing reliance on foreign supply chains.

India Deep- Sea Mining Market Trends

India, meanwhile, is rapidly expanding its presence through government-funded initiatives like the Deep Ocean Mission. Backed by substantial grants and two ISA contracts, India is targeting polymetallic sulphides and nodules in the Indian Ocean to strengthen its clean energy and manufacturing supply chains.

For instance, in 2025, India obtained 15-year exploration rights from the International Seabed Authority, allowing it to survey and study mineral-rich zones in the Indian Ocean. This move strengthens India’s position in securing vital undersea resources for future industrial and energy needs.

US Deep-Sea Mining Market Insights

U.S. is intensifying its interest in Deep- Sea mining as part of its broader strategy to secure domestic sources of critical minerals. Federal agencies and private firms are exploring seabed resources in the Pacific and Atlantic, particularly targeting polymetallic nodules and cobalt-rich crusts.

As per instance, in 2025, The U.S. Department of the Interior unveiled new rules to fast-track deep-sea mining in American waters, streamlining environmental reviews and extending prospecting permits.

Canada Deep-Sea Mining Industry Growth

Canada is emerging as a key player in the deep-sea mining market, leveraging its rich maritime resources, advanced research institutions, and strong regulatory frameworks. With growing global demand for critical minerals like cobalt, nickel, and rare earths, Canadian companies are exploring offshore opportunities to diversify supply chains and support the clean energy transition. The government's focus on sustainable resource development and strategic partnerships is positioning Canada to compete globally while balancing environmental stewardship and economic growth.

For instance, The Metals Company, based in Vancouver, is seeking two exploration licenses and a commercial recovery permit marking Canada's first commercial seabed mining bid and boosting its role in the global deep-sea mining industry.

Sustainability Analysis

Emerging Deep- Sea mining technologies offer promising environmental safeguards. Innovations such as low-impact robotic collectors, sediment plume control systems, and real-time ecological monitoring aim to minimize disruption to marine habitats. By targeting polymetallic nodules on the ocean floor rather than drilling into seamounts or hydrothermal vents some methods reduce habitat destruction and preserve biodiversity.

Competitive Landscape

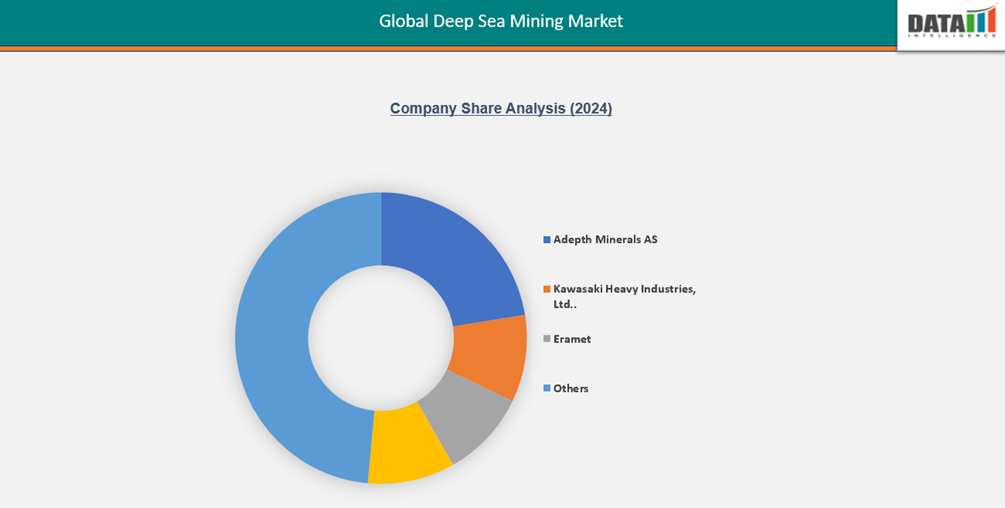

- The global deep-sea mining market is highly competitive, driven by a mix of global and regional players striving for technological efficiency and cost leadership.

- Key players include, Adepth Minerals, Cobalt Seabed Resources, Eramet Group, Impossible Metals, Kawasaki Heavy Industries, Nautilus Minerals, Neptune Minerals, Moana Minerals, The Metals Company, Global Sea Mineral Resources

Key Developments

In November 2025, Global Sea Mineral Resources (GSR) adopted an ESG-driven exploration and technology validation approach by pivoting toward real-time environmental oversight, leveraging AI and satellite monitoring to align with evolving sustainability requirements.

In August 2025, China Ocean Mineral Resources R&D Association (COMRA) strengthened its state-backed resource security strategy by emerging as a global leader in International Seabed Authority (ISA) exploration licenses and successfully deploying the “Jiaolong” human-occupied vehicle (HOV) for record-depth resource mapping.

In April 2025, The Metals Company (TMC) advanced its commercial permitting and vertical integration strategy by submitting the first-ever application for a commercial seabed mining permit, while securing an $85.2 million investment from Korea Zinc to support battery metal processing capabilities.

Why Choose DataM?

- Data-Driven Insights: Dive into detailed analyses with granular insights such as pricing, market shares and value chain evaluations, enriched by interviews with industry leaders and disruptors.

- Post-Purchase Support and Expert Analyst Consultations: As a valued client, you gain direct access to our expert analysts for personalized advice and strategic guidance, tailored to your specific needs and challenges.

- White Papers and Case Studies: Benefit quarterly from our in-depth studies related to your purchased titles, tailored to refine your operational and marketing strategies for maximum impact.

- Annual Updates on Purchased Reports: As an existing customer, enjoy the privilege of annual updates to your reports, ensuring you stay abreast of the latest market insights and technological advancements. Terms and conditions apply.

- Specialized Focus on Emerging Markets: DataM differentiates itself by delivering in-depth, specialized insights specifically for emerging markets, rather than offering generalized geographic overviews. This approach equips our clients with a nuanced understanding and actionable intelligence that are essential for navigating and succeeding in high-growth regions.

- Value of DataM Reports: Our reports offer specialized insights tailored to the latest trends and specific business inquiries. This personalized approach provides a deeper, strategic perspective, ensuring you receive the precise information necessary to make informed decisions. These insights complement and go beyond what is typically available in generic databases.

Target Audience 2026

- Manufacturers/ Buyers

- Industry Investors/Investment Bankers

- Research Professionals

- Emerging Companies