Data Center Water & Wastewater Treatment Equipment Market Definition and Overview

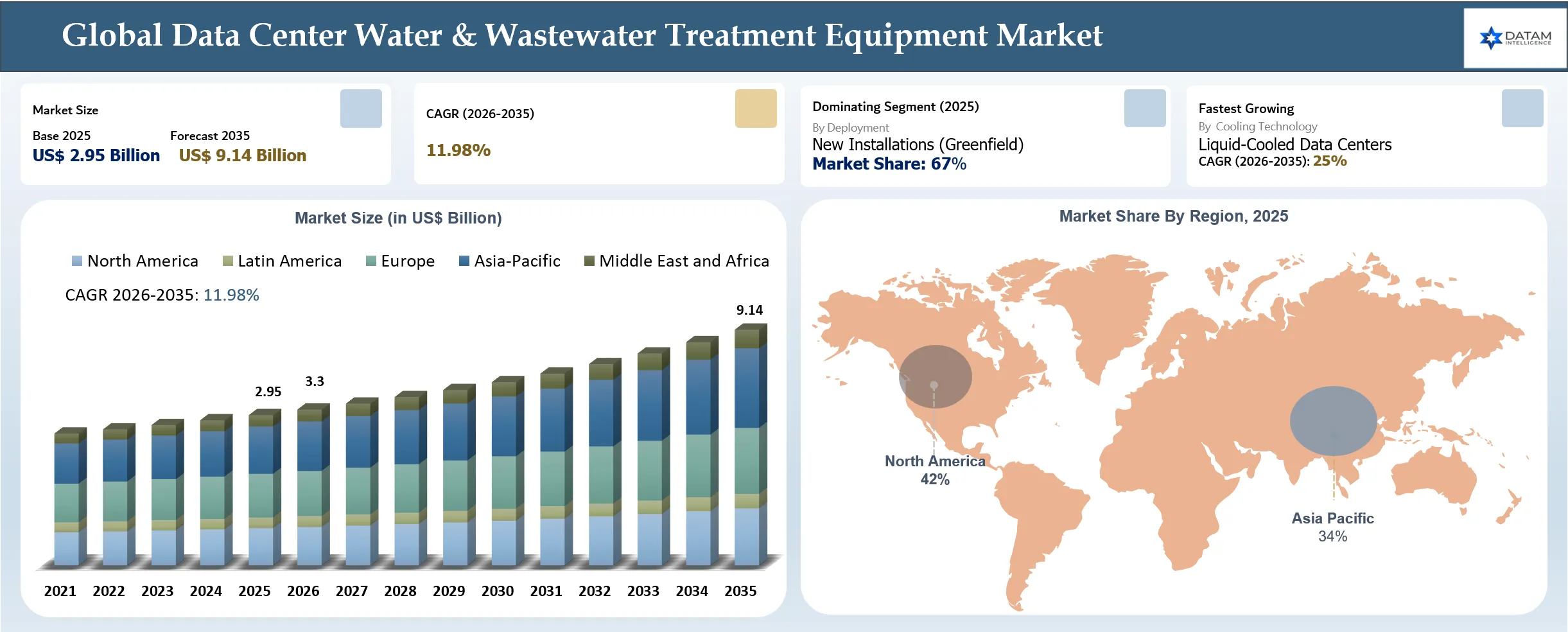

The global Data Center Water & Wastewater Treatment Equipment market reached USD 2.95 billion in 2025 and is expected to reach USD 9.14 billion by 2035, growing with a CAGR of 11.98% during the forecast period 2026-2035. The market is expanding due to an increase in water management solutions in hyperscale data centers, artificial intelligence computer centers, and cloud infrastructure facilities that demand high levels of water management solutions, such as water treatment and recycling solutions. As indicated by Google's Sustainability 2025 Environment Report, in 2024, Google returned 4.5 billion gallons of water, which saw it return 64% of the total amount of freshwater it used compared to the 18% recorded in 2023. Google has additionally made a commitment to replenish more freshwater than what it uses in its data centers and offices by the year 2030, having achieved over 7 billion gallons of water replenishment by the year 2025 through water stewardship programs. Such goals for sustainable water management have created an increased demand for treatment technologies, such as reverse osmosis, filtration units, closed-loop water treatment for cooling water, and wastewater recycling units. With water usage efficiency being the aim, water and wastewater treatment systems are becoming an integral part of data center technology.

The utilization of reclaimed water treatment solutions by hyperscale data center companies shows the growing need for advanced water management systems in order to ensure the sustainability of data center operations. In April 2026, Amazon partnered with Veolia to utilize the innovative water reuse solution at the company’s data center in Mississippi. This will be achieved through the installation of autonomous water treatment container units that will transform the effluent wastewater from neighboring water treatment facilities into high-quality reclaimed water that can be used in the cooling process within the data centers. The data center is estimated to be up and running in 2027 and will reuse over 83 million gallons of potable water per year.

Wide-Space Opportunities for the Data Center Water & Wastewater Treatment Equipment Value Chain

In January 2025, OpenAI, a U.S.-based artificial intelligence company, together with SoftBank Group (Japan), Oracle Corporation (U.S.), and MGX (UAE), announced the Stargate Project, a new AI infrastructure company that plans to invest USD 500 billion over the next four years to build AI data centers across the United States. The consortium will immediately deploy USD 100 billion during the initial phase, with the first hyperscale AI campus under development in Texas and additional campuses planned nationwide. SoftBank and OpenAI serve as the lead partners, with SoftBank assuming financial responsibility and OpenAI overseeing operations, while Arm, Microsoft, NVIDIA, Oracle, and OpenAI act as the project's key technology partners. The initiative is expected to create hundreds of thousands of jobs and represents one of the world's largest AI infrastructure investments. As part of the project, OpenAI also issued requests for proposals (RFPs) and qualifications (RFQs) for land acquisition, power infrastructure, architecture, engineering, and data center construction, creating substantial opportunities for infrastructure and utility suppliers.

The investment is expected to create significant procurement opportunities across the Data Center Water & Wastewater Treatment Equipment value chain. Water treatment and recycling companies, including Ecolab, Veolia Water Technologies, Xylem, Kurita Water Industries, SUEZ Water Technologies & Solutions, DuPont Water Solutions, Gradiant, Ovivo, and Pentair, are well-positioned to secure contracts for cooling water treatment, reverse osmosis (RO), ultrapure water (UPW), wastewater recycling, and zero-liquid discharge (ZLD) systems. Data center cooling and fluid management providers such as Vertiv, Schneider Electric, Johnson Controls, Trane Technologies, Baltimore Aircoil Company (BAC), and CoolIT Systems are expected to benefit from increasing demand for liquid cooling infrastructure and advanced thermal management. In addition, innovative water technology developers, including KMX Technologies, Hydroleap, Industrie De Nora, and Tekleen, are likely to gain opportunities for membrane-based water recovery, electrochemical water treatment, filtration, blowdown recovery, and sustainable water reuse solutions as hyperscale AI data center deployments accelerate across the United States.

Data Center Water & Wastewater Treatment Equipment Market Key Takeaways

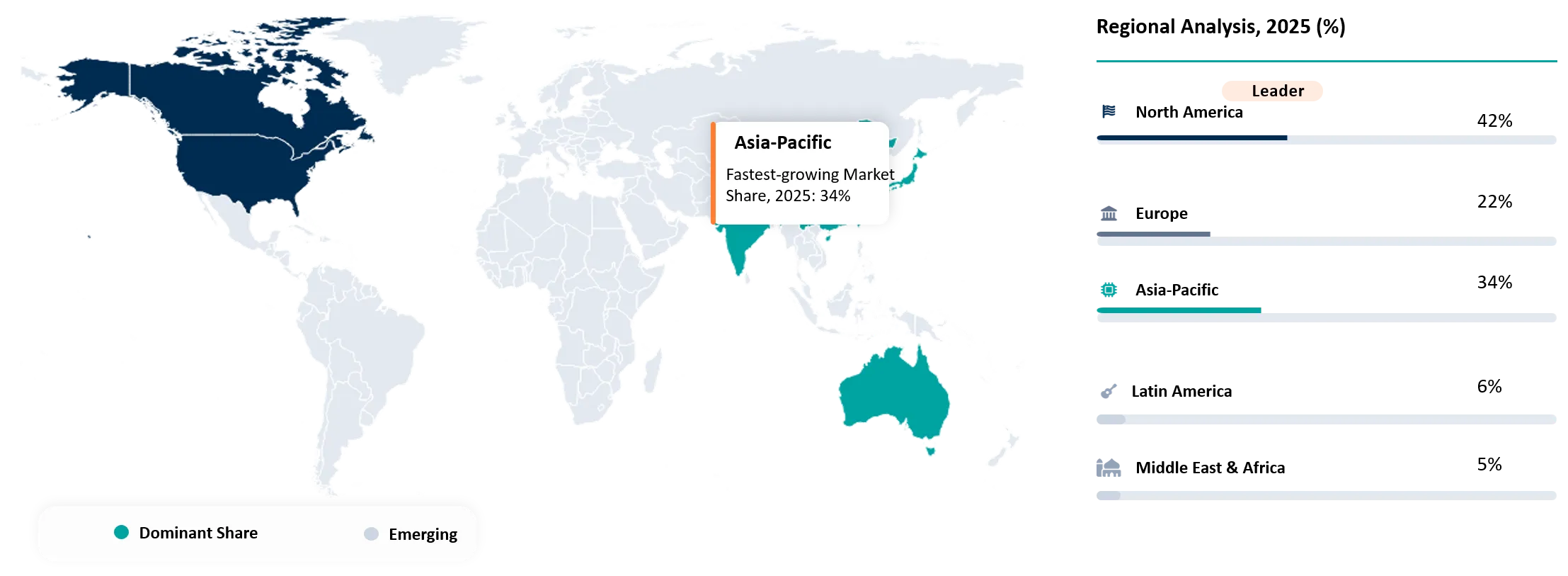

- North America secured the leading position in the industry, accounting for 42% of the global market share in 2025. This regional stronghold is primarily driven by massive infrastructure investments from tech giants like Microsoft, Google, and AWS.

- New greenfield installations dominated the market landscape by capturing 67% of the total market share in 2025. This allows operators to integrate advanced treatment technologies like reverse osmosis and zero liquid discharge directly from the design phase

- Data centers in India currently consume an estimated 150 billion liters of water each year for cooling operations. Due to the rapid boom in the sector, this figure is projected to skyrocket to 358 billion liters annually by 2030.

- Mega-consortiums are heavily backing AI development, highlighted by OpenAI, Oracle, and SoftBank committing USD 500 billion to the Stargate Project. Meanwhile, Microsoft standalone announced an approximate USD 80 billion investment in AI-enabled data centers for fiscal year 2025.

Data Center Water & Wastewater Treatment Equipment Market Industry Trends and Strategic Insight

- The rapid deployment of AI servers, high-performance computing (HPC), and GPU-intensive workloads is increasing thermal management requirements, pushing data center operators toward advanced water treatment and recycling infrastructure.

- Data center operators are increasingly investing in closed-loop water circulation systems, where treated water continuously circulates between cooling equipment and heat rejection systems with minimal freshwater replacement.

- Data center operators are increasingly measuring water performance through Water Usage Effectiveness (WUE), which evaluates water consumption relative to IT energy usage and helps optimize cooling efficiency.

- Data centers are moving beyond water reduction strategies toward water recovery models, where treated wastewater, condensate, and process water are reused for cooling and facility operations.

- Data center operators are integrating IoT sensors, predictive analytics, and AI-driven water management platforms to monitor parameters such as conductivity, pH, dissolved solids, chemical concentration, and cooling system performance.

- Increasing chip densities and liquid cooling adoption are creating demand for higher-quality water treatment systems capable of maintaining strict chemical and contamination control requirements.

Data Center Water & Wastewater Treatment Equipment Market Scope

| Metrics | Details | |

| 2025 Market Size | USD 2.95 Billion | |

| 2035 Projected Market Size | USD 9.14 Billion | |

| CAGR (2026-2035) | 11.98% | |

| Largest Market | North America | |

| Fastest Growing Market | Asia-Pacific | |

| By Equipment Type | Filtration Systems, Membrane Systems, Chemical Treatment Systems, Disinfection Systems, Water Softening Systems, Deionized (DI) Water Systems, Condensate Recovery Systems, Water Recycling & Reuse Systems, Zero Liquid Discharge (ZLD) Systems, Sludge Handling Equipment, Monitoring & Automation Systems. | |

| By Treatment Stage | Raw Water Pretreatment, High Purity Water Treatment, Cooling Water Treatment, Wastewater Treatment, Water Reuse & Recycling, Zero Liquid Discharge (ZLD). | |

| By Water Source | Municipal Water, Groundwater, Surface Water, Reclaimed/Recycled Water, Rainwater Harvested Water. | |

| By Cooling Technology | Air-Cooled Data Centers, Water-Cooled Data Centers, Liquid-Cooled Data Centers, Hybrid Cooling Systems. | |

| By Data Center Type | Hyperscale Data Centers, Colocation Data Centers, Enterprise Data Centers, Edge Data Centers. | |

| By Deployment | New Installations (Greenfield), Retrofit & Expansion (Brownfield) | |

| By End User | Cloud Service Providers, Telecom Operators, Banking, Financial Services & Insurance (BFSI), Government & Defense, Healthcare, Manufacturing, IT & Software, Others. | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Türkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

Data Center Water & Wastewater Treatment Equipment Market Disruption Analysis

AI-Driven Data Center Expansion Reshaping Water Treatment and Cooling Infrastructure Requirements

The disruptions in the Data Center Water & Wastewater Treatment Equipment market are largely caused by the quick rise in the use of AI workload, High-Performance Computing (HPC), and accelerated computing. These technological advances are driving changes to the demands on data center thermal management. The increase in server density and the presence of AI accelerators are taking data centers beyond the capabilities of existing air-based cooling systems and moving towards liquid cooling, immersion cooling, and closed-loop thermal management systems. This disruptive trend in data centers is leading to a change in demand for conventional water treatment systems. According to NVIDIA’s 2025 Blackwell platform analysis, hyperscale AI facilities that were formerly running around 20 kW per rack are now moving beyond 135 kW per rack, which is leading to thermal management difficulties and increasing the uptake of liquid cooling technology.

In addition, NVIDIA revealed that the use of the Blackwell platform would allow for water savings exceeding 300 times through the implementation of liquid cooling technologies. In 2025, AWS introduced the use of liquid cooling systems for AI infrastructure in response to the growing trend of liquid cooling architecture being implemented by hyperscale operators in the industry. These factors have led to changes in the Data Center Water & Wastewater Treatment Equipment Market in the sense that there is a move away from conventional cooling tower treatment systems towards water recycling systems.

Data Center Water & Wastewater Treatment Equipment Market BCG Matrix: Company Evaluation

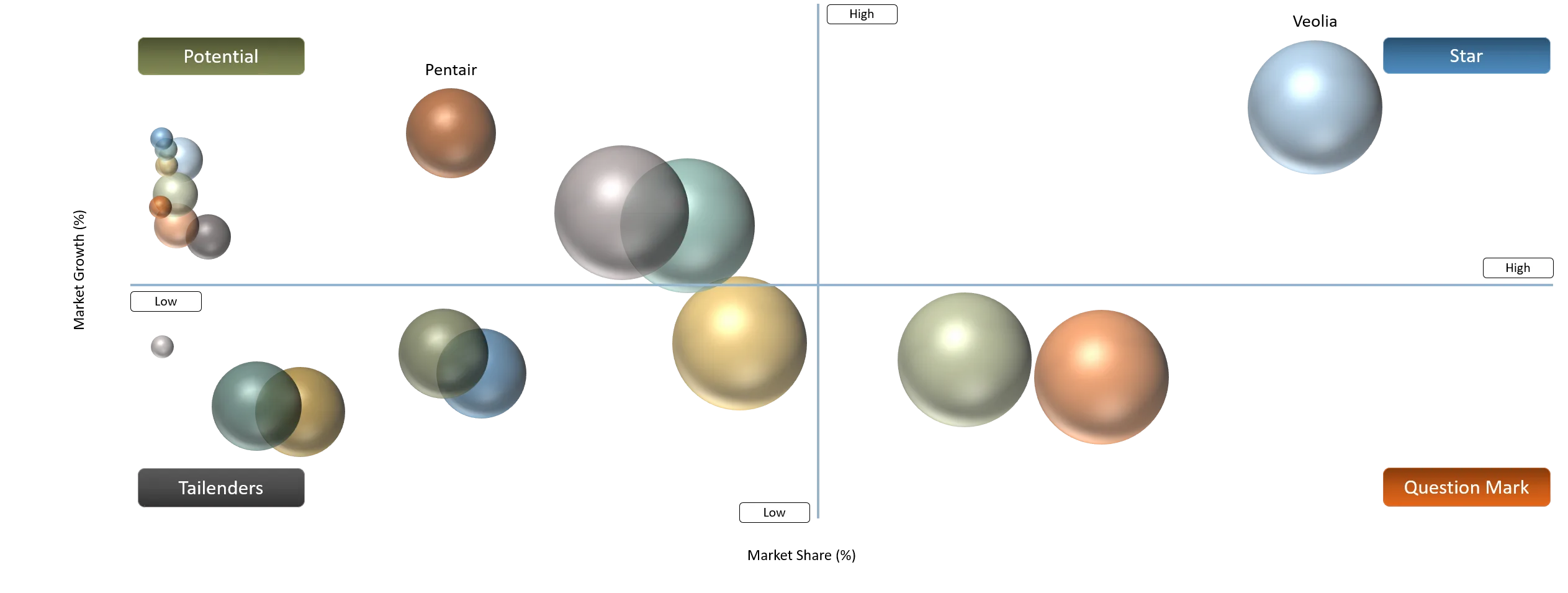

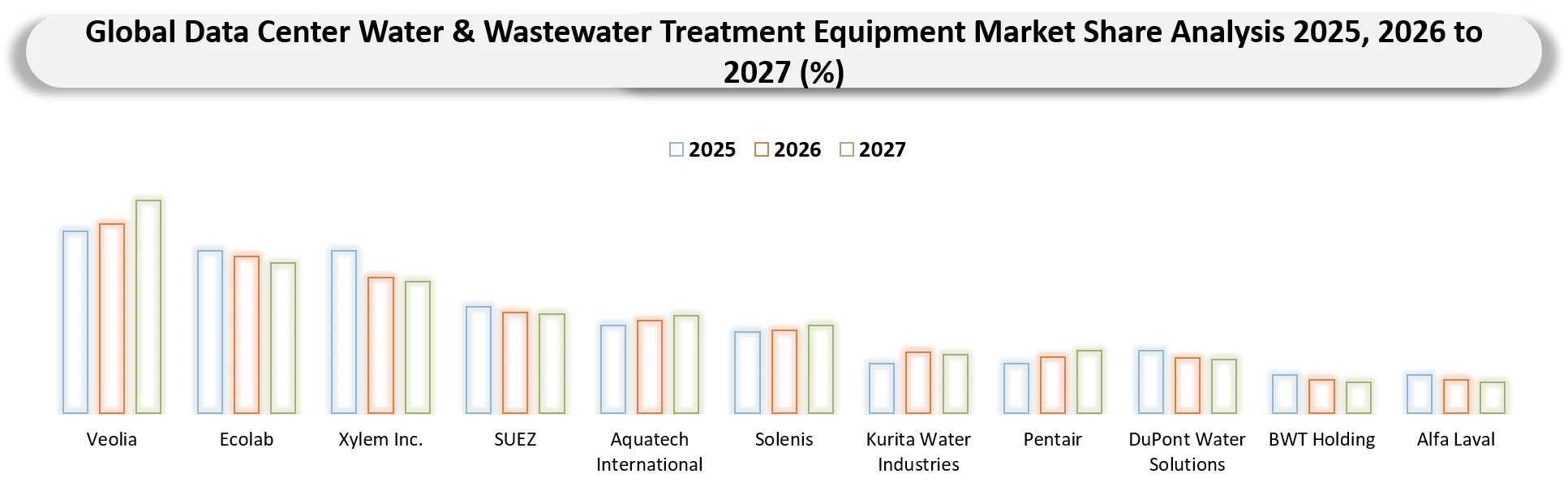

Stars include Veolia, Ecolab, Xylem Inc., and SUEZ due to the fact that these firms have dominant market positions in the field of industrial water management, and these players are aggressively developing their offerings in hyperscale data centers, AI infrastructure, and sustainable cooling systems. The integrated services of these firms include cooling water treatment, wastewater recycling, ultra-pure water systems, digital water management, and water optimization platforms. Question Marks include Aquatech International, Solenis, and Kurita Water Industries, which are strategically placed since they have high levels of technical proficiency in industrial water management, specialty chemicals, and high-purity water management, albeit with a more specialized focus on the data center market when compared to the large-scale water management firms.

Potential categories include Pentair, DuPont Water Solutions, BWT Holding, and Toray Industries. Their strength lies in the increasing demand for filters, reverse osmosis membranes, ultrafiltration, and purification of high-purity water required in data center cooling processes. They all have advanced technology strengths in water purification and membrane filtration, yet they lack positioning in data centers' comprehensive water management solutions as compared to other major integrated players. The Tailenders group includes the Alfa Laval company, as its participation in the Data Center Water & Wastewater Treatment Equipment market is limited to providing supporting equipment like heat exchangers, separators, and thermal management units for the purpose of treating water for data centers.

Data Center Water & Wastewater Treatment Equipment Market Dynamics

Driver Impact Analysis

| Driver | Market Growth Impact (%) | Demand Concentration | Impacted Use Case | Strategic Impact |

Rapid expansion of hyperscale and AI-driven data centers is increasing demand for advanced cooling water treatment and wastewater management systems. | 30% | High | AI data centers, hyperscale facilities, cloud computing infrastructure, high-performance computing (HPC) centers. | Accelerates adoption of advanced cooling water treatment, closed-loop cooling systems, high-purity water solutions, and wastewater recycling technologies to support higher computing densities. |

Rising water consumption concerns from large-scale data center operations are accelerating investments in water recycling, wastewater reuse, and zero-liquid discharge treatment technologies. | 25% | High | Cooling tower water reuse, reclaimed water systems, wastewater recovery, sustainable data center operations. | Drives transition from freshwater-dependent cooling toward circular water management models and increases demand for advanced wastewater treatment equipment. |

Increasing implementation of Water Usage Effectiveness (WUE) targets by data center operators is driving demand for real-time water monitoring, filtration, and optimization equipment. | 20% | Moderate to High | Water quality monitoring, cooling system optimization, chemical dosing control, facility water management. | Encourages integration of IoT-enabled monitoring systems, automated treatment controls, and digital water management platforms to improve operational efficiency. |

Rising demand for closed-loop cooling systems is driving the deployment of membrane filtration, reverse osmosis, ultrafiltration, and deionization technologies in data center facilities. | 25% | High | Liquid cooling systems, direct-to-chip cooling, immersion cooling, high-density server environments. | Shifts market demand toward high-purity water treatment technologies and specialized cooling fluid management solutions rather than conventional water treatment systems. |

Integration of IoT-based monitoring and AI-enabled water management platforms is improving treatment efficiency, reducing chemical usage, and enabling predictive maintenance of cooling systems. | 15% | Moderate | Smart water monitoring, predictive maintenance, automated chemical management, remote facility operations. | Creates opportunities for technology providers combining water treatment equipment with digital analytics, automation, and real-time optimization capabilities. |

Rapid expansion of hyperscale and AI-driven data centers is increasing demand for advanced cooling water treatment and wastewater management systems

Growing deployment of hyperscale data centers and AI-based computing facilities represents a significant trend that drives the need for modern Data Center Water & Wastewater Treatment Equipment. Growing deployment of AI, machine learning, and HPC workloads contributes to a higher density of servers, which increases the need for cooling water treatment, water recirculation, and wastewater treatment solutions. According to the International Energy Agency (IEA), in 2025, data center electricity consumption will grow by over two times by 2030, reaching 945 TWh due to the increasing role of AI and accelerated computing workloads. Growing infrastructure contributes to growing needs in cooling and supporting water treatment technologies, which allows operating facilities to operate effectively while saving resources. With the growing expansion of hyperscale data centers, modern equipment like reverse osmosis systems, ultrafiltration, closed-loop cooling water treatment, and wastewater reuse systems becomes crucial for the construction of sustainable infrastructure.

The rise of water intensity of AI data centers will increase the need for sustainable water management practices, including innovative water treatment techniques for cooling and water recycling. In June 2026, The Times of India reported that the rising use of AI-powered data centers is causing an increased consumption of fresh water because of high cooling needs. The article stressed that one single interaction of an AI data center, for example, a ChatGPT interaction, would lead to the usage of about 519 milliliters of water because of the cooling of servers and electricity-related water consumption. It was also mentioned that the rising AI infrastructure globally would cause increased water needs, thus leading to the requirement of innovative cooling water treatment, water recycling, and wastewater management.

Restraint Impact Analysis

| Restraint | Drag on Market Growth (%) | Primary Impact Area | Impacted Use Case | Strategic Impact |

Limited availability of water resources and regional restrictions on industrial water usage create operational challenges for data center expansion and water treatment deployment. | 15% | Data center site selection, cooling infrastructure expansion, and water sourcing | Hyperscale data centers, AI data centers, and colocation facilities in water-stressed regions | Increases the need for water-efficient cooling, wastewater recycling, and zero-liquid discharge (ZLD) solutions while delaying new facility deployments in regions with strict water regulations. |

Transition toward waterless cooling technologies reduces demand for conventional water-intensive treatment systems in certain data center applications. | 10% | Cooling technology adoption and water consumption reduction strategies | AI/HPC data centers adopting direct-to-chip liquid cooling, immersion cooling, and air-based cooling systems | Shifts market demand from traditional water treatment equipment toward specialized water management, monitoring, and closed-loop treatment solutions integrated with advanced cooling systems. |

Complex integration of water treatment equipment with existing cooling infrastructure creates deployment challenges, especially in retrofitting operational data centers. | 12% | Infrastructure integration, retrofit complexity, and operational downtime management | Existing enterprise data centers, colocation facilities, and aging data center infrastructure | Increases engineering complexity, installation timelines, and capital requirements, encouraging modular treatment systems and customized retrofit solutions. |

Dependence on external water utilities and availability of reclaimed water sources can restrict adoption of advanced water reuse systems in certain regions. | 9% | Water supply reliability and sustainability infrastructure availability | Large-scale data centers using recycled water, treated wastewater, and municipal reclaimed water systems | Limits deployment of water reuse technologies where supporting infrastructure is unavailable, driving investments in onsite treatment, water storage, and alternative cooling strategies. |

Limited availability of water resources and regional restrictions on industrial water usage create operational challenges for data center expansion and water treatment deployment

One of the major challenges limiting the expansion of Data Center Water & Wastewater Treatment Equipment is the increasing scarcity of freshwater resources and the implementation of regional restrictions on industrial water consumption. Data centers require substantial volumes of water for cooling operations, particularly in regions adopting water-intensive cooling technologies such as evaporative cooling and cooling towers. This growing water dependency has increased regulatory scrutiny, especially in water-stressed regions, where authorities are imposing stricter limits on industrial water withdrawals and encouraging the adoption of water-efficient cooling and recycling systems.

The increasing deployment of AI-based applications, cloud computing, and hyperscale data centers is intensifying the need for effective cooling solutions, hence posing challenges to water consumption. In July 2026, according to WION, the growing environmental issues associated with India’s booming data center sector were noted, especially in terms of increased need for water-based cooling solutions. It was noted that data centers need large amounts of water to cool servers, with industry projections showing that data centers in India consume about 150 billion liters of water each year and will continue to increase to about 358 billion liters by 2030.

Data Center Water & Wastewater Treatment Equipment Market Segment Analysis

The global Data Center Water & Wastewater Treatment Equipment market is segmented based on equipment type, treatment stage, water source, cooling technology, data center type, deployment, end user, and region.

Adoption of Greenfield Data Center Projects Driving Demand for Water & Wastewater Treatment Equipment

The New Installations (Greenfield) segment dominated the Data Center Water & Wastewater Treatment Equipment Market, accounting for 67% of the market share in 2025, driven by the rapid construction of hyperscale, AI, and cloud data centers worldwide. Greenfield projects provide operators with the opportunity to integrate advanced water treatment infrastructure from the design stage, including reverse osmosis (RO) systems, water recycling units, zero liquid discharge (ZLD) technologies, digital water quality monitoring, and high-efficiency cooling water treatment solutions. As environmental regulations tighten and sustainability becomes a key investment criterion, newly built facilities are increasingly designed to minimize freshwater consumption while maximizing water reuse and operational efficiency.

The continued expansion of AI infrastructure has further strengthened this segment's leadership. In January 2025, OpenAI, Oracle, and SoftBank announced the Stargate Project, committing US$500 billion over the coming years to develop next-generation AI infrastructure across the United States, with an initial investment of US$100 billion. Similarly, Microsoft announced in 2025 that it would invest approximately US$80 billion in AI-enabled data center infrastructure during fiscal year 2025. These large-scale greenfield developments are accelerating demand for integrated water and wastewater treatment equipment as operators prioritize sustainable cooling systems, high-purity process water, and advanced water reuse technologies to comply with evolving environmental standards while supporting high-density AI workloads.

Data Center Water & Wastewater Treatment Equipment Market Geographical Penetration

Rapid Expansion of AI Data Centers and Sustainable Water Infrastructure Driving North American Market Leadership

North America dominated the Data Center Water & Wastewater Treatment Equipment Market, accounting for 42% of the global market share in 2025, driven by the rapid expansion of hyperscale data centers, AI infrastructure investments, and stringent sustainability requirements across the United States and Canada. The region hosts the world's largest concentration of cloud service providers, including Microsoft, Google, Amazon Web Services (AWS), and Meta, all of which are investing heavily in next-generation data centers equipped with advanced water treatment, water recycling, and high-purity process water systems. Growing regulatory focus on water conservation and increasing adoption of circular water management strategies have further accelerated investments in reverse osmosis (RO), wastewater reuse, zero liquid discharge (ZLD), and digital water monitoring technologies, reinforcing North America's leadership in the market.

The acquisition reflects the increasing industry focus on advanced fluid management and water treatment technologies to support high-density AI data centers with liquid cooling infrastructure. In November 2025, Vertiv Holdings Co., a U.S.-based digital infrastructure manufacturer and service provider, announced its intention to acquire PurgeRite, a company from the USA, for approximately US$1.0 billion, with an additional earn-out amount of up to US$250 million depending on performance metrics in 2026. The goal of the merger is to enhance the liquid cooling portfolio of Vertiv by merging PurgeRite's technology in mechanical flushing, purging, filtration, and fluid management of data centers.

U.S. Data Center Water & Wastewater Treatment Equipment Market Trends

The U.S. holds dominance in the North American Data Center Water & Wastewater Treatment Equipment Market, owing to its extensive hyperscale data center infrastructure, fast deployment of AI infrastructure, and increased spending on innovative water management technologies. The United States is home to key cloud service providers such as AWS, Microsoft, Google, Oracle, and Meta, all of whom are increasing their AI-enabled data centers, necessitating the installation of state-of-the-art water treatment equipment, including RO filtration, water recycling, high-purity water treatment, and digitized water management. Increased environmental regulations and commitments of organizations towards responsible water use have driven innovations in this space, cementing the United States’ dominance in the market.

In December 2025, Sylmar Group, a U.S.-based industrial water treatment and infrastructure services company, acquired ProChem Water, a U.S.-based company that provides industrial and commercial water and wastewater treatment solutions. This merger enhances Sylmar Group’s capabilities for water treatment chemicals, cooling water treatments, boiler water treatment, wastewater treatment, and water quality services. The Sylmar Group is a mission-critical industry facility with high water management demands, including data centers.

Canada Data Center Water & Wastewater Treatment Equipment Market Outlook

Canada is emerging as the fastest-growing country in the North American Data Center Water & Wastewater Treatment Equipment Market, supported by increasing hyperscale data center investments, abundant renewable energy resources, and growing emphasis on sustainable water management. The country's cool climate enables energy-efficient operations, while expanding AI and cloud infrastructure projects are driving demand for advanced water treatment technologies, including reverse osmosis (RO), water recycling, high-purity water systems, and intelligent water quality monitoring.

In August 2025, Ecolab Inc., a U.S.-based sustainability and water treatment solutions company, announced its agreement to acquire Ovivo’s Electronics division, a Canadian-based provider of ultrapure water treatment solutions, for US$2.4 billion. The acquisition aims to strengthen Ecolab’s capabilities in ultrapure water, advanced water treatment, and water circularity technologies for high-tech industries, enhancing its ability to support semiconductor manufacturing and the growing water management requirements of AI-driven data centers.

Data Center Water & Wastewater Treatment Equipment Market Competitive Landscape

- The market is characterized by three key participant groups: global water technology providers, industrial water treatment specialists, and membrane & filtration technology manufacturers. Veolia, SUEZ, Xylem Inc., Ecolab (Nalco Water), Aquatech International, and Kurita Water Industries lead the market by providing end-to-end water treatment, wastewater recycling, cooling water management, and digital monitoring solutions for hyperscale and AI data centers. DuPont Water Solutions, Toray Industries, Pentair, and BWT Holding specialize in reverse osmosis (RO), ultrafiltration (UF), ion exchange, and membrane technologies, while Alfa Laval focuses on heat transfer and liquid cooling systems that complement advanced water treatment infrastructure. The market remains highly technology-driven, where expertise in water reuse, zero liquid discharge (ZLD), digital water management, and AI-enabled monitoring platforms determines competitive differentiation. Strategic partnerships with hyperscale cloud providers, AI data center developers, and engineering, procurement, and construction (EPC) firms are becoming increasingly important as operators prioritize water efficiency and regulatory compliance.

- Key players are Veolia, Ecolab, Xylem Inc., SUEZ, Aquatech International, Solenis, Kurita Water Industries, Pentair, DuPont Water Solutions, BWT Holding, Alfa Laval, and Toray Industries.

Key Developments

- July 2026: Ecolab Inc., a U.S.-based sustainability and water treatment solutions company, completed its acquisition of CoolIT Systems, a Canadian-based provider of direct liquid cooling solutions, for approximately US$4.75 billion.

- June 2026: Vertiv Holdings Co., a U.S.-based critical digital infrastructure manufacturer and service provider, launched Vertiv™ PurgeRite™ NearZero™, a fluid management service designed for data center cooling system commissioning. The solution integrates water recycling, reverse osmosis, filtration, engineered flushing, and water quality monitoring, delivering up to 78% reduction in water consumption, up to 91% reduction in water haul-off volume, and up to 34% reduction in discharge management costs, supporting sustainable water management in AI-driven data centers.

- December 2025: KMX Technologies, a U.S.-based water treatment technology company, launched its Vacuum Membrane Distillation (VMD) platform for liquid-cooled data centers.

- February 2026: Tekleen, a U.S.-based manufacturer of automatic self-cleaning water filtration systems, launched its Full-Flow Filtration and Dewatering Strategy for data center cooling systems.

- August 2025: Hydroleap, a Singapore-based provider of electrochemical water treatment solutions, raised US$4.75 million in funding to accelerate the deployment of its chemical-free water treatment technology across APAC data centers and industrial sectors.

- May 2026: Industrie De Nora S.p.A., an Italy-based provider of sustainable electrochemical and water treatment technologies, announced its acquisition of BW Water, a Denmark-based water and wastewater treatment solutions company.

Key Procurement Priorities and Buyer Evaluation Criteria

- Organizations investing in the Data Center Water & Wastewater Treatment Equipment Market increasingly select suppliers based on their ability to deliver integrated water treatment solutions that reduce freshwater consumption, improve water reuse, ensure high-purity process water, and support sustainable cooling operations for hyperscale and AI data centers. Suppliers offering complete systems—including reverse osmosis (RO), ultrafiltration (UF), wastewater recycling, zero liquid discharge (ZLD), and digital monitoring platforms—are preferred.

- Procurement decisions are increasingly influenced by the rapid expansion of AI-ready data centers, stricter environmental regulations, corporate ESG commitments, and growing concerns over water scarcity. Buyers prioritize vendors capable of delivering water-efficient, energy-efficient, and scalable treatment systems that support liquid cooling, reclaimed water utilization, and compliance with evolving water discharge and sustainability standards.

- Buyers evaluate suppliers based on water recovery efficiency, treatment reliability, operating cost, membrane performance, automation capabilities, water quality consistency, chemical optimization, and lifecycle maintenance costs. The ability to minimize downtime, maximize water reuse, and integrate predictive monitoring and remote diagnostics has become a key purchasing criterion.

Why Choose DataM?

- Technological Innovations: Explores advancements in data center water and wastewater treatment technologies, including reverse osmosis (RO), ultrafiltration (UF), zero liquid discharge (ZLD), AI-enabled water quality monitoring, smart SCADA systems, and closed-loop water recycling solutions that improve water efficiency, reduce freshwater consumption, and support next-generation AI and hyperscale data centers.

- Product Performance & Market Positioning: Evaluates how leading companies differentiate their solutions based on water recovery rates, treatment efficiency, membrane performance, energy consumption, automation capabilities, scalability, and lifecycle operating costs, highlighting competitive advantages across hyperscale, colocation, enterprise, and edge data center applications.

- Real-World Evidence: Highlights the deployment of advanced water treatment systems across AI data centers, hyperscale cloud facilities, colocation campuses, and liquid-cooled computing environments, demonstrating measurable benefits such as reduced water withdrawal, increased water reuse, improved cooling reliability, lower operating costs, and enhanced environmental compliance.

- Market Updates & Industry Changes: Tracks key developments including AI data center investments, hyperscale campus expansions, water reuse initiatives, sustainability regulations, digital water management technologies, and regional infrastructure investments across North America, Europe, Asia-Pacific, and the Middle East, providing timely insights into evolving market dynamics.

- Competitive Strategies: Analyzes how leading companies strengthen their market position through advanced membrane technologies, digital water management platforms, strategic partnerships with hyperscale cloud providers, acquisitions, sustainability-focused innovations, and expansion of industrial water treatment capabilities to address increasing demand from AI and high-density computing facilities.

- Pricing & Market Access: Explains pricing variations based on treatment capacity, membrane technology, automation level, water recovery efficiency, project complexity, and customization requirements, while assessing procurement models through EPC contractors, system integrators, OEMs, and direct partnerships with hyperscale and colocation data center operators.

- Market Entry & Expansion: Identifies growth opportunities driven by AI infrastructure expansion, liquid cooling adoption, increasing water scarcity, ESG commitments, stricter wastewater discharge regulations, and demand for circular water management, while outlining strategies such as localized manufacturing, technology partnerships, modular treatment systems, and expansion into emerging hyperscale data center markets.

Target Audience

- Hyperscale Data Center Operators

- Cloud Service Providers (CSPs)

- Colocation Data Center Providers

- Enterprise Data Center Owners & Operators

- AI Infrastructure Developers

- Data Center Design & Engineering (AEC) Firms

- EPC (Engineering, Procurement & Construction) Contractors