Data Center Piping Market Size & Share

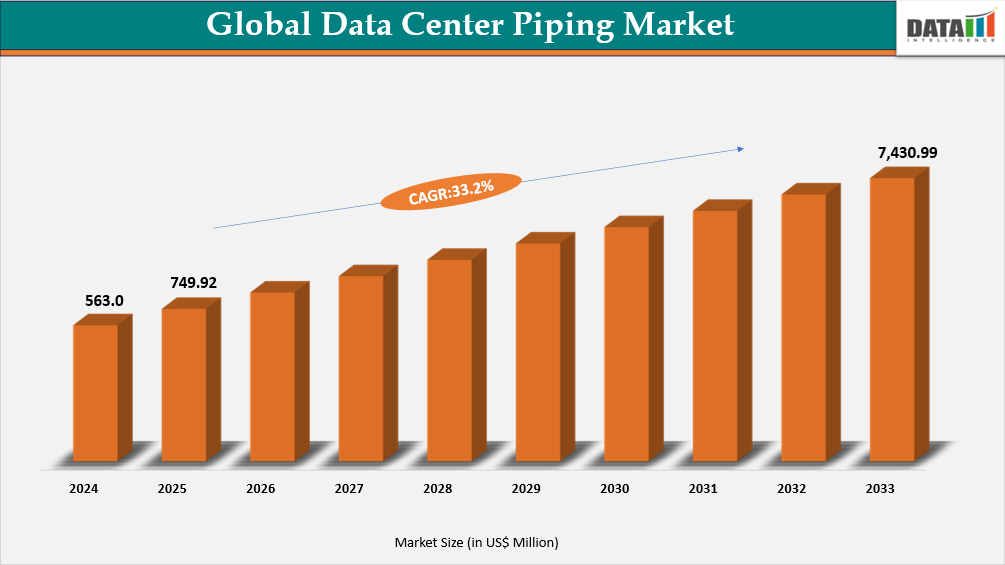

The global data center piping market reached US$ 749.92 million in 2025 and is expected to reach US$ 7,430.99 million by 2033, growing with a CAGR of 33.2% during the forecast period 2026-2033.

The global data center piping market is expanding due to increasing deployment of hyperscale, colocation, enterprise, and edge data centers, which require efficient thermal management and liquid cooling systems to support high-density computing.

For example, in 2025, BRUGG Pipes launched full-scale production of its pre-insulated flexible pipe system in Joliet, Illinois, enabling faster deployment and improved energy efficiency for North American data centers. Similarly, Ecolab expanded into advanced liquid cooling solutions, strengthening the fluid distribution ecosystem. These developments highlight that advanced piping solutions, rigid, flexible, and pre-insulated, are increasingly strategic for sustainable, high-performance data center operations.

Data Center Piping Industry Trends and Strategic Insights

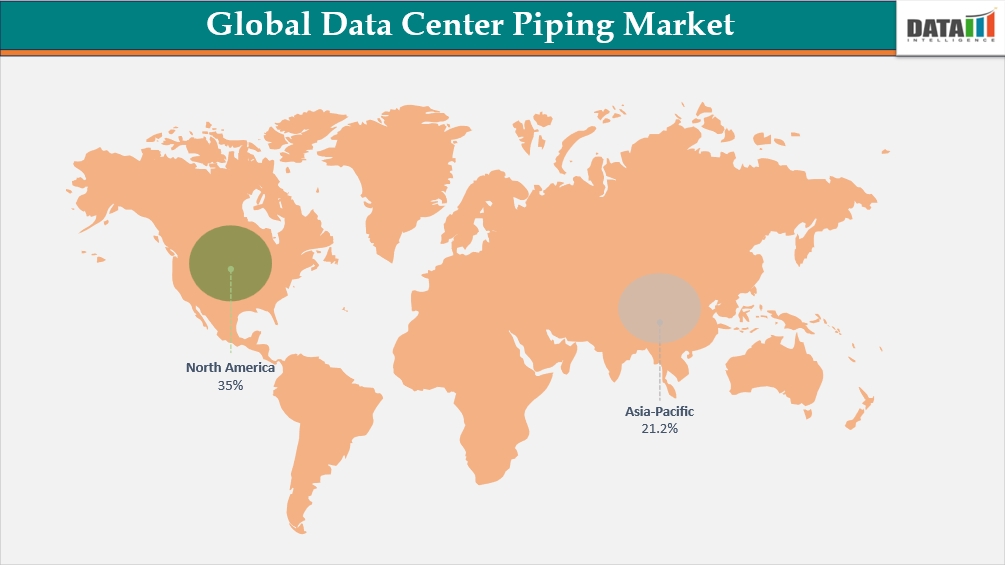

- Asia-Pacific is the fastest-growing region in the data center piping market, capturing the share of 21.2% in 2025.

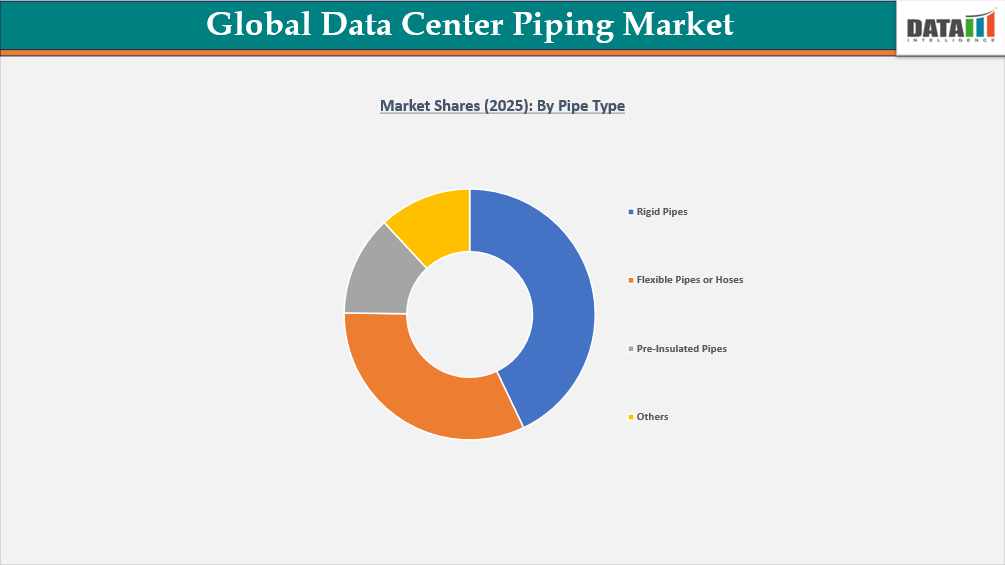

- By pipe type, the flexible pipes are projected to be the largest market, holding a significant share of about 28.2% in 2025.

Global Data Center Piping Market Size and Future Outlook

- 2025 Market Size: US$ 749.92 Million

- 2033 Projected Market Size: US$ 7,430.99 Million

- CAGR (2026-2033): 33.2%

- Largest Market: North America

- Fastest Market: Asia-Pacific

Data Center Piping Market Scope

| Metrics | Details |

| By Pipe Type | Rigid Pipes, Flexible Pipes or Hoses, Pre-Insulated Pipes, Others |

| By Material Type | Carbon Steel, Stainless Steel, Copper, Plastics, Others |

| By Data Center Type | Hyperscale Data Centers, Colocation Data Centers, Enterprise Data Centers, Others |

| By Application | Cooling Water Distribution, Heat Rejection, Liquid Cooling Loops, Others |

| By Installation Type | New, Retrofit, or Upgradation |

| By Diameter Size | Small Diameter (<2 inches), Medium Diameter (2–6 inches), Large Diameter (>6 inches) |

| By Region | North America, Latin America, Europe, Asia-Pacific, Middle East and Africa |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth |

Data Center Piping Market Dynamics

Increasing Demand for Prefabricated and Easy-Install Piping

The data center piping market is benefiting from the growing preference for prefabricated and easy-install systems, driven by the need to accelerate construction timelines. Hyperscale and edge deployments require rapid scalability, pushing operators toward modular piping solutions that can be assembled off-site and installed quickly. These systems reduce on-site labor dependency and minimize installation errors through standardized designs. For instance, in November 2025, Siemens partnered with Delta Electronics to deliver prefabricated, modular power solutions for data centers, highlighting the broader industry shift toward plug-and-play infrastructure.

Additionally, modular piping aligns well with evolving data center architectures that prioritize flexibility and phased expansion. Pre-engineered piping skids and plug-and-play systems allow seamless integration with cooling infrastructure, especially in liquid-cooled environments. This approach improves quality control, as fabrication occurs in controlled environments rather than on-site conditions. Consequently, operators can achieve consistent performance while optimizing capital expenditure and deployment speed across multiple facilities.

Leak Risk Sensitivity in High-Value Environments

Leak risk remains a critical concern in data center environments, where even minor fluid leakage can lead to severe equipment damage and operational disruption. High-value IT infrastructure, including servers and networking equipment, is extremely sensitive to moisture exposure, making reliability a top priority in piping design. This risk is further amplified in advanced liquid cooling systems, where coolant is circulated closer to critical components. As a result, operators tend to adopt conservative approaches, slowing the adoption of newer piping technologies.

Moreover, the financial and reputational impact of downtime caused by leaks can be substantial, particularly for hyperscale and colocation providers. To mitigate this, companies invest heavily in high-quality materials, rigorous testing, and leak detection systems, increasing overall system costs. The need for redundant piping configurations and strict compliance standards also adds complexity to design and installation. Consequently, leak sensitivity acts as a barrier to rapid innovation and widespread adoption of advanced piping solutions.

Segment Analysis

The global data center piping market is segmented based on pipe type, material type, data center type, application, installation type, diameter, and region.

Growing Adoption of High-Density Liquid Cooling and Modular Infrastructure Drives Flexible Pipe Demand in Data Centers

Flexible pipes and hoses are emerging as a dominant segment in the data center piping market, accounting for approximately 28.2% of the market share, driven by their adaptability and ease of installation. These systems are widely used in modern data centers where complex layouts and space constraints require flexible routing solutions. Their ability to reduce the number of joints minimizes potential leak points while enhancing system reliability. Additionally, flexible pipes support faster deployment, aligning with the growing demand for modular and prefabricated infrastructure.

The segment is further strengthened by ongoing innovation tailored to high-density cooling requirements. In March 2025, Gates Corporation launched Data Master MegaFlex, a large-diameter flexible cooling hose designed for high-flow liquid cooling systems in data centers, improving installation flexibility and thermal efficiency. Such advancements highlight the increasing role of flexible piping in enabling next-generation liquid cooling architectures. As data centers transition toward AI-driven workloads, demand for high-performance, scalable hose solutions is expected to accelerate further.

Rising Focus on Energy Efficiency and Rapid Deployment Drives Pre-Insulated Pipe Adoption in Data Centers

Pre-insulated pipes are emerging as the fastest-growing segment in the data center piping market due to their superior thermal efficiency and energy-saving capabilities. These pipes minimize heat loss during chilled water circulation, supporting sustainability and reducing operating costs in high-performance data centers. They are especially suitable for hyperscale and modular facilities, where long pipe runs and consistent temperature control are critical. The adoption of pre-insulated piping also enables quicker installation and maintenance, aligning with the trend toward plug-and-play infrastructure.

In April 2024, BRUGG Pipes, a Switzerland‑based pipe systems manufacturer, in collaboration with Rovanco Piping Systems, began production of its first pre-insulated flexible pipe at a new U.S. facility in Joliet, Illinois, strengthening its presence in North America and enhancing supply for energy-efficient thermal transport applications. The combination of energy efficiency, rapid deployment, and strategic regional production positions pre-insulated pipes as a key enabler for next-generation data centers, particularly those adopting modular and liquid-cooling architectures.

3 Fast Growing Use Cases

Direct to Chip Liquid Cooling Piping

Direct to chip liquid cooling piping is becoming a fast growing use case as AI servers create higher heat loads than air cooling can handle efficiently. These systems require reliable fluid distribution close to processors and accelerators, which increases the importance of leak resistant materials and precise flow control. Growth will be strongest in hyperscale and AI focused data centers where rack densities continue to rise. Flexible hoses and engineered piping assemblies will gain share because they support tighter routing and faster installation. The market is moving toward standardized liquid cooling loops with stronger monitoring and serviceability.

Prefabricated Modular Piping Systems

Prefabricated modular piping systems are expanding quickly because data center developers need faster construction and consistent quality across multiple sites. Off site fabrication reduces installation errors and lowers dependency on skilled labor at crowded project locations. These systems are especially valuable for hyperscale campuses and colocation facilities that follow repeatable design templates. Growth will accelerate as operators standardize cooling infrastructure for phased expansion. Pre engineered skids and modular pipe assemblies will become central to faster commissioning. Suppliers with strong fabrication capacity and regional delivery capability will gain advantage as data center build cycles become more compressed.

Chilled Water and Heat Rejection Networks

Chilled water and heat rejection piping remains a fast growing use case as large data centers require efficient movement of cooling fluids across equipment rooms, cooling towers and heat exchangers. Demand is rising as facilities scale power capacity and shift toward higher thermal loads. Pre insulated pipes are gaining importance because they reduce heat loss and support energy efficient operation. Growth will be strongest in large campuses with long pipe runs and high cooling intensity. The market is moving toward more efficient distribution networks with better monitoring and lower lifecycle cost. Reliability and thermal performance will define supplier selection.

Geographical Penetration

Strategic Infrastructure Expansion in North America

North America is a dominant region in the global data center piping market, holding approximately 35% share in 2025. The region’s growth is driven by hyperscale and AI-focused data center deployments, requiring advanced cooling and liquid distribution systems.

For example, in March 2026, Perma-Pipe International Holdings, Inc., a U.S.-based piping solutions company, announced a strategic expansion by establishing a new facility in the U.S. Northeast, aimed at serving rapidly growing AI-driven data centers and providing specialized thermal management solutions for high-density computing environments. This expansion strengthens local supply chains and supports faster deployment of modular and pre-insulated piping systems across North American facilities.

US Data Center Piping Market Insights

The United States is the largest single-country market in the global data center piping industry. Growth is driven by hyperscale and AI-focused data center deployments, which require advanced liquid and modular cooling systems.

For example, in March 2026, Ecolab agreed to acquire CoolIT Systems for approximately $4.75 billion to expand into advanced liquid cooling systems, a key part of the fluid distribution and thermal management landscape supporting high-density data centers in North America. This acquisition strengthens Ecolab’s capabilities to provide integrated thermal solutions, including flexible and pre-insulated piping systems, enabling faster deployment and greater efficiency for hyperscale and enterprise facilities.

Canada Data Center Piping Industry Growth

Canada is increasingly emerging as a strategic market within the global data center infrastructure landscape, contributing to North America’s dominance with growing investments in data center capacity and advanced cooling systems. The expansion of large‑scale facilities is driving demand for robust piping and thermal management solutions to support high‑density and AI workloads.

For example, in December 2025, Technologies New Energy partnered with Data District to support the development of a 1 GW data center pipeline in Alberta, Canada, including AI‑ready facilities with modern cooling and infrastructure needs. The initiative covers multiple projects planned in the province and underscores the rising importance of scalable piping and liquid cooling systems in Canada’s data center ecosystem.

Data Center Piping Market - Sustainability Analysis

Sustainability is becoming a critical focus in data center design, with advanced piping systems playing a key role in reducing environmental impact. Closed-loop liquid cooling, which circulates coolant through sealed piping networks, minimizes water consumption compared to traditional evaporative systems. These systems also improve energy efficiency by maintaining precise thermal management and reducing waste. Adoption of modular and pre-insulated piping further supports sustainable construction and efficient operation of high-density data centers.

For instance, in February 2026, Oracle deployed direct-to-chip closed-loop cooling systems at its AI data centers, enabling continuous coolant recirculation without additional water draw. This approach reduces potable water use, supports efficient thermal management, and highlights the role of advanced piping in sustainable data center operations. Overall, integrating closed-loop and high-efficiency piping solutions is key to achieving energy- and water-efficient facilities while meeting growing computational demands.

Competitive Landscape

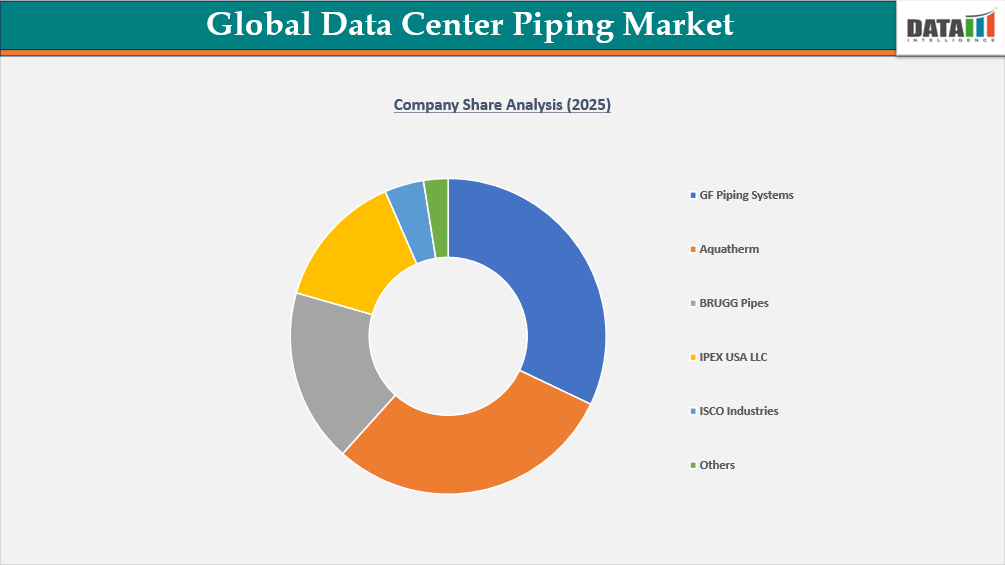

- The global data center piping market is characterized by a competitive landscape that includes both established and regional players.

- Key players include GF Piping Systems, Aquatherm, BRUGG Pipes, IPEX USA LLC, ISCO Industries, Victaulic Company, Hayward Industries, Inc., Watts EMEA Holding B.V., Valex, Harrington Industrial Plastics LLC, Collins Companies, Inc., Parker Hannifin Corp, Fixotec, Future Pipe Industries, and Agru Kunststofftechnik GmbH.

Key Developments

- In December 2025, Vertiv Group Corp. acquired PurgeRite Intermediate LLC, broadening its thermal management services portfolio, including liquid cooling, a key area influencing related piping and coolant distribution systems.

- In December 2025, industrial giant ABB partnered with OctaiPipe to accelerate the adoption of AI‑optimized cooling solutions, enhancing energy efficiency tied to fluid distribution, which will likely strengthen demand for flexible and advanced pipeline systems in data centers.

Thermal Infrastructure Pain Points and How to Overcome Them

Data center piping has become a critical infrastructure layer as AI workloads push facilities toward higher rack densities and more demanding thermal loads. Traditional chilled water layouts are under pressure because cooling distribution must support liquid cooling loops, direct to chip systems and immersion cooling networks with higher reliability. The main operating pain points are installation complexity, leak risk, energy loss and limited scalability during phased data center expansion. The strongest business action is to shift toward prefabricated piping, flexible hoses, pre insulated pipes and modular distribution skids. These solutions reduce installation time and improve repeatability across hyperscale and colocation campuses. Leak sensitive environments require stronger material selection, pressure testing, sensor enabled monitoring and redundant routing. Market demand is strongest where AI deployments require faster commissioning and thermal systems must scale without increasing operational risk.

Country Opportunity Scoreboard

The country opportunity scoreboard places the United States at the highest opportunity level because of hyperscale construction, AI focused data center investment and advanced liquid cooling adoption. Canada follows as a strong North American growth market, supported by large power availability, cold climate advantages and expanding AI ready campus development. China and India lead Asia Pacific growth because both markets are scaling digital infrastructure and cloud capacity. China shows stronger near term readiness due to larger data center clusters and advanced cooling investment. India shows rising future potential as cloud regions expand and domestic data localization accelerates. Europe remains attractive in markets with strict energy efficiency requirements and mature colocation demand. The highest scoring countries combine strong data center construction pipelines and liquid cooling readiness. Markets with weaker contractor capability and lower availability of advanced piping suppliers will face slower adoption.

Adoption Maturity Curve

The data center piping market is moving through four maturity levels. The first level is conventional cooling distribution, where facilities rely on rigid chilled water piping and standard mechanical room layouts. The second level is modular piping adoption, where operators use prefabricated sections and flexible hoses to shorten construction timelines. The third level is liquid cooling readiness, where piping systems support direct to chip cooling, higher flow rates, leak detection and tighter thermal control. The fourth level is intelligent fluid infrastructure, where piping networks connect with monitoring systems, energy optimization tools and predictive maintenance platforms. Most hyperscale and colocation facilities are moving from modular piping adoption to liquid cooling readiness. AI data centers are advancing fastest because thermal density is forcing a structural shift in cooling architecture. The next market phase will favor suppliers with modular design capability and liquid cooling integration expertise.

ROI and Total Cost Analysis

The ROI case for advanced data center piping is driven by faster deployment, lower installation error, improved energy efficiency and stronger cooling reliability. Prefabricated piping reduces on site labor dependency and shortens project timelines, which directly supports faster revenue generation for hyperscale and colocation operators. Pre insulated pipes reduce thermal loss across chilled water circulation and improve operating efficiency in large facilities. Flexible hoses lower routing complexity and reduce the number of joints in high density environments. Total cost analysis is shaped by material cost, installation time, leak protection, maintenance needs and future expansion flexibility. The strongest payback is achieved in AI data centers and large campuses where cooling infrastructure must scale quickly. Advanced piping carries higher upfront cost, but utilization value improves when it reduces commissioning delays and supports higher compute density.

Procurement Trigger Analysis

Procurement in data center piping is triggered by construction speed, thermal density, liquid cooling readiness and leak risk management. Hyperscale operators prioritize piping systems that support repeatable deployment across multiple campuses. Colocation providers focus on flexible infrastructure that can adapt to tenant requirements and changing rack densities. AI data center developers place higher value on high flow liquid cooling loops and reliable fluid distribution close to critical equipment. Mechanical contractors influence specifications when modular installation and labor efficiency become project priorities. Procurement teams place strong weight on pressure ratings, material compatibility, installation speed and supplier reliability. Leak risk remains a decisive buying factor because downtime in high value facilities carries major financial impact. Winning vendors will combine proven performance, local supply availability, prefabrication capability and strong technical support during design and commissioning.

Investor White Space Analysis

Investor white space is strongest in advanced piping systems that support liquid cooled and AI ready data centers. Pre insulated pipes offer growth potential because energy efficiency is becoming a core design requirement. Flexible hoses are gaining share because dense data center layouts need easier routing and faster installation. Prefabricated piping assemblies represent a high value opportunity as operators standardize modular construction across campuses. Software linked fluid monitoring is also becoming attractive because leak detection and predictive maintenance are critical in high value environments. The most attractive investment areas sit at the intersection of thermal efficiency and deployment speed. Companies with regional manufacturing, data center customer access, liquid cooling partnerships and engineering support will attract stronger strategic interest. Consolidation is likely as larger infrastructure and thermal management players look for specialized piping capabilities that strengthen their data center offering.

Competitive Moat and Vendor Positioning Scorecard

Vendor positioning in data center piping is defined by material performance, installation speed, leak reliability and liquid cooling compatibility. Strong vendors have proven solutions across flexible hoses, pre insulated pipes, stainless steel systems and engineered plastic piping. The highest value suppliers offer prefabrication support and design coordination with mechanical contractors. Competitive advantage also depends on regional manufacturing because data center projects require fast delivery and reliable supply continuity. Vendors serving AI data centers must handle higher flow requirements and tighter thermal performance standards. Partnerships with liquid cooling providers and data center engineering firms are becoming a major moat. Companies with strong testing protocols and field support will outperform suppliers that compete mainly on product availability. The market is shifting toward engineered fluid distribution platforms where quality assurance and technical integration drive vendor selection.

Funding, Partnership and M&A Tracking

Funding, partnership and M&A activity in data center piping is being shaped by the rapid rise of AI infrastructure and liquid cooling. Strategic buyers are targeting companies that can strengthen thermal management, fluid distribution and modular data center construction. Partnerships between piping suppliers, cooling technology firms and electrical infrastructure providers are increasing as operators demand integrated deployment models. Acquisitions in liquid cooling and thermal services signal rising value across the broader fluid infrastructure ecosystem. Capital is moving toward businesses that reduce construction timelines and improve cooling efficiency. Regional manufacturing expansion is also becoming strategically important as operators seek shorter supply chains and faster project execution. The strongest deal activity will center on pre insulated piping, flexible cooling hoses, modular piping skids and monitoring enabled distribution systems. Strategic value will concentrate around suppliers embedded in hyperscale and AI data center pipelines.

What You Get Compared with Competitors

| Dimension | Traditional Market Research | DataM Intelligence |

| Product | Static PDF reports covering broad data center infrastructure trends with limited visibility into piping systems, liquid cooling loops and modular installation models | Custom dashboards for data center piping with interactive views across pipe type, material, application, data center type and region |

| Data Age | 6 to 12 months old with historical snapshots of data center construction and limited updates on liquid cooling deployments | Living data with continuous updates on AI data centers, liquid cooling adoption, prefabricated piping activity and supplier moves |

| Engagement | One time transaction with limited follow up after delivery of market size, segmentation and company data | Continuous partnership with analyst support to track data center capacity expansion, vendor moves, investment activity and procurement triggers |

| Output | Raw market information with limited guidance on data center piping strategy and thermal infrastructure decisions | Actionable insights with clear recommendations for market entry, product positioning, customer targeting and investment evaluation |

| Customization | One size fits all syndicated templates with limited tailoring for data center type, cooling architecture, country readiness or installation model | Tailored solutions through DMI Insights and DMI Connect built around each client context with 81% of our clients choosing a customized solution |

| Market Depth | General coverage of data center infrastructure with limited detail on flexible hoses, pre insulated pipes, chilled water distribution and direct to chip liquid cooling | Focused intelligence on data center piping across applications, adoption maturity, ROI drivers and white space opportunities |

| Decision Support | Limited ability to compare countries, applications, suppliers and procurement readiness in one view | Dashboard based comparison of country opportunity, adoption maturity, vendor positioning and investment attractiveness |

| Investor View | Limited insight into funding activity, partnerships, recurring revenue models and acquisition potential | Investor focused tracking of white space, vendor moats, partnership moves and scalable revenue opportunities |

| Retention | Low chance of re engagement once the report is delivered | Over 35% of our clients are repeat customers due to ongoing updates, customization and long term decision support |

Why Choose DataM?

- Data-Driven Insights: Dive into detailed analyses with granular insights such as pricing, market shares, and value chain evaluations, enriched by interviews with industry leaders and disruptors.

- Post-Purchase Support and Expert Analyst Consultations: As a valued client, gain direct access to our expert analysts for personalized advice and strategic guidance, tailored to your specific needs and challenges.

- White Papers and Case Studies: Benefit quarterly from our in-depth studies related to your purchased titles, tailored to refine your operational and marketing strategies for maximum impact.

- Annual Updates on Purchased Reports: As an existing customer, enjoy the privilege of annual updates to your reports, ensuring you stay abreast of the latest market insights and technological advancements. Terms and conditions apply.

- Specialized Focus on Emerging Markets: DataM differentiates itself by delivering in-depth, specialized insights specifically for emerging markets, rather than offering generalized geographic overviews. This approach equips our clients with a nuanced understanding and actionable intelligence that are essential for navigating and succeeding in high-growth regions.

- Value of DataM Reports: Our reports offer specialized insights tailored to the latest trends and specific business inquiries. This personalized approach provides a deeper, strategic perspective, ensuring you receive the precise information necessary to make informed decisions. These insights complement and go beyond what is typically available in generic databases.

Target Audience

- Manufacturers/ Buyers

- Industry Investors/Investment Bankers

- Research Professionals

- Emerging Companies

Closest related market reports

1. Data Center Liquid Cooling Market

This is the most directly related report because piping systems are a core part of liquid cooling infrastructure (coolant distribution, loops, heat exchange).

- Covers direct-to-chip cooling

- Immersion cooling

- Chilled water systems

- Strong overlap with piping, valves, and fluid distribution systems