Cooling Distribution Unit Market Definition & Overview

What is the Cooling Distribution Unit Market?

The Cooling Distribution Unit Market covers engineered systems that circulate, filter, control, monitor and isolate coolant loops used to remove heat from data center servers, AI accelerators, high performance computing racks and edge compute systems. A CDU connects facility water or heat rejection infrastructure to technology cooling loops through pumps, heat exchangers, valves, sensors and controls. The market includes rack mounted, row based, facility side and modular units used with direct to chip liquid cooling and immersion cooling. Demand is tied to rising rack power density, thermal reliability needs, energy efficiency goals and the shift from air cooling toward liquid based architectures.

Cooling Distribution Unit Industry Background & Evolution

Parent market background: The parent market is data center thermal management, which evolved from room level air conditioning toward precision cooling, containment, rear door heat exchange and liquid cooling. From 2015 to 2019, hyperscale cloud growth increased thermal density but air cooling remained dominant. From 2020 to 2022, GPU acceleration and HPC clusters increased adoption of direct liquid cooling pilots. From 2023 to 2025, AI training racks moved beyond conventional air cooling limits, making CDUs a key control layer between IT loops and facility infrastructure. From 2026 onward, the market is expected to evolve toward standardized warm water loops, intelligent controls, service based fluid management and integrated power cooling packages.

Historical Cooling Distribution Unit Market Trend Analysis

Over the last five years, the market shifted from experimental liquid cooling deployments to repeatable commercial procurement. AI accelerators, dense GPU servers and sovereign cloud projects exposed the limits of traditional air cooling, especially in racks exceeding 40 kW. Colocation operators began offering liquid ready halls, while hyperscalers pushed suppliers toward higher capacity CDUs with redundancy, leak detection and remote monitoring. Supply chains also changed as cooling vendors integrated pumps, manifolds, controls and service support into pre engineered platforms. The historical impact has been a higher average selling price per thermal management system, shorter qualification cycles with chip vendors and stronger demand for field service capability. Retrofits became important because many existing data centers needed liquid cooling without rebuilding full mechanical plants.

Cooling Distribution Unit Growth Outlook Summary

Short term growth will be driven by AI data center construction, accelerated GPU adoption and colocation providers racing to support high density tenants. Mid term growth will depend on standardized direct to chip designs, facility water quality management, modular deployment methods and stronger integration with power infrastructure. Long term growth toward 2035 will be shaped by warm water loops, heat reuse, digital commissioning and full lifecycle fluid services. The market outlook is strong because CDUs sit at the operating boundary between IT hardware and facility cooling, making them critical for reliability, energy use and compute density. Pricing may remain premium in the near term because supply capacity, qualified components and service technicians are constrained. By 2035, the market is expected to be more platform based, with larger players bundling CDU hardware, controls, chemistry, commissioning and maintenance into managed thermal infrastructure offerings.

Cooling Distribution Unit Market Key Takeaways

- Liquid to Liquid CDU is the largest segment because it enables efficient heat transfer between facility and technology cooling loops.

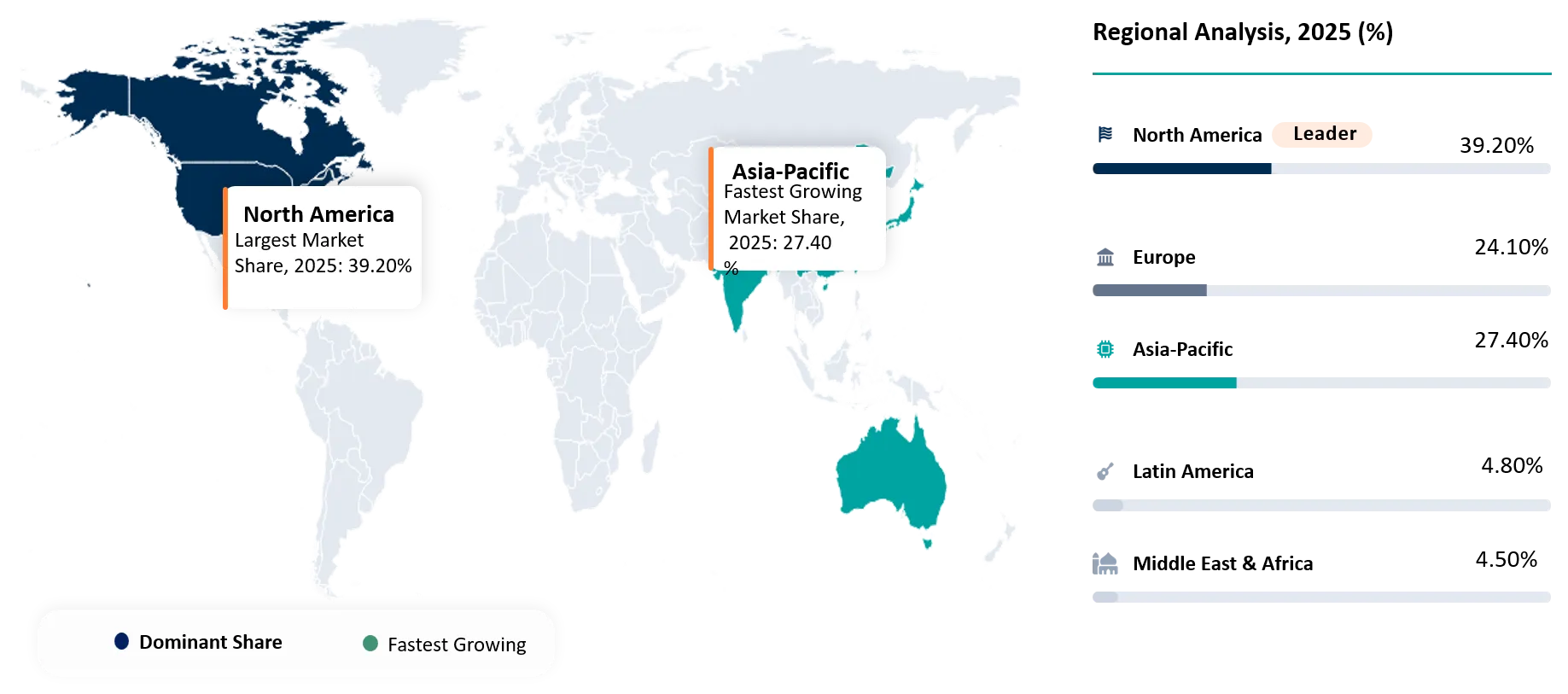

- North America is the largest region because hyperscale AI buildout, cloud capex and early liquid cooling adoption are concentrated there.

- In Rack CDU is the fastest growing segment because AI clusters need localized thermal control close to dense servers.

- Asia Pacific is the fastest growing region because sovereign AI, semiconductor ecosystems and data localization are accelerating high density data center investment.

- The strongest market advantage is shifting from standalone equipment supply toward integrated cooling design, controls, commissioning and service capability.

- Buyers increasingly evaluate CDUs as uptime infrastructure because coolant quality, pump redundancy and sensor accuracy influence server availability.

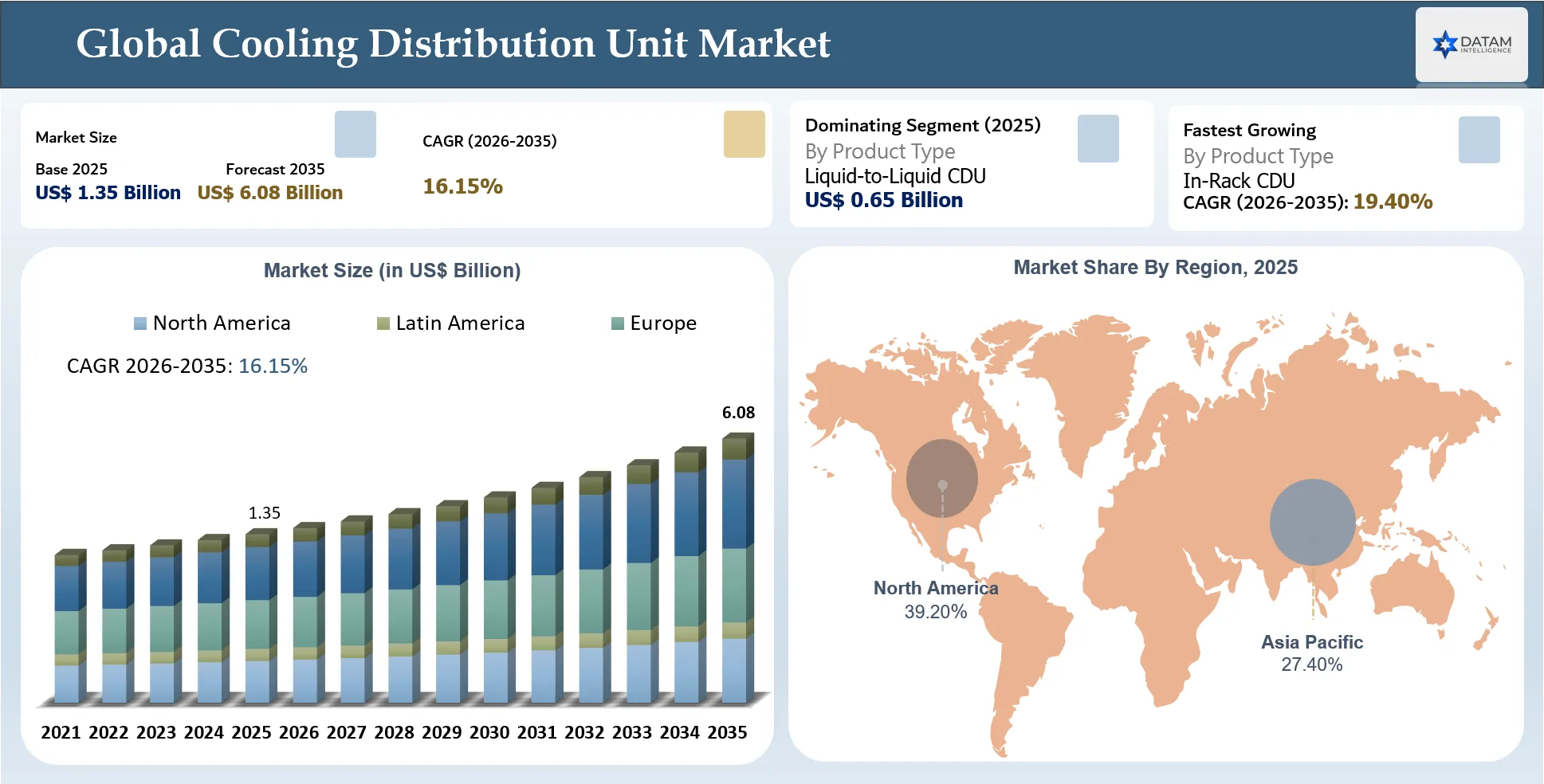

Cooling Distribution Unit Market Snapshot

| Metric | Details |

| Market Report Name | Cooling Distribution Unit Market |

| Global Market Size 2025 | USD $1.35 Billion |

| Projected Market Size 2035 | USD $6.08 Billion |

| CAGR 2026-2035 | 16.15% |

| Largest Segment Name | Liquid to Liquid CDU |

| Largest Segment Share | 47.80% |

| Fastest Growing Segment Name | In Rack CDU |

| Fastest Growing Segment Share/CAGR | 19.40% |

| Largest Region Name | North America |

| Largest Region Share | 39.20% |

| Fastest Growing Region Name | Asia Pacific |

| Fastest Growing Region Share/CAGR | 18.70% |

| Geographic Market Share for the 5 Regions | North America: 39.20%, Europe: 24.10%, Asia Pacific: 27.40%, Latin America: 4.80%, Middle East and Africa: 4.50% |

| Top Companies | Vertiv, Schneider Electric, CoolIT Systems, nVent Electric, Boyd, Delta Electronics, Envicool, STULZ, Nortek Air Solutions, Asetek |

Cooling Distribution Unit Market White Space & Investment Opportunities

White space opportunities highlight underserved areas where CDU suppliers can differentiate through retrofit kits, fluid analytics, heat reuse interfaces, regional service hubs, and standardized commissioning packages.

- Standardized retrofit CDU kits are underserved because many brownfield data centers need compact units, flexible piping and simplified commissioning. Investment can unlock enterprise and regional colocation demand.

- Fluid analytics platforms are underdeveloped compared with hardware. Vendors that combine sensors, chemistry data and predictive models can capture recurring service revenue.

- High temperature heat reuse interfaces remain a white space as operators seek to monetize waste heat. CDUs designed for stable warm water operation can support district energy partnerships.

- Regional manufacturing and service hubs are receiving investment because hyperscale customers need shorter lead times, spare parts availability and trained technicians near major data center clusters.

Cooling Distribution Unit Market Procurement & Buyer Behavior Analysis

Procurement behavior is becoming more technical because buyers evaluate CDUs as uptime critical infrastructure. Selection criteria now include thermal performance, redundancy, integration risk, service support and lifecycle cost rather than simple equipment price.

Cooling Distribution Unit Market Buyer Decision-Making Criteria

Buyers prioritize proven performance, deployment speed and operating assurance because CDUs protect high value compute assets. Procurement teams increasingly involve facilities engineers, IT hardware teams, sustainability leaders and risk managers.

- Cooling capacity matched to current and future rack density

- Redundant pumps, valves, sensors and controls

- Compatibility with server cold plates, manifolds and coolant chemistry

- Leak detection, isolation and alarm integration

- Ease of maintenance, filtration access and bypass design

- Digital monitoring, data logging and DCIM integration

- Supplier lead time, spare parts availability and field service coverage

- Total lifecycle cost including commissioning and coolant management

Cooling Distribution Unit Market Economic & Investment Analysis

Economic and investment analysis shows a market shaped by AI capex, data center construction cost, power availability and consolidation around liquid cooling expertise.

Cooling Distribution Unit Market Macroeconomic Impact Factors

Macroeconomic conditions affect the market through data center capital spending, interest rates, energy costs, supply chain inflation and AI investment cycles. High interest rates can delay speculative colocation builds, but AI driven demand has kept strategic projects moving because compute capacity is tied to competitive advantage. Energy prices strengthen the case for efficient cooling because liquid systems can reduce fan power and support warmer operating loops. Component inflation affects pumps, controls, heat exchangers and stainless assemblies, which can lift average selling prices. Supply chain localization is becoming more important as hyperscale buyers demand predictable lead times. The broader economic impact is positive because CDUs help unlock higher compute density per square foot and per megawatt, improving revenue potential for data center operators despite higher upfront costs.

Cooling Distribution Unit Market Investment Trends in the Market

Investment is shifting from standalone cooling equipment toward integrated liquid cooling platforms, service capability and acquisitions of specialist suppliers.

- Advanced CDU manufacturing and regional assembly capacity

- Fluid management, chemistry and predictive maintenance platforms

- Direct to chip cooling ecosystems that include CDUs, manifolds and cold plates

- Retrofit kits for brownfield data centers and liquid ready colocation halls

Cooling Distribution Unit Market Funding & M&A Activity

Funding and M&A are expected to focus on specialist liquid cooling firms, component suppliers, service platforms and companies with validated hyperscale relationships. Larger infrastructure players want to own more of the cooling stack as AI data center spending accelerates.

- March 2026: Ecolab agreed to acquire CoolIT Systems for $4.75 billion, backed by a strategy to combine liquid cooling technology with water, chemistry and service capabilities.

- February 2025: Schneider Electric completed the acquisition of a controlling interest in Motivair, strengthening its advanced thermal management portfolio for HPC and AI workloads.

- 2025: Liquid cooling specialists attracted strategic interest as investors recognized the high value of supplier qualification with cloud and AI infrastructure buyers.

- 2026 outlook: M&A is expected to target CDU controls, fluid analytics and regional service capabilities because recurring revenue is becoming more important.

Cooling Distribution Unit Market Regulatory & Policy Analysis

Regulatory pressure is indirect but powerful because CDUs support energy efficient data center cooling. Key rules focus on data center energy reporting, environmental performance, water footprint and equipment safety. In Europe, the Energy Efficiency Directive requires monitoring and reporting of energy performance for significant data centers, raising interest in cooling efficiency and operational transparency. In the United States and Asia, policies around AI infrastructure, grid capacity and water stewardship influence project design.

- 2025: EU data center reporting obligations strengthen attention on energy and water metrics, improving demand for monitored cooling systems.

- 2025: Sustainability scrutiny around large data center approvals increases focus on efficient cooling and water conscious designs.

- 2026: AI infrastructure efficiency frameworks are expected to raise buyer interest in measurable power and cooling performance.

Cooling Distribution Unit Market Regulatory Framework Overview

The regulatory framework for the cooling distribution unit market is shaped by data center energy efficiency rules, water management expectations, electrical safety standards and facility codes. CDUs must operate within pressure, coolant compatibility, controls and safety requirements set by data center design standards and customer specifications. The EU Energy Efficiency Directive creates a clear push toward energy performance reporting, while ASHRAE guidance helps define liquid cooling design and operating practices. Environmental scrutiny also influences whether operators choose warm water loops, dry coolers and heat reuse. These frameworks do not mandate CDUs directly, but they increase the value of monitored and efficient liquid cooling infrastructure.

Cooling Distribution Unit Policy Impact on Market Growth

Government policy supports market growth when it encourages efficient data centers, AI infrastructure and lower environmental impact. Policy pressure also raises the importance of verified cooling performance.

- EU energy reporting rules increase demand for monitored CDU platforms that can support facility efficiency documentation.

- Public investment in AI and digital infrastructure supports new high density data center construction, increasing liquid cooling demand.

- Water stewardship policies encourage warm water and dry cooling architectures, making advanced CDU design more valuable.

- Grid constraint policies push operators toward higher compute density per megawatt, supporting liquid cooling adoption.

Cooling Distribution Unit Market Trends & Innovation Landscape

The innovation landscape is moving from basic coolant circulation toward intelligent thermal infrastructure. Buyers now compare CDU platforms by capacity, redundancy, control accuracy, serviceability, fluid management and integration with broader data center power and cooling systems.

Cooling Distribution Unit Key Market Trends

CDU adoption is moving fastest where compute density is changing facility economics. The most visible trends are liquid ready colocation offerings and high-capacity AI pods, both of which require repeatable cooling designs and stronger operational controls.

- Liquid ready colocation halls are expanding as tenants demand AI capable capacity without owning infrastructure. This increases demand for standardized row and facility CDUs.

- High-capacity rack cooling is gaining share because GPU clusters require local flow control and faster commissioning.

- Warm water operation is rising as operators seek lower chiller use and more heat rejection flexibility.

- Integrated power and cooling procurement is increasing because AI campuses need coordinated electrical and thermal design.

Cooling Distribution Unit Market Technology Advancements

Technology development is focused on capacity, reliability and digital control because CDU failure can affect high value compute workloads. Recent innovations show a move toward modular platforms and closer chip level cooling alignment.

- June 2025: Vertiv expanded the CoolChip CDU 70, 100 and 600 family in EMEA, improving scalable direct to chip cooling options for AI and HPC deployments.

- November 2025: nVent introduced modular liquid cooling and power solutions with enhanced row and rack CDUs for current and future chip requirements.

- September 2025: Schneider Electric unveiled a liquid cooling portfolio with Motivair including CDUs, rear door heat exchangers and technology cooling loops.

- 2026: Advanced microchannel and chip level cooling research is increasing demand for CDUs with tighter flow and temperature control.

Cooling Distribution Unit Industry Transformation Trends

The industry is transforming from equipment procurement toward thermal infrastructure platforms. CDU vendors are combining hardware, controls, service, fluid chemistry and installation support. Data center buyers increasingly want qualified ecosystems rather than isolated components because server warranties, facility water quality and uptime requirements are interconnected.

Disruption Analysis of Cooling Distribution Unit Market

Disruption is being driven by AI compute density and the migration from room-based cooling to rack and chip adjacent heat capture. This affects facility design, supply chains and procurement models. Large infrastructure vendors are acquiring or partnering with specialists to control more of the liquid cooling stack. Smaller niche vendors can still win with speed, customization and engineering depth, but scaled buyers increasingly prefer globally supported platforms. The market is also disrupted by sustainability reporting because operators must manage energy and water impact more visibly. CDUs that support warm water loops, dry cooling and heat reuse can shift from optional technology to core infrastructure.

Cooling Distribution Unit Market Disruption & Structural Shift Analysis

Structural change is centered on the shift from air cooling dominated design to liquid enabled compute infrastructure. CDUs are becoming strategic assets because AI capacity depends on thermal design readiness.

Technology Disruption Impact on Cooling Distribution Unit Market

Technology disruption is visible in two areas: higher power chips and smarter cooling control. Both trends make CDUs more important in facility planning and supplier selection.

- High power GPUs are disrupting data center design because rack thermal loads exceed traditional air cooling assumptions. CDUs enable liquid heat capture close to the server, allowing denser compute deployment.

- Intelligent controls are disrupting operations because CDU telemetry supports predictive maintenance, optimized flow control and faster fault detection. This shifts value from mechanical equipment to digital thermal management.

Cooling Distribution Unit Future Market Transformation

By 2035, the CDU market will likely transform into a lifecycle service market. Hardware will still matter, but buyers will increasingly pay for thermal assurance, fluid quality management, predictive maintenance and sustainability performance. CDUs will integrate with data center infrastructure management platforms, server telemetry and energy reporting systems. Vendors will differentiate through data, uptime guarantees, regional service networks and standardized deployment kits. Business models may include performance based contracts where suppliers manage cooling loops over the asset life. This will favor companies that combine hardware scale with software, chemistry and field service capability.

Cooling Distribution Unit Market Growth Dynamics

Growth dynamics are defined by the mismatch between compute density and legacy air cooling capacity. The market benefits when AI racks require direct heat capture, when operators need lower power usage effectiveness and when colocation providers commercialize liquid ready capacity.

Cooling Distribution Unit Market Drivers

- AI and HPC rack density is pushing operators toward liquid cooling because conventional air systems struggle above high power thresholds. CDUs become essential because they control flow, pressure, heat exchange and water quality between IT hardware and facility loops.

- Hyperscale and colocation expansion is creating repeatable demand for standardized CDU platforms. Large operators want scalable units that can be deployed across regions with predictable serviceability, redundancy and control integration.

- Energy efficiency pressure is driving CDU adoption because liquid cooling can reduce fan energy and improve heat rejection efficiency. Operators seeking lower power usage effectiveness are treating CDU design as part of the core efficiency strategy.

- Hardware vendor liquid cooling roadmaps are accelerating procurement because next generation GPUs and accelerators increasingly assume liquid capable data center infrastructure. This makes CDUs a prerequisite for future server deployments.

Cooling Distribution Unit Market Driver Impact Assessment

| Driver | Market Growth Impact (%) | Demand Concentration | Impacted Use Case | Strategic Impact |

| AI rack density | 5.80% | Hyperscale AI clusters and HPC centers | Direct-to-chip cooling for dense GPU racks | Increases demand for high-capacity, redundant coolant distribution units (CDUs) capable of supporting mission-critical AI infrastructure. |

| Liquid-ready colocation expansion | 4.60% | North America and Europe colocation campuses | Tenant-ready high-density data halls | Shifts procurement toward modular, scalable, and standardized CDU designs that simplify deployment and accommodate diverse customer requirements. |

| Energy efficiency targets | 3.90% | Operators facing power constraints and sustainability reporting requirements | Reduced fan power consumption and warm-water cooling | Encourages adoption of digitally monitored, energy-efficient CDUs compatible with heat reuse and sustainability initiatives. |

| Chip vendor thermal roadmaps | 3.50% | GPU server OEMs and cloud service providers | Qualification of liquid-cooled AI servers | Strengthens collaboration requirements between CDU manufacturers, server OEMs, and semiconductor vendors to ensure compatibility with next-generation liquid cooling platforms. |

Cooling Distribution Unit Market Restraints

- High upfront cost limits adoption among smaller enterprise data centers because liquid loops require CDUs, manifolds, facility connections and trained maintenance teams. This slows replacement cycles in sites with moderate rack density.

- Integration complexity restrains deployment because facilities must align water quality, pressure control, leak detection and server warranty requirements. Poor integration increases commissioning time and raises operational risk.

- Supply chain constraints affect pumps, valves, heat exchangers and control electronics. Long lead times can delay data center build schedules and push operators toward suppliers with larger manufacturing footprints.

- Skills shortages restrict adoption because liquid cooling maintenance requires mechanical, electrical and controls expertise. Operators without trained staff may delay CDU projects until service partners are secured.

Cooling Distribution Unit Market Restraint Impact Assessment

| Restraint | Drag on Market Growth (%) | Primary Impact Area | Impacted Use Case | Strategic Impact |

| High upfront cost | 3.80% | Enterprise and smaller colocation retrofits | Low- to mid-density data halls | Slows adoption of liquid cooling solutions beyond AI and HPC environments due to significant initial capital investment. |

| Integration complexity | 3.40% | Facility design and commissioning | Direct-to-chip liquid cooling deployments | Increases demand for specialized engineering expertise, system integration services, and vendor qualification to ensure reliable implementation. |

| Supply constraints | 2.90% | High-capacity CDUs and control components | Hyperscale data center deployments | Favors vertically integrated suppliers with stronger manufacturing capabilities and more resilient supply chains. |

| Operations skills gap | 2.40% | Service readiness and workforce capabilities | Ongoing coolant and fluid management | Drives demand for managed services, operator training, and maintenance support to ensure efficient system operation. |

Emerging Cooling Distribution Unit Growth Factors

Emerging growth factors show where CDU demand is expanding through AI rack density, predictive monitoring, OEM validation, higher coolant temperatures, and service led liquid cooling models.

- Direct partnerships with GPU server OEMs are becoming a growth factor because CDU compatibility must be validated with cold plates, manifolds and thermal design power targets.

- Higher capacity rack level units are gaining demand as AI racks move toward localized control and faster deployment. These products reduce piping complexity for certain high density pods.

- Digital twins and predictive maintenance are emerging because operators need early warning on pump wear, heat exchanger fouling, filter loading and coolant drift.

- Heat reuse compatible CDUs are gaining interest in Europe and dense urban campuses where waste heat can support district heating or nearby buildings.

Cooling Distribution Unit Market Segmentation Analysis

Segmentation is primarily shaped by how close the CDU sits to the rack, what cooling architecture it supports and how much thermal capacity it controls. The highest value segments are tied to dense AI and HPC workloads.

Cooling Distribution Unit Market by Type Trends

Liquid to Liquid CDUs dominate type based demand because they provide efficient heat transfer and control between facility and IT loops. The trend is toward rack, row and facility variants that can be mixed inside the same campus. Growth is strongest where AI operators need scalable cooling blocks, redundant pumps and precise flow control. The market is headed toward platform families that let buyers start with localized deployments and later scale to facility distribution without changing the full control philosophy.

Cooling Distribution Unit Market by Cooling Type Trends

Direct to chip cooling is the most important cooling type because it aligns with GPU server roadmaps and high density AI training requirements. The segment is being shaped by cold plate compatibility, manifold design and fluid quality assurance. Immersion support is growing in selected workloads, yet direct to chip remains more widely adopted because it fits current server ecosystems. The market is headed toward hybrid halls where CDUs support multiple liquid cooling approaches under unified monitoring and maintenance practices.

Cooling Distribution Unit Market by End User Trends

Hyperscale and colocation customers account for the strongest demand because they deploy large blocks of AI capable capacity. The major trend is the commercialization of liquid ready data halls that can attract cloud, model training and enterprise AI tenants. Enterprise data centers are slower but important for private AI and research workloads. The market is headed toward differentiated service models where hyperscalers demand custom scale, while colocation operators demand flexible standardized CDU packages that can support varied tenant densities.

Cooling Distribution Unit Regional Market Analysis

Regional demand follows AI infrastructure intensity, hyperscale buildout, power availability and data center sustainability rules. North America leads current share, while Asia Pacific is expected to scale fastest through cloud, sovereign AI and semiconductor-linked demand.

North America Cooling Distribution Unit Market

North America is the largest Cooling Distribution Unit Market because hyperscale cloud platforms, AI model training clusters and advanced colocation campuses are concentrated in the United States and Canada. Demand is shifting from isolated liquid cooling pilots toward multi hall deployment strategies, especially around campuses designed for accelerated computing. Production capacity is strengthening through supplier expansion, regional assembly, acquisitions and deeper partnerships with server OEMs. The region also benefits from strong venture and private equity interest in thermal management, shown by major transactions involving liquid cooling specialists. Demand is changing from capacity procurement to lifecycle thermal management, with buyers asking for coolant quality monitoring, commissioning support, remote diagnostics and service level commitments. Power scarcity in key data center markets is making energy efficient cooling more valuable. By 2035, North America is expected to remain the revenue leader, although share may gradually normalize as Asia Pacific scales. The strongest opportunity is in liquid ready colocation and brownfield retrofits that need compact, repeatable CDU solutions.

Europe Cooling Distribution Unit Market

Europe is a high value market because data center operators face stronger energy transparency, water use and sustainability expectations. The EU Energy Efficiency Directive requires data center energy performance reporting, which increases attention on cooling efficiency and operational data. Demand is strongest in FLAP D markets, Nordic locations and emerging AI campuses where power availability and heat reuse potential influence site selection. Production and service capacity is improving as global vendors expand EMEA specific product availability and local support. European buyers are more likely to evaluate CDUs for warm water operation, heat reuse compatibility and environmental reporting support. Growth is supported by AI infrastructure investment, but permitting, power grid constraints and community scrutiny can slow projects.

Asia Pacific Cooling Distribution Unit Market

Asia Pacific is the fastest growing region because cloud capacity, semiconductor ecosystems, sovereign AI investment and digital services growth are converging. China, Japan, South Korea, India and Singapore linked markets are adopting liquid cooling for high density deployments as data center operators face land, power and thermal constraints. Production capacity is improving through electronics manufacturing strength, local component supply and regional system integrators. Demand is shifting from low density enterprise cooling toward AI ready colocation and cloud deployments. Local vendors are likely to gain share where customization, price competitiveness and short lead times matter. The region is expected to see strong growth in rack based and row based CDUs because operators need scalable systems for phased campus development.

Cooling Distribution Unit Market: Country-Level Analysis

Country-level demand is concentrated where AI compute, hyperscale cloud capacity, data localization and high density colocation investment are strongest. The United States leads, while China, Japan and India are major growth engines.

United States Cooling Distribution Unit Market Size/Forecast

The United States is the largest country market because AI training clusters, hyperscale data centers and advanced colocation campuses are expanding rapidly. Demand is concentrated in regions with cloud campuses, but power constraints are pushing operators to evaluate more efficient liquid cooling architectures. Production capacity is strengthening through acquisitions, supplier expansions and local service networks. Buyers are moving from experimental CDU deployments to standardized purchase programs that include commissioning, coolant management and telemetry. Growth through 2035 is expected to remain strong as GPU density rises and brownfield data centers add liquid ready pods. Procurement will favor vendors with proven uptime performance and quick field support.

Japan Cooling Distribution Unit Market Size/Forecast

Japan is a high potential market because data center operators face space constraints, energy efficiency pressure and rising AI workloads. Demand is led by cloud, telecom, financial services and advanced research computing. Production and integration capacity benefit from strong precision engineering and electronics supply chains, although large scale CDU deployments still depend on global vendor partnerships. The market is likely to favor compact, reliable systems that suit dense urban facilities and seismic design requirements. Growth through 2035 will be supported by sovereign AI initiatives, enterprise modernization and the need for energy efficient cooling in constrained sites. Service reliability and engineering documentation will be important buyer criteria.

China Cooling Distribution Unit Market Size/Forecast

China is one of the fastest scaling country markets because AI infrastructure, cloud services and domestic hardware ecosystems are driving dense data center demand. Demand is supported by large internet platforms, telecom operators and government backed digital infrastructure programs. Production capacity is strong because local manufacturers can supply components, systems and customized engineering at scale. The market is shifting from conventional air cooled data centers toward liquid cooling in large AI clusters and high performance computing environments. Growth through 2035 will be shaped by domestic chip evolution, energy efficiency targets and regional data center clustering. Local competition may pressure pricing while accelerating product innovation.

India Cooling Distribution Unit Market Size/Forecast

India is an emerging high growth country market because cloud adoption, digital public infrastructure, data localization and AI service demand are increasing data center investment. Most current facilities are still designed around air cooling, but high density workloads are pushing large colocation operators to plan liquid ready zones. Production capacity is improving through domestic electrical equipment manufacturing and foreign vendor partnerships, although advanced CDU systems remain import dependent in many projects. Growth through 2035 will be driven by hyperscale campuses, banking workloads, telecom cloud and enterprise AI. Buyers will prioritize cost effective systems, local service support and reliability in high ambient temperature conditions.

Cooling Distribution Unit Market Other Key Countries

Germany Cooling Distribution Unit Market: Germany is important due to Frankfurt data center density, strict energy rules and industrial cloud demand. Operators are evaluating CDUs for efficient high density cooling and potential heat reuse. United Kingdom Cooling Distribution Unit Market: The UK benefits from London colocation demand and AI infrastructure investment. CDU adoption is increasing in high density halls where power and cooling constraints limit traditional expansion. Singapore Cooling Distribution Unit Market: Singapore has land and energy constraints, making liquid cooling relevant for higher compute density. Regulatory pressure on data center efficiency supports advanced CDU adoption. South Korea Cooling Distribution Unit Market: South Korea benefits from semiconductor capability, cloud growth and AI infrastructure strategy. CDUs are gaining interest for dense GPU deployments. United Arab Emirates Cooling Distribution Unit Market: The UAE is investing in AI, sovereign cloud and smart city infrastructure. Hot climate conditions make efficient liquid cooling and reliable CDU service important for future data centers.

Cooling Distribution Unit Market Competitive Landscape

The competitive landscape is led by global data center infrastructure companies and specialist liquid cooling vendors. Competition is shifting from standalone CDU hardware toward full liquid cooling ecosystems that include controls, manifolds, service and fluid management.

- Vertiv

- Schneider Electric

- CoolIT Systems

- nVent Electric

- Boyd

- Delta Electronics

- Envicool

- STULZ

- Nortek Air Solutions

- Asetek

Cooling Distribution Unit Market Competitive Benchmarking

Benchmarking is increasingly based on platform breadth, thermal capacity, service depth and buyer segment fit. Major players are positioning around AI readiness, liquid cooling validation and global deployment capability. Vertiv: Strong portfolio across critical power, thermal management and CoolChip CDUs, targeting hyperscale, colocation, AI and HPC deployments. Schneider Electric: Uses Motivair assets to combine CDUs with broader data center infrastructure and services, targeting integrated AI factories. CoolIT Systems: Specialist in liquid cooling technology with strong data center and server ecosystem focus, strengthened by Ecolab fluid management strategy. nVent: Focuses on modular liquid cooling and power infrastructure, targeting chip aligned high density data center deployments.

Cooling Distribution Unit Market BCG Matrix List

Stars: Vertiv, Schneider Electric. Question Marks: nVent, Envicool. Cash Cows: STULZ, Nortek Air Solutions. Niche Players: Asetek, Delta Electronics.

Cooling Distribution Unit Market BCG Matrix Analysis

Stars such as Vertiv and Schneider Electric are placed in the highest position because they combine strong market visibility, broad data center portfolios, global service capability and active liquid cooling investment. Question Marks such as nVent and Envicool have strong growth exposure, but their position depends on how quickly they expand customer qualification and global support. Cash Cows such as STULZ and Nortek Air Solutions benefit from established thermal management relationships, yet their CDU growth depends on how aggressively they move into AI liquid cooling. Niche Players such as Asetek and Delta Electronics have important technical or component strengths, but they need broader ecosystem positioning to capture larger hyperscale programs. The matrix shows that market leadership will depend on scale, integration and service depth.

Cooling Distribution Unit Market Company Profiles & Strategy Analysis

Company strategy is being reshaped by AI infrastructure demand. Leading players are expanding portfolios, acquiring specialist capabilities and bundling CDU hardware with design, control software and service offerings.

Cooling Distribution Unit Market Expansion & Partnership Strategy

Expansion strategy is being driven by acquisitions, product launches and regional portfolio rollouts. The market is rewarding vendors that can control more of the liquid cooling stack and support global data center programs. February 2025: Schneider Electric completed the acquisition of a controlling interest in Motivair, strengthening liquid cooling and advanced thermal management for HPC. Impact: improves full stack AI data center cooling capability. June 2025: Vertiv launched expanded CoolChip CDU 70, 100 and 600 models in EMEA. Impact: increases regional access to scalable direct to chip cooling. November 2025: nVent introduced modular liquid cooling and power solutions at SC25. Impact: supports chip aligned row and rack CDU demand. March 2026: Ecolab agreed to acquire CoolIT Systems for $4.75 billion. Impact: combines liquid cooling technology with water, chemistry and service expertise.

Cooling Distribution Unit Market Key Developments 2025 to 2026

Developments show rapid portfolio expansion and consolidation around liquid cooling capability. These actions indicate that CDUs are becoming core infrastructure for AI data centers.

Cooling Distribution Unit Major Industry Developments

Recent developments are concentrated around acquisitions, product launches and portfolio integration. Each development points to stronger demand for full stack liquid cooling solutions.

- February 2025: Schneider Electric completed the acquisition of a controlling interest in Motivair, expanding HPC and advanced thermal management capability.

- June 2025: Vertiv launched CoolChip CDU 70, 100 and 600 in EMEA, increasing scalable direct to chip options.

- September 2025: Schneider Electric unveiled a liquid cooling portfolio with Motivair including CDUs and technology cooling loops.

- November 2025: nVent introduced modular liquid cooling and power solutions with enhanced row and rack CDUs.

- March 2026: Ecolab agreed to acquire CoolIT Systems for $4.75 billion, bringing fluid management and cooling technology together.

Cooling Distribution Unit Recent Market Announcements

March 2026: Ecolab announced an agreement to acquire CoolIT Systems for $4.75 billion. The announcement is important because it signals that liquid cooling is becoming a strategic market for water, chemistry and service companies as well as data center infrastructure vendors. CoolIT brings liquid cooling technology and hyperscale relevance, while Ecolab brings fluid management, global service and customer relationships. The impact is likely to be deeper competition around lifecycle cooling services, not just hardware. It may also accelerate M&A as other infrastructure companies look for specialist CDU, cold plate or fluid analytics capabilities.

Cooling Distribution Unit Market Technology Launches & Partnerships

Technology launches and partnerships are focused on making liquid cooling easier to deploy at scale. Recent activity emphasizes modular CDU families, end to end portfolios and chip aligned designs.

- June 2025: Vertiv expanded CoolChip CDU models in EMEA for scalable AI and HPC cooling.

- September 2025: Schneider Electric and Motivair portfolio integration added CDUs, cooling loops and high density data center services.

- November 2025: nVent introduced modular liquid cooling and power platforms with row and rack CDU options.

- March 2026: Ecolab and CoolIT transaction positioned fluid management as part of future CDU value creation.

Cooling Distribution Unit Market Strategic Insights & Analyst Perspective

Analyst perspective emphasizes that CDUs are becoming capacity enablers rather than peripheral cooling equipment. The strongest companies will combine hardware, digital controls, service and ecosystem validation.

Analyst Insights for Cooling Distribution Unit Market

From a DataM Intelligence perspective, the Cooling Distribution Unit Market is entering a strategic acceleration phase because AI infrastructure demand has changed the economics of thermal management. In 2025, CDUs are still purchased as a specialized liquid cooling component in many projects, but by 2035 they will function as a core operating layer for high density compute. The market will reward suppliers that can reduce deployment risk through validated designs, global service coverage and digital monitoring. Revenue growth will be supported by hyperscale AI campuses, liquid ready colocation halls and selective retrofits in enterprise data centers. The strongest margin opportunities will come from managed fluid services, predictive maintenance and integrated power cooling packages rather than equipment sales alone. Regional growth will remain strongest in North America and Asia Pacific, while Europe will push innovation in energy reporting, heat reuse and efficient cooling. The main risk is execution complexity because liquid cooling requires mechanical and IT teams to coordinate more closely. Overall, the market is headed toward consolidation, platform standardization and lifecycle service monetization.

Strategic Recommendations for Cooling Distribution Unit Market

Recommendation 1: Companies should develop modular CDU families that cover rack, row and facility Capacitys with a common control architecture. This strategy reduces engineering variation, improves manufacturing scale and helps customers deploy liquid cooling in phases. Vendors should pair these platforms with documented server compatibility, factory acceptance testing and commissioning templates. This will support hyperscale repeatability and make the offering easier for colocation operators to standardize across liquid ready halls. Recommendation 2: Companies should invest in lifecycle services around fluid quality, predictive maintenance and remote monitoring. Hardware margins may compress as more competitors enter the market, while recurring service revenue can deepen customer relationships and improve profitability. A strong service model should include coolant testing, filtration advice, spare parts programs, pump health analytics and emergency support. This positions the vendor as a thermal assurance partner rather than a box supplier.

Cooling Distribution Unit Future Market Outlook (2035 Vision)

In 2025, the market is still transitioning from early liquid cooling adoption to wider commercial deployment. Buyers are learning how to specify CDUs, qualify vendors and manage coolant loops. By 2035, the market will be much more standardized, service oriented and digitally managed. CDUs will be integrated into data center design from the first planning stage, especially for AI, HPC and high density colocation. The largest change will be business model maturity. Vendors will sell validated platforms, controls software, coolant services and performance assurance together. Regional supply chains will be stronger and buyers will demand lower installation risk. Sustainability will also matter more, with warm water operation, heat reuse and water efficient heat rejection influencing design. The market will likely have fewer dominant platform providers, supported by specialist component and service companies.

Cooling Distribution Unit Market Target Audience

- CDU Manufacturers: Need market size, share, forecast and growth intelligence to plan product capacity, pricing and regional expansion.

- Data Center Operators: Need buyer analysis to understand technology direction, suppliers and procurement risks.

- Colocation Providers: Need demand insight for liquid ready halls and tenant strategy.

- Component Suppliers: Need visibility on pumps, sensors, heat exchangers and control demand.

- Investors and M&A Teams: Need acquisition targets, growth factors and competitive positioning.

- Engineering Consultants: Need segmentation and regional intelligence for project planning.

- Government and Energy Agencies: Need insight on efficient cooling and infrastructure readiness.

Who Should Buy this Report?

This report is suited for decision makers that need practical market intelligence on CDU demand, competitive positioning and investment opportunities. It supports product planning, procurement, partnership strategy and market entry decisions across the liquid cooling ecosystem.

- CDU and liquid cooling equipment manufacturers

- Data center developers and colocation operators

- Hyperscale and enterprise infrastructure teams

- Component suppliers for pumps, heat exchangers, sensors and controls

- Investors, private equity teams and M&A advisors

- Engineering, procurement and construction firms

- Data center sustainability and energy strategy teams

- Government bodies evaluating AI infrastructure readiness

Why Choose DataM Intelligence?

- DataM Intelligence connects market size, share, forecast and growth outlook to specific business outcomes such as capacity planning, product positioning and investment screening.

- The report explains country specific market size and share dynamics so clients can prioritize regional expansion.

- The analysis links technology trends with buyer procurement behavior, helping sales teams refine target strategy.

- Competitive benchmarking helps clients identify price positioning, portfolio gaps and partnership opportunities.

- Regulatory and policy analysis helps clients understand how energy, water and sustainability rules influence demand.

- Strategic recommendations translate market data into actionable growth moves for manufacturers, investors and operators.