Market Size

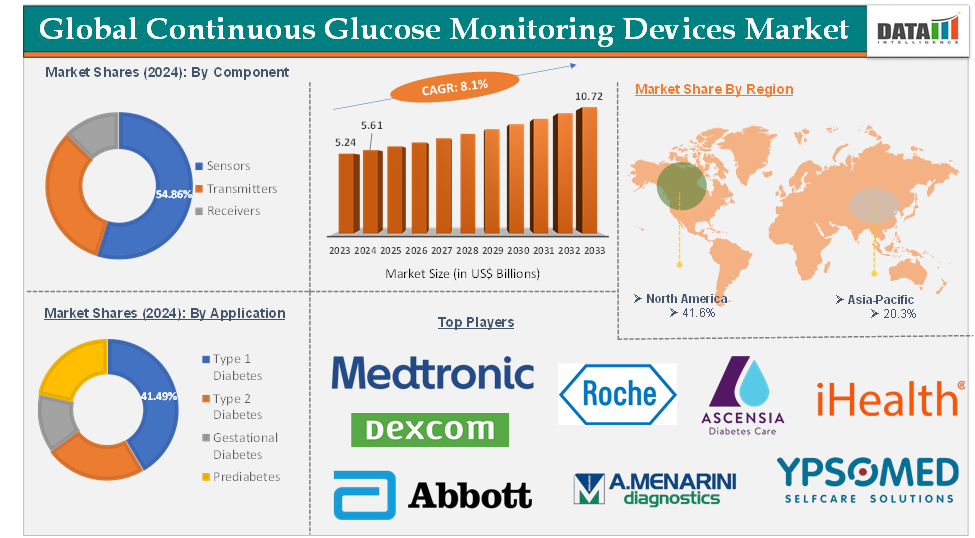

The Global Continuous Glucose Monitoring Devices Market reached US$ 6.06 billion in 2025 and is expected to reach US$ 10.72 billion in 2033, growing at a CAGR of 8.1% during the forecast period (2026–2033).

The global continuous glucose monitoring (CGM) devices market is primarily driven by the rising prevalence of diabetes worldwide, which increases demand for effective blood glucose management solutions. Growing clinical evidence supports the benefits of real-time glucose monitoring in reducing complications, leading to greater adoption among healthcare providers and patients. Additionally, advances in sensor accuracy, longer wear duration, and improved integration with insulin delivery systems have enhanced both patient adherence and clinician confidence in these technologies.

Key trends shaping the CGM market include the shift toward digital health platforms and integration of CGM data with mobile apps and remote care systems, strengthening user engagement, and enabling telemedicine. Technological innovations, such as longer-lasting sensors, improved accuracy, and seamless interoperability with smart insulin pens and pumps, are driving ongoing product development and differentiation.

Significant opportunities exist in expanding access to CGMs in low- and middle-income countries, where diabetes prevalence is rising but device penetration remains low due to cost and awareness barriers. The growing trend of personalized healthcare and preventive wellness is expected to drive demand for CGMs beyond traditional diabetes management, tapping into markets for fitness, sports, and general health monitoring.

Companies can capitalize on the increasing acceptance of digital health tools by developing user-friendly, AI-powered analytics and coaching platforms that enhance the value proposition of CGM devices. Furthermore, as healthcare systems globally move toward value-based care, CGMs are well-positioned to play a central role in remote patient monitoring and chronic disease management programs, creating new revenue streams and partnership opportunities for manufacturers.

Executive Summary

Market Dynamics:

Drivers : Technological advancements

Technological advancements are a major driver propelling the growth of the global continuous glucose monitoring (CGM) devices market. Innovations in sensor technology have significantly improved the accuracy, reliability, and lifespan of CGM devices. Modern sensors can now provide real-time glucose readings with minimal lag and can be worn for extended periods, sometimes up to several months, reducing the need for frequent replacements and enhancing user convenience.

Key advancement is the integration of CGM systems with wireless connectivity features such as Bluetooth and NFC. This allows CGMs to automatically sync data with smartphones, smartwatches, and cloud-based health platforms, enabling users and healthcare providers to access glucose data anytime and anywhere. Such seamless connectivity supports remote patient monitoring, telemedicine, and timely clinical interventions, which are especially valuable for people managing diabetes in rural or underserved areas.

Furthermore, the integration of artificial intelligence (AI) and advanced data analytics into CGM apps has transformed the user experience. These technologies can analyze glucose trends, predict potential highs and lows, and provide personalized recommendations for diet, exercise, and medication. This not only empowers users to make informed decisions but also helps healthcare professionals deliver more precise and proactive care.

For instance, in June 2025, Tracky, a healthtech brand by DrStore Healthcare Services, launched India’s first Bluetooth-connected continuous glucose monitor (CGM), marking a significant advancement in diabetes care and preventive health management in the country. All these factors demand the global continuous glucose monitoring devices market.

Restraints : High cost of devices

The high cost of continuous glucose monitoring (CGM) devices is a significant restraint on the global market, limiting access and adoption, especially among lower-income populations and in low- and middle-income countries (LMICs).

CGM systems require users to purchase not only the initial device but also recurring consumables such as sensors and transmitters, which need frequent replacement. For example, the monthly cost for a CGM system typically ranges from $100 to $300, with some estimates placing annual costs even higher due to the need for a continuous supply of ancillary components. In LMICs, this cost is often prohibitive, as most people must pay out-of-pocket with minimal public financing or insurance support, leading to inequitable access and health disparities.

The high cost of CGMs not only affects individual patients but also has broader public health implications. People unable to afford these devices may experience poorer diabetes management, leading to higher rates of complications and increased long-term healthcare costs. This financial barrier is a key reason why CGM adoption remains suboptimal, despite clear evidence of the technology's benefits for glycemic control and quality of life. Thus, the above factors could be limiting the global continuous glucose monitoring devices market's potential growth.

Opportunities : Expanding use in non-insulin and pre-diabetic populations

The expanding use of continuous glucose monitoring (CGM) devices in non-insulin and pre-diabetic populations represents a significant growth opportunity for the global CGM market. Traditionally, CGMs were primarily used by people with diabetes who required insulin therapy. However, recent trends show increasing adoption among individuals with type 2 diabetes managed by oral medications, people with prediabetes, and even health-conscious individuals without a diabetes diagnosis.

This shift is driven by the need for early detection and proactive intervention. CGMs provide real-time, detailed glucose data that can reveal abnormal patterns such as postprandial hyperglycemia or the dawn phenomenon, often before traditional diagnostic tests would indicate a problem. For pre-diabetic individuals, this early insight enables timely lifestyle changes, such as dietary adjustments and increased physical activity, which can delay or prevent the progression to type 2 diabetes.

For more details on this report, Request for Sample

Segmentation Analysis

The global continuous glucose monitoring devices market is segmented based on component, connectivity, application, end-user, and region.

Component:

The sensors component segment in the continuous glucose monitoring (CGM) devices market refers to the tiny, minimally invasive sensors that are inserted just under the skin, typically on the arm or abdomen, to continuously measure glucose levels in the interstitial fluid. These sensors are the core functional element of a CGM system, detecting and quantifying glucose concentrations in real time or at frequent intervals (such as every 5 minutes), and transmitting this data to a receiver, smartphone, or insulin pump for monitoring and analysis.

Applications of CGM sensors extend across various user groups. They are widely used by people with type 1 and type 2 diabetes for ongoing glucose management, allowing for more precise insulin dosing and better glycemic control. Increasingly, sensors are also being adopted by pre-diabetic individuals, people using oral diabetes medications, and even those interested in wellness or athletic performance, as they provide actionable insights into how diet, exercise, and lifestyle impact glucose levels.

Drivers for the growth of the sensors segment include continuous technological advancements that have improved sensor accuracy, comfort, and longevity. Some sensors now last up to 14 days or even several months before needing replacement. The trend toward miniaturization and user-friendly designs has made sensors less intrusive and easier to apply, broadening their appeal. Additionally, the integration of sensors with digital health platforms, wireless connectivity (Bluetooth/NFC), and automated insulin delivery systems has expanded their utility and market reach.

Geographical Analysis

North America, particularly the United States and Canada, has a high and rising prevalence of diabetes, with Billions of individuals requiring effective glucose management solutions. This has increased public and clinical awareness about the importance of tight glycemic control and the benefits of real-time glucose monitoring, fueling demand for CGM devices.

The region benefits from highly developed healthcare systems, widespread access to advanced medical technologies, and a robust digital health ecosystem. This environment supports rapid adoption of new CGM technologies, including sensors with improved accuracy, longer wear times, and seamless integration with digital platforms and insulin delivery systems.

Major CGM manufacturers such as Dexcom, Abbott, Medtronic, and Senseonics have operational headquarters or significant market presence in North America. Their ongoing investment in research and development, frequent product launches, and strategic partnerships drive both innovation and market expansion.

Rapid advancements in sensor technology, data analytics, and artificial intelligence have improved the accuracy, usability, and clinical value of CGMs. Integration with smartphones and cloud-based platforms enhances patient engagement and enables remote monitoring by healthcare providers, further supporting adoption.

Asia-Pacific is home to the world’s largest diabetic populations, particularly in China and India, where urbanization, sedentary lifestyles, and aging demographics are fueling a surge in type 2 diabetes cases. The region’s rapidly aging population is especially vulnerable, creating an urgent need for effective, continuous glucose monitoring solutions to manage and prevent diabetes-related complications.

Advances in sensor technology, such as improved accuracy, longer sensor wear duration, and integration with smartphones and digital health platforms, are making CGMs more attractive and accessible to consumers. The widespread adoption of smartphones and better internet connectivity across the region has facilitated real-time data sharing, remote monitoring, and integration with mobile health applications, supporting proactive and personalized diabetes management.

Governments across Asia-Pacific are increasingly prioritizing diabetes management, launching public health campaigns, expanding insurance coverage, and implementing supportive reimbursement policies for CGM devices. For example, Japan’s national insurance coverage for CGMs has grown significantly, and similar trends are emerging in China and other countries, making these devices more affordable and accessible to a broader patient base.

Competitive Landscape

The major global players in the continuous glucose monitoring devices market include Abbott, Dexcom, Inc., Medtronic Pvt. Ltd., Ascensia Diabetes Care Holdings AG., F. Hoffmann-La Roche Ltd, iHealth Labs Inc., Ypsomed AG, Medtrum Technologies Inc., Menarini Diagnostics s.r.l Nemaura, Senseonics, Glucovation, Inc., Afon Technology, and Signos Inc., among others.

Recent Developments

In March 2026, Dexcom, Inc. expanded its CGM portfolio with next-generation sensors offering longer wear time and improved accuracy. The innovation focuses on real-time glucose tracking and user convenience. This supports better diabetes management.

In February 2026, Abbott Laboratories introduced advanced FreeStyle Libre systems with enhanced connectivity and data analytics. The development improves remote monitoring and patient engagement. This benefits both patients and healthcare providers.

In January 2026, Medtronic plc strengthened its CGM solutions with integrated insulin pump systems. The focus is on automated insulin delivery and closed-loop systems. This supports improved glycemic control.

Market Scope

Metrics | Details | |

CAGR | 8.1% | |

Market Size Available for Years | 2023-2033 | |

Estimation Forecast Period | 2026-2033 | |

Revenue Units | Value (US$ Bn) | |

Segments Covered | Component | Sensors, Transmitters, Receivers |

Connectivity | Bluetooth, Wi-Fi | |

Application | Type 1 Diabetes, Type 2 Diabetes, Gestational Diabetes, Prediabetes | |

End-User | Hospitals & Clinics, Homecare Settings, Diagnostic Centers, Others | |

Regions Covered | North America, Europe, Asia-Pacific, South America, and the Middle East & Africa | |

DMI Insights:

Our research indicates that the market for continuous glucose monitoring devices is expected to expand at a compound annual growth rate (CAGR) of 8.1% from 2025 to 2033. This expansion is driven by the increasing prevalence of diabetes, demand for real-time and less invasive glucose monitoring, and advances in sensor technology and digital health integration. CGM systems are becoming a cornerstone of modern diabetes management, offering improved patient outcomes, enhanced remote monitoring, and strong adoption across both clinical and home settings worldwide

The global continuous glucose monitoring devices market report delivers a detailed analysis with 87 key tables, more than 67 visually impactful figures, and 173 pages of expert insights, providing a complete view of the market landscape.

For more medical device-related reports, please click herere