Obesity Therapeutics Market Size

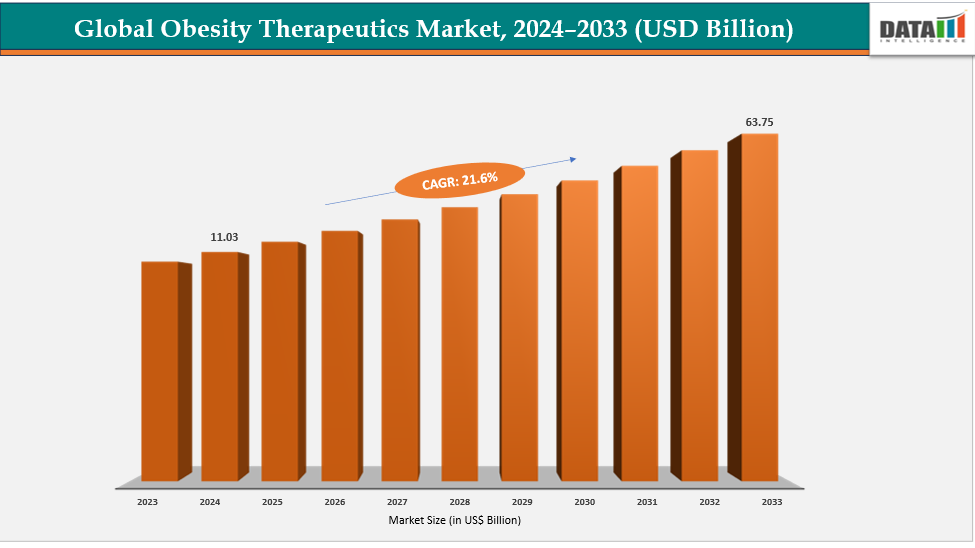

The global obesity therapeutics market size reached USD 13.41 billion in 2025 and is expected to reach US$ 63.75 billion by 2035, growing at a CAGR of 21.6% during the forecast period 2026-2035.

The obesity treatments market has grown considerably since the discovery of GLP-1 receptor agonists and dual-agonist medications. These medications showed previously unheard-of benefits for metabolism and weight loss, which led to widespread clinical adoption and patient demand. They were positioned as game-changing treatments for obesity and associated disorders due to their shown capacity to lower cardiovascular risks and enhance glycaemic glucose management. In order to provide next-generation incretin and non-incretin treatments with increased convenience, safety, and efficacy, big pharmaceutical corporations concurrently widened their R&D pipelines and established strategic alliances.

Key Takeaways

- The obesity therapeutics market is expected to expand from USD 13.41 billion in 2025 to USD 95.09 billion by 2035, reflecting sustained pharmaceutical innovation and expanding patient adoption.

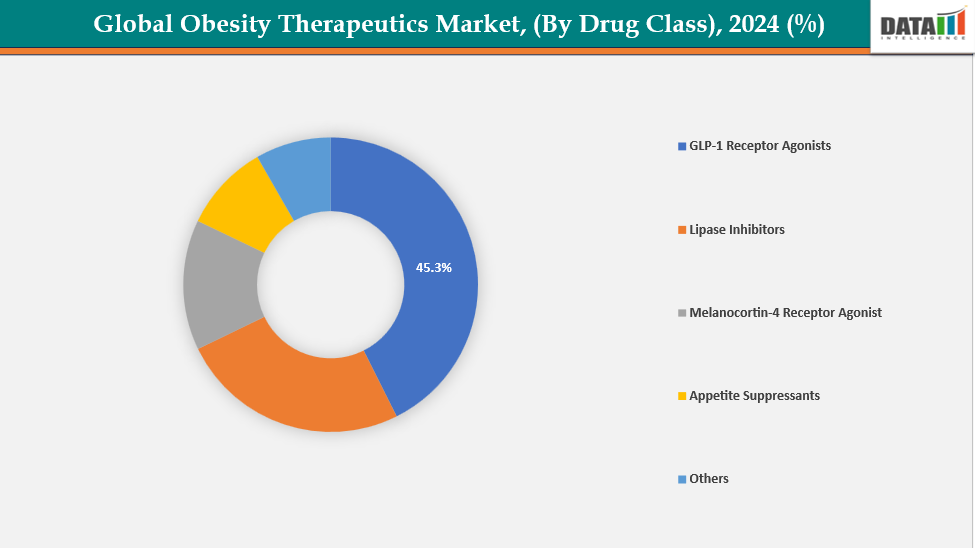

- GLP-1 receptor agonists remain the leading drug class, accounting for 45.3% of the market in 2024 due to proven efficacy in long-term weight management and cardiometabolic benefits.

- Oral therapies represented 41.3% of the market in 2024, highlighting strong patient preference for convenient administration and improved treatment adherence.

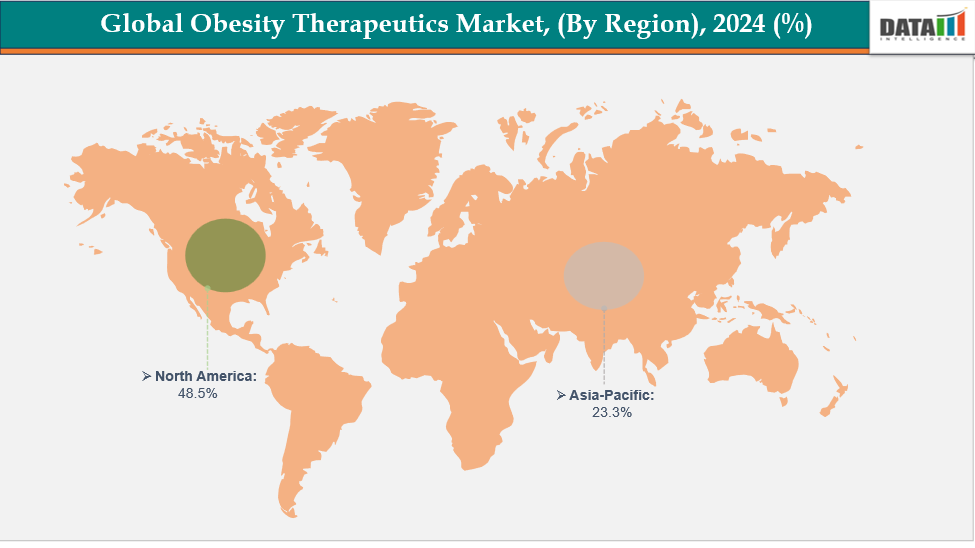

- North America maintained the largest regional position with 48.5% market share in 2024, supported by high obesity prevalence, favorable reimbursement, and rapid commercialization of innovative therapies.

- Asia-Pacific is emerging as the fastest-growing regional market, supported by increasing healthcare investment, regulatory approvals, and expanding pharmaceutical manufacturing capabilities.

- Pharmaceutical companies are shifting from single-target therapies toward multi-receptor agonists designed to improve efficacy, durability, and long-term metabolic outcomes.

Obesity Therapeutics Market Scope

| Metric | Details |

| Market Size (2025) | USD 13.41 Billion |

| Forecast Market Size (2035) | USD 95.09 Billion |

| CAGR | 21.60% |

| Historic Years | 2023-2024 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Segments Covered | Drug Class, Route of Administration, Distribution Channel, Region |

| Leading Region | North America |

| Fastest Growing Region | Asia-Pacific |

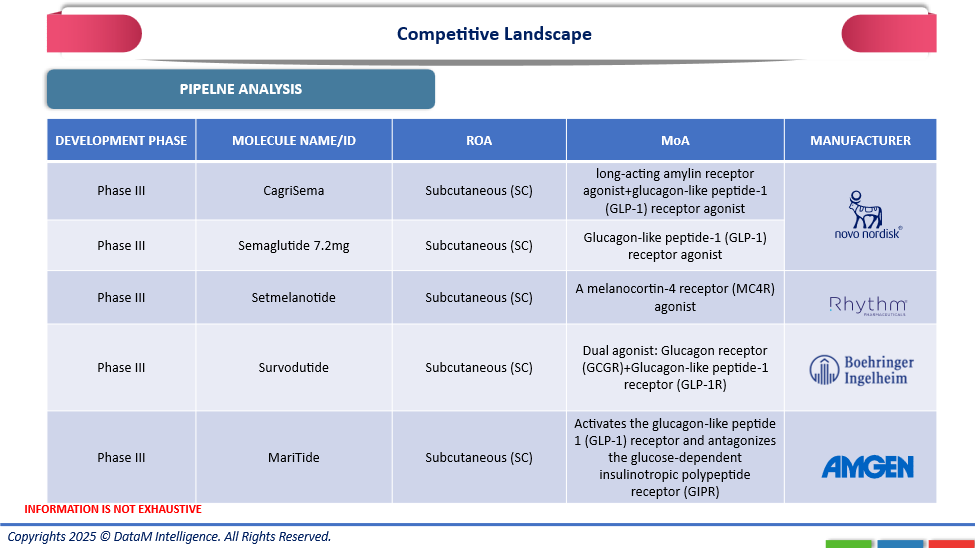

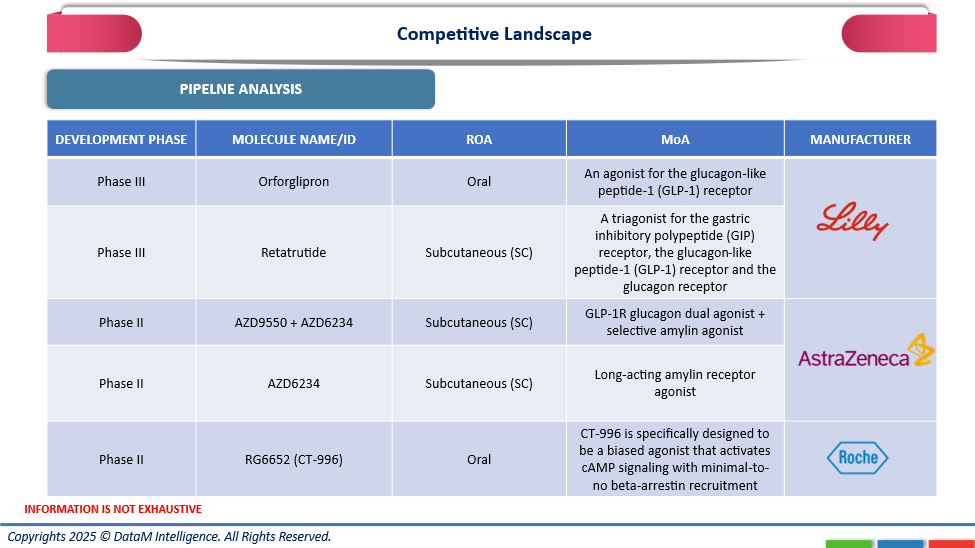

Competitive Landscape

Market Dynamics

Drivers: Rising prevalence of obesity worldwide are accelerating the growth of the obesity therapeutics market

The obesity treatments market is expanding at an accelerated rate due to the increased prevalence of obesity globally. The need for efficient weight-management programs is growing quickly as more people acquire weight-related illnesses like diabetes, high blood pressure, and heart disease. Pharmacological therapies are becoming more widely used as healthcare systems acknowledge obesity as a chronic, curable illness. Owing to the factors like worldwide prevalence, for instance, according to WHO data published in 2024, overweight and obesity were among the leading causes of disability and mortality in the European Region, affecting around 60% of adults, one-third of school-aged children, and 8% of children under five.

Additionally, patients are being encouraged to seek medical assistance due to increased awareness caused by public health campaigns and the media. Global need for long-term, safe treatment alternatives is driving robust market expansion as obesity rates continue to climb across all age groups and geographical areas.

Restraints: Regulatory withdrawals and rollout bottlenecks and off-label is hampering the growth of the obesity therapeutics market

The market expansion for obesity treatments is being hampered by regulatory withdrawals and deployment difficulties. New medicine launches across regions are delayed by stringent approval requirements and protracted evaluation durations. Market penetration is slowed by additional delays caused by manufacturing and distribution approvals.

Additionally, increased demand has resulted in the off-label or unsupervised use of anti-obesity drugs, which are frequently bought online without a doctor's supervision because of adverse impacts on people, the businesses are pulling their products off the market and stopping their development. For instance, in April 2025, Pfizer discontinued the development of its oral GLP-1 receptor agonist, danuglipron, which was under investigation for chronic weight management. The decision followed a comprehensive review of clinical data and regulatory feedback after a potential drug-induced liver injury was observed in one study participant.

Obesity Therapeutics Market, Segmentation Analysis

The global obesity therapeutics market is segmented based on drug class, route of administration, distribution channel and region

By Drug Class: The GLP-1 receptor agonists segment from drug class is dominating the obesity therapeutics market with a 45.3% share in 2025

The obesity treatments market is dominated by the GLP-1 receptor agonists segment because of its higher efficacy and established clinical results. These medications enhance glucose metabolism and cardiovascular health while promoting noticeable and long-lasting weight loss. They cause people to eat less because they mimic the natural gut hormones that control hunger and satiety. Long-term use is encouraged by their simple dosage schedules and good safety profile.

Furthermore, GLP-1 receptor agonists are becoming the most popular treatment choice for obesity due to their sophisticated formulations and delivery systems, which are being driven by ongoing research, new product launches, and growing regulatory approvals. For instance, in July 2024, the MHRA approved semaglutide (Wegovy) to reduce the risk of serious heart problems or strokes in overweight and obese adults. This GLP-1 receptor agonist was already approved for obesity and weight management, used alongside diet, physical activity, and behavioral support, marking a major milestone in preventive care.

By Route of Administration: The oral segment route of administration is dominating the obesity therapeutics market with a 41.3% share in 2025

The obesity treatments market is dominated by the oral route of administration since it is convenient, safe, and preferred by patients. Compared to injectables, oral medications are more convenient and non-invasive, which improves treatment adherence. They lessen reliance on medical personnel by enabling self-administration. This tendency has been reinforced by recent advancements, approvals, pharmaceutical launches, and exclusive licensing agreements in oral GLP-1 agonists and combination formulations. For instance, in November 2023, AstraZeneca entered into an exclusive licensing agreement with Eccogene for ECC5004, a next-generation oral GLP-1 receptor agonist, gaining global rights to develop and commercialize it for obesity, type 2 diabetes, and cardiometabolic conditions.

Additionally, cost-effective production and increased accessibility via physical and virtual pharmacies further increase use. Additionally, oral medications have easier logistics and a longer shelf life. To improve absorption and efficacy, pharmaceutical companies are concentrating on creating innovative oral formulations of incretin-based medications.

Geographical Analysis

North America is dominating the global obesity therapeutics market with a 48.5% in 2025

The obesity treatments market was dominated by North America due to high obesity rate, sophisticated healthcare system, and robust uptake of new anti-obesity medications. Growing awareness of the health problems associated with obesity, attractive reimbursement policies, and ongoing product innovation all contributed to regional expansion and market supremacy.

In the USA, obesity therapeutics market growth was driven by rising obesity prevalence, increasing patient awareness, and advancements in GLP-1 and combination therapies. Moreover, the recent launch of new companion combination products further supported effective and personalized weight management solutions. For instance, in November 2023, the U.S. FDA approved Eli Lilly’s Zepbound (tirzepatide) injection for chronic weight management in adults with obesity or overweight and at least one weight-related condition, as an adjunct to a reduced-calorie diet and increased physical activity.

Europe is the second region after North America which is expected to dominate the global obesity therapeutics market with a 34.5% in 2025

In Europe, the obesity therapeutics market has grown rapidly due to rising obesity prevalence, increasing health awareness, and expanding access to advanced GLP-1 therapies. Market growth was further supported by favorable regulatory frameworks, continuous product innovation and new product launches, and growing adoption of combination and personalized treatment approaches.

Owing to factors like new product launches, for instance, In June 2024, Rhythm Pharmaceuticals Netherlands B.V. received a positive opinion from the CHMP recommending changes to the marketing authorisation of Imcivree. The approval extended its use to children aged two years and above. Imcivree was indicated for the treatment of obesity and the control of hunger associated with genetic disorders.

The obesity treatment market in Germany was propelled by the country's robust healthcare system, rising obesity prevalence, and expanding knowledge of medical weight control. Market expansion and therapeutic adoption across patient demographics were further reinforced by the growing use of GLP-1 agonists, favorable reimbursement policies, and a focus on safe, clinically established medicines.

The Asia Pacific region is the fastest-growing region in the global obesity therapeutics market, with a CAGR of 7.7% in 2025

Asia-Pacific's obesity treatments market, which includes China, India, South Korea, and Japan, grew quickly as a result of rising obesity rates, rising healthcare costs, and increased awareness of weight-loss options. The expansion and adoption of the regional market were further hastened by improvements in drug development, increased accessibility to anti-obesity drugs, and encouraging government measures.

China’s obesity therapeutics market expanded rapidly, driven by rising obesity rates, higher disposable incomes, and increasing health awareness. Continuous innovation, expanding local players, and favorable NMPA approvals for advanced anti-obesity drugs supported strong market growth and accelerated adoption of effective therapeutic solutions nationwide. Owing to factors like NMPA approvals, for instance, in June 2025, Innovent Biologics, Inc. announced that China’s NMPA had approved Mazdutide, the world’s first dual GCG/GLP-1 receptor agonist, for chronic weight management in adults with overweight or obesity, marking a major milestone in advanced obesity treatment.

Obesity Therapeutics Market Competitive Landscape

Top companies in the obesity therapeutics market include Novo Nordisk, Eli Lilly, VIVUS LLC, Currax Pharmaceuticals LLC, GSK plc, Roche Laboratories Inc, AstraZeneca, Rhythm Pharmaceuticals, Inc, Takeda Pharmaceutical Company Limited, and KVK Tech, Inc, among others.

Novo Nordisk: Novo Nordisk is a global healthcare leader, specializing in diabetes and obesity care. The company has pioneered obesity therapeutics with innovative GLP-1 receptor agonists such as Saxenda (liraglutide) and Wegovy (semaglutide). Focused on addressing the global obesity epidemic, Novo Nordisk emphasizes sustainable weight management through evidence-based, safe, and effective treatments.

Key Developments

June 2026: Novo Nordisk expanded its obesity therapeutics portfolio across North America and Europe by advancing the commercialization and global rollout of next-generation GLP-1-based weight management therapies, strengthening manufacturing capacity to address growing patient demand and improve treatment accessibility.

May 2026: Eli Lilly and Company strengthened its obesity treatment business across North America by expanding production capabilities and accelerating global market access for incretin-based therapies, supporting the rising adoption of pharmacological treatments for chronic weight management.

April 2026: Amgen Inc. advanced its obesity therapeutics pipeline across North America and Europe by progressing clinical development of long-acting obesity drug candidates targeting incretin pathways, aiming to improve weight reduction outcomes and offer differentiated treatment options for patients with obesity.

March 2026: Roche expanded its metabolic disease portfolio across Europe by strengthening the development of next-generation obesity therapies through strategic collaborations and clinical pipeline advancements, supporting innovation in combination therapies for long-term weight management.

February 2026: Structure Therapeutics enhanced its obesity therapeutics pipeline across North America and Asia-Pacific by advancing oral GLP-1 receptor agonist programs and expanding clinical development activities, supporting the growing demand for convenient, non-injectable obesity treatment options and broadening the future therapeutic landscape.

The global obesity therapeutics market report delivers a detailed analysis with 62 key tables, more than 56 visually impactful figures, and 159 pages of expert insights, providing a complete view of the market landscape.Report Benefits

This report supports:

- Pharmaceutical manufacturers evaluating pipeline expansion opportunities.

- Biotechnology companies developing next-generation metabolic therapies.

- Investors assessing high-growth therapeutic markets.

- Healthcare providers monitoring treatment adoption trends.

- Procurement teams evaluating emerging obesity medicines.

- Corporate strategy teams benchmarking competitive positioning and regional opportunities.

Target Audience

- Pharmaceutical Companies

- Biotechnology Firms

- Contract Research Organizations

- Healthcare Providers

- Hospital Procurement Teams

- Institutional Investors

- Venture Capital Firms

- Regulatory Authorities

- Drug Manufacturers

- Distribution Companies

- Healthcare Consultants

- Market Intelligence Teams

Conclusion

The obesity therapeutics market is positioned for substantial long-term expansion as obesity continues to place increasing pressure on healthcare systems worldwide. Advances in GLP-1 receptor agonists, oral therapies, multi-receptor biologics, and precision metabolic medicine are broadening treatment options while improving clinical outcomes.

Commercial success through 2035 will depend on maintaining strong clinical efficacy, demonstrating long-term safety, securing regulatory approvals, and expanding manufacturing capacity to meet accelerating global demand. Organizations investing in differentiated therapeutic platforms, strategic partnerships, and geographically diversified commercialization strategies are likely to strengthen their competitive position as obesity management becomes an increasingly important component of chronic disease care.

Suggestions for Related ReportFor more pharmaceutical-related reports, please click here