Co-Packaged Optics Market Overview

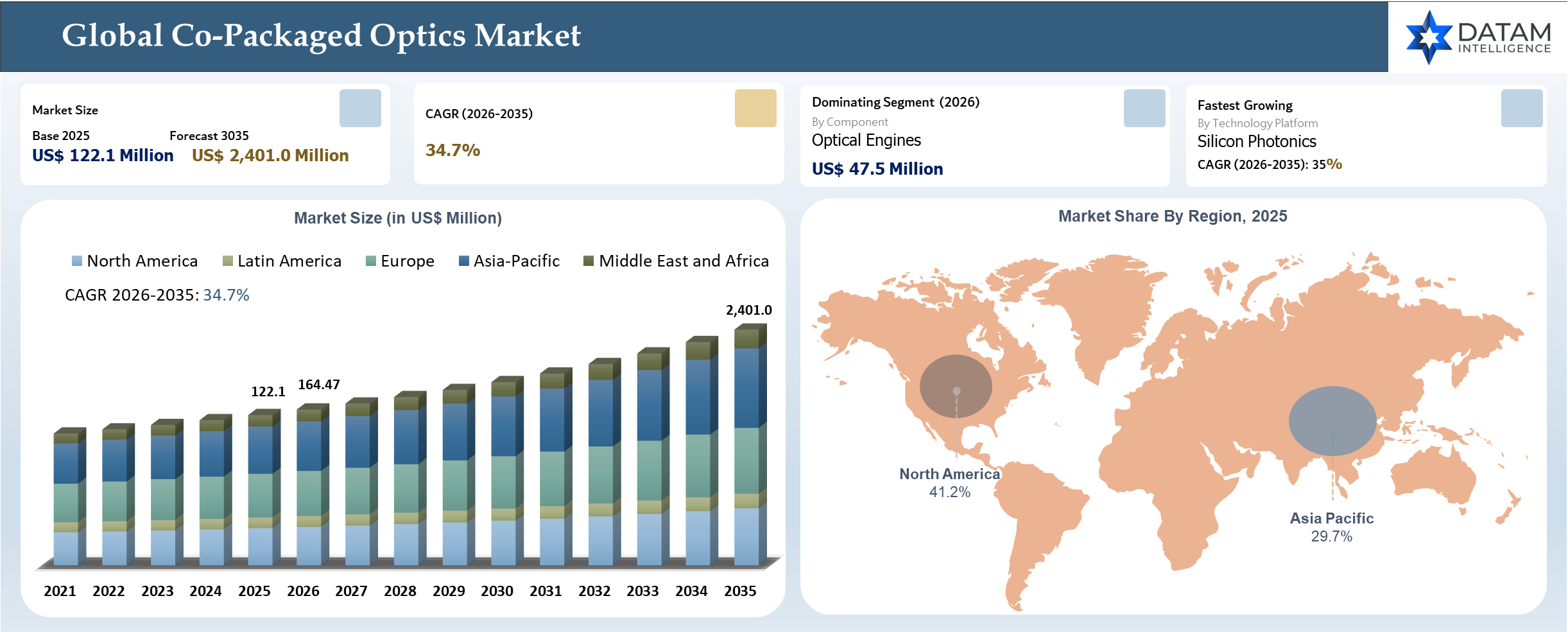

The global Co-Packaged Optics market reached US$ 122.1 million in 2025 and is expected to reach US$ 2,401.0 million by 2035, growing with a CAGR of 34.7% during the forecast period 2026-2035. The Co-Packaged Optics market is revolutionizing digital infrastructure design by eliminating the historic divide between electronic switching and optical communication and combining them into one system-level layer. Rather than adding capacity to existing optics through evolutionary improvements, the Co-Packaged Optics model involves rethinking the whole platform to optimize bandwidth density and energy efficiency simultaneously. From a structural point of view, this is key because AI-based tasks demand bandwidth beyond the capacity of either copper or standalone optics alone.

Co-Packaged Optics Industry Trends and Strategic Insights

- In the Co Packaged Optics industry, there is a fast shift towards an AI-driven data center architecture where hyperscaler companies like Microsoft Corporation, Amazon Web Services, and Google Cloud are working to deploy optical engine embedded switching platforms to combat bandwidth and power limitations in AI training clusters. This shift is fueled by the exponential rise in GPU workloads and a need to decrease electrical interconnect losses at hyperscaler scale.

- Leading technology vendors like NVIDIA Corporation, Broadcom Inc and Intel Corporation are pushing their silicon photonics product roadmap and co integration strategies where optical interfaces will be integrated into switching ASICs. Through this, they can improve the system bandwidth density with products like 800G and 1.6T interconnects along with enhancing the energy efficiency per bit.

- Major cloud and data center industry companies like Meta Platforms, Microsoft and Amazon Web Services are working with optical component vendors like Coherent Corp and Lumentum Holdings for developing co-packaging optics.

Market Scope

| Metrics | Details | |

| 2025 Market Size | US$ 122.1 Million | |

| 2035 Projected Market Size | US$ 2,401.0 Million | |

| CAGR (2026-2035) | 34.7% | |

| Largest Market | North-America | |

| Fastest Growing Market | Asia-Pacific | |

| By Component | Optical Engine, Electrical Integrated Circuit (IC), Laser Source, Optical Interposers or Substrates, Others | |

| By Integration Approach | On-Board Optics, Fully Integrated CPO Modules, Hybrid Solutions | |

| By Data Rate | 400G, 800G, 1.6T, 3.2T, 6.4T and above | |

| By Application | Hyperscale Data Center Switching, High Performance Computing, Cloud Network Infrastructure, Telecommunications Core and Metro Networks, Edge and Distributed Compute Systems, Others | |

| By Technology Platform | Silicon Photonics, Indium Phosphide (InP) Photonics, Vertical-Cavity Surface-Emitting Laser (VCSEL)-Based Optical Systems, Hybrid Photonic Integration Platforms | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

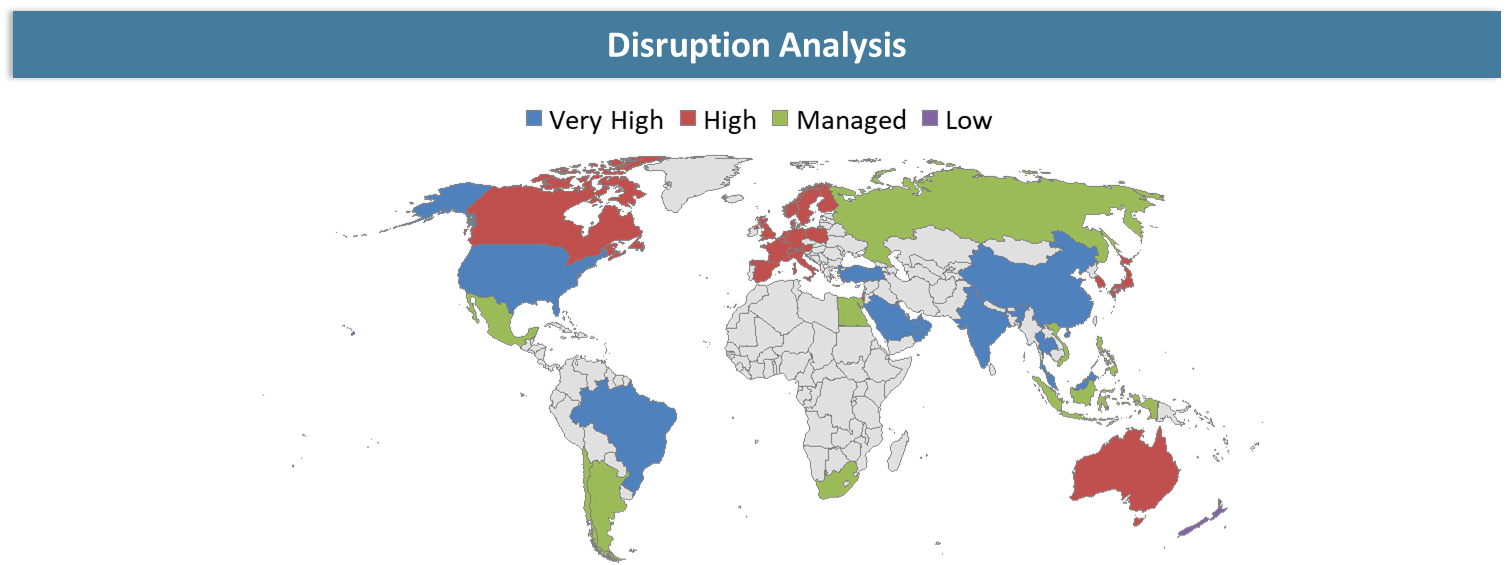

Disruption Analysis

Shift from Pluggable Optics to Integrated Co-Packaged Photonics Redefining Data Center Architectures

The disruption in the co-packaged optics space is a function of an architectural evolution that is taking place in the data center architecture, whereby optical interconnections are moving closer to computing. Increasing bandwidth demands caused by AI applications and high-performance computing workloads have led to a rapid deployment of 800G technology while making the 1.6T technology commercially viable. These developments reflect the increasing pressure for moving from pluggable optics to an integrated photonic solution within switching silicon.

Another disruptive trend involves the drive for energy efficiency and optimization in terms of power consumption for hyperscale data centers. Co-packaged optics could potentially offer reductions in power consumption per bit by up to 30-50 percent, along with improvements in bandwidth density. Meanwhile, it is expected that by the end of the decade, data centers will consume almost 10-12 percent of electricity usage in developed economies. Yet another challenge lies in the form of decreased serviceability and increased thermal management requirements. The co-packaged optics industry is undergoing a serious technology disruption due to the increasing demands for energy efficiency and bandwidth requirements driven by AI.

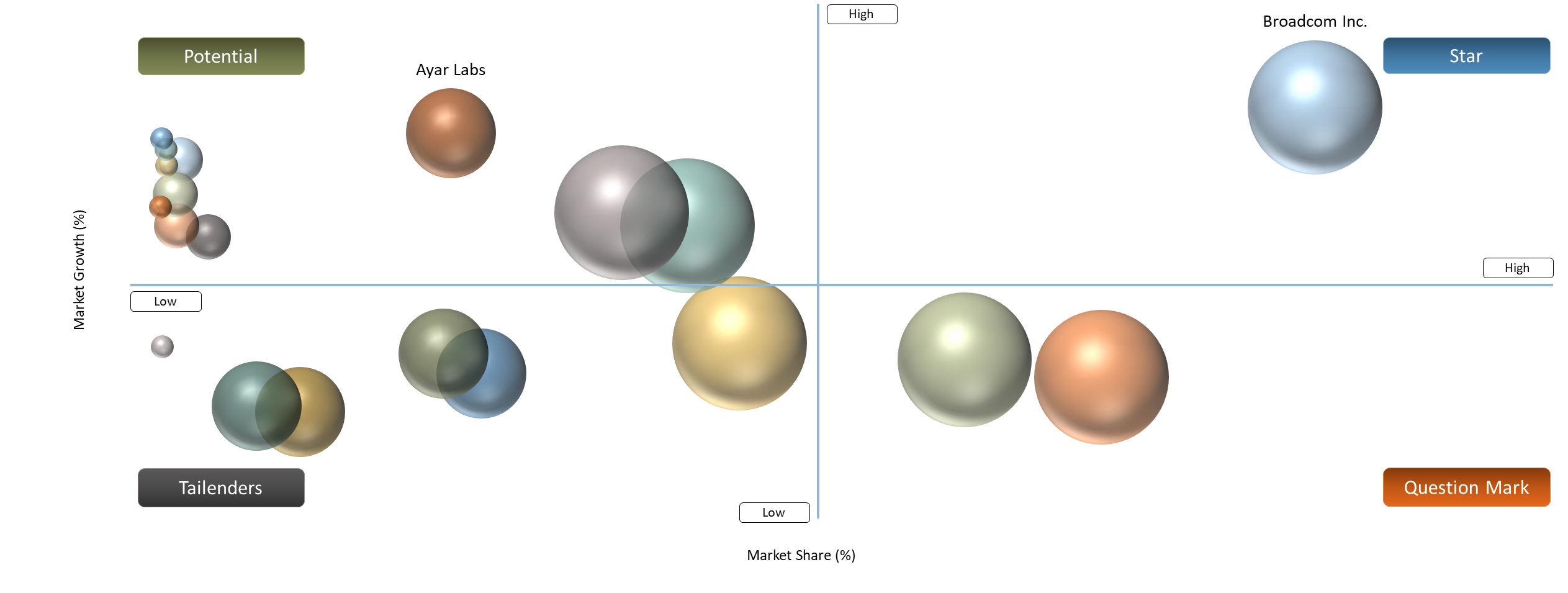

BCG Matrix: Company Evaluation

In the co-packaged optics market, players like Broadcom Inc., Intel Corporation, NVIDIA Corporation, and Cisco Systems, Inc. fall into the category of Stars due to their solid presence, technological strength in silicon photonics and their direct link with AI-scale data center demand. The high level of investment in 800G/1.6T ecosystems and the close partnership with the hyperscaler community support their success in this field. Firms like Marvell Technology, Inc. and Coherent Corp have the potential to become Leaders due to their solid technological base; however, their market penetration in co-packed architectures is still developing.

Potential players are emerging innovators like Ayar Labs and Ranovus Inc. They deliver promising innovative optical I/Os and chip-to-chip interconnect solutions with high growth opportunities but lack large market share. The firms like Lumentum and FURUKAWA ELECTRIC CO., LTD belong to Tailenders. These enterprises are still more focused on traditional optical components and gradually make their way towards co-packed optics. It is worth noting that this market demonstrates an interesting BCG Matrix. Established semiconductor players act as Stars whereas emerging startups create innovation momentum.

Market Dynamics

Rapid Growth in AI and Machine Learning Workloads Accelerating Demand for High-Bandwidth Optical Interconnects

Workload sizes in AI/machine learning have scaled up tremendously, with compute-intensive training clusters running more compute than before. Current state-of-the-art AI models are trained on clusters from 10k to above 100,000 GPUs, with hyperscale cluster installations reaching 400,000 GPUs within a single system. The rate of scale-up is clear when one looks at future predictions, whereby hyperscaler firms aim to deploy clusters with over a million GPUs by 2027. These clusters will demand extremely fast and low-latency interconnections, creating an absolute necessity for the development of co-package optics technology.

From a practical perspective, hyperscalers and cloud computing services have been working towards increasing AI infrastructure capabilities by deploying huge numbers of GPUs and forming partnerships. For example, Oracle intends to install 50,000 GPUs in a single AI supercomputer. Meanwhile, Meta and other parties are running clusters comprising more than 100,000 GPUs to enable training next-generation models. Moreover, there are growing shipments of GPUs with an estimation of millions of next-generation AI GPUs to be deployed each year to handle AI computing tasks. The tremendous growth in parallel compute nodes is likely to create huge amounts of data flows in data centers in the form of east-west data movement, which underlines the importance of using co-packaged optical interconnect solutions.

Manufacturing Complexity and Heterogeneous Integration Yield Challenges Limiting Scalability

One of the main factors restraining the large-scale adoption of CPO is the issue of manufacturing complexity. CPO is more complex than conventional optical components because of the combination of photonics and electronics in a single package, whereas ordinary optics do not need the two elements to be precisely aligned in the same manner. Therefore, the production process for CPO is complicated and leads to low initial yields. Since heterogeneous integration in silicon photonics, advanced packaging technology, and application-specific integrated circuits involves many components, failure is common during the initial production process.

Moreover, yield management is another important concern that needs to be addressed in order to achieve high product quality and reliability. Research indicates that the initial yield rate in advanced packaging manufacturing can be much lower than that of mature semiconductor production technology, which impacts the industry's ability to mass-produce products. Lack of standard manufacturing methods and procedures may lead to inefficiency during production. Thus, manufacturing complexity and heterogeneous integration yield restrictions will continue to be some of the key factors that restrain the large-scale adoption of CPO.

Segmentation Analysis

The global Co-Packaged Optics market is segmented based on component, integration approach, data rate, application, technology platform and region.

Optical Engine Emerging as the Core Enabler of High-Bandwidth Co-Packaged Optics Architectures

The optical engines category makes up the majority of the overall market share owing to its importance in facilitating high bandwidth low power data transfers in an AI scale data center. The proximity between these engines and the switching ASICs leads to no need for electrical traces and increased signal integrity. Some of the leading players in the development of optical I/O solutions that deliver multi-terabit bandwidth per chip include Ayar Labs and Ranovus Inc. This category is dominant as it is the basic unit in all co-packaging applications, which support the migration to 800G and 1.6T interconnect ecosystem.

In terms of usage, optical engines have proven to be highly effective due to lower power consumption and size. Specifically, there have been demonstrations made by Intel Corporation where optical engines have been successfully embedded into Ethernet switch silicon, and Broadcom Inc., which continues working on the same technology applied to next-generation switching platforms. These devices have been found to be able to offer a 30% to 50% reduction in interconnect power per bit and improved bandwidth densities, making them quite popular in large AI clusters.

Geographical Penetration

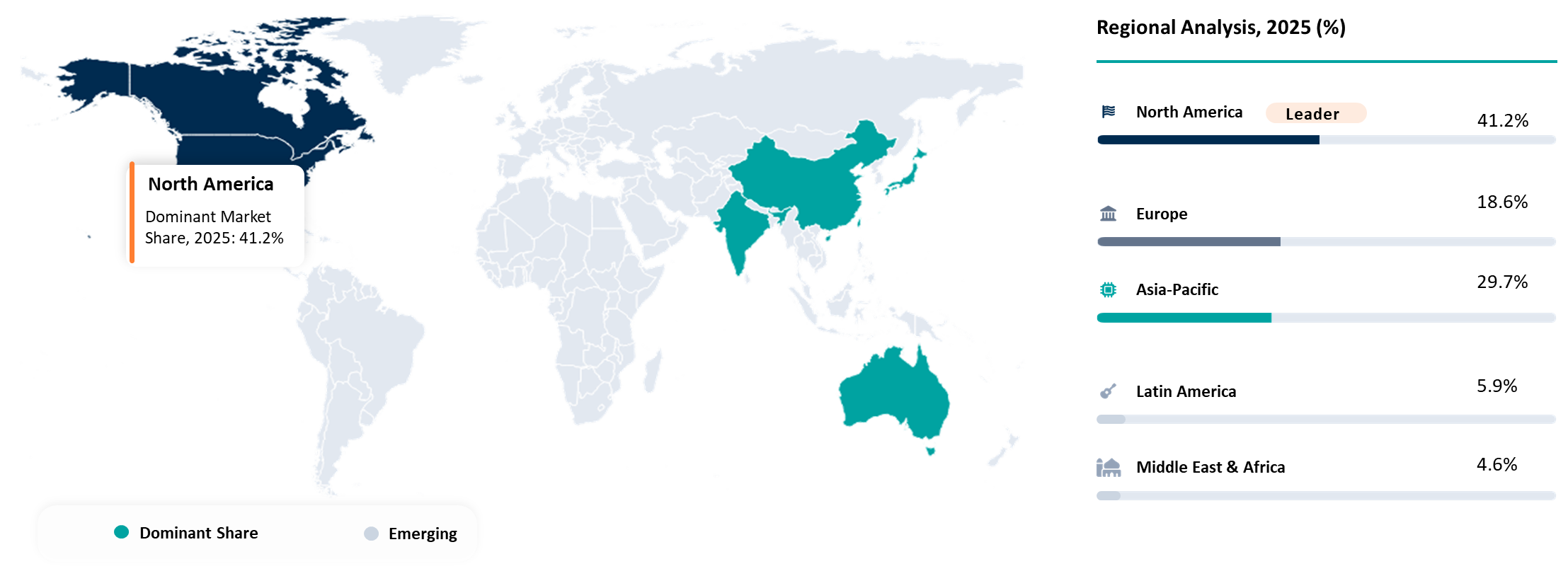

North America Leading Region Driven by Hyperscale AI Infrastructure and Early CPO Adoption

In the co-packaged optics space, the major player in the region remains North America because of the existence of major hyperscale players and advanced semiconductor industry infrastructure. These companies include Google LLC, Microsoft Corporation, and Meta Platforms, Inc., which are rapidly building up their AI infrastructures to a point where GPU cluster counts have already gone above 100,000 and future roadmaps will focus on even more deployment. Moreover, innovations by local firms such as Broadcom Inc. and NVIDIA Corporation will drive the development of technologies like 800G/1.6T networking solutions. The presence of these conditions ensures that North America will become an early adopter of CPO.

Policies like the CHIPS and Science Act will help to foster the growth of advanced technologies by reducing dependency on foreign fabrication facilities and enhancing domestic capabilities through the allocation of more funding into strengthening supply chains. It will improve silicon photonic devices and co-packaged optics technologies. In addition, the electricity consumption rate for data centers is expected to grow substantially with the increase in AI computing requirements in the US, further supporting CPO technologies.

U.S. Co-Packaged Optics Market Trends

The United States is leading the way in the co-packaged optics industry because of its ability to set industry standards as well as make ecosystem alliances that favor CPO adoption. Some of the American-based companies that are making strides in co-packaged optics standards include Intel Corporation and Cisco Systems, Inc., which are currently making efforts toward co-packaged optics standards under the Consortium for On-Board Optics group. At the same time, there is Ayar Labs, which has showcased the capabilities to achieve more than 2 Tbps I/O bandwidths per chip. The United States is leading the way through standard setting and ecosystem alliances that favor co-packaged optics adoption.

Canada Co-Packaged Optics Market Outlook

The uniqueness of Canada stems from its ability to offer advanced testing abilities, packaging research capabilities, and high-level photonics talent development. Organizations like CMC Microsystems facilitate prototyping and verification of silicon photonics and system integration that are vital for boosting yields in co-packaging of optics. Moreover, due to the emphasis placed by the country on developing specialized semiconductors, there will always be an adequate supply of engineers in the realm of photonics and packaging development. Canada serves as an essential backend innovation center for the development of co-packaged optics.

Competitive Landscape

- The competitive landscape of the co-packaged optics market is led by vertically integrated semiconductor and networking players such as Broadcom Inc., Intel Corporation, NVIDIA Corporation, and Cisco Systems, Inc., which are driving commercialization through switching ASIC integration and silicon photonics development

- Key players include Broadcom Inc., Intel Corporation, NVIDIA Corporation, Cisco Systems, Inc., Marvell Technology, Inc., Ranovus Inc., Coherent Corp, Lumentum, FURUKAWA ELECTRIC CO., LTD., Ayar Labs

Key Developments

- January 2025 - Marvell Technology announced the launch of a new AI accelerator integrated with co-packaged optics technology to enhance server performance.

- May 2025 - Broadcom introduced third-generation co-packaged optics (CPO) technology with 200G-per-lane capability, advancing its Tomahawk-based switch ecosystem for AI data centers.

- August 2025 - Nvidia ecosystem developments accelerated toward silicon photonics and co-packaged optics integration in next-generation AI switches, targeting large GPU clusters and high-bandwidth networking systems expected to scale into 2026 deployments.

- November 2025 - Lightwave Logic announced a co-development program with a Fortune 500 semiconductor partner to build 400G co-packaged optics solutions for AI data centers, focusing on electro-optic polymer integration into silicon photonics platforms for higher bandwidth and lower power optical interconnects.

- June 2024 - Samsung showcased its advanced semiconductor innovations at the Samsung Foundry Forum (SFF) in San Jose, unveiling cutting-edge 2nm (SF2Z) and 4nm (SF4U) process nodes.

- June 2024 - Intel demonstrated the world’s first fully integrated optical compute interconnect (OCI) chiplet co-packaged with an Intel CPU at the Optical Fiber Communication Conference (OFC).

- March 2024 - MediaTek entered the heterogeneous integration co-packaged optics space through a strategic partnership with Ranovus. The collaboration introduced a customized ASIC design platform tailored for next-generation CPO applications.

- March 2024 - Broadcom launched “Bailly,” the world’s first 51.2 Tbps co-packaged optics Ethernet switch, combining silicon photonics with its Tomahawk 5 switch architecture to improve efficiency and performance in AI data center infrastructure.

Why Choose DataM?

- Technological Innovations: Focuses on silicon photonics integration, co-integration of switch ASICs with optical engines, advanced thermal management systems, and high-density interconnect packaging. Innovations in low loss waveguides, multi wavelength lasers and on chip optical switching are enabling higher bandwidth scaling beyond traditional pluggable optics.

- Product Performance & Market Positioning: Evaluates performance metrics such as bandwidth density, power per bit efficiency, latency reduction and port scalability across OEM offerings. Leading vendors differentiate through tighter ASIC optical integration, improved thermal stability and support for AI optimized network architectures in hyperscale environments.

- Real World Evidence: Highlights deployment of co packaged optics in AI data centers, high performance computing clusters and cloud backbone infrastructure. Early implementations show measurable reductions in power consumption per switch system and improved data throughput efficiency in large scale AI training workloads.

- Market Updates & Industry Changes: Tracks advancements such as silicon photonics roadmaps, 800G and 1.6T networking transitions, hyperscaler pilot deployments, and increasing collaboration between semiconductor foundries and networking OEMs. Investments are also rising in advanced packaging facilities to support next generation optical integration.

- Competitive Strategies: Analyzes how companies are forming strategic alliances between ASIC designers, optical component manufacturers and foundries. Competitive differentiation is driven by early CPO prototypes, ecosystem partnerships, proprietary photonic integration platforms and hyperscaler co development programs.

- Pricing & Market Access: Reviews cost structures influenced by advanced packaging complexity, yield optimization challenges and early-stage manufacturing scale. Market access is currently concentrated among hyperscale cloud providers, AI infrastructure leaders and select telecom backbone operators due to high initial deployment costs.

- Market Entry & Expansion: Identifies growth opportunities driven by AI infrastructure scaling, data center modernization and transition toward high-speed Ethernet standards. Expansion strategies include ecosystem partnerships, co-development with hyperscalers and gradual migration from pluggable optics to integrated photonic architectures.