Circular Textiles Market Definition & Overview

What is the Circular Textiles Market?

The Circular Textiles Market covers products, materials, services, technologies and systems that keep textile resources in productive use for longer periods through reuse, repair, resale, remanufacturing, rental, mechanical recycling, chemical recycling and closed loop fiber recovery. The market includes post consumer and post industrial textile collection, sorting, fiber regeneration, recycled yarn production, circular apparel, home textiles, technical textiles, traceability platforms and reverse logistics. It also covers business models that reduce virgin fiber dependence, lower waste disposal, improve material transparency and help brands comply with emerging producer responsibility rules across global textile supply chains.

Circular Textiles Industry Background & Evolution

Parent market background: The parent textile market has historically grown through volume led production, low cost global sourcing, synthetic fiber expansion and fast inventory turnover. Circular textiles emerged as a response to waste generation, landfill pressure, volatile raw material prices and climate commitments across apparel, home textile, automotive and technical textile users. Roadmap evolution: 2015 to 2018 focused on resale, donation and recycled polyester from bottles. 2019 to 2021 expanded brand take back programs and traceability pilots. 2022 to 2024 shifted toward policy backed circular design, digital product passports and early chemical recycling scale up. 2025 to 2026 is moving toward mandatory textile waste rules, fiber to fiber partnerships, automated sorting and commercial offtake agreements. From 2027 to 2035, the market is expected to mature through regional recycling hubs, recycled content procurement and integrated circular supply contracts.

Circular Textiles Market Snapshot

| Metric | Details |

| Market Report Name | Circular Textiles Market |

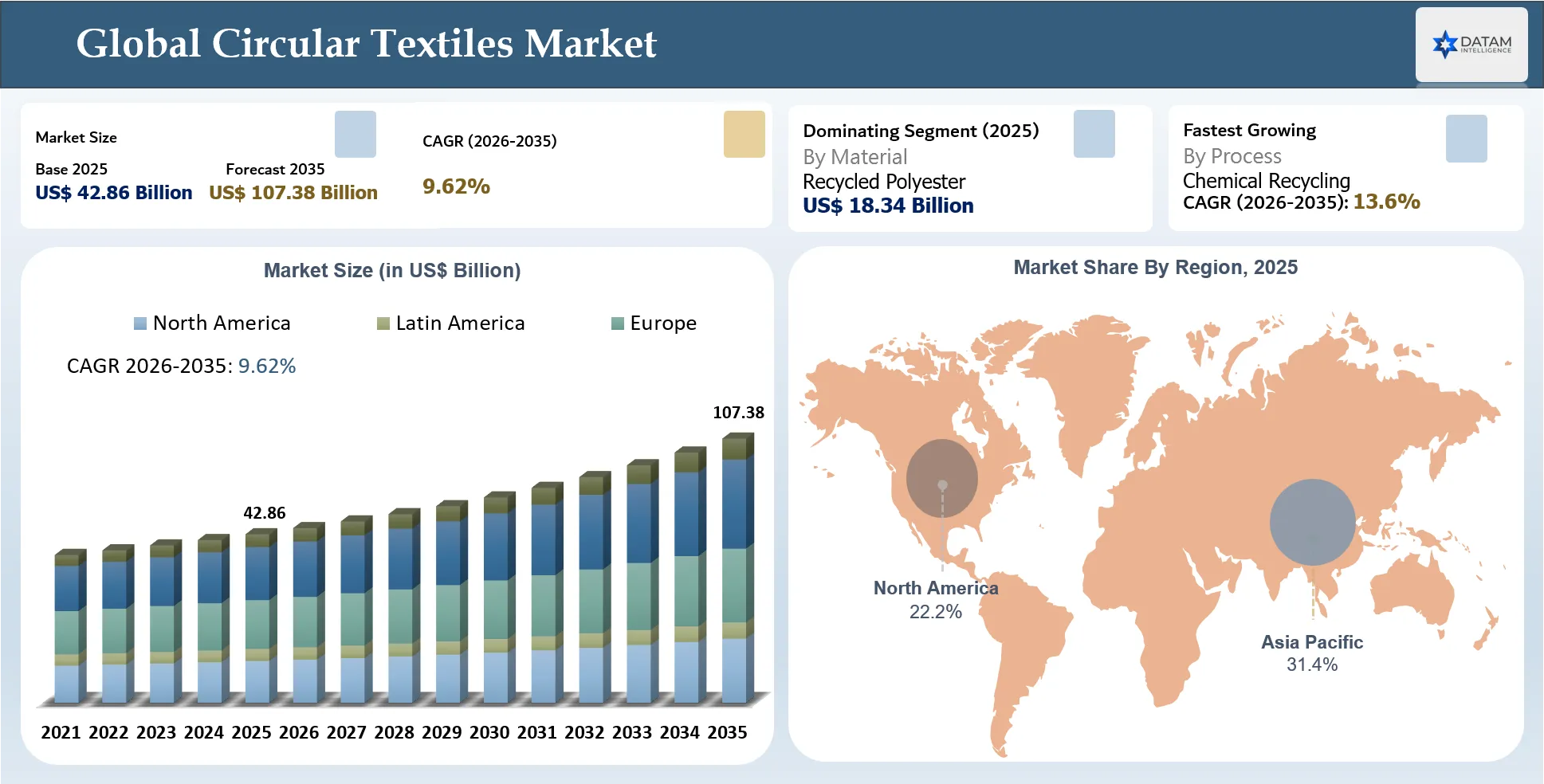

| Global Market Size (2025) | USD $42.86 Billion |

| Projected Market Size (2035) | USD $107.38 Billion |

| CAGR (2026-2035) | 9.62% |

| Largest Segment Name and Share | Recycled Polyester - 42.8% |

| Fastest Growing Segment Name and Share | Chemical Recycling - 13.6% |

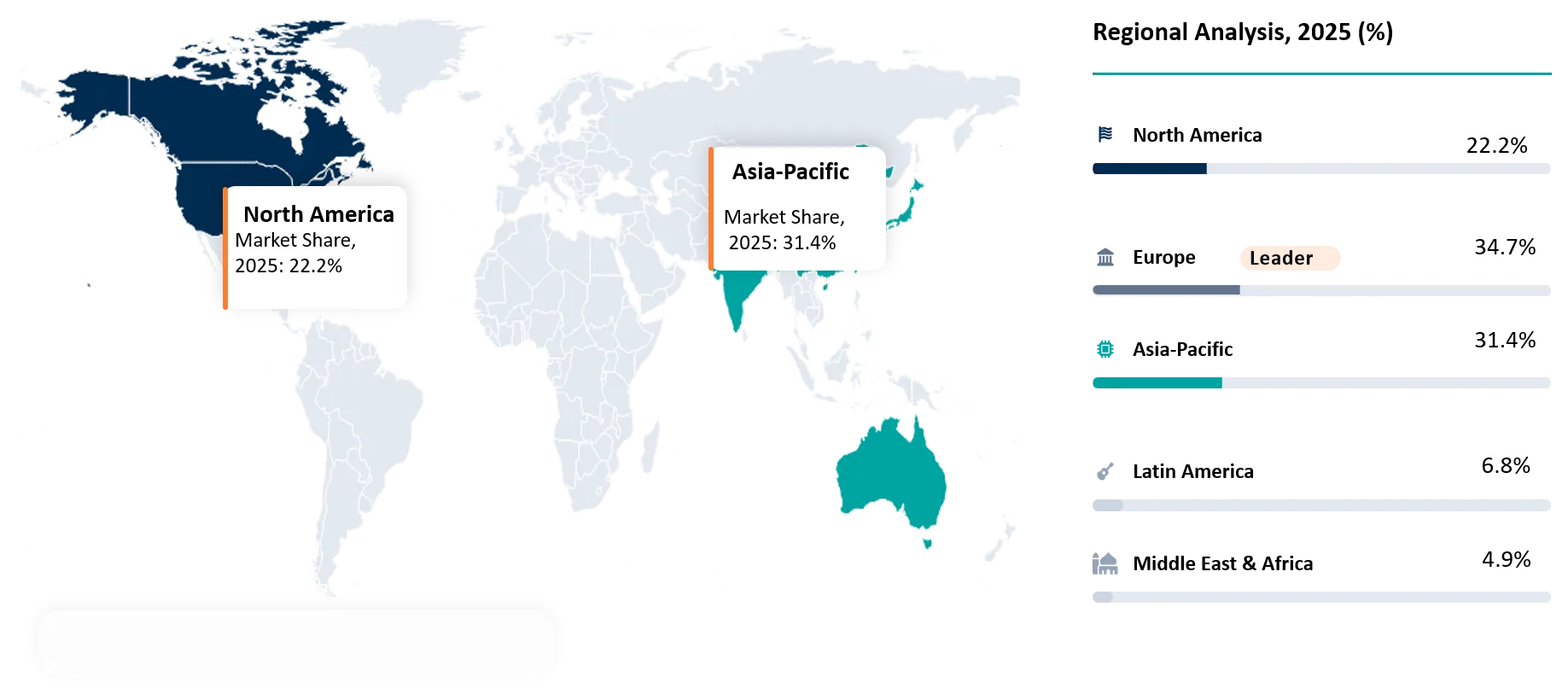

| Largest Region Name and Share | Europe - 34.7% |

| Fastest Growing Region Name and Share | Asia Pacific - 11.8% |

| Geographic Market Share for the 5 Regions | Europe: 34.7%; Asia Pacific: 31.4%; North America: 22.2%; Latin America: 6.8%; Middle East and Africa: 4.9% |

| Top Companies | Renewcell, Circ, Ambercycle, Evrnu, Worn Again Technologies, Infinited Fiber Company, Lenzing Group, Indorama Ventures, Eastman, Recover Textile Systems |

Global Circular Textiles Market Size & Forecast Analysis

Global Market Size (2025)

USD $42.86 Billion

Projected Market Size (2035)

USD $107.38 Billion

CAGR (2026–2035)

9.62%

Historical Circular Textiles Market Trend Analysis

During the last five years, the Circular Textiles Market moved from sustainability messaging toward operational redesign. Brand take back programs became more structured as retailers faced pressure to show measurable recovery rates. Recycled polyester remained the largest commercial pathway, although bottle based feedstock began to face credibility concerns because it diverts material from beverage loops. Mechanical recycling gained traction in cotton rich waste streams, while chemical recycling attracted investment for polyester cotton blends that traditional recycling systems struggle to process. Europe accelerated policy pressure through textile waste separation and producer responsibility discussions. Asia Pacific strengthened sorting, spinning and manufacturing capacity as brands looked for recycled inputs closer to production clusters. The major impact has been a shift in buyer evaluation from recycled content claims toward feedstock origin, chain of custody, material quality and scalable circular procurement contracts.

Circular Textiles Growth Outlook Summary

The Circular Textiles Market is expected to grow through a combination of regulation, brand procurement pressure and technology scale up. In the short term, from 2026 to 2028, growth will be led by Europe’s producer responsibility framework, higher textile waste collection volumes and expanded recycled polyester and recycled cotton procurement. In the mid term, from 2029 to 2031, fiber to fiber recycling plants, automated sorting systems and long term offtake agreements are expected to reduce supply uncertainty. In the long term, from 2032 to 2035, circular textiles are likely to shift from niche sustainability lines into mainstream fiber sourcing, particularly in apparel, home textiles and technical textile applications. The market outlook is strongest where policy, feedstock aggregation, recycling technology and brand demand converge. Profitability will depend on collection economics, output fiber quality, energy cost exposure and the ability to replace virgin inputs without disrupting performance specifications.

Circular Textiles Market Strategic Takeaways

- Europe remains the largest region because textile waste rules, circular design policy and producer responsibility schemes are forcing measurable recovery and recycled content planning.

- Asia Pacific is the fastest growing region as recycling capacity, AI sorting, textile manufacturing clusters and brand sourcing programs converge near major garment supply bases.

- Recycled polyester is the largest segment because it has established processing infrastructure, broad apparel use and strong compatibility with sportswear, fashion and home textile demand.

- Chemical recycling is the fastest growing process segment because blended fabrics, polyester cotton waste and high quality regenerated outputs require separation technologies beyond mechanical recycling.

- The market is moving toward long term offtake contracts as brands seek secure recycled fiber volumes before regulation tightens.

- Digital traceability is becoming a procurement requirement as buyers demand verifiable feedstock origin, recycling method and recycled content integrity.

- Textile recyclers with sorting access and brand partnerships are gaining strategic leverage because feedstock control is becoming as important as processing technology.

- Circular textiles are increasingly tied to country specific market policies, making regional compliance capability a core competitive advantage.

Circular Textiles Market White Space & Investment Opportunities

Investment opportunities are strongest where circular textile models solve supply gaps, compliance pressure and waste recovery challenges while creating repeatable commercial value for brands, recyclers and institutional buyers.

- Closed loop workwear programs are under served because industrial uniforms offer predictable composition, repeat purchase cycles and strong compliance value for large employers.

- Textile waste data platforms are gaining investment potential because brands need traceable recovery metrics for reporting, sourcing and EPR obligations.

- Regional cotton waste regeneration plants present a white space in South Asia and Latin America where garment manufacturing waste is abundant.

- Circular technical textiles remain under developed because automotive, filtration, insulation and protective fabrics require higher performance validation and specialized recycling pathways.

Circular Textiles Market Procurement & Buyer Behavior Analysis

Circular Textiles Market Buyer Decision-Making Criteria

Procurement teams are evaluating circular textile suppliers based on performance, proof, supply security and cost. Buyers want circular materials that can enter existing production lines without quality failures while supporting compliance and sustainability reporting.

- Verified recycled content and chain of custody documentation

- Consistent fiber quality, tensile strength, color performance and process compatibility

- Reliable delivery volume supported by secured feedstock and offtake planning

- Competitive cost compared with virgin and conventional recycled alternatives

- Certification coverage for chemical safety, recycled claims and responsible sourcing

- Ability to support country specific market compliance and reporting requirements

- Low contamination risk and clear material origin data

- Supplier roadmap for scaling capacity through 2035

Circular Textiles Market Economic & Investment Analysis

Circular Textiles Market Macroeconomic Impact Factors

Macroeconomic conditions influence the Circular Textiles Market through consumer spending, raw material prices, energy costs, labor availability and capital markets. Inflation can slow discretionary apparel purchases, but it also pushes brands to reduce waste and improve inventory recovery through resale and reuse. Volatile cotton and polyester prices increase interest in recycled inputs, especially when brands seek supply resilience. Energy prices affect chemical recycling economics because depolymerization, dissolution and regeneration processes can be energy intensive. Labor costs increase the value of automated sorting and digital traceability tools. Interest rates influence the financing of recycling plants, which require patient capital and long term offtake confidence. Trade tensions and nearshoring strategies also support regional circular hubs because brands want lower transport risk and faster supply response. Overall, macroeconomic pressure is pushing the market toward efficiency, local recovery and contract backed investment models.

Circular Textiles Investment Trends in the Market

Investment is moving from brand pilots into infrastructure, technology scale up and offtake supported capacity creation. Investors are prioritizing circular systems that can secure feedstock and prove commercial demand.

- AI sorting and automated grading systems

- Chemical recycling for polyester and blended fabrics

- Textile to textile recycled polyester capacity

- Digital traceability and product passport platforms

Circular Textiles Market Funding & M&A Activity

Future funding and M&A activity is expected to focus on commercial scale recycling plants, feedstock aggregation, material technology and partnerships that give brands secure circular supply. Investors are favoring companies with offtake agreements, proven output quality and strong policy tailwinds.

- April 2025: Circ raised US $25 Million in funding led by Taranis to scale textile recycling and advance industrial facility development.

- February 2025: Ambercycle and Huilong announced a partnership to scale circular polyester materials and accelerate adoption in textile manufacturing.

- November 2025: Indorama Ventures and Jiaren Chemical Recycling formed a joint venture to enhance global textile circularity through polyester recycling.

- 2025 to 2026: Strategic investment focus shifted toward feedstock control, recycling plants and brand backed offtake structures.

Circular Textiles Market Regulatory & Policy Analysis

Circular Textiles Market Regulatory Framework Overview

The regulatory framework for circular textiles is led by waste reduction, producer responsibility, eco design, green claims and recycling policy. Europe is the most advanced region, with the EU Strategy for Sustainable and Circular Textiles shaping expectations around durability, recyclability, digital product passports and textile waste accountability. The revised EU Waste Framework Directive increases pressure on textile and footwear producers to manage end of life flows. Other regions are moving more gradually through waste diversion targets, public procurement rules, recycling incentives and product transparency requirements.

- September 2025: EU Parliament approved revised textile waste rules, increasing producer responsibility and creating stronger demand for collection and recycling services.

- 2025 to 2026: Digital product passport preparation accelerated, improving traceability requirements for fiber composition and product lifecycle data.

- 2026: Green claims scrutiny increased, pushing brands toward verified recycled content and credible circularity evidence.

Circular Textiles Policy Impact on Market Growth

Policy is increasing market growth by turning textile waste into a measurable producer responsibility issue. It also supports investment because future demand for recycling, sorting, repair and traceability becomes more predictable.

- EU producer responsibility rules increase demand for formal textile collection, sorting and recycling contracts.

- Public procurement sustainability criteria support circular uniforms, linens, workwear and institutional textiles.

- Waste diversion policies improve feedstock availability by moving textiles away from landfill and incineration.

- Green claims rules increase demand for certified data, chain of custody and verified recycled content.

Circular Textiles Market Trends & Innovation Landscape

Circular Textiles Key Market Trends

Circular textile demand is shifting from brand image projects toward operational procurement. Buyers are focusing on material origin, recycling method, verified chain of custody and long term supply security because recycled content claims are facing stronger scrutiny.

- Fiber to fiber recycling is moving from pilot programs into commercial offtake agreements as brands seek apparel grade recycled inputs.

- Automated sorting is becoming a critical infrastructure layer because mixed textile waste requires accurate fiber identification before recycling.

Circular Textiles Market Technology Advancements

Technology development is centered on improving yield, output quality and feedstock flexibility. The most important advances are those that convert mixed waste into fibers that mills can process without major performance loss.

- February 2025: Ambercycle and Huilong announced a partnership to scale circular polyester materials, improving commercialization routes for textile derived recycled polyester.

- November 2025: Indorama Ventures and Jiaren Chemical Recycling formed a joint venture to enhance global textile circularity through polyester chemical recycling capability.

Circular Textiles Industry Transformation Trends

The industry is transforming through closer integration between waste management, textile manufacturing and retail operations. Circularity is creating new commercial links between garment collection, digital sorting, fiber regeneration, spinning and branded product development. Large brands are moving toward offtake agreements to secure circular input volumes. Recycling companies are moving upstream into collection partnerships and downstream into material qualification with mills. Textile mills are adapting spinning and finishing processes to handle recycled fibers with variable properties. Retailers are becoming reverse logistics operators because product returns, take back programs and resale channels now influence customer lifetime value. The market is headed toward regional circular ecosystems where waste generated in one market can be processed and reused within nearby manufacturing or consumption networks.

Circular Textiles Market Disruption Analysis

The circular textiles market is being disrupted by regulation and technology at the same time. Regulation is changing the cost structure of textile waste by forcing brands to account for collection, treatment and recyclability. Technology is changing material recovery through AI sorting, chemical recycling, enzymatic processing and digital traceability. The combined impact is shifting power from traditional linear suppliers toward companies that control waste feedstock, recycling intellectual property and verified data. Disruption is also emerging in business models as resale, rental, repair and take back programs create revenue beyond first sale. By 2035, circularity could become a standard sourcing requirement for large brands rather than a separate sustainability initiative.

Circular Textiles Market Disruption & Structural Shift Analysis

Technology Disruption Impact

Technology disruption is changing circular textiles by improving material recovery from waste streams that were previously downcycled or discarded.

- AI sorting is disrupting textile waste economics by increasing classification speed, reducing contamination and improving feedstock quality for recyclers.

- Chemical recycling is disrupting blended fabric recovery by enabling polyester and cellulose separation from complex garments.

- Digital product passports are disrupting compliance by linking product composition data with end of life processing routes.

- Advanced regenerated fibers are disrupting virgin material procurement by offering circular inputs with comparable performance for selected applications.

Circular Textiles Future Market Transformation

By 2035, the Circular Textiles Market is expected to transform from project-based sustainability programs into a recurring sourcing and compliance system. Brands will treat circular fibers as strategic materials rather than experimental inputs. Recycling companies will increasingly sell certified outputs through long term contracts, while digital platforms will verify product composition and recycled content. Business models will expand around repair, resale, rental and material recovery services. Regional hubs will process textile waste near consumption or manufacturing centers, reducing transport cost and improving compliance. The future market will reward companies that combine circular design, feedstock access, technology scale and transparent data.

Circular Textiles Market Growth Dynamics

Circular Textiles Market Drivers

- Regulatory pressure on textile waste is accelerating collection, sorting and recycling investments because producers need compliant end of life pathways for apparel, footwear and home textiles.

- Brand decarbonization targets are increasing demand for recycled fibers because material sourcing represents a large share of product emissions and supply chain risk.

- Feedstock volatility in cotton, polyester and viscose is making circular inputs more attractive for buyers seeking resource resilience and predictable sourcing.

- Consumer resale and repair adoption is expanding circular business models because buyers increasingly accept longer product lifecycles and authenticated second life channels.

Circular Textiles Market Driver Impact Assessment

| Driver | Market Growth Impact (%) | Demand Concentration | Impacted Use Case | Strategic Impact |

| Regulatory textile waste mandates | 4.8% | Europe, North America, Japan | Collection, sorting, EPR compliance | Pushes brands into formal recycling partnerships and traceable waste recovery. |

| Brand recycled content procurement | 4.4% | Apparel brands, sportswear brands, retailers | Recycled polyester, recycled cotton, circular apparel | Creates long term offtake demand for consistent recycled fiber supply. |

| Automated sorting deployment | 3.9% | China, EU recycling hubs, United States | Fiber identification, waste grading, feedstock aggregation | Improves yield and lowers contamination risk for recycling plants. |

| Chemical recycling scale up | 3.7% | Polyester cotton blends, performance textiles, mixed waste | Fiber to fiber outputs, specialty circular materials | Unlocks waste streams that mechanical recycling cannot upgrade effectively. |

Circular Textiles Market Restraints

- High collection and sorting costs restrict margins because textile waste is fragmented across households, retailers, municipalities and informal recovery networks.

- Inconsistent recycled fiber quality limits adoption in premium apparel and technical textiles where strength, color and durability specifications are strict.

- Chemical recycling plants require high capital investment, steady feedstock and energy optimization, creating scale barriers for early commercial projects.

- Weak labeling and blend complexity reduce recycling yields because garments often contain elastane, trims, coatings and mixed fibers that complicate separation.

Circular Textiles Market Restraint Impact Assessment

| Restraint | Drag on Market Growth (%) | Primary Impact Area | Impacted Use Case | Strategic Impact |

| Fragmented feedstock supply | 4.1% | Collection networks and sorting hubs | Post consumer textile recycling | Raises cost and creates supply uncertainty for recyclers. |

| Quality variation in recycled fibers | 3.8% | Yarn mills and textile manufacturers | Apparel, home textiles, technical textiles | Slows substitution of virgin fibers in performance focused products. |

| Capital intensity of chemical recycling | 3.6% | Recycling plant financing | Polyester cotton blend recovery | Delays industrial scale deployment without offtake guarantees. |

| Material blend complexity | 3.4% | Product design and end of life processing | Stretch apparel, coated fabrics, footwear | Forces redesign toward recyclable construction and better labeling. |

Emerging Circular Textiles Growth Factors

Circular textile growth is moving toward scalable systems where technology, regulation, feedstock control and brand offtake combine to improve recycling economics and long term market adoption across regions.

- AI sorting is improving fiber identification, contamination control and plant throughput, enabling recyclers to process mixed textile waste with higher confidence and lower manual labor dependence.

- Enzymatic and solvent based recovery technologies are widening circular options for cotton rich and polyester rich waste streams that need high purity regenerated outputs.

- Brand backed offtake agreements are improving bankability by giving recyclers committed demand before they build commercial plants.

- Extended producer responsibility systems are turning textile waste from a disposal issue into a measurable compliance cost that supports circular service demand.

Circular Textiles Market Segmentation Analysis

Circular Textiles Market by Material Trends

Recycled polyester is the leading material segment because polyester dominates global apparel and home textile production, while recycling technologies and supply chains are more mature than most alternatives. The major trend is the transition from bottle derived recycled polyester toward textile derived recycled polyester, which improves circular credibility and reduces competition with packaging recycling loops. Brand demand is strongest in sportswear, fashion basics, uniforms and home textiles where polyester performance is valued. The market is headed toward higher textile waste based content, stronger certification and closer integration between chemical recyclers and yarn producers.

Circular Textiles Market by Process Trends

Mechanical recycling remains commercially important because it is lower cost and suitable for cotton, wool and some single fiber textile waste streams. However, chemical recycling is becoming the fastest growing process because it can address blended fabrics and produce higher quality regenerated outputs. The major trend is a two track system where mechanical recycling handles cleaner industrial scrap and chemical recycling handles complex post consumer waste. The market is headed toward hybrid facilities combining automated sorting, mechanical pre processing and chemical recovery to improve yield and broaden accepted feedstock types.

Circular Textiles Market by Application Trends

Apparel remains the largest application because fashion, sportswear, uniforms and basics generate high waste volumes and face strong consumer and regulatory scrutiny. The major trend is movement from limited capsule collections toward recurring circular sourcing programs with measurable recycled content. Home textiles and hospitality products are also growing because bulk replacement cycles create predictable waste streams. The market is headed toward product categories where material specifications can be standardized, allowing recycled fibers to be blended into mainstream collections without major design or performance compromises.

Circular Textiles Market by End User Trends

Fashion brands and retailers are the largest demand group because they face direct pressure from consumers, regulators and investors to reduce textile waste. The major trend is the shift from voluntary take back programs to structured reverse logistics, resale integration and long term offtake contracts with recyclers. Textile mills are becoming more active buyers as recycled yarn demand increases. The market is headed toward strategic partnerships where brands, mills and recyclers co design materials, secure feedstock and share data for compliance and quality control.

Circular Textiles Market Regional Analysis

North America Circular Textiles Market

North America Circular Textiles Market is supported by brand sustainability commitments, resale growth, retail take back programs and rising state level interest in textile waste diversion. The 2025 market size is estimated at USD $9.51 Billion and is forecast to reach USD $22.14 Billion by 2035. Demand is strongest in apparel resale, recycled polyester, recycled cotton, uniforms and home textiles. Production capacity is shifting from small recovery programs toward regional sorting hubs, mechanical recycling facilities and specialty chemical recycling partnerships. The United States is leading demand because large fashion retailers and sportswear brands are seeking recycled content and traceable sourcing. Canada is gaining momentum through circular economy programs and municipal waste reduction strategies. The region still faces fragmented collection infrastructure and cost pressure, which limits rapid scale. Over the next decade, growth will be shaped by stronger retailer participation, public procurement, investor backing for recycling technology and increased use of circular textiles in workwear, hospitality and automotive interior applications.

Europe Circular Textiles Market

Europe Circular Textiles Market is the largest regional market, with 2025 size estimated at USD $14.87 Billion and projected size of USD $35.09 Billion by 2035. Growth is being shaped by the EU Strategy for Sustainable and Circular Textiles, textile waste separation rules, producer responsibility measures and higher scrutiny of green claims. Demand is strongest in recycled apparel, circular home textiles, repair, resale and fiber to fiber recycling. Production capacity is expanding through sorting centers, textile recycling pilots and commercial partnerships between brands, recyclers and mills. Western Europe leads adoption through policy pressure and premium brand participation, while Central and Eastern Europe are becoming attractive for processing and reverse logistics. The market is headed toward compliance driven circular sourcing, digital product passports and regional material recovery networks that reduce landfill and incineration exposure.

Asia Pacific Circular Textiles Market

Asia Pacific Circular Textiles Market is the fastest growing region, with 2025 size estimated at USD $13.46 Billion and forecast to reach USD $41.09 Billion by 2035. Growth is supported by the region’s massive textile manufacturing base, growing domestic apparel consumption and investment in automated sorting and chemical recycling. China is leading through high volume textile waste processing and AI sorting deployment. Japan is advancing through recycling technology and disciplined waste management systems. India offers strong potential due to cotton waste availability, garment manufacturing clusters and rising sustainability targets among exporters. Production capacity is moving closer to apparel manufacturing hubs, which improves recycled yarn integration. Demand is increasingly shaped by global brands asking suppliers to provide recycled content, traceability and lower impact materials for export markets.

Circular Textiles Market Country-Level Analysis

United States Circular Textiles Market Size/Forecast

The United States Circular Textiles Market is estimated at USD $7.41 Billion in 2025 and forecast to reach USD $17.31 Billion by 2035. Growth is supported by large apparel retailers, sportswear brands, resale platforms and rising attention to textile waste policy. Demand is strongest in recycled polyester, recycled cotton, uniforms, resale, repair and branded take back programs. Production capacity is expanding through sorting pilots, specialty recycling facilities and material innovation partnerships. The market remains challenged by fragmented collection infrastructure and price sensitivity. Over the forecast period, growth is expected to strengthen as brands seek country specific market compliance, verifiable recycled content and domestic circular sourcing resilience.

Japan Circular Textiles Market Size/Forecast

Japan's circular textiles market is estimated at USD $1.62 Billion in 2025 and forecast to reach USD $3.96 Billion by 2035. The country benefits from disciplined waste management, strong material engineering and consumer acceptance of high quality sustainable products. Demand is concentrated in apparel, uniforms, home textiles and technical textile applications. Japanese companies are exploring chemical recycling, fiber regeneration and closed loop manufacturing to reduce dependence on virgin inputs. Production capacity is likely to expand through partnerships between chemical companies, textile mills and brand owners. Market growth will be shaped by quality standards, traceability and demand for circular materials with reliable performance.

China Circular Textiles Market Size/Forecast

China's circular textiles market is estimated at USD $5.94 Billion in 2025 and forecast to reach USD $19.34 Billion by 2035. China is central to circular textile growth because it combines massive textile production, large domestic waste streams and rapid deployment of automated sorting technology. Demand is driven by export brands, domestic apparel platforms, recycling companies and policy pressure to improve resource efficiency. Production capacity is expanding through AI sorting systems, chemical recycling partnerships and regenerated polyester supply chains. The market is headed toward industrial scale circularity where automated collection, sorting and fiber recovery support both domestic consumption and global export requirements.

India Circular Textiles Market Size/Forecast

India's circular textiles market is estimated at USD $2.04 Billion in 2025 and forecast to reach USD $6.79 Billion by 2035. Growth is supported by a large textile manufacturing base, cotton waste availability, export buyer requirements and government focus on textile sector expansion. Demand is strongest in recycled cotton, industrial scrap recovery, denim, home textiles and apparel export supply chains. Production capacity is fragmented but improving through spinning clusters, textile recycling startups and sustainability programs among exporters. India’s opportunity lies in converting post industrial waste into higher value circular yarns while building collection systems for post consumer textiles. Forecast growth depends on traceability, certification access and buyer funded capacity creation.

Circular Textiles Market Other Key Countries

Germany Circular Textiles Market: Germany is a key European circular textile hub because of strong recycling research, brand participation and policy alignment with EU waste rules. Demand is growing in apparel, automotive textiles, technical textiles and home textile recovery.

France Circular Textiles Market: France is advancing through producer responsibility systems, repair incentives and circular fashion programs. The market benefits from premium brand engagement and strong policy pressure on waste reduction.

United Kingdom Circular Textiles Market: The UK market is shaped by resale platforms, charity collection networks, retailer take back programs and circular fashion innovation. Growth depends on improving fiber sorting and domestic recycling capacity.

Italy Circular Textiles Market: Italy’s textile clusters create opportunities in luxury waste recovery, wool recycling and high value regenerated fibers. The country is positioned for premium circular material development.

Turkey Circular Textiles Market: Turkey is growing as a circular production base due to textile manufacturing strength, proximity to Europe and demand from brands seeking regional recycled content sourcing.

Circular Textiles Market Competitive Landscape

Competitive Benchmarking

Competitive benchmarking in circular textiles is shifting from sustainability claims toward measurable scale, material performance, offtake security and regional supply readiness. Leading players differ by process focus and customer target.

- Circ focuses on blended textile recycling and targets fashion brands needing polyester and cellulose recovery from complex waste.

- Ambercycle focuses on circular polyester through Cycora and targets apparel brands seeking textile derived recycled polyester with strong performance.

- Infinited Fiber Company focuses on regenerated cellulose from cotton rich waste and targets premium apparel brands seeking cotton like circular fibers.

- Indorama Ventures focuses on polyester scale and technical textile applications, using global manufacturing reach and partnerships to support circular supply.

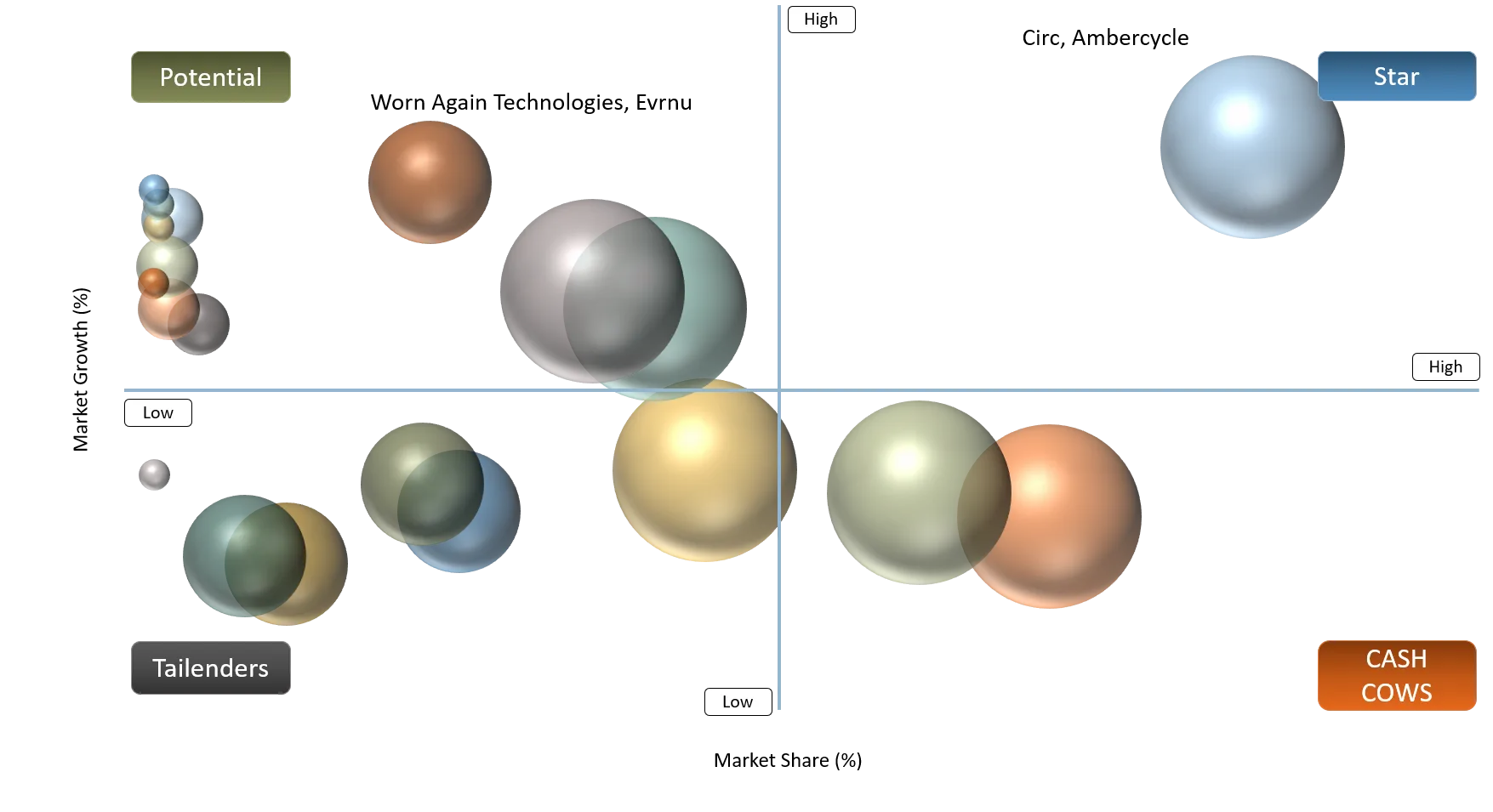

Circular Textiles Market BCG Matrix List

Stars: Circ, Ambercycle

Question Marks: Worn Again Technologies, Evrnu

Cash Cows: Lenzing Group, Indorama Ventures

Niche Players: Recover Textile Systems, Infinited Fiber Company

Circular Textiles Market BCG Matrix Analysis

Stars such as Circ and Ambercycle are positioned in high growth areas because they address major pain points in textile derived recycling, blended waste and circular polyester demand. Their growth potential is supported by brand partnerships, investor attention and the shift from pilot projects toward offtake based commercialization. Question Marks such as Worn Again Technologies and Evrnu have differentiated technology but face scale, financing and adoption risk as buyers wait for consistent output and reliable supply. Cash Cows such as Lenzing Group and Indorama Ventures benefit from established manufacturing networks, customer relationships and material expertise, giving them stronger resilience as circular products expand. Niche Players such as Recover Textile Systems and Infinited Fiber Company occupy focused positions in mechanically recycled cotton or regenerated cellulose, where specialized capabilities can support premium buyers but scale may be narrower than broad polyester platforms.

Circular Textiles Market Expansion & Partnership Strategy

Expansion strategies are centered on offtake agreements, joint ventures and manufacturing partnerships that reduce commercialization risk. Partnerships help recyclers secure customers while helping brands lock in future circular material supply.

- February 2025: Ambercycle and Huilong announced a partnership to scale circular polyester materials, improving access to dope dyed yarn manufacturing and accelerating commercialization in Asia.

- November 2025: Indorama Ventures and Jiaren Chemical Recycling formed a joint venture to enhance polyester textile circularity, strengthening global capacity for chemical recycling and regenerated fibers.

- April 2025: Circ secured US $25 Million led by Taranis to scale textile recycling and support movement toward industrial facility development.

- 2025: Ganni expanded its circular polyester sourcing relationship with Ambercycle through a long-term offtake model, helping validate demand for textile derived recycled polyester.

Circular Textiles Market Key Developments (2025–2026)

Major Industry Developments

Major developments show that circular textiles are moving from pilot stage toward policy backed infrastructure and commercial partnerships. Activity in 2025 and 2026 is focused on producer responsibility, recycling scale up and technology deployment.

- February 2025: Ambercycle and Huilong announced a partnership to scale circular polyester materials for textile manufacturing.

- April 2025: Circ secured US $25 Million led by Taranis to support textile recycling scale up and industrial facility plans.

- September 2025: EU Parliament approved revised textile waste rules, strengthening producer responsibility and circularity requirements.

- November 2025: Indorama Ventures and Jiaren Chemical Recycling formed a joint venture to enhance global polyester textile circularity.

Circular Textiles Recent Market Announcements

September 2025: The European Parliament approved revised textile waste rules under the Waste Framework Directive, increasing producer responsibility for the end of life management of textile and footwear products. The announcement is important because it makes circularity a direct compliance issue for brands selling into Europe. Producers will need stronger collection systems, recycling partnerships and reporting capabilities. The impact on the market is expected to be higher demand for sorting, traceability, repair, reuse and fiber recovery services. It also improves investor confidence because future recycling demand becomes more policy backed and less dependent on voluntary sustainability budgets.

Circular Textiles Market Technology Launches & Partnerships

Technology launches and partnerships are accelerating commercialization by connecting recycling innovation with manufacturing capacity and brand demand. The strongest announcements are those that improve scale, reduce quality risk and create clearer routes to market.

- February 2025: Ambercycle and Huilong partnered to scale circular polyester materials, supporting manufacturing integration in Asia.

- November 2025: Indorama Ventures and Jiaren Chemical Recycling formed a joint venture to strengthen polyester recycling capacity.

- April 2025: Circ funding supported movement from demonstration scale toward industrial textile recycling.

- 2025: AI sorting deployment in China demonstrated faster material classification and lower unrecyclable waste rates.

Circular Textiles Market Strategic Insights & Analyst Perspective

Analyst Insights of Circular Textiles Market

DataM Intelligence views the Circular Textiles Market as a structural transition market where regulation, brand commitments and material technology are converging. The market is moving beyond sustainability storytelling into measurable business outcomes such as waste cost reduction, recycled content security, compliance readiness and lower virgin material exposure. The strongest growth will come from segments where circular materials solve both environmental and procurement problems. Recycled polyester will remain the largest material category, while chemical recycling will grow fastest because it addresses blended fabrics and higher quality output requirements. Europe will lead market share due to policy pressure, while Asia Pacific will deliver the highest growth due to manufacturing scale and technology deployment. The main bottleneck remains feedstock quality and collection economics. Companies with access to sorted textile waste, validated recycling technology and committed buyers will outperform. The market will also reward suppliers that provide transparent data because circularity claims face increasing scrutiny. By 2035, circular textiles are expected to become a standard sourcing pillar for large brands, technical textile producers and institutional buyers. The forecast indicates that market winners will combine operational scale with credible circular impact measurement.

Strategic Recommendations of Circular Textiles Market

Recommendation 1: Companies should prioritize feedstock security before expanding processing capacity. The most attractive strategy is to build partnerships with retailers, municipalities, laundries, hospitality groups and uniform providers that generate predictable textile waste. Secure feedstock improves plant utilization, lowers sorting risk and supports stronger buyer commitments. Firms should also invest in automated sorting and material databases to improve recovery yield. A company that controls input quality can negotiate better offtake contracts and reduce production variability. This strategy improves margins and creates a defensible position as policy increases competition for textile waste.

Recommendation 2: Companies should focus commercialization on two scalable use cases before broad portfolio expansion. Apparel grade recycled polyester and institutional textile recovery offer strong near term demand because they combine large volume, clear buyer need and measurable sustainability value. Firms should avoid overextending into too many fiber types before proving quality and cost performance. Strategic partnerships with mills and brands can help qualify materials faster and secure repeat demand. This focused approach supports faster market entry, stronger quality control and better investment credibility.

Circular Textiles Market Future Market Outlook (2035 Vision)

In 2025, the Circular Textiles Market is still characterized by fragmented feedstock, pilot scale recycling, uneven policy enforcement and limited availability of apparel grade fiber to fiber outputs. Many brands use circular textiles in selected product lines, while mainstream sourcing remains dependent on virgin and conventional recycled materials. By 2035, the market is expected to be significantly more integrated and compliance driven. Producer responsibility rules, digital product passports and recycled content targets will make circularity part of core procurement. Automated sorting will improve feedstock quality, while chemical recycling and regenerated fibers will expand the usable waste base. Regional hubs will reduce transport dependency and improve country specific market responsiveness. Brands will increasingly use circular textiles for apparel, home textiles, uniforms and technical applications. The business model will shift from one time product sales toward lifecycle services including repair, resale, take back, material recovery and verified circular sourcing contracts.

Circular Textiles Market Target Audience

- Textile recycling companies: Need market size, forecast, feedstock trends and investment priorities to plan capacity and partnerships.

- Apparel brands and retailers: Need circular sourcing insights to reduce waste exposure, improve recycled content planning and support compliance.

- Textile mills and yarn producers: Need segment demand, material trends and technology shifts to qualify circular fibers.

- Investors and private equity firms: Need growth outlook, funding trends and competitive benchmarking to identify scalable opportunities.

- Waste management companies: Need insights on textile collection, sorting and producer responsibility driven revenue models.

- Hospitality and institutional buyers: Need procurement intelligence for circular linens, uniforms and closed loop textile programs.

- Policy and regulatory bodies: Need market impact analysis to support circular economy planning and waste infrastructure decisions.

- Chemical and material companies: Need technology pathways and partnership opportunities in regenerated fibers and polymer recycling.

Who Should Buy this Report?

This report is designed for organizations that need a detailed, outcome focused view of circular textile opportunities, risks, market size, market share, forecast, country specific market trends and competitive strategy. It helps buyers understand where growth is occurring and how to position for circular textile adoption.

- Brands seeking circular sourcing strategies

- Recyclers planning capacity expansion

- Textile mills evaluating recycled fiber integration

- Investors assessing circular economy opportunities

- Retailers building take back and resale models

- Institutional buyers procuring circular uniforms and linens

- Technology providers targeting sorting, traceability and recycling systems

- Policymakers designing textile waste programs

Why Choose DataM Intelligence?

- Business outcome focus: DataM Intelligence connects market forecast data with procurement, investment and commercialization implications for decision makers.

- Segment depth: The report breaks down materials, recycling processes, applications, end users and regions to identify specific growth pockets.

- Competitive strategy clarity: The analysis benchmarks players by portfolio, target strategy, partnerships and market positioning.

- Policy impact assessment: The report explains how producer responsibility, digital product passports and green claims rules affect market growth.

- Investment guidance: DataM highlights white space opportunities, funding shifts and scalable business models across circular textile value chains.

- Country specific market intelligence: The report supports localized planning by assessing major regions and key countries.

- Buyer behavior analysis: The report explains procurement criteria, risks and supplier selection priorities for circular textile solutions.

- Future outlook: DataM provides a 2035 vision to help clients align near term actions with long term market transformation.