Circular Polymers Market Definition and Overview

The global Circular Polymers market reached USD 88.9 billion in 2025 and is expected to reach USD 248.3 billion by 2035, growing with a CAGR of 10.82% during the forecast period 2026-2035, due to increase in the adoption of recycled and chemically produced polymers as the global plastics industry generated around 413 million metric tons of plastics in 2025 according to the Plastics Europe, with the recycling rate of plastics accounting for 9.8% in global plastics production. The European Union's Packaging and Packaging Waste Regulation (PPWR) and the expansion of the Extended Producer Responsibility (EPR) scheme in 2025-2026 in the European Union, as well as in Europe and Asia, led to increased demand for polymers that have certified recycled content, thereby forcing leading resin producers to invest in advanced recycling capacity and closed-loop polymer agreements.

Meanwhile, investment in chemical recycling technology through techniques such as pyrolysis, depolymerization, and solvent purification continued to rise, leading to better availability of food-grade and engineering-grade circular polymers for various uses, including in packaging, automotive, and consumer products. While market prospects remain promising, limited availability of waste feedstocks, inadequate collection infrastructure, and high capital expenditure on advanced recycling plants have been the main barriers. In July 2025, Loop Industries launched Twist™, a premium brand of circular polyester resins. It is an excellent polyester resin, entirely produced from waste fabrics through the company’s patented process of depolymerization. The resins are intended for use in the production of fashion, sportswear, and home textiles and have the ability to emit up to 81% less greenhouse gas than traditional fossil fuel-based polyester resins.

Key Takeaways

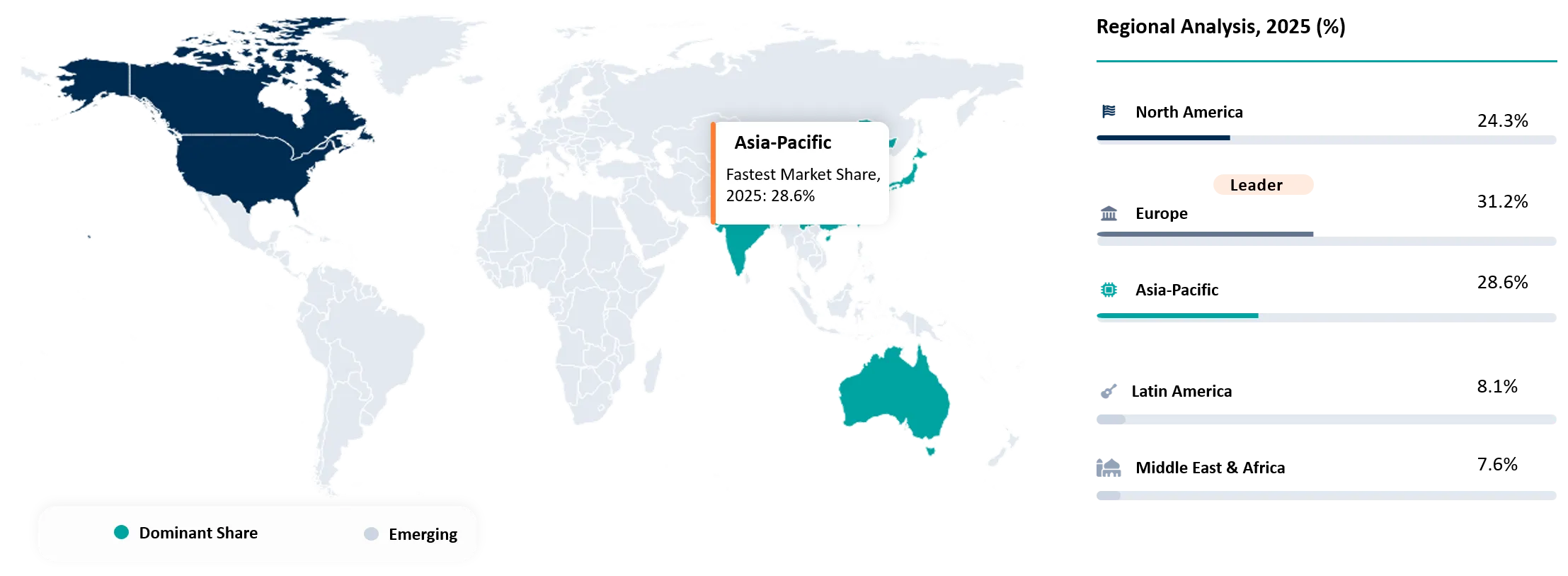

- Europe established the highest regional dominance in the circular polymers market, capturing an approximate share of 31.22% of the overall market in 2025.

- The global plastics industry generated around 413 million metric tons of plastics in 2025, according to data from Plastics Europe. Out of this massive volume, the actual recycling rate of plastics accounted for only 9.8% of global plastics production.

- According to the OECD Global Plastics Outlook, only 9% of global plastic waste gets successfully recycled. Meanwhile, another 22% is completely mismanaged, which severely restricts the pool of high-quality feedstock available for premium recycling.

- The mechanical recycling segment heavily dominated the circular polymers market, holding a global market share of about 63.5% in 2025.

- Germany held the largest share of the European circular polymers market, occupying an individual market share of 24.8% in 2025. The country's strong position is fueled by its mature polymer production sector, highly efficient recycling facilities, and strict compliance regulations.

Circular Polymers Market Industry Trends and Strategic Insight

- Chemical recycling is becoming a strategic complement to mechanical recycling rather than an alternative. Polymer manufacturers have developed large-scale pyrolysis, depolymerization, and solvent purification technologies in order to effectively recycle the plastic material that cannot be easily recycled by mechanical recycling systems.

- Packaging manufacturers are reshaping polymer procurement and sourcing around recycled-content regulations. The adoption of the PPWR and other EPR schemes is accelerating long-term purchasing practices.

- Digital traceability is being incorporated into polymer value chains. it has become mandatory to provide information on recycled content, origin of polymer, lifecycle emissions, and chain of custody information, thus promoting digital product passports.

- Automotive and consumer goods manufacturers are adopting circular polymers in their product designs. Vehicle parts, consumer goods, household appliances, and electronic enclosures are increasingly being designed using engineered plastics made from certified recycled materials.

- Expansion in capacity is being increased in modern recycling centers that are complemented by petrochemical industry facilities. The large manufacturers of resins are undertaking construction of chemical recycling plants alongside their existing polymer manufacturing facilities in order to enhance efficiency, lower transport costs, and manufacture virgin polymers from recycled feedstock.

Circular Polymers Market Scope

| Metrics | Details | |

| 2025 Market Size | USD 88.9 Billion | |

| 2035 Projected Market Size | USD 248.3 Billion | |

| CAGR (2026-2035) | 10.82% | |

| Largest Market | Europe | |

| Fastest Growing Market | Asia Pacific | |

| By Polymer Type | Polyethylene (PE), Polypropylene (PP), Polyethylene Terephthalate (PET), Polyvinyl Chloride (PVC), Polystyrene (PS), Polyamide (PA), Polycarbonate (PC), Acrylonitrile Butadiene Styrene (ABS), Others | |

| By Circular Process | Mechanical Recycling, Chemical Recycling, Dissolution-Based Recycling, Depolymerization, Bio-Circular Polymers, Others | |

| By Form | Recycled Resins/Pellets, Polymer Compounds, Polymer Flakes, Polymer Powders, Reprocessed Granules, Others | |

| By End-use | Packaging, Automotive & Transportation, Building & Construction, Electrical & Electronics, Consumer Goods, TextilesIndustrial Manufacturing, Agriculture, Others | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Türkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

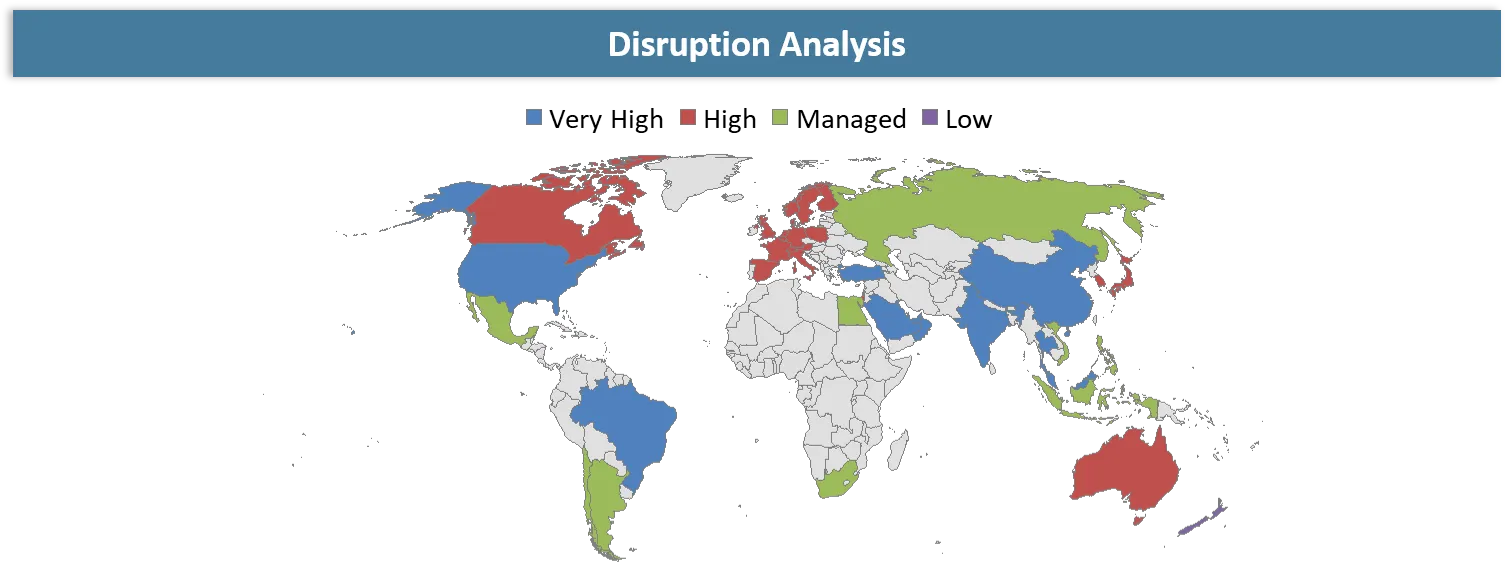

Circular Polymers Market Disruption Analysis

Advanced Chemical Recycling Reshaping the Circular Polymers Value Chain

The primary disruption in the Circular Polymers Market is the rapid commercialization of advanced chemical recycling technology, such as pyrolysis, depolymerization, purification, and dissolution techniques. Contrary to the traditional mechanical recycling approach, chemical recycling technology makes it possible to recycle virgin-grade polymers from mixed, laminated, and contaminated plastic wastes that would otherwise be disposed of in landfills or for power production. In 2025-2026, the market saw increased investment in chemical recycling plants by the polymer manufacturers and petrochemical firms due to the strict regulations on recycled content. Simultaneously, regulatory developments during 2025-2026, especially those related to the Packaging and Packaging Waste Regulation (PPWR) and the development of Extended Producer Responsibility (EPR), have further hastened the transition from traditional resin manufacture to circular polymers.

Leading polymer companies are incorporating chemical recycling facilities within their petrochemical sites and implementing the ISCC PLUS mass balance approach for large-scale production of recycled food-contact and engineering-grade polymers. Consequently, competition in the polymer industry is now moving from virgin polymer capacity to more advanced recycling facilities, feedstock reliability, and closed-loop material loops.

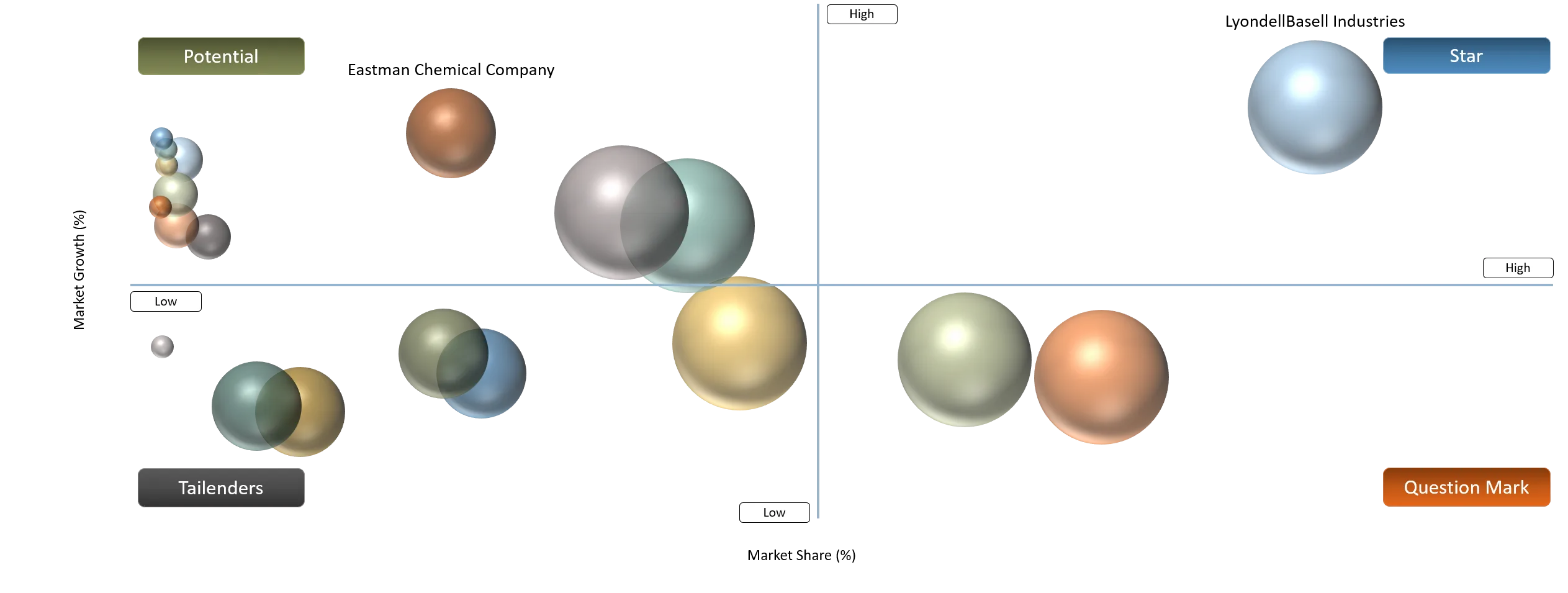

Circular Polymers Market BCG Matrix: Company Evaluation

Stars include LyondellBasell Industries, BASF SE, SABIC, and Borealis AG since they have the most extensive range of circular polymers with the support of high-end mechanical and chemical recycling facilities along with certified circular resin systems. They have included circular polymers in their portfolio of polyolefins and engineering polymers using their own technology platforms like Circulen, ChemCycling, TRUCIRCLE, and Borcycle. Question Marks include Dow Inc., ExxonMobil, INEOS Group, and TotalEnergies since these firms are developing their advanced recycling processes and circular polymer product lines via strategic investments and technologies and new recycling plants. Although these firms have considerable financial strength and integrated petrochemical facilities, their circular polymers division is still growing in relation to the market players.

Potential players include companies such as Eastman Chemical Company, Covestro AG, and Neste Oyj that have demonstrated their technological expertise in areas like molecular recycling, circular feedstocks, and engineering polymers but have an overall narrow range of products in the circular polymers industry. Tailenders include ARKEMA S.A. because its circular polymer applications are mostly found in specialty materials and bio-sourced polymers as compared to bulk polyolefins.

Circular Polymers Market Dynamics

Driver Impact Analysis

| Driver | Market Growth Impact (%) | Demand Concentration | Impacted Use Case | Strategic Impact |

Stringent Regulations are Driving Up Recycled Polymer Content. Governments in Europe, North America, and the Asia-Pacific region have adopted recycling content regulations, EPR programs, and plastic waste regulations requiring incorporation of recycled polymers in packaging and consumer goods. | 38% | Very High | Packaging, Food & Beverage Packaging, Consumer Goods, Automotive | Accelerates adoption of recycled-content polymers, strengthens regulatory compliance, and stimulates investments in closed-loop recycling systems. |

Rapid Commercialization of Advanced Recyclable Technologies such as Pyrolysis, depolymerization, solvent-based purification, and dissolution recycling. | 32% | High | Food-grade Packaging, Automotive, Electrical & Electronics, Engineering Plastics | Expands high-quality recycled polymer supply, enables recycling of difficult plastic waste streams, and reduces dependence on virgin fossil-based polymers. |

Increasing Investments in Circular Polymer Infrastructure by polymer producers, petrochemicals, recyclers, and waste management firms to set up new and efficient recycling centers. | 24% | Medium-High | Recycling Facilities, Waste Management, Polymer Production, Industrial Manufacturing | Improves feedstock availability, expands recycling capacity, strengthens regional supply chains, and enhances commercial-scale circular polymer production. |

Growing demand for Sustainable High-Performance Polymers for recycled and chemically regenerated polymers which provide mechanical performance similar to that of virgin polymers. | 20% | High | Automotive Components, Consumer Electronics, Construction Materials, Consumer Goods | Drives development of engineering-grade recycled polymers, increases demand for premium circular materials, and supports corporate ESG and decarbonization strategies. |

Rapid Commercialization of Advanced Recyclable Technologies such as Pyrolysis, depolymerization, solvent-based purification, and dissolution recycling

The fast commercialization of advanced recycling processes like pyrolysis, depolymerization, solvent purification, and dissolution recycling is increasingly turning out to be the key factor driving growth in the Circular Polymers Market. These recycling techniques facilitate the processing of plastic waste streams that cannot be recycled through traditional mechanical processes by virtue of being mixed, multi-layered, and contaminated and provide higher-purity polymers as an output. In 2025-26, prominent polymer producers like BASF, SABIC, LyondellBasell, Dow, Eastman, and Borealis made huge investments in setting up advanced recycling plants at scale, along with offering certified circular polymers made using chemically recycled feedstock. Parallel to this, over 650 companies, which include global consumer brands, packaging companies, retail chains, and polymer suppliers, are involved with the Ellen MacArthur Foundation's Global Commitment, thus emphasizing the need for circular polymers within global supply chains.

For instance, in September 2025, Matter, a Germany-based chemical recycling firm, announced plans to build a 10,000 tonnes per year chemical depolymerization facility to be constructed at Chemiepark Knapsack that would chemically recycle difficult-to-sort PET packaging and polyester textiles waste to monomers.

Restraint Impact Analysis

| Restraint | Drag on Market Growth (%) | Primary Impact Area | Impacted Use Case | Strategic Impact |

Limited availability of high-quality recycling feedstock, making it insufficient to meet the growing demand for high-quality circular polymers. | 34% | Feedstock Supply & Material Recovery

| Food-grade Packaging, Automotive, Consumer Goods, Electronics | Restricts production of premium recycled polymers, increases raw material costs, intensifies competition for high-quality waste streams, and delays expansion of circular polymer capacity. |

Fluctuations in crude oil and petrochemical feedstock prices directly influence virgin polymer prices. | 28% | Polymer Pricing & Cost Competitiveness | Packaging, Construction, Industrial Manufacturing | Low virgin resin prices reduce the price competitiveness of recycled polymers, affecting adoption rates and slowing investments in circular polymer production. |

Even though recycling processes become more advanced day by day, it is hard to produce recycled polymers with identical properties, purity, coloring, and workability. | 26% | Material Quality & Product Performance

| Food-contact Packaging, Medical Products, Electrical & Electronics, Engineering Plastics | Limits the use of recycled polymers in high-specification applications, requiring additional purification, compounding, and quality assurance processes that increase production costs. |

Underdeveloped Collection and Recycling Infrastructure in Emerging Economies. | 20% | Waste Collection & Recycling Infrastructure | Municipal Recycling, Consumer Packaging, Industrial Plastics | Reduces recovery rates of recyclable plastics, limits feedstock availability, and slows the development of regional circular polymer value chains and recycling ecosystems. |

Limited availability of high-quality recycling feedstock, making it insufficient to meet the growing demand for high-quality circular polymers

One of the primary restraints limiting the growth of the Circular Polymers Market is the limited availability of high-quality recyclable feedstock, which is insufficient to meet the rapidly increasing demand for premium recycled polymers. Inefficient plastic waste stream collection systems, contamination of post-consumer plastic waste, and a lack of adequate sorting systems represent some of the major reasons why there is an insufficient supply of quality feedstock during 2025-2026. According to the OECD Global Plastics Outlook, only 9% of global plastic waste gets recycled, and another 22% is mismanaged, making the amount of plastic suitable for high-value recycling rather small. Moreover, PlasticsEurope (2025) indicates that post-consumer plastic waste collection in Europe was at the level of approximately 29.5 million tonnes, but the proportion of this waste not suitable for high-grade recycled polymers was significant.

For instance, in October 2025, the Bureau of International Recycling (BIR), a Belgium-based international association of the recycling industry, reported that recyclers in Asia and Eastern Europe were having trouble finding high-quality plastic scrap because of contamination, poor recycling systems, and scarcity of feedstock.

Circular Polymers Market Segment Analysis

The global circular polymers market is segmented based on polymer type, circular process, form, end-use, and region.

Mechanical Recycling Maintaining Leadership Through Established Infrastructure and Commercial Scalability

The Mechanical Recycling segment dominated the Circular Polymers Market, holding a global market share of about 63.5% in 2025, due to its advanced processing technologies, low cost of production, and wide use in plastics production chains. The process of sorting, cleaning, grinding, melting, and recycling plastics in order to obtain new recycled plastics is still the preferred method for recycling PE, PP, and PET plastics used in packages, consumer goods, building materials, and automotive sectors. In 2025-2026, growing application of recycled content requirements within the Packaging and Packaging Waste Regulation (PPWR) of the EU and development of Extended Producer Responsibility (EPR) programs contributed to the growth of the market for mechanically recycled polymers.

Further strengthening the leadership of the segment is through constant reinvestment in infrastructure for collection, sorting, and recycling. Based on data from Plastics Recyclers Europe, the capacity of the European plastics recycling industry exceeded 13.2 million tonnes in 2025, while the European Union target for recycling 55% of plastic packaging waste was to be achieved by 2030.

Circular Polymers Market Geographical Penetration

Stringent Circular Economy Regulations and Advanced Recycling Infrastructure Driving Europe's Market Leadership

Europe had the highest dominance in the Circular Polymers Market with an approximate share of 31.22% of the overall market share in 2025, due to its circular economy laws, established recycling processes, and timely development of advanced recycling technology. The region is known to have formed a highly integrated ecosystem of circular polymers owing to stringent regulations such as PPWR, SUPD, and EPR, which have helped accelerate the use of recycled and chemically-regenerated polymers in various sectors, including packaging, automotive, construction, and consumer goods industries. In 2025-2026, Europe made significant investment in mechanical and chemical recycling plants and certified production of circular polymers via collaboration of resin producers, recyclers, and brand owners.

In June 2025, Selenis, a Portugal -based specialty polyester manufacturer, formed a strategic collaboration with Circ®, a U.S.-based textile-to-textile recycler company, towards scaling the manufacturing process of circular polyester in Europe. As part of the deal, Selenis will be processing thousands of metric tons of Circ® Polyester that are made from used textiles to promote textile-to-textile recycling technology.

Germany Circular Polymers Market Trends

Germany held the largest share of the European Circular Polymers Market, occupying a market share of 24.8% in 2025, due to its matured polymer production sector, efficient recycling facilities, and regulations favoring circular plastic products. Germany has been recognized as the country hosting many leading manufacturers of circular polymers such as BASF SE, Covestro AG, and several other mechanical recyclers and chemical recycling technologies developers, forming an ecosystem consisting of waste collection, polymers production, compounding, and marketing. Germany's dominance in this market is fueled by its high demand for recycled polymers from various sectors such as packaging, automotive, construction, and electrical & electronics sectors due to the requirement imposed under Packaging and Packaging Waste Regulation (PPWR) and Extended Producer Responsibility (EPR) of the European Union in 2025-2026.

For instance, in August 2025, LyondellBasell got approval from regulators to start building its Wesseling pyrolysis plant in Germany, a huge step towards commercializing advanced chemical recycling technologies. This plant is built to recycle 50,000 tonnes of mixed plastic waste every year using its innovative MoReTec technology to manufacture pyrolysis oil and gas for manufacturing circular polymers.

Netherlands Circular Polymers Market Outlook

The Netherlands is a rapidly growing country in the European Circular Polymers Market due to its unique geographical position, swift implementation of innovations in the field of recycling, and governmental support for the principles of the circular economy. Currently, the Netherlands has become one of the favorite destinations for investment in the development of chemical recycling, pyrolysis, and production of circular feedstock, which is supported by the activities of the Port of Rotterdam, the biggest chemical-energy integrated complex in Europe. Within 2025–2026, global manufacturers of polymers such as LyondellBasell, SABIC, and Neste were continuing the development of circular polymer production and advanced recycling plants to satisfy the rising demand for certified recycled PE, PP, and other circular polymers in the fields of packaging, automotive industry, and consumer goods. The Netherlands comprised about 11.2% of the European Circular Polymers Market in 2025 and will be experiencing a CAGR of approximately 12.8% in 2026–2035.

For instance, in June 2025, Invest-NL, a Netherlands-based national financial and development agency, joined hands with MYNE, a Netherlands-based innovative plastic recycling company, to enhance the commercialization of chemical plastic recycling. Under the collaboration, MYNE is going to scale up its patented depolymerization technology through the construction of a commercial facility that can recycle up to 20,000 tonnes of plastic waste every year into virgin-grade monomers to produce new circular polymers.

Circular Polymers Market Competitive Landscape

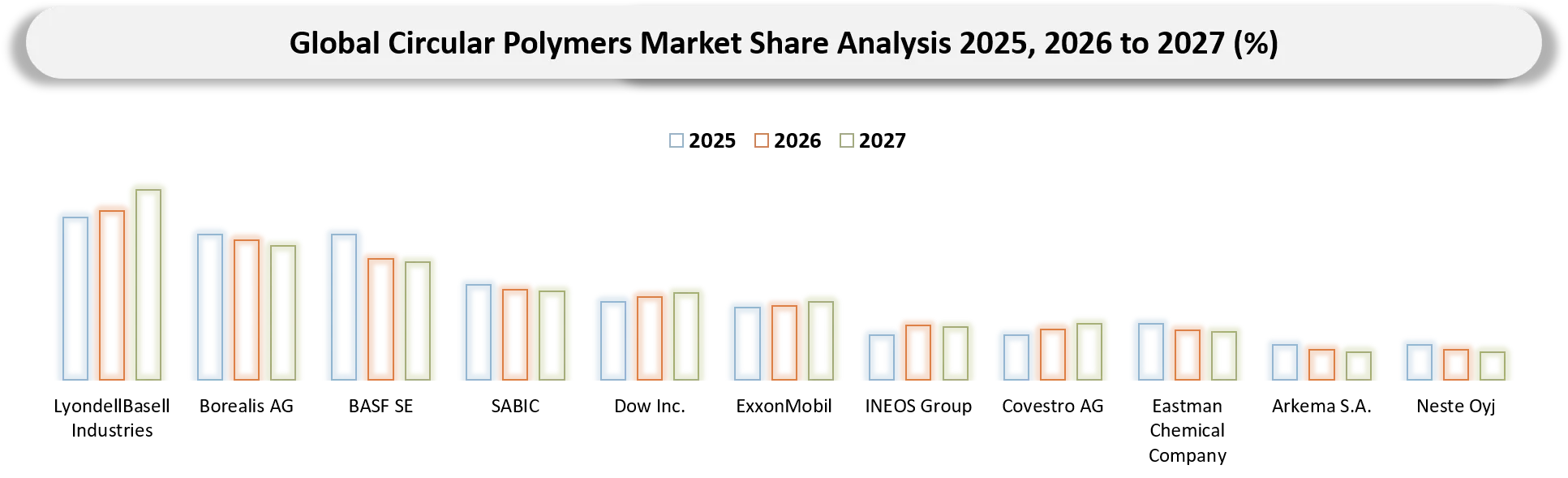

- The market is characterized by three major participant groups: integrated polymer producers, advanced recycling and circular polymer innovators, and renewable feedstock producers. As per the forecast for 2025, the total share of LyondellBasell Industries, BASF SE, SABIC, Dow Inc., ExxonMobil, Borealis AG, and INEOS Group in the global Circular Polymers Market stands between 58 and 62%, owing to their integrated petrochemical plants, extensive resin manufacturing capacity, and substantial investment in mechanical and chemical recycling technologies. Other prominent players in this market include Covestro AG, Eastman Chemical Company, Arkema S.A., and TotalEnergies through their contributions to specialty circular polymers, molecular recycling and bio-attributed engineering plastics; and Neste Oyj through its critical role as a renewable and circular feedstock provider using a mass balance-certified process. The competitive structure in the market is becoming more focused on advanced recycling capacity, availability of quality feedstock, ISCC PLUS certification, partnerships, and vertically integrated circular value chain.

- Key players include LyondellBasell Industries, Borealis AG, BASF SE, SABIC, Dow Inc., ExxonMobil, INEOS Group, Covestro AG, Eastman Chemical Company, Arkema S.A., Neste Oyj, and TotalEnergies.

Key Developments

- In October 2025: ExxonMobil, a U.S.-based corporation dealing in petroleum and chemicals, launched the Signature Polymers range that comprises polyethylene, polypropylene, and elastomers using the revolutionary recycling technology known as Exxtend™.

- In April 2025: BASF, a German-based chemical company, promoted its Ultramid® Ccycled® polyamides made through the process of ChemCycling®, where waste plastic is turned into pyrolysis oil that is utilized to manufacture circular polyamides (PA6/PA66).

- In April 2025: Borealis, an Austria-based chemical firm, and AnQore, a Netherlands-based chemical manufacturing firm, established a collaboration strategy to develop a circular acrylonitrile supply chain through the use of renewable and mass balance feedstock for Econitrile-MB™.

- In September 2025: Ester Industries, an Indian-based specialty polymers manufacturer, and Loop Industries, a Canadian clean technology company, established a joint venture worth ₹1,600 crore in Gujarat for the construction of a massive plant that will use Loop’s depolymerization technology to manufacture recycled polyester (rPET) and circular PET resins.

- In November 2025: Nike, a U.S.-based sports apparel company, partnered with Loop Industries, a Canada-based clean technology company, in support of the use of Twist™ circular polyester resin made through chemically recycled PET.

- In December 2025: Borealis, an Austria-based chemicals company, partnered with BlueAlp, a Netherlands-based advanced recycling technologies company, to expedite the development and deployment of chemical recycling technology (pyrolysis) which uses mixed plastic waste to produce circular feedstock.

Key Procurement Priorities and Buyer Evaluation Criteria

- Circular Polymers Market-oriented businesses are more likely to consider suppliers who can provide them with quality materials through mechanical recycling, chemical recycling such as depolymerization, pyrolysis, and solvolysis, and circular polymer recovery.

- The procurement decision process is significantly affected by the increasing pressure exerted by sustainability regulations, extended producer responsibility models, recycled content requirements, and environmental, social, and governance objectives of corporations, forcing buyers to opt for certified circular polymers with clear sources and carbon reduction impacts.

- Buyers judge suppliers based on the flexibility of their feedstock, capability of contamination management, consistency of polymer performance, scalability of recycling processes, and capacity to provide food-grade or high-performance engineering-grade recycled polymers.

Why Choose DataM?

- Technological Innovations: Covers progress in the development of manufacturing processes for circular polymers, involving chemical recycling (depolymerization, glycolysis, pyrolysis), advanced mechanical recycling, enzymatic recycling, and polymer upcycling methods that enhance material quality, reliability, and replace the use of virgin plastics.

- Product Performance & Market Positioning: Evaluates how market participants differentiate based on recycled content quality, polymer grade consistency (PET, PE, PP, PVC), mechanical strength retention, odor and color removal efficiency, and scalability of production, highlighting how leading players position themselves through high-performance circular polymer solutions aligned with industrial and consumer-grade requirements.

- Real-World Evidence: Highlights adoption of circular polymers in packaging, FMCG products, automotive components, construction materials, and apparel, demonstrating real-world benefits such as reduced carbon footprint, improved resource efficiency, compliance with sustainability targets, and substitution of fossil-based virgin plastics in global supply chains.

- Market Updates & Industry Changes: Tracks key developments such as expansion of chemical recycling capacity, brand-owner commitments to recycled content, regulatory tightening on single-use plastics, EPR implementation across regions, and strategic partnerships between petrochemical companies, recyclers, and consumer brands driving circular economy transformation.

- Competitive Strategies: Analyzes how leading companies expand through vertical integration across collection–sorting–recycling value chains, investments in advanced depolymerization facilities, joint ventures with packaging and FMCG companies, and innovation in feedstock sourcing strategies to secure consistent waste supply and improve output quality.

- Pricing & Market Access: Explains pricing dynamics driven by feedstock availability, recycling technology type, energy intensity, and purification costs, along with market access shaped by long-term supply contracts with brand owners, recycling consortiums, petrochemical players, and sustainability-linked procurement frameworks.

- Market Entry & Expansion: Identifies growth opportunities driven by increasing global demand for sustainable materials, regulatory mandates for recycled content, corporate net-zero commitments, and rising adoption across packaging, automotive, and textile industries, while outlining strategies such as regional recycling infrastructure development, technology licensing, and circular ecosystem partnerships to scale globally.

Target Audience

- Plastic & Polymer Manufacturers

- Packaging Industry Players

- Chemical & Petrochemical Companies

- Recycling & Waste Management Companies

- Automotive & Transportation OEMs

- Textile & Apparel Brands

- Consumer Goods & Retail Companies