Certified-Circular Polyethylene Market Definition and Overview

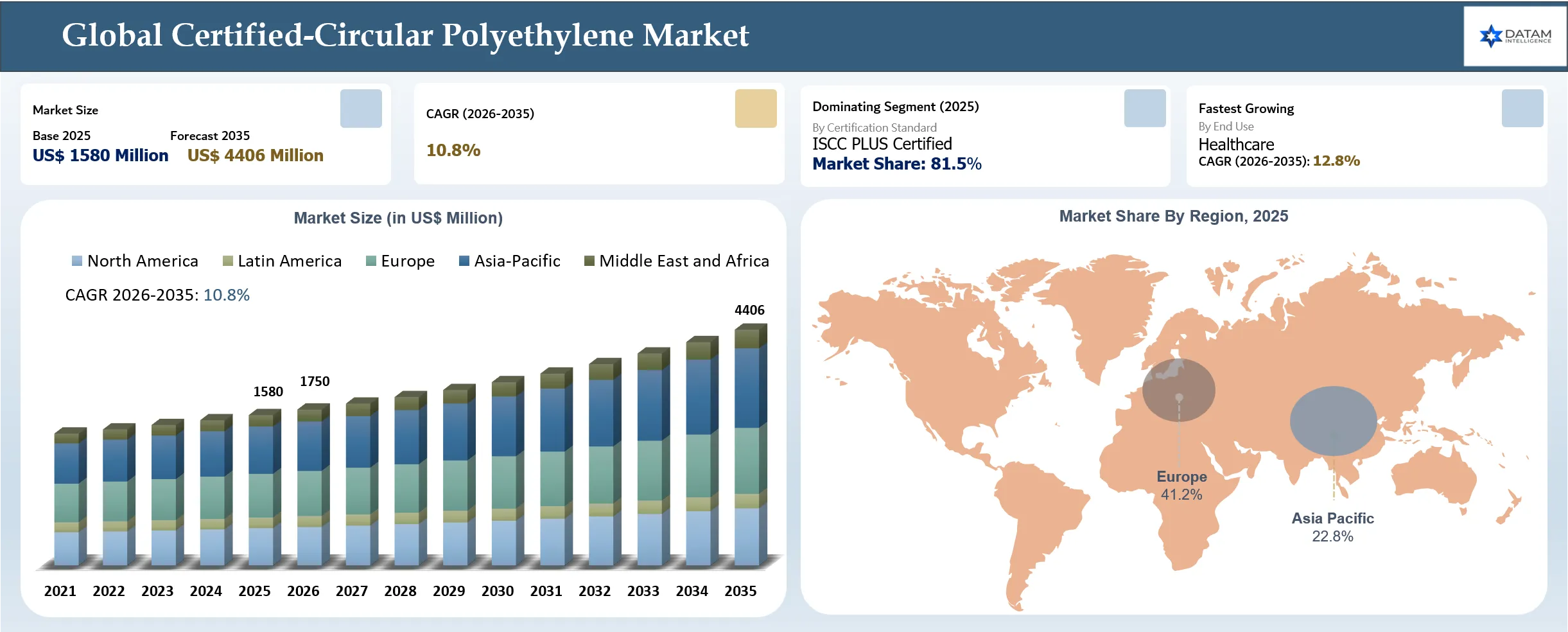

The global Certified-Circular Polyethylene market reached USD 1,580 million in 2025 and is expected to reach USD 4,406 million by 2035, growing with a CAGR of 10.8% during the forecast period 2026-2035, due to the use of mass balance systems, allowing producers to use recyclable feedstock, yet retaining its virgin grade performance. In 2025, ISCC PLUS reached 6,000 valid certifications around the world, with more than 24 million metric tonnes of ISCC PLUS materials being processed throughout the last certification period across 86 countries. This highlights the rapid commercial adoption of circular plastics, which have been certified and traceable recycled polymers becoming increasingly common worldwide. Among such large companies as ExxonMobil, SABIC, Borealis, LyondellBasell, Dow, and Shell Chemicals are continually increasing the production capacity for their advanced recycling processes and ISCC PLUS-certified polyethylene due to increased demand in packaging, consumer goods, healthcare, and industry sectors. However, the main problems include the lack of suitable feedstock for the process, investments in chemical recycling technologies, and difficulties in obtaining the ISCC PLUS certificate.

In September 2025, Shell Polymers and Charter Next Generation (CNG) entered into a commercial collaboration to provide ISCC PLUS-certified circular polyethylene for flexible packaging films that offer high performance. The ISCC PLUS-certified circular PE is manufactured through the use of the mass balance method and pyrolysis oil made from recycled plastic waste, making it possible to have the performance of virgin-grade resin as well as diverting plastic waste to meet the objectives of the circular economy. The raw materials will be supplied at CNG's ISCC PLUS-certified manufacturing plants for use in applications such as pet food packaging, meat packaging, and healthcare packaging. CNG has 18 manufacturing plants in the US with over 2,600 employee-owners, and Shell has a plant in Monaca, Pennsylvania, serving over 70% of the North American polyethylene market.

Certified-Circular Polyethylene Market Key Takeaways

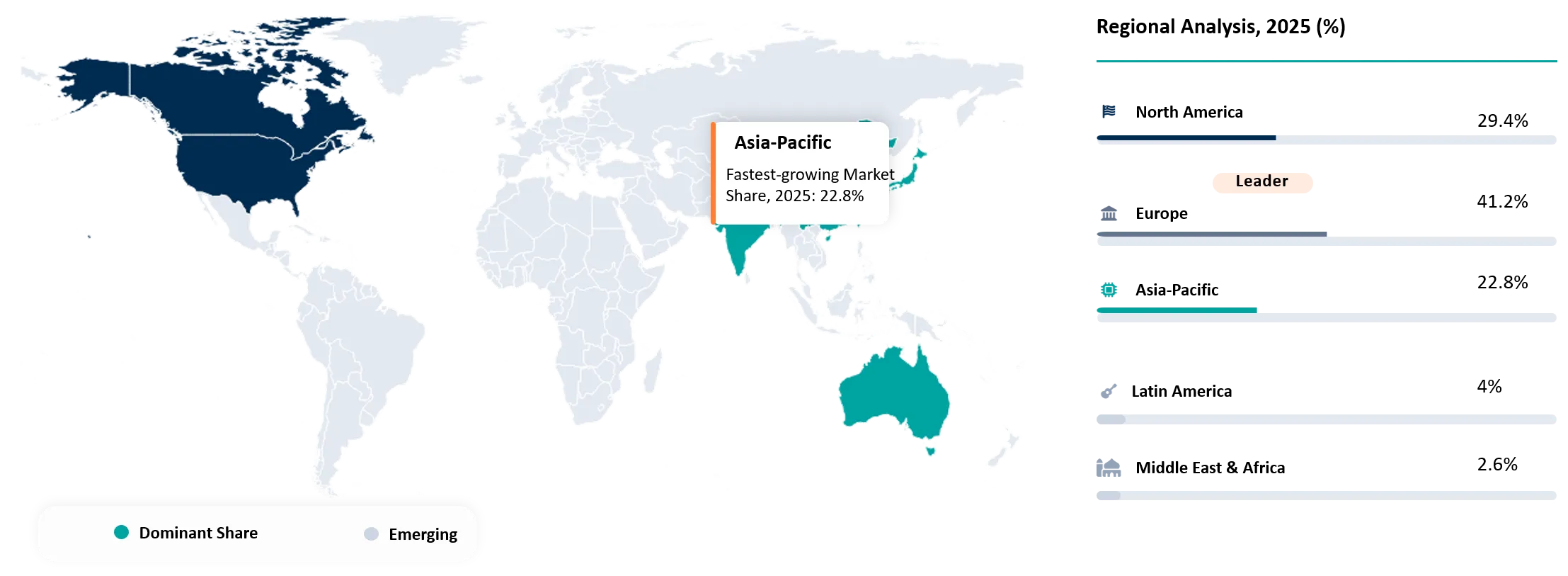

- The Europe region dominated the certified-circular polyethylene market with a market share of 41.2% in 2025. The dominant position in the market is due to the existence of stringent environmental policies such as the EU Circular Economy Action Plan and PPWR.

- The ISCC PLUS Certified segment had an overwhelming dominance in the market, accounting for 81.5% market share in 2025. The dominant market share is attributed to the acceptance of the chain of custody and mass balance practices worldwide.

- In 2025, the total number of ISCC PLUS-certified projects around the world amounted to 6,000, with 86 countries involved. Over 24 million tonnes of material were processed under the ISCC PLUS certification system during this period.

- The UK government made a statement saying that the use of mass balance for chemically recycled plastic is to be introduced by April 1, 2027. This regulation makes it possible to exempt an important tax on all plastic packaging with 30% or more recycled plastic content.

Certified-Circular Polyethylene Market Industry Trends and Strategic Insight

- Certified-circular polyethylene has adopted the mass balance approach as its main commercialization strategy, allowing the petrochemical companies to utilize chemically recycled feedstock through their existing steam crackers without compromising the quality standards of virgin polyethylene.

- Recycling capabilities have become an increasingly important competitive advantage. Some major producers are stepping up their investments in the areas of pyrolysis oil manufacturing, feedstock preparation, and recycling chemical plants to ensure supply of circular feedstock.

- Flexible packaging is increasingly becoming the high-value application segment owing to the virgin-grade mechanical properties that certified-circular polyethylene offers while meeting recycled-content goals for food-contact and consumer packaging.

- Production centers in regions are growing due to investments that rely on certification. Europe is still the leader in terms of the market since it has tough rules regarding the circular economy, whereas North America and Asia-Pacific are experiencing a quick rise in production centers for ISCC PLUS-certified materials instead of building polymer plants.

- Diversification of the portfolio in terms of certified-circular polymers enhances market positioning. Leading manufacturers are moving beyond polyethylene by incorporating certified-circular polypropylene, specialty polyolefins, and engineering plastics in a common portfolio of circular products.

Certified-Circular Polyethylene Market Scope

| Metrics | Details | |

| 2025 Market Size | USD 1,580 million | |

| 2035 Projected Market Size | USD 4,406 million | |

| CAGR (2026-2035) | 10.8% | |

| Largest Market | Europe | |

| Fastest Growing Market | Asia-Pacific | |

| By Product Type | High-Density Polyethylene (HDPE), Low-Density Polyethylene (LDPE), Linear Low-Density Polyethylene (LLDPE), Others | |

| By Certification Standard | ISCC PLUS Certified, REDcert² Certified, Others | |

| By Feedstock Source | Post-Consumer Plastic Waste (PCR), Post-Industrial Plastic Waste (PIR), Others | |

| By End-Use | Packaging, Consumer Goods, Healthcare, Food & Beverage, Construction, Automotive, Agriculture, Industrial Manufacturing, Others | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Türkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

Certified-Circular Polyethylene Market Disruption Analysis

Rapid Commercialization of Advanced Chemical Recycling Technologies Reshaping the Certified-Circular Polyethylene Value Chain

Disruption in the Certified-Circular Polyethylene Market is the rapid development of the chemical recycling process, mainly the pyrolysis process, which is making it possible to convert mixed and hard-to-recycle plastic waste into circular feedstocks to manufacture virgin-like polyethylene. The technology innovation disrupts the traditional polyethylene value chain by making it possible to replace the feedstock that was traditionally derived from fossil fuels with chemically recycled pyrolysis oil without modifying the polymer production infrastructure. Commercial deployment intensified during 2025-2026 amid the expansion of circular polymer platforms by prominent resins suppliers at an industrial scale. Thus, in 2025, Borealis raised its circular manufacturing capacity by 18% to 227,900 metric tons, whereas circular feedstock processing volumes almost doubled to 221,200 metric tons, illustrating the quick growth of circular polyolefin manufacturing.

Moreover, SABIC recorded a total output of 55.5 million metric tons of polymers in 2025, further developing its TRUCIRCLE™ range with lifecycle assessments highlighting that certified circular polymers produced via advanced recycling technology cut down around 2 kg of CO₂ emissions per kilogram of polymer manufactured and reduce fossil material depletion by about 80-84% in comparison to standard fossil-based manufacturing processes. The trends are transforming the competitive environment by making advanced recycling capabilities, certified circular feedstock, and verified carbon reduction among strategic advantages for polyethylene producers.

Certified-Circular Polyethylene Market BCG Matrix: Company Evaluation

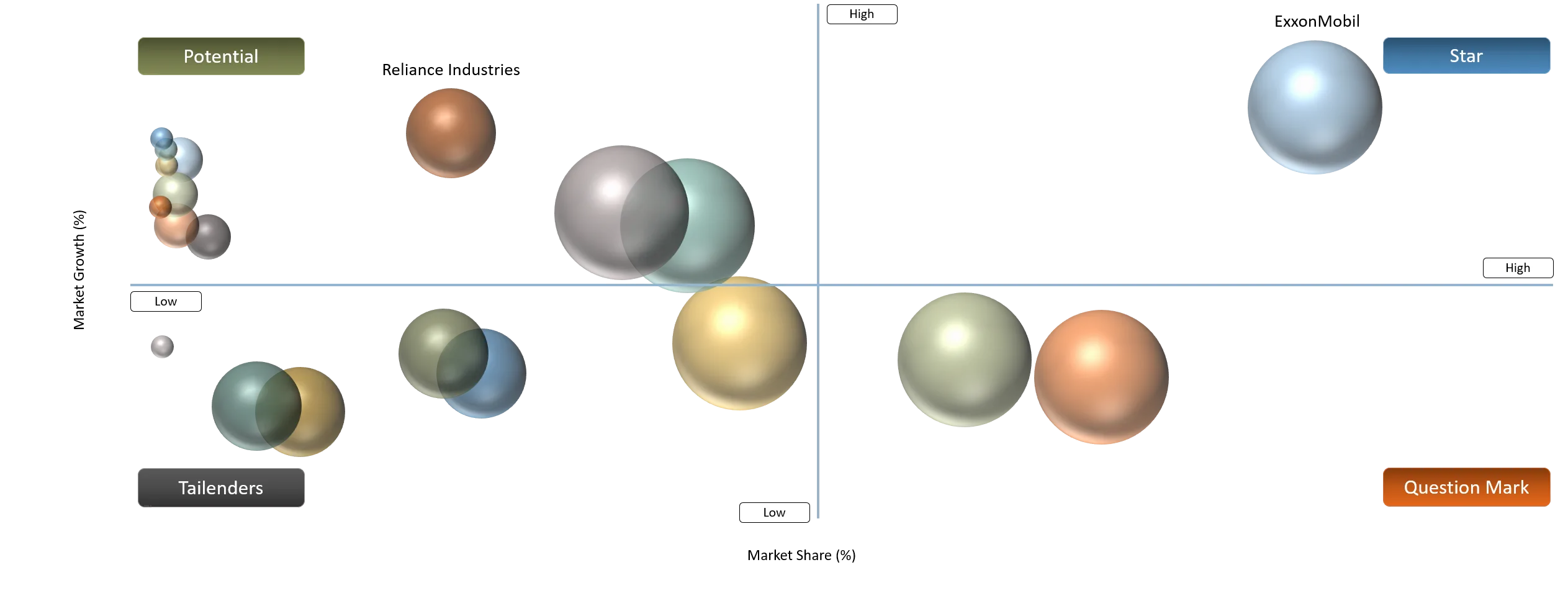

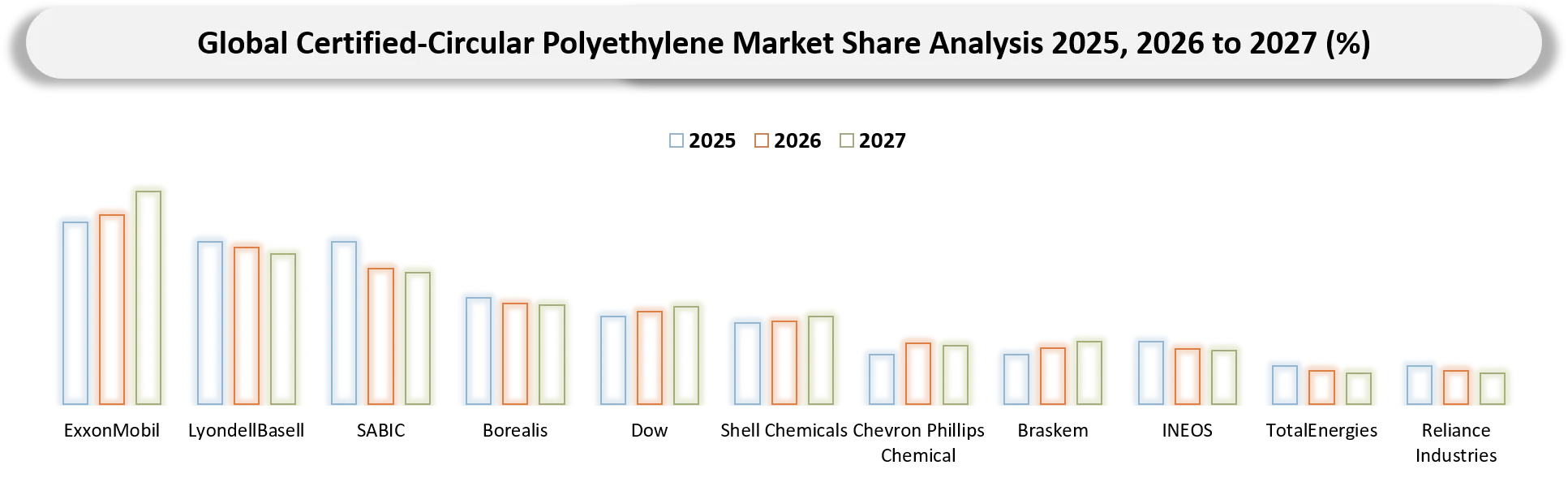

Stars consist of ExxonMobil, SABIC, LyondellBasell, Borealis, and Dow since they hold the biggest commercial footprint in terms of certified circular polyethylene with regard to major investments in advanced recycling technology, broad ISCC PLUS certified polymer offerings, and vertical integration in their petrochemical processes. These firms have built long-standing relationships with advanced recyclers as well as major consumer brands around the globe that can provide them with certified circular polyethylene on a commercial scale. Question Marks are Shell Chemicals, Chevron Phillips Chemical, Braskem, INEOS, and TotalEnergies because they are actively working on the certification of circular polyethylene products via advanced recycling and mass balance certification initiatives, but they still lag behind the dominant players in terms of production and product range.

Potential category includes Reliance Industries, MOL Group, Formosa Plastics Corporation, and LG Chem. These firms are reinforcing themselves through the use of ISCC PLUS certification in production, regional circular polymers programs, and sustainable petrochemical manufacturing. Tailenders include Mitsui Chemicals, which is relatively underrepresented in the certified circular polyethylene market since its engagement revolves around regional sustainability programs and circular polymer projects.

Certified-Circular Polyethylene Market Dynamics

Driver Impact Analysis

| Driver | Market Growth Impact (%) | Demand Concentration | Impacted Use Case | Strategic Impact |

Increasing Adoption of Mass Balance-Certified Circular Polymers such as ISCC PLUS and REDcert² is accelerating demand for certified-circular polyethylene. | 32% | Very High | Food-contact packaging, flexible films, rigid containers, personal care packaging | Accelerates commercialization of certified-circular PE, strengthens traceable recycled-content supply chains, and supports compliance with recycled-content regulations. |

Expansion of Advanced Chemical Recycling Infrastructure is increasing the availability of chemically recycled feedstocks suitable for producing certified-circular polyethylene. | 28% | High | Circular PE resin production, packaging films, industrial molded products | Expands circular feedstock availability, improves supply security, and enables large-scale production of virgin-quality certified-circular polyethylene. |

Growing Sustainability Commitments from Global Brand Owners are incorporating certified-circular polyethylene into product portfolios to achieve corporate recycled-content targets. | 24% | High | Flexible packaging, e-commerce mailers, household product packaging | Drives long-term procurement contracts, increases demand for certified materials, and encourages investment in circular polymer portfolios. |

Rising Demand for Virgin-Quality Recycled Polyethylene making it suitable for demanding applications such as food-contact packaging, healthcare packaging, and personal care products. | 18% | Moderate-High | Medical packaging, food-contact films, bottles, caps & closures | Expands certified-circular PE into high-value applications where mechanically recycled plastics have limited acceptance due to quality requirements. |

Increasing Investments by Integrated Petrochemical Producers are expanding ISCC PLUS-certified polyethylene production. | 14% | Moderate | Certified PE resins, packaging compounds, industrial components | Strengthens production capacity, supports global commercialization, and enhances competitive differentiation through integrated circular polymer platforms. |

Increasing Adoption of Mass Balance-Certified Circular Polymers such as ISCC PLUS and REDcert² is accelerating demand for certified-circular polyethylene

The rising adoption of mass-balance-based circular polymers is driving the growth of the certified-circular polyethylene market, given that certification schemes such as ISCC PLUS and REDcert² allow chemically recycled feedstocks to be split across polyethylene manufacturing facilities while ensuring full traceability and virgin-equivalent properties of the material. With this kind of certification, packaging manufacturers and brand owners can utilize recycled materials in food contact and medical applications without any modifications to the production process, and therefore, certified-circular polyethylene is one of the fastest-commercializing circular polyolefins. Tetra Pak became the first food and beverage packaging company in India to introduce packaging containing 5% ISCC PLUS-certified recycled polymers in 2025, aligning with India's mandatory recycled-content requirements that came into effect on 1 April 2025. In parallel, the ISCC Impact Report 2025 showed that polyethylene, polypropylene, and pyrolysis oil were among the most certified outgoing products under the Processing Unit scope, highlighting the rapid integration of certified circular polyolefins into industrial production.

In addition to this, in November 2025, the UK Government (HM Revenue & Customs) announced that, from 1 April 2027, it will introduce a mass balance approach for chemically recycled plastics under the Plastic Packaging Tax, enabling manufacturers to claim tax exemption when plastic packaging contains 30% or more recycled plastic.

Restraint Impact Analysis

| Restraint | Drag on Market Growth (%) | Primary Impact Area | Impacted Use Case | Strategic Impact |

Limited availability of high-quality plastic waste feedstock for advanced chemical recycling remains insufficient compared to growing demand. | 30% | Feedstock Procurement & Advanced Recycling Supply Chain | Certified-circular PE resin production, food-contact packaging, healthcare packaging | Restricts commercial production capacity, increases feedstock procurement costs, and delays expansion of certified-circular polyethylene supply. |

Premium Pricing Compared with Virgin Polyethylene due to feedstock collection, sorting, advanced recycling, reducing adoption in price-sensitive applications. | 24% | Production Economics & Pricing Competitiveness | Flexible packaging, consumer goods, industrial packaging | Reduces adoption in cost-sensitive markets and limits substitution of virgin polyethylene where sustainability premiums are difficult to justify. |

Complexity of Mass Balance Certification and Chain-of-Custody Compliance such as ISCC PLUS and REDcert² requires rigorous auditing, documentation, and supply-chain traceability, increasing operational complexity and administrative costs. | 19% | Certification & Regulatory Compliance | Food-contact packaging, healthcare products, export packaging | Increases compliance costs, extends certification timelines, and creates barriers for small and mid-sized resin producers entering the certified-circular market. |

Competition from Mechanically Recycled Polyethylene often offers a lower-cost alternative, limiting the adoption of certified-circular polyethylene. | 16% | Market Adoption & Product Positioning | Non-food packaging, construction products, industrial components | Encourages end users to select mechanically recycled PE in applications where virgin-equivalent performance and certification are not essential, reducing demand for certified-circular grades. |

Limited availability of high-quality plastic waste feedstock for advanced chemical recycling remains insufficient compared to growing demand

One of the major restraints limiting the growth of the Certified-Circular Polyethylene Market is the insufficient availability of high-quality plastic waste feedstock required for advanced chemical recycling. Certified-circular polyethylene is produced from post-consumer and post-industrial plastic wastes that meet high-quality standards to convert them into pyrolysis oil for the manufacturing of polymers. But the lack of proper waste collection facilities and poor sorting systems have made it difficult to collect the right raw materials. According to the OECD Global Plastics Outlook, only 9% of global plastic waste is recycled, while 19% is incinerated, 50% is landfilled, and 22% is mismanaged, leaving only a limited fraction of plastic waste available for high-quality recycling pathways. Furthermore, according to Eurostat's Packaging Waste Statistics (published 2025), the European Union generated 16.4 million tonnes of plastic packaging waste in 2022, yet only 6.7 million tonnes were recycled, corresponding to a recycling rate of 40.7%.

Further in June 2026, Nature published a report which is done by Researchers at Ghent University showing that even though sorting after mixing of plastic waste helps to make more feedstock available for recycling, at the same time, it adds more contaminants like cadmium, lead, halogens, water, and dirt, making less high-quality feedstock available for advanced chemical recycling. It has been found in the paper that the production of plastic all around the world in 2024 was more than 413.8 million tons, out of which only 9% was recycled.

Certified-Circular Polyethylene Market Segment Analysis

The global certified-circular polyethylene market is segmented based on product type, certification standard, feedstock source, end-use, and region.

ISCC PLUS Certified Segment Dominates the Certification Standard Due to Widespread Industry Acceptance and Global Supply Chain Integration

The ISCC PLUS Certified segment dominated the Certified-Circular Polyethylene Market, with about 81.5% of the market share in 2025, owing to the prevalent use of this certification throughout the entire petrochemical and plastics supply chain worldwide. It can be said that the ISCC PLUS Certification has been adopted as the ideal certification standard for certified-circular polyethylene due to the mass-balance calculation, chain-of-custody verification, and traceability of the chemical recycling of the raw materials from waste collection to the polymer manufacturing process. This is largely due to the acceptance of the certification among resin manufacturers, packaging converters, and multinationals, thus enabling certified-circular polyethylene in various high-end applications including food-grade, medical, personal care, and consumer goods packaging.

During 2025, Borealis Compounds Inc. obtained ISCC PLUS certification for its North American operations, enabling the commercial production of certified circular polyolefins for wire & cable, consumer, and industrial applications. In the same year, Shell Chemicals and Charter Next Generation commercialized ISCC PLUS-certified circular linear low-density polyethylene (LLDPE) for flexible packaging applications, while Tetra Pak introduced packaging in India containing 5% ISCC PLUS-certified recycled polymers to support compliance with the country's recycled-content regulations that came into effect in 2025.

Certified-Circular Polyethylene Market Geographical Penetration

Strong Regulatory Framework and Commercial Scale-Up of Circular Polyolefins Position Europe as the Leading Regional Market

The Europe region held a dominant position in the Certified-Circular Polyethylene Market with an estimated 41.2% market share in 2025. Europe is led by strict circular economy policies, a highly developed mass balance system for certification, and the early commercialization of chemical recycling technology. Various policies such as the PPWR and the Single-Use Plastics Directive in Europe have encouraged the usage of certified-circular polyethylene through their policies of recycled content in plastics. The other reason why Europe leads in this market is that there are some leading petrochemical companies such as Borealis, SABIC, INEOS, TotalEnergies, LyondellBasell, and Shell Chemicals, which have increased the production of certified-circular polyethylene in Europe. Furthermore, Eurostat reported in 2025 that the European Union generated 16.4 million tonnes of plastic packaging waste, with 6.7 million tonnes recycled, highlighting both the substantial feedstock base available for circular polymer production and the significant opportunity to increase advanced recycling utilization.

Further, in September 2025, MOL Group, a Hungary-based integrated oil, gas, and petrochemicals company, completed its first ISCC PLUS-certified production trial using post-consumer plastic waste-based circular feedstock at its Tiszaújváros petrochemical complex. The initiative supports MOL's SHAPE TOMORROW strategy, which targets processing up to 1.5 million tonnes of alternative feedstock annually by 2030, strengthening the availability of certified-circular polyethylene across Central and Eastern Europe.

Germany Certified-Circular Polyethylene Market Trends

Germany holds a dominant position in the European Certified-Circular Polyethylene Market owing to its highly developed petrochemical industry and advanced investments in chemical recycling, coupled with its early entry into producing circular polymers based on the ISCC PLUS certificate. Germany is home to some production and innovation hubs of such companies as LyondellBasell, BASF, INEOS, and SABIC that allow a smooth transition to incorporating chemically recycled feedstocks in the process of production of traditional polyethylene. Germany also enjoys favorable policy support from the EU Circular Economy Action Plan and PPWR. In addition, Eurostat reported in 2025 that Germany generated approximately 5.6 million tonnes of packaging waste for recycling in 2022, the highest volume among EU Member States, providing a substantial resource base for circular plastics processing.

Further, in October 2025, Agilyx ASA, a Norway-based advanced recycling technology company, acquired a 44% stake in GreenDot Global, a Germany-based circular plastic recycling platform, through a €52 million investment to strengthen the supply chain for advanced recycling feedstock in Europe. GreenDot processes more than 1 million tonnes of packaging waste annually, including over 400,000 tonnes of plastic waste, and the partnership aims to expand plastic waste collection, sorting, and recycling infrastructure across Germany, Austria, and Italy.

Netherlands Certified-Circular Polyethylene Market Outlook

Netherlands is the fastest-growing country in the European Certified-Circular Polyethylene Market owing to its favorable geographical location, excellent port facilities, and fast-paced growth in terms of advanced recycling and circular polymers' manufacturing. The Netherlands enjoys the advantage of having chemical plants such as the Shell Moerdijk chemical plant, which makes it possible to use chemically recycled feedstock in manufacturing polyethylene through a mass balance approach. Moreover, the Netherlands acts as a major gateway for circular plastics in Europe in terms of logistics with the help of the Port of Rotterdam, where recycled feedstock, pyrolysis oil, and circular polymers are moved between the producers and converters.

Further, in August 2025, LyondellBasell, a Netherlands-headquartered global chemical manufacturer, received regulatory approval to begin construction of its MoReTec advanced recycling plant in Wesseling, Germany. The commercial-scale facility will process 50,000 tonnes of post-consumer plastic waste annually into pyrolysis oil for the production of ISCC PLUS-certified circular polyolefins, including polyethylene, using a mass balance approach. Backed by €40 million from the EU Innovation Fund, the project is expected to commence operations in 2026, strengthening Germany's capacity for certified-circular polyethylene and advancing Europe's circular plastics economy.

Certified-Circular Polyethylene Market Competitive Landscape

- The market is characterized by three key categories of participants, including integrated petrochemicals and polymers producers, providers of circular polymer technologies, and regional producers of polyethylene products venturing into sustainable offerings. Prominent firms like ExxonMobil, Dow, LyondellBasell, SABIC, Borealis, and TotalEnergies have a major presence in the world of certified-circular polyethylene with high polyethylene manufacturing capacities, chemical recycling, mass-balance feedstocks incorporation, and association with international packaging brands. Collectively, these firms represent a significant share of the certified circular polymers supply base, with SABIC, ExxonMobil, and Borealis expected to be some of the key players, while major petrochemical companies hold a sizeable market share owing to their integrated operations and recycling capabilities.

- Key players include ExxonMobil, LyondellBasell, SABIC, Borealis, Dow, Shell Chemicals, Chevron Phillips Chemical, Braskem, INEOS, TotalEnergies, Reliance Industries, MOL Group, Formosa Plastics Corporation, LG Chem, and Mitsui Chemicals.

Key Developments

- September 2025: Shell Polymers and Charter Next Generation (CNG), a U.S.-based specialty film manufacturer, entered into a commercial collaboration to supply ISCC PLUS-certified circular polyethylene for high-performance flexible packaging applications. The partnership uses a mass balance approach, where pyrolysis oil produced from recycled plastic waste is used as circular feedstock to manufacture virgin-quality polyethylene resin.

- February 2026: Borealis, Borouge, Pelita Mekar Semesta (PMS), Reciki Solusi Indonesia, and the Subnational Climate Fund partnered to establish an integrated circular waste management ecosystem in Indonesia to increase the recovery and recycling of post-consumer plastic waste.

- January 2026: Prysmian, an Italy-based cable manufacturer, and Versalis (Eni’s chemical company) partnered to chemically recycle plastic cable scrap containing cross-linked polyethylene (XLPE) using Versalis’ Hoop® advanced recycling technology.

- December 2025: Circulate Capital, a Singapore-based impact investment firm focused on circular economy solutions, invested in See Hau Global, a Malaysia-based plastic recycling company, to expand regional recycling capacity and strengthen the supply of recycled polyolefin materials.

- April 2026: Circular Plastics Australia (CPA) achieved SCS Global Recycled Content Certification for its rFresh-100 resin, a 100% post-consumer recycled high-density polyethylene (rHDPE) material produced from recovered plastic packaging waste.

Key Procurement Priorities and Buyer Evaluation Criteria

- Organizations procuring certified-circular polyethylene are increasingly selecting suppliers based on their ability to provide high-quality recycled-content polyethylene solutions with verified sustainability credentials, consistent material performance, and scalability for large-volume applications across packaging, consumer goods, automotive, and industrial sectors.

- The procurement decision-making process is being influenced by the growing demand for sustainable packaging, corporate carbon reduction targets, extended producer responsibility (EPR) regulations, and brand-owner commitments toward recycled and circular plastic adoption. Buyers are increasingly prioritizing suppliers with certified circular production pathways, reliable recycled feedstock availability, and compliance with global sustainability standards.

- Buyers evaluate factors such as ISCC PLUS certification, recycled content traceability, mechanical performance, contamination control, product consistency, processing compatibility, and ability to maintain virgin-like polyethylene properties when selecting certified-circular polyethylene suppliers for applications such as flexible packaging, rigid containers, films, and consumer products.

Why Choose DataM?

- Sustainability Innovations: Investigates technological innovations within certified circular polyethylene technologies that include chemical recycling, feedstocks created through the pyrolysis process, mass balance techniques, and ISCC Plus certification of production processes. Such innovations allow businesses to minimize their reliance on virgin polymers and cut greenhouse gas emissions.

- Product Performance and Market Positioning: Assesses the ability of key players in polyethylene manufacturing to differentiate their certified circular products in terms of recycled content quality, performance, compliance with food contact, processability, greenhouse gas reduction capabilities, and scalability.

- Real World Evidence: Emphasizes the use of circular-certified polyethylene-based solutions by global companies in applications like packaging, personal care products, food packaging, films, and automobile parts, highlighting some of its advantages, including reducing plastic waste, sustainability, regulatory compliance, and achieving corporate recycling goals.

- Market News & Industry Developments: Monitors major events including expansion of advanced recycling plants, introduction of circular polymer products, collaboration among petrochemical and branding organizations, certification progress, and regulatory modifications in Europe, North America, and Asia-Pacific regions that aid in the formation of circular plastic value chains.

- Competitive Strategies: Evaluates how major firms such as ExxonMobil, SABIC, Dow, LyondellBasell, Borealis, TotalEnergies, Braskem, and INEOS improve their market power by means of investments in chemical recycling, recycling technology development, capacity increases, sustainability collaboration, and incorporation of circular feedstock into current polyethylene manufacturing systems.

- Price and Market Access: Outlines the rationale behind different pricing structures depending on the source of recycled feedstock, certifications, type of recycling technology used, volume of production, and premium on sustainability, as well as market access through petrochemical companies, polymer distributors, converters, and packaging chains.

- Market Entry & Growth: Determines areas of expansion due to increasing demand for eco-friendly packaging, recycling efforts against plastic waste, compliance with laws and regulations, and brands' commitment towards using recycled materials in their products, by formulating strategies like building regional recycling capacity, certification, technological collaborations, and circular supply chain management.

Target Audience

- Polyethylene Manufacturers & Petrochemical Companies

- Chemical Recycling & Advanced Recycling Technology Providers

- Packaging Manufacturers & Converters

- Consumer Goods & Brand Owners

- Automotive & Industrial Material Users

- Recycling Companies & Waste Management Organizations

- Chemical & Material Distributors