Ceramics Market Overview

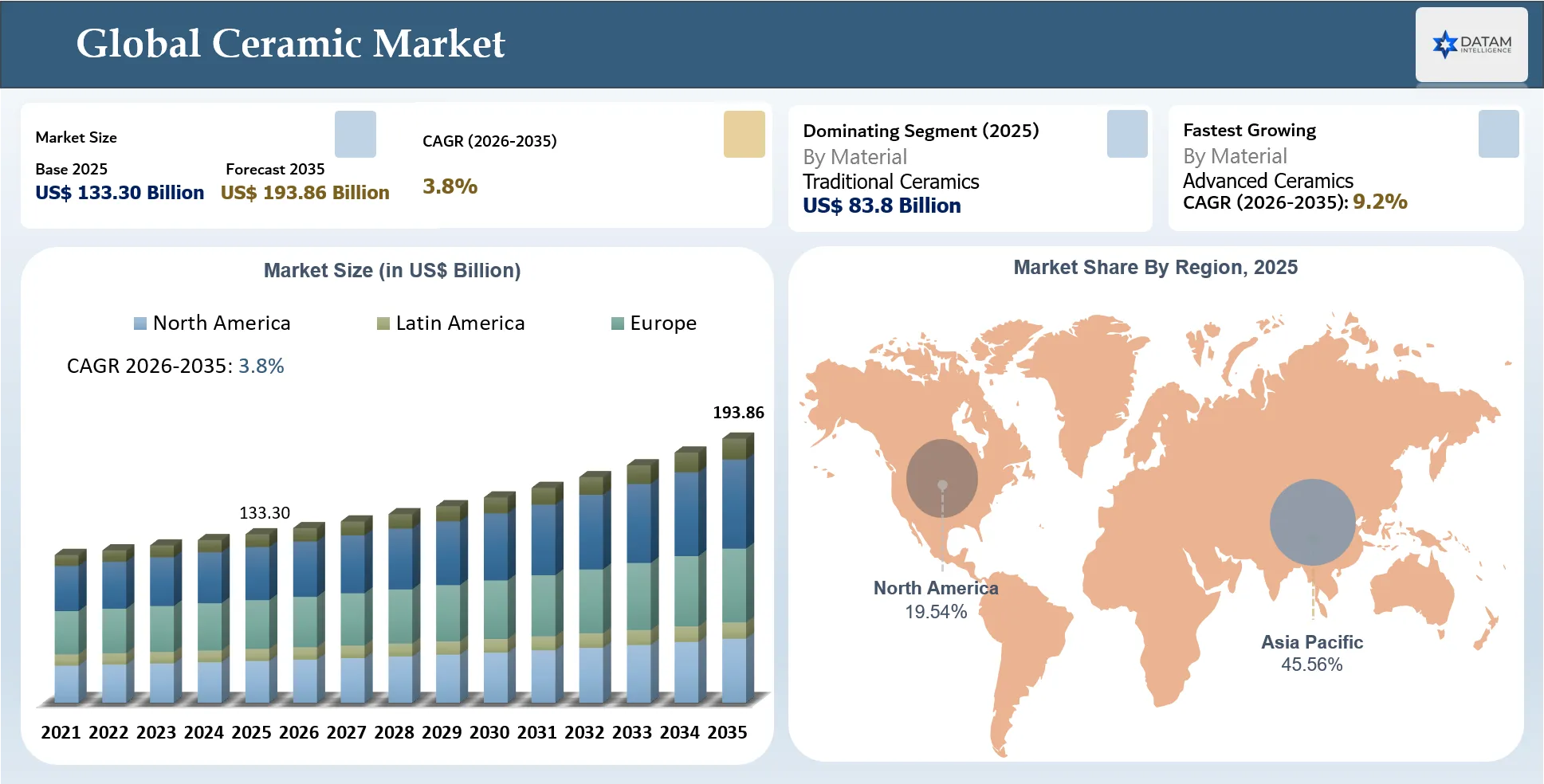

The global ceramic market reached US$ 133.30 Billion in 2025 and is expected to reach US$ 193.86 Billion by 2035, growing at a CAGR of 3.8% during 2026 to 2035 due to rising penetration of ceramic materials in the construction, industrial processing, electronics, transportation, healthcare and energy. Due to the inherent properties such as high mechanical strength, high thermal stability, high corrosion resistance, electrical insulation and long life through several applications, the demand for ceramic materials is increasing among both traditional and technology-based applications. Availability of the high demand are observed for various ceramic applications such as tiles, sanitary ware, refractories, electronic components, medical implants, aerospace parts and industrial wear resistant components, in both developing and developed economies.

The construction sector is the largest consumer of ceramic materials across the globe, where high demand for ceramics in the form of floor and wall tiles, sanitary ware, pipes and decorative building materials is fuelled by increasing need for residential, commercial and public development, due to massive urbanization coupled with investments in infrastructure. Apart from the construction applications, the steel, cement, mining and chemical segments rely on refractory linings and abrasive wear resistant ceramic components under high temperature and processing conditions. Along with investment in renovation and remodelling on the trend of in-house interior design and renovation, there is a market demand for premium quality and durable ceramic applications.

Recently, advanced ceramics have emerged as one of the fastest growing markets with the support of continuous technological innovations and a wide range of applications such as semiconductors, electric vehicles, renewable energy systems, medical applications, aerospace and precision engineering. The superior electrical, thermal and mechanical performance of Ceramic products make them suitable replacements for conventional materials in many key applications. The growth and convergence of advanced ceramic technologies with automation drives, digital manufacturing, additive manufacturing, AI-enabled process optimization and energy efficient production technologies are improving product performance, operational efficiency, environmental friendliness and applicability.

Key Takeaways

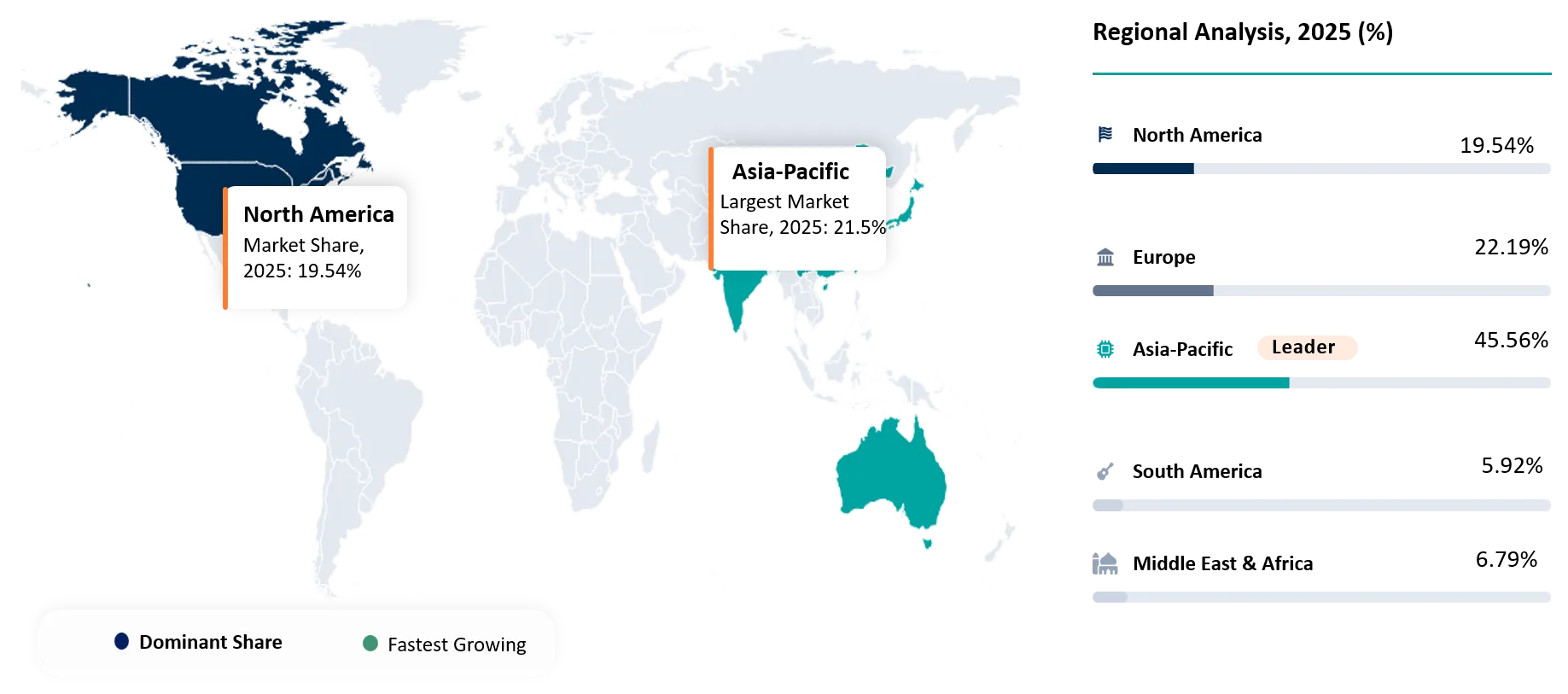

- Asia-Pacific captured 45.56% share of the global ceramic market in 2025 due to rapid urbanization, large-scale construction projects, manufacturing strengths and ever-increasing demand from electronic devices, automobiles and other industries in countries such as China, Japan, India and South Korea.

- With vast production capabilities, a massive domestic consumption base, rampant construction and robust exports, China led the worldwide ceramic market in 2025, due to significant investment in high-end ceramics for usage in consumer electronics, electric vehicle technologies, machinery and equipment, as well as renewable energy technologies, further cemented its global leading role.

- In 2025, Construction & infrastructure dominated the market in terms of revenue, backed by growing requirement for decorative building materials, tiles and pipes in various building and infrastructure development projects.

- Advanced Ceramics is anticipated to register the fastest growth rate, as the products are experiencing demand in various applications such as medical, renewable energy, EVs, semiconductors, defence and aerospace, industrial automation etc.

- Ceramics tiles led the overall product category in 2025 with significant revenue shares due to increasing construction and renovation projects and increasing demand from the premium interior designing sector in various developed and developing countries.

- Both sustainability practices and digital manufacturing are the leading aspects of differentiating businesses in terms of increased manufacturing efficiency as well as the reduction of carbon footprints. It can be seen as the firms increasingly focus on implementing digital technology in terms of designing, artificial intelligence, automatization, digital printing, in low carbon technologies.

- The competitive differentiation is moving in terms of product innovations, enhanced manufacturing capability, global distribution, sustainable practices and quality in terms of ensuring premium brand perception globally for the players of Ceramics Industry.

Ceramics Market Scope

| Metrics | Details | |

| 2025 Market Size | US$ 133.30 Billion | |

| 2035 Projected Market Size | US$ 193.86 Billion | |

| CAGR (2026-2035) | 3.8% | |

| Largest Market | Asia-Pacific, 45.56% Share in 2025 | |

| Fastest Growing Market | Asia-Pacific | |

| Dominating Sales Channel | Medical and Healthcare | |

| By Product Grade | Medical Grade COC, Optical Grade COC, Packaging Grade COC, Electronics Grade COC, General Purpose COC | |

| By Processing Method | Injection Molding, Extrusion, Blow Molding, Thermoforming, Film Casting, Others | |

| By Application | Medical and Healthcare, Packaging, Optics, Electronics, Others | |

| By End-User | Pharmaceutical, Medical Device, Diagnostics, Packaging, Optical Component, Electronics, Research Laboratories, Others | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| South America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

Why This Report Matters in 2026

Entering 2026, the global ceramics industry faces unprecedented growth on the back of accelerated technological advancements, stringent sustainability guidelines and increased demand from both conventional and hi-tech sector. Unlike before, construction businesses, manufacturing units and high-tech sectors are prioritizing the strength, reliability, consistency, eco-friendliness of ceramic products more than the price. Increased usage of ceramic materials for electric vehicles, electronic gadgets, medicines, space exploration as well as renewable energy sector requires companies producing ceramics to combine the need to meet production requirements with that of adopting innovation and keeping in sync with the environmental norms and regulations. Companies that can offer high performance together with the ability to accommodate varying market needs would dominate this segment.

Advanced ceramics consumption is growing in sectors such as electric vehicles, semiconductor, clean energy, healthcare and aerospace, owing to government support towards smarter cities. Also, it increased the investment in infrastructure and housing projects in urban areas further fuelling growth. Growing demand is pushing manufacturers to increase investments in technologies such as digital manufacturing, automated production, energy efficiency and AI, for boosting output and to contain harmful environmental emissions.

Strategic Indicators for Ceramics

High Regulation Impact

European and North American regulations and standards enforce strict compliance with environmental (relevant to industrial emissions to ambient air and liquids), energy, product quality and safety standards for ceramic processes and services. Product and equipment design requirements for various sectors such as healthcare, aerospace, communications, defense and electronics require rigorous testing, material traceability and certifications to meet product industry and international standards. Ongoing tightening of sustainability regulations increases the need for funding investments in environmental technologies and cleaner and safer operational processes to comply with regulations and achieve operational excellence.

High Investment Activity

Investment in the world's ceramics industry trend continues to increase as drivers such as capital spending by manufacturers is increasing in improving production capacity as well as developing new manufacturing technologies. In addition to expanding production capacity, manufacturers are investing in automation, artificial intelligence (AI) based inspection systems, digital printing technologies and efficient energy consumption kiln technologies to improve manufacturing capabilities, product quality and operational efficiency. Global infrastructure development and increasing urbanization in emerging economies are also driving establishment of new plants and facilities for sanitary ware, construction materials and ceramic tiles.

Supply Chain Disruption

Supply chain disruptions have become a critical issue for the ceramics industry. Raw materials such as clay, feldspar, silica, alumina, mica, calcite, quartz and zircon have significant supply risks in terms of access and transportation. Rising logistics costs, weather, geopolitical issues and increasing fuel prices have directly impacted the industry. Supply chain will be an issue to ceramics manufacturers when they need to increase their global supply. Diversity in sourcing strategies and forward contracts with suppliers can be highly effective in overcoming the short supply of raw materials.

Pricing Volatility

Price structure in the ceramics industry is affected by changes in the cost of raw materials, electricity and fuel, labor, transportation and processing complexity. Energy is one of the major inputs because production process requires firing materials high temperatures. The cost of premium ceramics and engineered ceramic components is higher because of the use of advanced raw materials, high-precision processing and stringent quality standards. Therefore, many companies are focusing on process optimization, increased value and streamlined processes to preserve profitability while maintaining competitiveness.

Procurement Pressure

The concept of procurement is becoming more sophisticated due to value of quality, performance and continuity of supply and compliance with the relevant legislation. The factors play an increasingly decisive role for purchasing decisions in many sectors, particularly in electronics-based applications in healthcare, aerospace and industrial engineering. In these industries, material failures may have significant financial and operational impacts. The significance of developing long-term supplier relationships is been able to meet requirements for material quality and continuity of supply, technical support and price assurance.

New Technology Adoption

Innovative technologies are revolutionizing the ceramics industry, including artificial intelligence, robots, Industrial Internet of Things (IIoT), additive manufacturing, automation, digital printing. The technologies have the potential to ‘optimize operational processes, increase production efficiency, reduce costs, improve maintenance and quality control and reduce material wastage.’ Digital printing technologies are transforming ceramic surfaces to create more specific and expensive aesthetic finishes. Additive manufacturing is being utilized to produce more complex products used in the aerospace and medical industries. The effect of digital transformation on the ceramics industry is significant and there is increasing evidence that leading ceramic manufacturers will have a strategic advantage in this disruptive era.

Import-Export and Pricing Intelligence

Existing robust international supply chains bolster the global ceramics trade. Exports remain dominated by nations that have substantial manufacturing capabilities and favourable production economics. Export and import trends vary in accordance with ceramics tiles, sanitary wares, refractories, high performance ceramics and engineering ceramic products. Asia-Pacific continue to be the principal regions for production as well as exports. The most prominent elements dictating the rates is the availability of raw material, energy, wages of labour, freight and transportation costs, manufacturing techniques and quality of ceramics product. However, advanced ceramics and engineering ceramics will attract higher costs compared to its lower value peers.

| Reporter | Trade Flow | 2025 Trade Value | Interpretation |

| Japan | Export | USD 3.5 Billion | Japan is a leading exporter of advanced ceramic materials and technical ceramic components used in semiconductor manufacturing, automotive systems, electronics, healthcare and precision industrial applications. |

| Germany | Import | USD 3.2 Billion | Germany's imports are supported by demand from construction, automotive, industrial manufacturing and healthcare sectors, with a strong preference for premium ceramic products and high-performance ceramic components. |

| U.S. | Import | USD 6.87 Billion | The U.S. is one of the largest ceramic importing countries, reflecting strong demand for ceramic tiles, sanitary ware, technical ceramics and specialty ceramic products across construction, healthcare, electronics and industrial sectors. |

| China | Export | USD 24-25 Billion | China remains the world's largest ceramic exporter by value, supported by extensive manufacturing capacity and exports of ceramic tiles, sanitary ware, refractories, tableware and advanced ceramics to Asia, Europe, the Middle East, Africa and North America. |

| Germany | Import | USD 3.2 Billion | Germany's imports are supported by demand from construction, automotive, industrial manufacturing and healthcare sectors, with a strong preference for premium ceramic products and high-performance ceramic components. |

Key Procurement Priorities and Buyer Evaluation Criteria

- The most important features of products that the construction and infrastructure buyers look for are their longevity, design uniformity, slip resistance, certification compliance, competitive costs and their schedule of deliveries.

- Industrial users prioritize thermal resistance, abrasion resistance, resistance to a multitude of chemicals, aggressive media, precise dimensional tolerance and durability.

- Manufacturers of Electronics, HealthCare, Space and Aerospace expect to be served with advanced, engineered ceramic items offering top-notch material hardness, mechanical properties, excellent thermal and electrical insulation standards, high geometric precision.

- Distributors and retailers prioritize a broad product portfolio, ready stock availability, competitive pricing, strong brand recognition, and reliable customer service to enhance customer satisfaction.

- Suppliers contribute by assuring reliable product quality and service, offering customer technical support, adopting sustainable manufacturing processes, demonstrating consistent on-time delivery, maintaining global presence to deliver products, and proactively continuing to innovate products and enhance quality of services.

AI Impact Analysis

Artificial Intelligence (AI) is revolutionizing the ceramics industry worldwide by improving efficiency in production, improving quality control and decision making. Production of ceramic products require temperature, pressure, firing cycle and composition control. Predictive analytics and machine learning enables companies to optimize these factors during production to improve efficiency of production, minimize wastage and reduce cost of production. With adoption of advanced manufacturing techniques in ceramic manufacturing, AI is becoming part of ceramic production process.

AI is also transforming quality assurance through computer vision and automated defect detection. Other than the production process, AI is used in prediction of demand, supply chain optimization and inventory management, which is done by analysing sales history, demand patterns of customers and availability of raw materials.

AI has further hastened the pace of innovation in the ceramics sector. The use of artificial intelligence has enabled firms to enhance the formulation of material compositions, simulate product performance and reduce time in developing products for applications in electronics, electric vehicles, aerospace, medical care and renewable energy sectors. With the emergence of more technologies in Industry 4.0, artificial intelligence is predicted to become a major competitive advantage for ceramics firms.

Ceramics Industry Disruption Analysis

In the world of ceramics market, there is a structural change that occurred due to technological advancements, sustainability demands and changes in the requirements of end-use industries. One of the disruptions is usage of advanced ceramic products as the substitute for metals and polymers in electronics, electric cars, aviation, healthcare and renewable energy sectors. It is creating additional growth opportunities for companies that manufacture advanced materials.

Another disruption is a move towards sustainable and digital manufacturing. High prices of energy resources, tightening environmental regulations and carbon reduction objectives lead to a greater need for energy-efficient kilns, recycling of raw materials, renewable energy resources and cleaner production process. Meanwhile, digital technologies such as Artificial Intelligence (AI), automation, Industrial Internet of Things (IIoT), robotics and digital printing make the manufacturing process more efficient, accurate, customized and cost-effective.

Reallocation of the global supply chain is another disruptive trend. Price fluctuations of raw materials, energy, shipping and geopolitical instability is due to diversified sourcing strategies, regional manufacturing and increased supply chain resilience. Manufacturing companies that implement advanced manufacturing technologies, sustainable manufacturing methods and resilient procurement strategies are likely to become competitive players in the future.

BCG Matrix: Company Evaluation

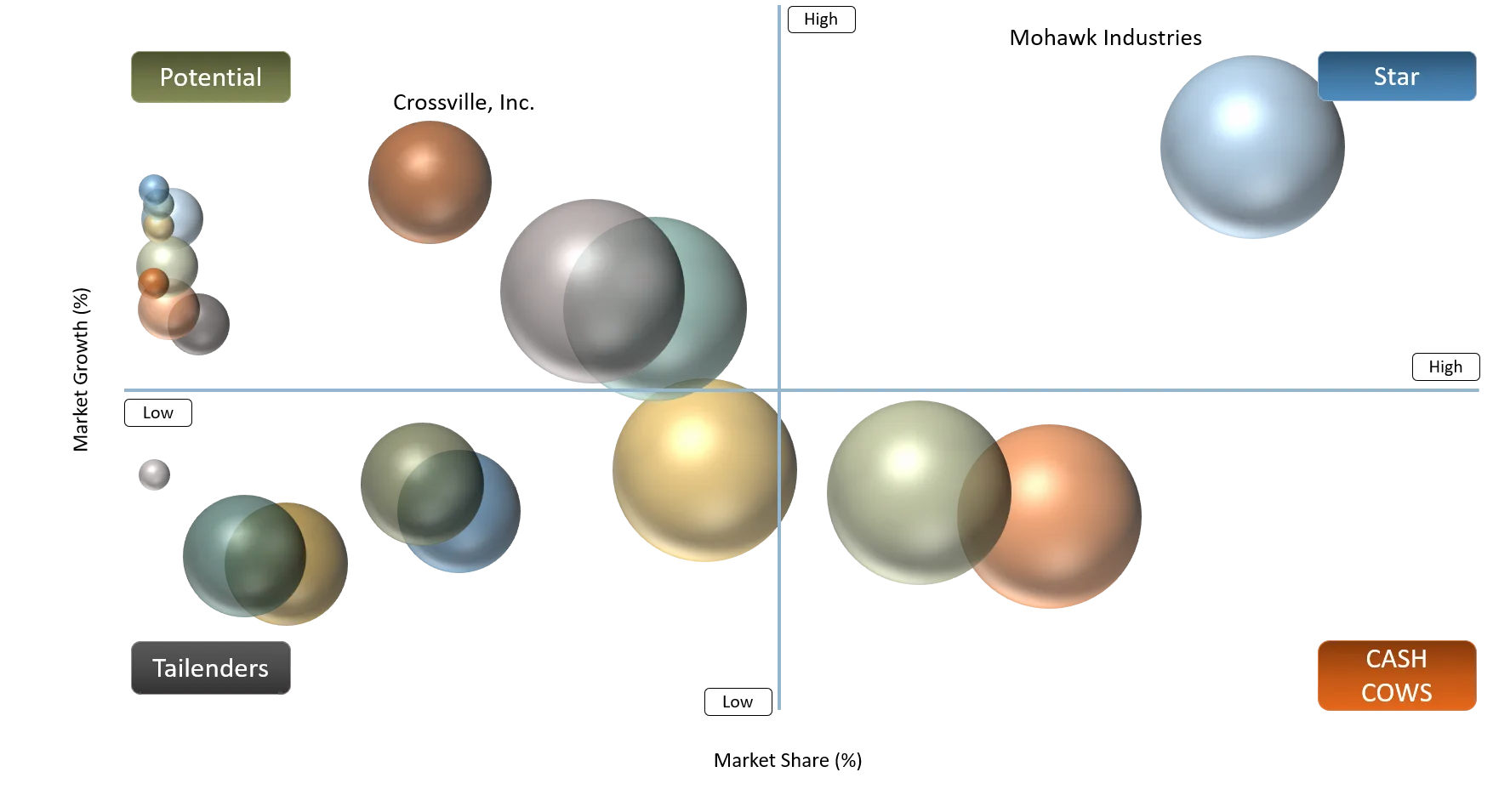

STAR

Star players are Mohawk Industries, SCG Ceramics, RAK Ceramics, Kajaria Ceramics and Grupo Lamosa as these companies are well-positioned players in the global ceramic tiles and sanitary ware market. The players have broad product portfolios, strong global distribution networks and brand recognition that will help them to benefit from increasing demand in the residential construction, commercial and infrastructure and renovation segment. They are also expanding their business into advanced ceramics along with other high-value product categories to maximize their growth opportunities.

POTENTIAL

Potential players are advanced ceramic manufacturers, specialty ceramic component manufacturers, 3D ceramic printing companies, medical ceramic manufacturers, precision engineering companies that are focused on high-performance ceramic applications. Although these players do not have the scale of major global ceramic manufacturers, they are well positioned to take advantage of the increasing advanced ceramics market opportunities in electronics, electric vehicles, aerospace, healthcare, semiconductors and renewable energy applications. These players are investing in R&D, cutting edge manufacturing technology and emerging industrial applications for advanced ceramics to expedite their growth.

Ceramics Market Dynamics

Driver Impact Analysis

| Driver | Market Growth Impact | Demand Concentration | Impacted Use Case | Strategic Impact |

Construction and infrastructure development continues to drive ceramic demand | High | Asia-Pacific, Middle East, North America | Ceramic tiles, sanitary ware, pipes and building materials | Supports capacity expansion and long-term revenue growth |

Rising adoption of advanced ceramics across high-tech industries | High | U.S., Japan, China, Germany and South Korea | Electronics, EVs, aerospace, medical devices and semiconductors | Accelerates investment in high-value ceramic solutions |

Increasing preference for sustainable and premium ceramic products | Medium to High | Europe, North America and Asia-Pacific | Energy-efficient buildings, luxury interiors and green construction | Strengthens innovation and premium product positioning |

Technological advancements in ceramic manufacturing | Medium | Global | Digital printing, automation and 3D-printed ceramics | Improves production efficiency and product differentiation |

Driver: Construction and Infrastructure Development Continues to Create the Strongest Demand Pull

As the largest demand generator for the global ceramics market, the construction and infrastructure industry benefits from the growing investment in housing and developments such as smart towns, highways, airports, highways and metro development. Moreover, due to increased urbanization and the surge in the construction of public buildings and infrastructures, the consumption of ceramic tiles, sanitaryware, pipes and decorative building accessories has also increased rapidly.

Moreover, since paint and decorative elements are used in most commercial and residential construction and renovation projects, growing renovations and remodelling are also seen as another major contributing factor for the growth of the market. Furthermore, demand for ceramic building and decorative products has increased significantly due to increasing construction activities such as hotel, hospital, shopping malls, residential, educational building, transport, office building and many other commercial and infrastructure projects worldwide.

Restraint Impact Analysis

| Restraint | Drag On Market Growth | Primary Impact Area | Impacted Use Case | Strategic Impact |

High energy consumption and volatile fuel prices increase production costs | High | Europe, Asia-Pacific and North America | Ceramic tiles, sanitary ware, refractories and industrial ceramics | Reduces profit margins and accelerates investment in energy-efficient technologies |

Fluctuating raw material prices and supply chain disruptions | High | Global | Construction materials, advanced ceramics and industrial components | Increases procurement costs and encourages supplier diversification |

Stringent environmental regulations and emission standards | Medium to High | Europe, North America and China | Energy-intensive ceramic manufacturing facilities | Drives investment in sustainable production processes and regulatory compliance |

Competition from alternative materials in selected applications | Medium | Global | Construction products and industrial components | Encourages product innovation and value-added ceramic solutions |

Restraint: High Energy Consumption Continues to be the Most Significant Market Constraint

One of the major market restraints for the global ceramics market is high energy consumption. Ceramic production process involves firing products at high temperatures, which makes the industry dependent on the natural gas and electricity. Fluctuation in the price of energy increases the cost of operations, reduces profit margins and resulting in substantial production costs, especially in regions where energy prices are high.

The impact of energy cost is most significant for manufacturers of ceramic tiles, sanitary ware, refractories and industrial ceramics, where energy costs impact production costs. One of the drivers of cost pressure for the industry is increasing cost of fuels and carbon content associated with product components. Therefore, to increase efficiency, manufacturers are investing in energy efficient kilns, waste heat recovery systems, renewable energy, automation of processes. Companies that can achieve significant reduction in energy consumption while maintaining product quality are expected to strengthen the competitive position and impact the long-term profitability of the ceramics market.

Ceramics Market Segmentation Analysis

Ceramics Market By Application

Building Surfaces and Fixtures Will Continue to Lead Market Value Creation

Building surfaces and fixtures are projected to remain the biggest application sector within the global ceramic industry on account of their vast consumption in applications such as flooring, wall cladding, roofing tiles, bathroom fixtures, kitchen surfaces and decorative architectural elements. In 2025, the sector held the maximum share in the global ceramic market size and it is expected to retain its dominance by 2035 owing to rapid industrialization, increasing urbanisation, growth in housing construction, expanding commercial infrastructure and augmenting renovation initiatives. Ceramic materials have gained prevalence due to their durability, resistance to chemicals, fire, water and their low maintenance and prolonged lifecycle, coupled with wide aesthetic options. The demand for ceramic construction materials has further been supported by numerous government initiatives, which include substantial investment in affordable housing projects, urban smart cities development, public transport, schools and hospital infrastructures along with office buildings and commercial structures.

In the building segments, both residential and commercial space developers and users are more inclined towards high-value ceramic offerings with better designs, durability and sustainability. Various innovations are underway in ceramic products to cater the changing market demand from large format, light-weight, digitized printing technology and energy-efficient products. The manufacturing practices are being focused on increasing the efficiency and product differentiation with minimum wastage and environmental impact in mind.

Ceramics Market By Product

Ceramic Tiles and Slabs

The ceramics tiles and slabs is considered to be the largest product segment for the industry, owing to its immense applications in residential buildings, commercial spaces and industries. The segment has witnessed significant traction across the construction, renovation, high-end interior design trends and the investments in sectors like hospitality, healthcare and education, etc. The technological advancement in the digital printing techniques and modern glazing procedures the tiles and allow ceramic tiles and slabs to replicate the appearance of natural stone, wood, metal, and fabric with high-definition designs, enhancing their aesthetic appeal.

The buying preference by residential buyers and interior designers largely depend on the durable, slip-resistance, stain-resistance and dimensionally consistent properties of ceramics over other natural materials such as marble or granite. Availability in variety of finishes, sizes, textures and price points makes this product extremely useful in residential as well as in commercial & institutional buildings. Automation, digital technology, enhanced glazing are expected to improve their performance and offer variety of designs, surface textures, thereby strengthening market positions.

Ceramics Market By Material

Traditional Ceramics

The traditional ceramics is accounted to hold the largest share under material segment for the ceramics industry and it comprises of ceramic tiles and sanitary ware, tableware, bricks and roof tiles, etc. Traditional ceramics possess great qualities with optimal usage and manufacturing costs. The materials have found wide application as they balance performance, manufacturing price and efficiency to serve both residential and industrial applications.

The usage of traditional ceramics is closely correlated with the new construction activities, increasing consumer income levels and public infrastructure investment in both developing and mature economies. Traditional ceramics manufacturers are improving manufacturing process through optimization of raw material utilization and increasing efficient methods to achieve cost-effectiveness. The segment contributes for a large share of the total global ceramics revenue and it is projected to maintain its position by 2035.

Geographical Penetration

U.S. Ceramics Market Outlook

Increasing demand for ceramics in various sectors such as residential renovations, commercial constructions, aerospace, healthcare, electronics and semiconductors is driving the U.S. ceramics market. The rise in investments in advanced manufacturing technologies and infrastructural development will ensure continuous adoption of ceramic material applications in both traditional as well as advanced ceramics. Consumers have become interested in buying high-end ceramic floorings, sanitary wares and other decorative ceramic goods because of their durability and long-lasting performance. Advanced ceramics are also gaining acceptance in medical devices, semiconductor equipment, aerospace components and electric vehicle technologies due to the unique features offered by them.

Technological advancements are another distinguishing factor in the U.S. ceramics market. Manufacturers are adopting new technologies such as automation, digital manufacturing, additive manufacturing and AI-based quality assurance systems. Companies are also working on sustainability and energy-efficient manufacturing techniques owing to the increasing regulatory compliance requirements. Companies that can supply high-end ceramic materials without compromising the quality of products and technical assistance are likely to gain a competitive edge in the coming years.

China Ceramics Market Landscape

China will remain the largest manufacturer and consumer of ceramic goods owing to its rapid urbanization, infrastructure construction and large-scale manufacturing operations. The country's demand for ceramic tiles, sanitary ware, refractory goods and construction ceramics is likely to continue being driven by growing requirements from residential housing, commercial building, transport infrastructure and industries. China is also one of the major sources of advanced ceramics used in electronics, semiconductors, electric cars, renewable energy and industrial machinery.

Support for smart manufacturing, industrial upgrading and value-based manufacturing from the government is likely to result in more investments in advanced ceramic technology and energy-efficient plants. More automation and digital printing along with sustainable manufacturing are likely to be witnessed in China's manufacturing companies in an effort to increase product quality and competitiveness in export markets.

India Ceramics Market Overview

India is among the fastest-growing ceramics markets due to the increasing trends of urbanization, development of infrastructure and investment in residential and commercial constructions. The government policies such as Smart Cities Mission and Housing for All and infrastructure programs have been contributing to the growing demand for ceramic tiles, sanitary ware, pipes and other building materials. Higher incomes of consumers along with the tendency of using high-end interior items will continue to contribute to the market growth.

At the same time, India has become an important manufacturer and exporter of ceramics because of low-cost production, sufficient supply of raw materials and consistent investments in production capacity. The adoption of digital printing, automation and energy efficiency will continue to increase the quality of products and the number of export destinations.

Japan Ceramic Market Dynamics

Japan occupies a dominant place in the international ceramics sector owing to its advancements in advanced ceramics materials and precision technology. The key drivers of demand include the use of high-performance and highly reliable ceramics in electronics, automotive, semiconductor, healthcare, aerospace and industrial equipment sectors. Japanese players will be emphasizing innovation in materials, manufacturing processes and product development for specific applications.

R&D activities continue to play an important role in sustaining the competitive edge of Japan owing to its focus on the development of next generation ceramic materials for semiconductor fabrication, healthcare renewable energy and electric vehicles. Automation and smart manufacturing technologies are extensively used to enhance the efficiency of manufacturing and ensure quality. Although there is not much scope for growth in the demand for traditional ceramics, its expertise in advanced ceramics is likely to help it retain its relevance in the international market.

Competitive Landscape

- The competitive ceramicist approach is mostly among global companies and specialized advanced ceramic manufacturers instead of local markets. For large-scale, high-quality, technology-driven manufacturing and R&D based manufacturing, dynamic competition is prevalent among leading companies.

- Key players include Mohawk Industries, RAK, Kajaria Ceramics, Grupo Lamosa, SCG leading the competition in ceramic tiles, sanitary ware, building materials while specialized manufacturers focus on advanced ceramics for electronics, automotive, aerospace, healthcare and industrial applications.

- Three major aspects for ceramic buyers in construction and industrial industries include non-price elements such as durability, quality, technical performance, design, price, delivery schedule and after-sales service as their main purchasing criteria. For special applications product consistency, certifications of quality and conformity, supply reliability are mandatory.

- Buyers of construction and industrial products consider variables such as product portfolio, customization capabilities, digital printing technology, energy efficient manufacturing and green sustainability certifications rather than price alone when comparing suppliers.

- Competitive benchmarking includes production capacity, presence in geographic regions, diversification of product portfolio, R&D capability, level of manufacturing technology, sustainability efforts, quality of products, delivery reliability and strength of distribution network.

List of Companies

- Mohawk Industries, Inc.

- RAK Ceramics PJSC

- Kajaria Ceramics Limited

- SCG Ceramics Public Company Limited

- Grupo Lamosa, S.A.B. de C.V.

- Kyocera Corporation

- CoorsTek, Inc.

- CeramTec GmbH

- Morgan Advanced Materials plc

- Saint-Gobain Ceramics

- Murata Manufacturing Co., Ltd.

- NGK Insulators, Ltd.

- Corning Incorporated

- Imerys S.A.

- Vesuvius plc

- Carborundum Universal Limited (CUMI)

- Somany Ceramics Limited

- Crossville, Inc.

- Florida Tile, Inc.

- Porcelanosa Grupo

Company Coverage Preview

The global ceramic market contains various multinational manufacturers, as well as smaller regional manufacturers, together with those that supply traditional and cutting-edge ceramic technology applications. Product quality, the extent of manufacturing capability, advancements in technology, eco-friendly initiatives, channels of distribution, along with pricing points constitute competitive key factors. Important manufacturers keep putting resources in terms of expanding production, automation, automated manufacturing in addition to producing energy-efficient facilities which could potentially increase their competency to make money against increasing demand coming from construction, electronics, healthcare, motor vehicle production, aerospace along with different business-related industry sectors.

The leading global players like Mohawk Industries, RAK Ceramics, Kajaria Ceramics, SCG Ceramics, Kyocera Corporation, Grupo Lamosa, Crossville Inc and so forth have built a solid market presence by diversified products, wider production facilities, global distributions with focus on producing and launching innovative & sustainable ceramic products, strengthening the foothold across the various regions, operational streamlining through modern techniques and technology.

The advanced ceramics sector where companies such as Kyocera Corporation, CoorsTek Inc., CeramTec GmbH, Morgan Advanced Materials and Saint-Gobain Ceramics are fortifying market presence through a high-level of R&D and the development of specialized high-performance ceramic material used in applications which includes semiconductor, health-tech, aviation and defence. The key manufacturers are consistently pouring their funds into R&D to improve products and to develop enhanced next-generation ceramic technology in order to lead the market in a sustained long run.

Major Pain Points

- High level of energy use and fluctuating fuel costs results in more expense to ceramic production, lowering manufacturer margins.

- Uncertainty about the prices and supply availability of raw materials (clay, feldspar, silica, alumina, zircon) adds concern for manufacturers.

- Stringent environmental policies and carbon emission standards require investment in cleaner technologies and environmentally friendly business practices

- Ceramic products can be large, weighty and delicate in nature, adding considerable cost to shipment, handling and storage which causes product damage.

- Low-cost producers in certain regions apply price-pressure on the ceramic industry, restricting expansion possibilities for profit generation, particularly for more commoditized ceramic items.

- Buyer requirement for top-notch quality, tailored options, certified components and consistent supply makes supplier choice more arduous.

- Substantial investment in newer kilns, automated operations, printing tech and more modern ceramic creation restricts expansion plans by small and medium enterprises.

- Demand from infrastructure, automotive, construction and various industries is irregular and it's challenging for organizations to plan production or fully utilize their capacity while the economy declines.

Recent Developments

- March 2026: RAK Ceramics expanded premium product range by investing in new sustainable ceramic and sanitaryware product lines to emphasize green manufacturing and energy efficiency in production processes.

- February 2026: Kajaria Ceramics accelerated retail distribution and investment in premium vitrified tile and digitally printed ceramic tile product categories to enhance presence in the residential and commercial building sector.

- December 2025: Mohawk Industries invested in manufacturing upgrades and new product development particularly with the focus on premium ceramic flooring options and digitally printed product development, along with sustainability practices in the production processes.

- September 2025: Kyocera Corporation enhanced advanced ceramic product portfolio to increase high-value ceramic components, especially for semiconductor production, electric vehicles, healthcare applications and industrial applications, aiming to benefit from a growth trend.

- June 2025: SCG Ceramics continued its strategy of enhancing energy efficiency in its manufacturing, producing high-value tile ranges and targeting expansion across Southeast Asia’s key regions to meet rising residential, commercial and infrastructure demand.

Analyst View and Opinion

- Construction & Infrastructure account for majority of the revenue share driven by ongoing urbanization, government initiatives towards building infrastructure across the globe and ongoing residential and commercial construction activities worldwide.

- Advanced ceramics is expected to outperform conventional ceramic products as adoption of advanced ceramic products across various end use applications such as semiconductor, automotive (EVs), healthcare, aerospace, renewable energy, industrial automation is gaining pace.

- Sustainability will act as a major competitive differentiator. The focus will be on enhancing product properties and adopting greener alternatives to conserve environment and adhere to global sustainability regulations.

- Asia-Pacific will lead the market and occupy largest share both in production and demand. North America and Europe will account for significant market share in high value segments of advanced ceramics through technological innovations, industrial developments.

- Growing manufacturing & exporting capabilities due to relatively cheap production costs coupled with augmenting productive capacities is attracting key global ceramic producers to look at countries such as India & Southeast Asia to enhance manufacturing operations and export base of conventional ceramics.

- Manufacturing process enhancements through advancement in artificial intelligence (AI), automation, additive manufacturing (AM) and digitally manufactured components will further drive efficiencies, quality enhancements, manufacturing agility, supporting and strengthening market positions of the larger manufacturers.

- The presence of product portfolio diversity, extensive distribution network, capability to adopt sustainable practices and constant efforts towards innovation in research and development is important for success in the long run and also to capitalize the potential to acquire maximum share in the evolving global ceramics market.

Target Audience

| Industry | Who Should Buy This Report? | Reason To Buy This Report |

| Construction& Infrastructure | Project Developers, EPC Contractors, Architects, Procurement Teams | Evaluate demand trends for ceramic tiles, sanitary ware, pipes and decorative building materials across residential, commercial and infrastructure projects. |

| Industrial Manufacturing | Plant Managers, Process Engineers, Procurement Heads | Assess demand for refractories, wear-resistant ceramics and industrial ceramic components across steel, cement, mining and chemical industries. |

| Electronics Semiconductors | Product Development Teams, Materials Engineers, R&D Teams | Understand growth opportunities for advanced ceramics in semiconductors, electronic components and precision engineering applications. |

| Automotive Aerospace | Design Engineers, Component Manufacturers, Innovation Teams | Evaluate the adoption of high-performance ceramics for electric vehicles, aerospace systems, thermal management and lightweight engineering applications. |

| Healthcare & Medical Devices | Medical Device Manufacturers, Product Development Teams, Quality Managers | Analyse the use of advanced ceramics in medical implants, dental applications, surgical instruments and diagnostic equipment. |

| Distributors & Building Material Suppliers | Distribution Managers, Channel Partners, Commercial Teams | Identify regional demand trends, supplier benchmarking, product portfolio opportunities and distribution strategies across construction and industrial markets. |

| Investors & Consulting Firms | Private Equity Firms, Corporate Strategy Teams, Market Consultants | Assess market growth potential, competitive positioning, investment opportunities, technology trends and regional expansion strategies within the global ceramics industry. |

What DataM Uniquely Provides

- Client-ready market intelligence linking ceramic demand by product, manufacturing type, end use and end use application and geography.

- Bottom-up market modelling from ceramic manufacturers, raw material suppliers, distributors and other new industrial activity, advanced ceramics users etc

- Competitive profiling across manufacturing capacity, product types, technology usage, investment, sustainability initiatives, distribution, presence in different geographic markets etc

- Procurement and price trends covering raw materials costs, energy costs impact, suppliers’ reliability, lead times, inventory strategy and supply chain security.

- A comparative analysis of ceramic tiles, sanitary ware, refractories, glass-ceramics, ceramic matrix composites and traditional, advanced ceramic options for construction, industrial, consumer electronics, automotive and healthcare applications.

- Strategic and operational risk ranging from raw material security to the rise of competitors.