Ceramic Liner Market Size

The global ceramic liner market reached US$ 15.85 billion in 2025 and is expected to reach US$ 26.17 billion by 2035, growing with a CAGR of 5.1% during the forecast period 2026-2035. Ceramic liners with their high abrasion resistance, corrosion resistance, and improved hardness, especially the alumina and silicon carbide variants, are increasingly being used to replace traditional metal liners in highly abrasive applications. Growth in the industry is also being fueled by growth in investments made in the modernization and automation of mineral processing plants along with large infrastructure developments that call for continuous handling of abrasive materials. In its "Mineral Commodity Summaries 2026" report, the U.S. Geological Survey has reported continued growth in the consumption of industrial minerals, including bauxite, alumina, iron ores, copper, and other hard rocks around the world. It states that 1.7 million metric tons of bauxite were used in U.S. in 2025, while production of alumina was about 710,000 metric tons.

Engineers and operators in industries such as the manufacture of cement, mining, electricity generation, and steel production are gradually integrating engineered ceramic liners in order to enhance the performance of the equipment and reduce the downtime experienced due to extreme wear. The development of environmentally friendly infrastructure as well as resource efficient manufacturing processes is being supported by the governments and industrial manufacturers resulting in more incorporation of wear resistant materials. According to the International Energy Agency (IEA), the world's cement industry comprises of old production assets that are in need of renovation.

Key Takeaways

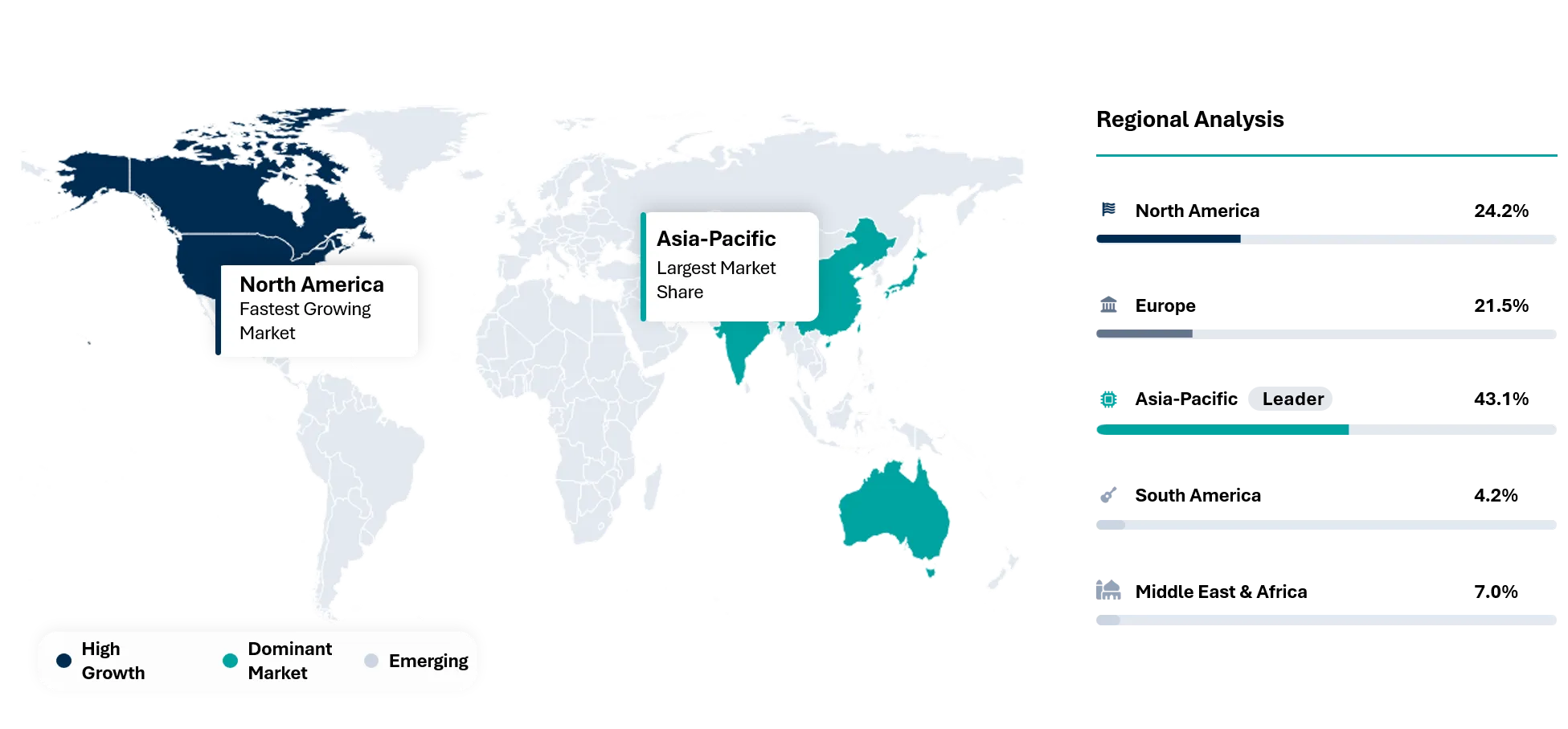

- Asia-Pacific dominated the global ceramic liner market with 43.1% in 2025, supported by rapid expansion of mining, cement, steel, power generation, and industrial processing industries across China, India, and Australia, while North America continues to witness steady demand driven by replacement of wear-resistant equipment and modernization of bulk material handling infrastructure.

- Alumina ceramic liners accounted for the largest market share in 2025, owing to their superior wear resistance, cost-effectiveness, high hardness, and extensive adoption across mining, cement, power generation, and mineral processing applications.

- Zirconia ceramic liners are expected to be the fastest-growing product segment during the forecast period, driven by increasing demand for high-impact resistance, exceptional fracture toughness, and superior performance in highly abrasive and corrosive industrial environments.

- Saint-Gobain, Metso, FLSmidth, CoorsTek, and CeramTec have established themselves as leading players in the market through continuous product innovation, advanced engineered wear protection solutions, strategic capacity expansions, and strong partnerships with mining and industrial processing companies.

Market Scope

| Metrics | Details | |

| 2025 Market Size | US$ 15.85 Billion | |

| 2035 Projected Market Size | US$ 26.17 Billion | |

| CAGR (2026-2035) | 5.1% | |

| Largest Market | Asia-Pacific | |

| Fastest Growing Market | North America | |

| By Material Type | Alumina Ceramic Liners, ZTA Ceramic Liners, Silicon Carbide Ceramic Liners, Zirconia Ceramic Liners, Ceramic Rubber Composite Liners, Ceramic Steel Composite Liners, Cast Basalt Liners, Others | |

| By Product Type | Ceramic Wear Tiles, Ceramic Liner Plates, Ceramic Lined Pipes and Elbows, Ceramic Pulley Lagging, Ceramic Chute Liners, Ceramic Cyclone Liners, Modular Ceramic Panels, Others | |

| By Installation Method | Direct Bonding, Stud Welding, Bolt-On Liners, Rubber Backed Liners, Steel Backed Liners, Pre-Engineered Modular Systems, Others | |

| By Application | Mining Transfer Chutes and Material Handling, Cement Mill and Kiln Areas, Coal Handling and Power Plants, Steel and Metal Processing, Battery Powder Conveying, Chemical Processing, Oil and Gas Slurry Handling, Pulp and Paper, Others | |

| By End-User | Mining Companies, Cement Producers, Power Plants, Steel Producers, Battery Material Manufacturers, Chemical Processors, OEM Equipment Manufacturers, Maintenance Contractors, Others | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia, Singapore, Vietnam, Thailand, Philippines, Taiwan | |

| South America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

Why does this report matter in 2026?

Ceramic liners will see a strategic phase of expansion for the global market in 2026 with increased investments being made by the mining industry, cement industry, power generation plants, steel production facilities and the bulk material handling industries towards the development of wear resistant machines that help achieve higher levels of efficiency and lower maintenance costs. Increased focus on increasing life expectancy of industrial machines and lowering machine downtimes and increasing their productivity in abrasive conditions is driving the adoption of ceramic liner technologies in industrialized and developing economies globally.

The ceramic liner producers are coming under pressure to offer high-performing products for their applications and provide cost-effective solutions based on the changing demands of the industry. The ongoing developments in the alumina, silicon carbide, zirconia, and composite ceramics have led to enhanced durability, impact resistance, and corrosion resistance properties while transforming the competitive scenario in the market. The purchasing decision makers and engineering community now need to have an understanding of the material composition, wear-life, installation, cost of ownership, customizability, manufacturing quality, supply chain, and partnerships in order to find technologically competitive ceramic liner producers.

White Space & Investment Opportunities

- High-end ceramic liners designed specifically for hydrogen plants, green steel and carbon capture factories have largely been under-serviced in spite of increasing spending on high-temperature industrial installations.

- Local production of high-end alumina, zirconia, and silicon carbide lined products in India, South-east Asia, Middle East and South America provides a promising avenue as the capabilities for mining and mineral processing grow.

- Predictive wear monitoring through AI for ceramic-lined machinery provides another high growth avenue by decreasing unplanned downtime and improving maintenance schedules in mining, cement and energy sectors.

- Ceramic liners' recycling, ceramic lining system modules, as well as circular economy concepts provide promising investment targets as industrial consumers increasingly focus on lifecycle cost reduction.

Future Market Transformation

By 2035, the global market for ceramic liners will shift from providing regular wear-resistant components to offering smart solutions for protecting assets that have been designed to integrate with digital maintenance ecosystems. Suppliers will offer custom-made ceramic solutions backed by digital engineering, wear simulation, predictive maintenance analysis, and lifecycle assurance instead of liner products alone. Companies will move away from selling products towards service agreements, maintenance agreements, and plant reliability collaborations. The ceramic liners will be lightweight, modular, easy to install, and purpose-built for future generation mines, cement plants, power plants, steel mills, chemical processors, and hydrogen generation plants.

Buyer Decision-Making Criteria

The industrial operators, EPC contractors, and OEM equipment manufacturers mostly consider the following criteria when selecting ceramic liners manufacturers – wear resistance, operational life, quality of materials used, installation proficiency, total lifecycle cost, and proven performance in harsh conditions. High abrasion, corrosion, and impact resistance are some of the minimum technical parameters that must be met by any ceramic liners manufacturers. In most cases, the promptness of responses from suppliers, customization abilities, and reliability of deliveries become decisive criteria in making purchase decisions. Nowadays, buyers tend to favor suppliers who can perform digital wear analysis, finite element simulations, and material selection for applications.

Economic & Investment Analysis

High interest rates could lead to delayed investments into mining capacity expansion, setting up cement factories and industrial facilities, thereby resulting in temporary decline in demand for ceramic liners. Growing investments into critical minerals, renewable energy, steel modernization, and industrial decarbonization remain supportive factors for long-term fundamentals of the market. Cost inflation in raw materials, energy-intensive production process, logistics and personnel expenses could be a challenge for producers' margins unless supplemented with long-term supply agreements and value-based pricing strategy. Currency movement will also impact international procurement because of internationally linked supply chain. While industrial investments move cyclically, the ceramic liner market remains favored with growing demand for longer service life, lower maintenance expenses, increased efficiency and plant uptime. Increasing capital expenditures are allocated to automated ceramic manufacturing, digital testing, innovative ceramic materials, local production and predictive maintenance systems.

Investment Trends in the Market

- Advanced alumina, zirconia, silicon carbide, and composite ceramic liner development.

- Automated pressing, robotic installation, precision machining, and AI-enabled quality inspection systems.

- Regional ceramic manufacturing facilities near major mining, cement, steel, and industrial clusters.

- Digital wear monitoring, predictive maintenance platforms, and lifecycle asset management solutions.

- Sustainable ceramic production technologies, recyclable ceramic materials, and low-carbon manufacturing processes.

Strategic Indicators For Ceramic Liner Market

High Regulation Impact

The global market for ceramic liner has become more influenced by the growing strictness of industrial safety, mining sustainability, and emissions regulations favoring high durability wear-resistant systems to regular metal replacement. Australia and Canada have continued to demand rigorous mine safety and asset integrity standards that have led to the adoption of ceramic liners on bulk material handling systems. In the United States, there has been emphasis on the reliability of operations in mining and power industry standards. Europe through the Industrial Emissions Directive has promoted equipment upgrade with the use of durable ceramic liners. China has tightened environmental inspections on its mining and heavy industries, forcing the substitution of wear materials with ceramic liners.

High Investment Activity

Investment levels continue to rise as the industry focuses on technologies that will improve productivity. Australia is leading in investments as a result of growth in iron ore, lithium, and critical minerals processing, leading to increased demand for high-quality ceramic liners. An increased investment level is seen in Canada in battery mineral projects which will need abrasion-resistant equipment. In Saudi Arabia, there are emerging opportunities for ceramic lined equipment as a result of the diversification of the mining industry. In Indonesia, there are more investment opportunities due to the expansion of the nickel processing industry.

Supply Chain Disruption

Vulnerability still exists within the ceramic liners' supply chain from alumina, zirconia, specialized bonding materials, and precision ceramic components manufacturing. China is a major source of high purity alumina processing and ceramic tiles manufacturing, meaning that there is reliance on China's industrial activities and exports. Shipping delays from the Red Sea have increased transportation times for customers from Europe and the Middle East, while the trade policies remain important in influencing purchasing decisions for North American consumers. Australia is a reliable source of raw materials, although processing occurs mostly in Asia.

Pricing Volatility

Price volatility is mainly caused by the price fluctuation of raw material such as alumina, energy usage in ceramic sintering process, overseas freight charges, and professional installation. The pricing benchmark remains influenced by Chinese manufacturing costs since China is leading in production capacity. High manufacturing cost in Europe can be attributed to high industrial energy cost in the region whereas North America players favor value pricing based on life cycle performance and not the purchase cost. Periodic increase in demand from Australian mining makes premium ceramic liners scarce during growth period.

Procurement Pressure

Procurement departments have been moving away from low cost towards total lifecycle value as mining, cement, steel, and power producers focus on optimizing maintenance activities. Increasingly, big industrial consumers are demanding suppliers who can deliver ceramic engineering, wear monitoring systems, quick installation and product availability. In Australia and Chile, there is an emphasis on local technical service for mining activities, while North America demands robust regional inventory to mitigate disruptions. In Europe, sustainable development principles are being included as part of supplier qualification. At the same time, reliance on Asian ceramic manufacturing leads to concentration risk.

New Technology Adoption

Adoption of technology is revolutionizing the manufacture of ceramic liners through improved material engineering, design, and predictive maintenance applications. China is leading automation of ceramic manufacture with the application of robotics and precise sintering processes. Germany and Japan are continuously developing high-performance formulas of alumina and zirconia that possess higher abrasion and impact resistance. In Australia, the use of digital asset management software and predictive maintenance tools in mining is contributing towards efficient ceramic liners replacement. Lasers scanning, digital twin modeling, finite element analysis, and modular ceramic lining systems are being applied by manufacturers.

Regional Expansion Opportunity

The Asia-Pacific region provides the best potential for business expansion by capitalizing on China's industrial development, Indonesia's nickel ore-processing investments, India's infrastructure development, and Australia's mining expansion. Growing need for abrasion-resistant machinery in the cement, steel, power generation, and critical minerals industries presents consistent opportunities for ceramic linings producers in the region.

Government Policy Support

Government policies in support of mining modernization, critical minerals production, infrastructure developments, and industry decarbonization have been boosting ceramic liner usage across the globe. In Australia, government policies favor advanced mining technologies that ensure operational efficiency and machinery durability. In Canada, government policies encourage critical minerals processing within the country through strategic investment approaches that involve wear-resistant processing infrastructures. In Saudi Arabia, Vision 2030 has boosted the growth of the mining sector, thus increasing the need for durable process machinery. In India, National Infrastructure Pipeline policy is still promoting investment in the cement, steel, and bulk materials industries.

Import Export and Pricing Intelligence

The global ceramic liner trade continues to be dominated by manufacturing exports from Asia, which cater to countries with high mining activities within Australia, North America, South America, and Africa. Buyers are now seeking diversity in terms of sourcing from a single country while ensuring warehousing, finishing, and installation partnerships in specific regions.

The price for ceramic liners is now based on performance as opposed to just the cost of production. High-end suppliers distinguish themselves through design flexibility, installation capabilities, life-cycle warranties, and technical advice. Suppliers are being evaluated based on total cost of ownership, maintenance efficiency, availability, and replacements.

| HS Code | Reporter | Trade Flow | 2025 Trade Value (US$) | Interpretation |

| 690912 | U.S. | Export | 2.1 Trillion | High-value ceramic exports strengthen advanced industrial liner manufacturing competitiveness globally. |

| 690912 | Germany | Export | 1.8 Trillion | Strong engineering exports reinforce premium ceramic liner production and technology leadership. |

| 690912 | United Kingdom | Import | 948.8 Billion | Rising imports indicate growing dependence on specialized wear-resistant ceramic component suppliers. |

| 690912 | Japan | Import | 755.4 Billion | Industrial demand supports sustained imports of precision ceramic liners for manufacturing. |

AI Impact Analysis

The application of Artificial Intelligence in the production of ceramic liners is revolutionizing the industry with respect to design optimization, manufacturing, and predictive maintenance. With the aid of AI, material simulation can be done quickly and faster to produce efficient and effective ceramic materials. Predictive analytics can predict the amount of wear of the liners through condition monitoring. Machine learning techniques are used to optimize the sintering process and decrease any errors in the production process. In addition, AI will assist in predicting demand, which increases the responsiveness of the manufacturers to their industrial customers.

Disruption Analysis

Conventional metal-based wear parts are being substituted with modern ceramic linings, which provide significantly better performance in terms of resistance against abrasion, corrosion, impact, and high temperatures. It can be seen in the mining, cement, steel, coal handling, energy, and bulk materials handling sectors, where any sort of unexpected shutdowns will have serious monetary consequences. Companies are reshaping their industries with their new products including engineered ceramic composite materials, rubber ceramic liner systems, and modular wear systems.

The increasing use of high-purity alumina, zirconia-toughened alumina (ZTA), silicon carbide, and advanced ceramic composites continues to increase product longevity and broaden the range of applications in harsh industrial settings. Sustainability goals are also influencing industry dynamics, with industries looking for more durable wear-resistant products that consume fewer raw materials and generate less waste.

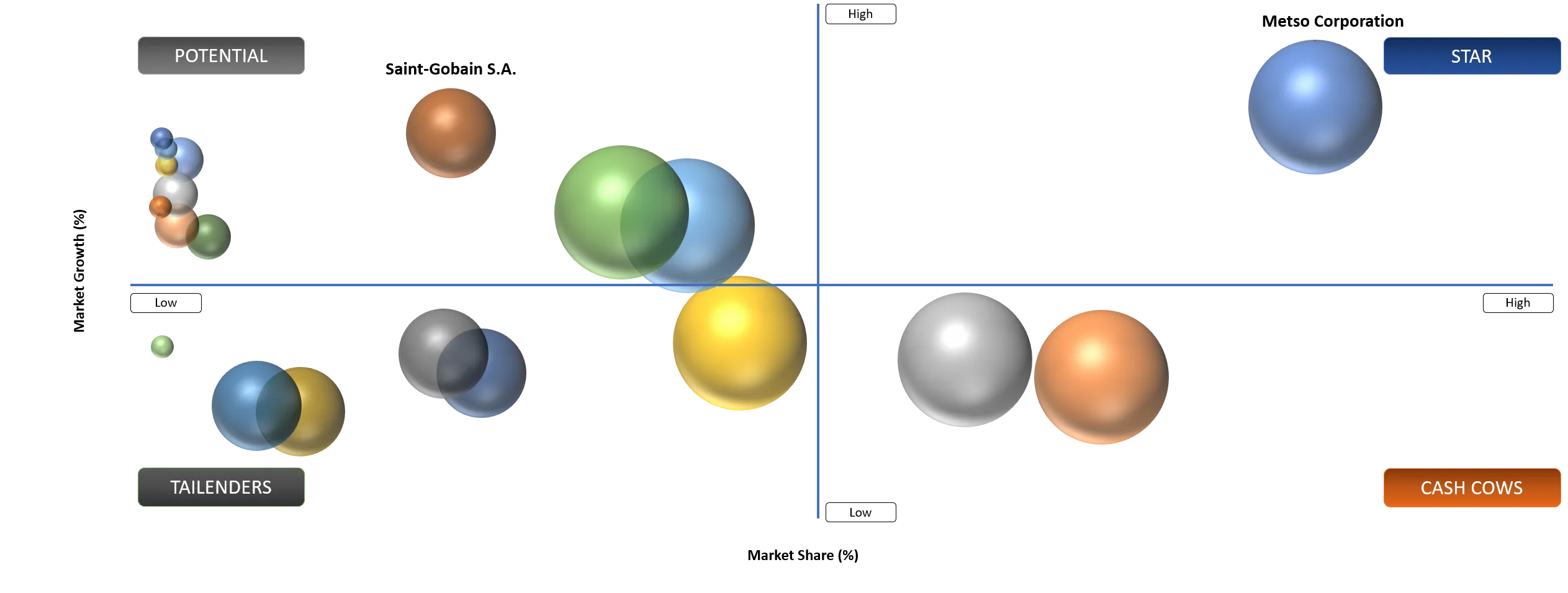

BCG Matrix: Company Evaluation

STAR

Star quadrant comprises corporations with technological strengths, industrial diversity, and positions in the wear-resistant materials solution industry. Companies like Metso Corporation, FLSmidth, Weir Group, and Kingcera maintain their superiority through continued product innovations, cutting-edge alumina and zirconia ceramic technology, and engineering solutions. The prominence in the mining, cement, steel, power generation, and mineral processing industries has created a constant need for premium ceramic lining solutions. Strategic focus on plant optimization, tailored lining solutions, and service network worldwide enhances their competitive advantage and makes these firms market leaders that generate consistent revenues and retain customers.

POTENTIAL

Potential players include regional manufacturers as well as ceramic engineering firms that have ventured beyond their home frontiers through customizing and offering cost-effective ceramic linings. Firms like Tega Industries, Saint-Gobain, CeramTec, and Blasch Precision Ceramics will enhance their market position through application-based wear protection technologies and increasing their efficiency in production as well as through distribution alliances. Increased investment in industrial modernization, localized production facilities, and innovative ceramic composite technologies give these firms an opportunity to increase their market presence. The increasing need for equipment longevity and reduced maintenance costs across the world makes these firms ready to become future market leaders.

Market Dynamics

Driver Impact Analysis

| Driver | Market Growth Impact (%) | Demand Concentration | Impacted Use Case | Strategic Impact |

Rising Demand for Wear-Resistant Solutions Across Mining and Mineral Processing | 5.20% | Australia, China, South Africa, Chile, and North America mining operations | Slurry pipelines, chutes, cyclones, hoppers, and beneficiation equipment | Increases equipment lifespan while reducing maintenance costs and operational downtime |

Expanding Adoption of Ceramic Liners in Cement, Power Generation, and Bulk Material Handling | 4.80% | Asia-Pacific, Middle East, and emerging industrial manufacturing hubs | Coal handling systems, conveyors, pulverizers, silos, and transfer points | Improves abrasion resistance and enhances operational efficiency in high-wear environments |

Increasing Industrial Investments in Corrosion and Abrasion-Resistant Processing Equipment | 4.50% | Chemical processing, steel manufacturing, and heavy industrial facilities globally | Reactors, pipes, tanks, elbows, and process equipment protection | Strengthens asset reliability and lowers lifecycle operating expenses across critical infrastructure |

Growing Focus on Predictive Maintenance and Asset Life Extension Strategies | 4.20% | Large industrial enterprises, utilities, and process industries worldwide | Maintenance optimization, equipment refurbishment, and plant reliability programs | Accelerates ceramic liner adoption to maximize equipment availability and reduce unplanned shutdowns |

Growing Investments in Mining and Critical Mineral Processing

Investments in increased capacities and beneficiation of the mined minerals have become one of the most powerful catalysts driving ceramic liner usage throughout the world. Crushing circuits, slurries pipelines, hydrocyclones, flotation circuits, chute transfers, and grinding mills undergo severe abrasive wear, hence, necessitating the use of ceramic liners to achieve high levels of availability of plant equipment. The Investment in Critical Minerals Development is accelerating according to the International Energy Agency (IEA). Countries such as Australia, Chile, Indonesia, Canada, and various African countries are increasing their production of lithium, nickel, copper, cobalt, and rare earth minerals and require larger plants that are lined with premium wear-resistant ceramics. Also, the annual investment of over US$8 billion by ICMM member companies in innovation and sustainability is an indication that ceramic liner usage will continue to increase due to its benefits in maintenance reduction and increased plant efficiency.

Restraint Impact Analysis

| Restraint | Drag on Market Growth (%) | Primary Impact Area | Impacted Use Case | Strategic Impact |

High Installation and Replacement Costs of Ceramic Liners | 4.50% | Capital investment and maintenance budgets | Mining equipment, slurry pipelines, material handling systems | Restricts adoption among cost-sensitive industries and delays replacement of conventional wear protection solutions |

Performance Limitations Under Extreme Thermal Shock and Mechanical Impact | 3.90% | Operational reliability in harsh environments | High-temperature processing, cement kilns, steel manufacturing, power generation | Limits application in operations involving sudden temperature fluctuations and severe impact loading |

Complex Installation and Downtime During Retrofitting | 3.70% | Maintenance scheduling and production continuity | Retrofit of chutes, cyclones, hoppers, and industrial conveying systems | Increases operational downtime and discourages upgrades in continuous-process industries |

Availability of Lower-Cost Alternative Wear Protection Materials | 4.10% | Material selection and procurement decisions | Rubber liners, alloy steel liners, polymer-based wear protection systems | Intensifies pricing pressure and slows ceramic liner penetration in price-sensitive industrial applications |

High Installation Costs and Complex Replacement Procedures

Specialized adhesives and installation experts are required along with precision-designed substrates for efficient functioning of precision-ceramics under harsh conditions. Upgrading and replacements carried out during downtime are more complicated in continuous process-based industries like cement plants, mines, steel works, and thermal power stations. Smaller and medium-sized industrial sites defer upgrading owing to the initial low cost of standard steel linings even though their life is less than that of ceramics. Changing operating environments need custom-designed ceramic products, which further increase the cost of engineering and procurement. Uncertainty related to supply chains of specialty ceramic products like high purity alumina and zirconia is another factor contributing to rising costs.

Segmentation Analysis

The global ceramic liner market is segmented based on the material type, product type, installation method, application, end-user and region.

By End-User

Mining Industry Leads Market Adoption

The ceramic lining of equipment plays an important role in increasing the lifespan of equipment in such devices as crushers, SAG mills, ball mills, hydrocyclones, slurry pumps, pipes, and chutes exposed to extreme wear and tear. As stated by the International Energy Agency (IEA), there is an increasing demand for minerals used in clean energy technologies, such as copper, lithium, nickel, graphite, and rare earth elements. The largest mining firms are making huge investments in building concentrators and processing plants in Australia, Chile, Peru, Indonesia, and Canada, leading to the continued need for ceramic liner solutions. The modern-day digital mine increasingly utilizes predictive maintenance tools that help schedule ceramic liner replacements in the best possible way.

By Application

Power Generation and Industrial Processing Expand Applications

The use of high temperatures along with the movement of abrasive particles offers excellent opportunities for the utilization of Al2O3 and SiC ceramic linings. According to the statistics provided by the International Energy Agency (IEA), the demand for electricity is continuously growing together with the process of industrial electrification and, therefore, there are still investments being made in the area of thermal power generation maintenance, biomass plants, and industrial energy systems where wear-resistant equipment is highly required. The production of cement is gradually switching from the use of metallic to ceramic liners in order to lower the time periods for maintenance.

Market Segmentation

- By Material Type

- Alumina Ceramic Liners

- ZTA Ceramic Liners

- Silicon Carbide Ceramic Liners

- Zirconia Ceramic Liners

- Ceramic Rubber Composite Liners

- Ceramic Steel Composite Liners

- Cast Basalt Liners

- Others

- By Product Type

- Ceramic Wear Tiles

- Ceramic Liner Plates

- Ceramic Lined Pipes and Elbows

- Ceramic Pulley Lagging

- Ceramic Chute Liners

- Ceramic Cyclone Liners

- Modular Ceramic Panels

- Others

- By Installation Method

- Direct Bonding

- Stud Welding

- Bolt-On Liners

- Rubber Backed Liners

- Steel Backed Liners

- Pre-Engineered Modular Systems

- Others

- By Application

- Mining Transfer Chutes and Material Handling

- Cement Mill and Kiln Areas

- Coal Handling and Power Plants

- Steel and Metal Processing

- Battery Powder Conveying

- Chemical Processing

- Oil and Gas Slurry Handling

- Pulp and Paper

- Others

- By End-User

- Mining Companies

- Cement Producers

- Power Plants

- Steel Producers

- Battery Material Manufacturers

- Chemical Processors

- OEM Equipment Manufacturers

- Maintenance Contractors

- Others

Geographical Penetration

U.S. Ceramic Liner Market Landscape

The U.S. ceramic liner market is witnessing continuous growth as industries such as mining, minerals processing, power generation, cement, steel, and bulk materials handling continue to adopt ceramic liner made from materials like alumina and silicon carbide due to better performance compared to traditional liners made using steel. Investments in domestic manufacturing and critical minerals supply chain are driving the need for abrasion-resistant equipment.

More than US$6 billion worth of funds from the U.S. Department of Energy were granted through the Industrial Demonstrations Program to expedite decarbonization within the scope of heavy industries such as steel, cement, chemicals, and refining, providing incentives for the improvement of plants that benefit from using ceramic-lined chutes, cyclones, pipes, hoppers, and slurries because these allow for less frequent maintenance and greater operational efficiency. Additionally, the Infrastructure Investment and Jobs Act will allocate more than US$1.2 trillion to transportation, manufacturing, and energy infrastructure.

The United States is also witnessing growing adoption of advanced ceramics supported by federal research initiatives and domestic manufacturing incentives. The National Institute of Standards and Technology (NIST) continues expanding advanced manufacturing research involving structural ceramics and high-performance materials used in extreme industrial environments. The Department of Energy's Advanced Manufacturing Office (AMO) supports projects focused on improving industrial productivity, energy efficiency, and equipment durability, where ceramic liners contribute by minimizing downtime and reducing replacement cycles.

Japan Ceramic Liner Market Outlook

Japan's ceramic liner market is driven primarily by its globally competitive advanced manufacturing sector, where operational reliability, equipment longevity, and process precision remain critical priorities. Although Japan has comparatively limited domestic mining activity, its strong presence in steel production, chemicals, cement, power generation, waste recycling, and industrial machinery manufacturing creates consistent demand for high-performance ceramic wear solutions.

Organizations such as the Japan Fine Ceramics Association (JFCA) and leading research institutions continue advancing high-purity alumina, zirconia, silicon carbide, and composite ceramic materials with improved wear resistance and thermal stability for industrial applications. Regional recognized engineering companies increasingly integrate ceramic liners into material handling systems exported to mining, cement, and mineral processing industries globally.

China Ceramic Liner Market Trends

China remains the world's largest manufacturing and mining economy, making it the most significant demand center for ceramic liners used in highly abrasive industrial operations. The country's continuous expansion of steel, cement, coal, rare earth processing, and non-ferrous metal production has substantially increased the installation of wear-resistant ceramic solutions across material handling systems.

The International Energy Agency (IEA) reports that China continues to account for more than half of global coal consumption, sustaining enormous demand for ceramic-lined coal preparation plants, ash handling systems, slurry pipelines, and power generation equipment. China's strategic emphasis on advanced manufacturing under industrial modernization programs is also driving wider adoption of engineered ceramics capable of extending equipment life while reducing operational maintenance costs across heavy industries.

Competitive Landscape

- The global ceramic liner market is characterized by competition among established wear protection specialists, industrial ceramics manufacturers, engineered materials companies, and mining equipment suppliers.

- Competition focuses on ceramic composition, wear life, impact resistance, installation technology, customized engineering, and lifecycle service offerings.

- Companies continue investing in high-purity alumina ceramics, zirconia-toughened composites, silicon carbide solutions, modular liner designs, digital wear monitoring technologies, and application-specific engineering services to enhance operational efficiency across mining, power generation, cement, steel, and bulk material handling industries while supporting industrial decarbonization and asset reliability initiatives.

Company Coverage Preview

The Metso Corporation has been able to position itself among the leading technological suppliers in the international ceramic liner industry owing to the wide range of innovative wear protection products it offers to customers from mining, aggregates, and bulk material handling industries. Metso has immense experience in supplying ceramic wear liners, rubber-ceramic liners, chute liner solutions, mill liner solutions, and digital wear monitoring systems to ensure maximum machine availability and reduced maintenance and down time cost for the customers. Metso provides an integrated solution combining wear materials and lifecycle services including predictive maintenance and innovative attachment solutions which make it stand out from other suppliers due to high abrasiveness applications. Due to the global production network, well-developed aftermarket business and sustainable mining technology, Metso can be described as a leading supplier of high performance ceramic linings solutions.

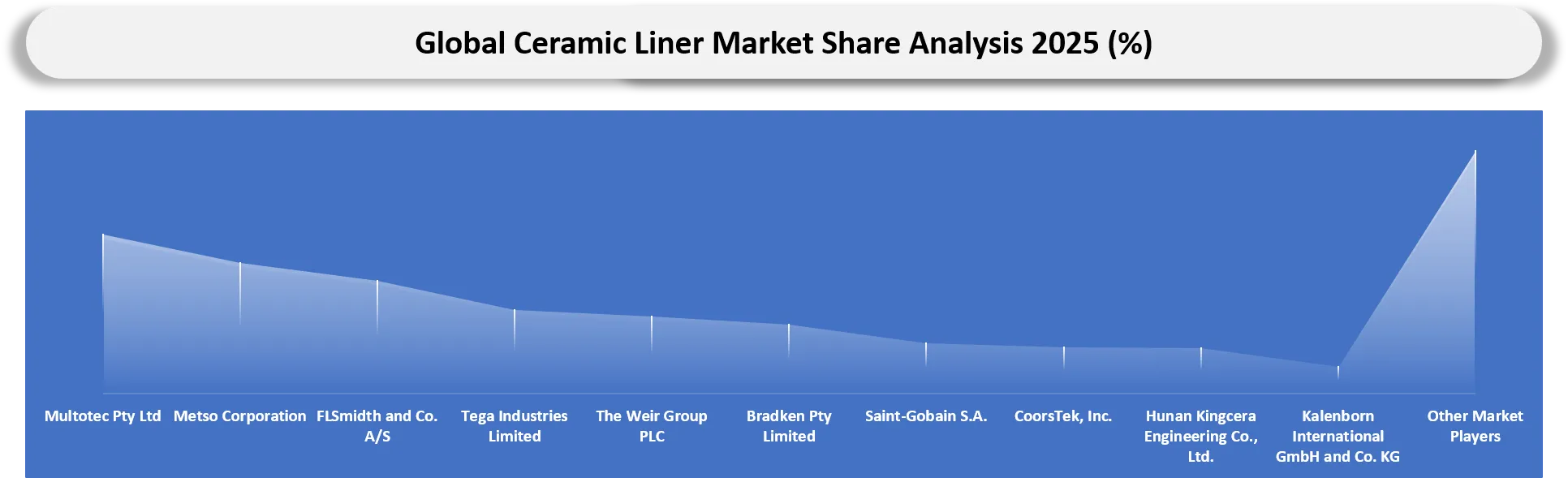

Key Companies

- Multotec Pty Ltd

- Metso Corporation

- FLSmidth and Co. A/S

- Tega Industries Limited

- The Weir Group PLC

- Bradken Pty Limited

- Saint-Gobain S.A.

- CoorsTek, Inc.

- Hunan Kingcera Engineering Co., Ltd.

- Kalenborn International GmbH and Co. KG

- Blasch Precision Ceramics, Inc.

- Corrosion Engineering, Inc.

- Hofmann Engineering Pty Ltd

- AIA Engineering Limited

- Vautid GmbH

- BMW Steels Ltd.

- Jyoti Innovision Pvt. Ltd.

- DMC Wear Parts

- Ceramic Technology, Inc.

- Good Earth Tools, Inc.

Major Pain Points

- High Initial Installation and Replacement Costs

- Complex Installation and Maintenance Requirements

- Brittleness and Risk of Mechanical Fracture

- Limited Suitability for High-Impact Applications

- Long Lead Times for Customized Ceramic Liners

- Raw Material Price Volatility

- Competition from Alternative Wear Protection Materials

- Challenges in Retrofitting Existing Industrial Equipment

- Supply Chain and Manufacturing Capacity Constraints

Recent Developments

- January 2026: Metso Corporation introduced next-generation mining wear solutions emphasizing integrated ceramic wear protection and lifecycle optimization, strengthening sustainable minerals processing offerings.

- January 2026: FLSmidth & Co. A/S expanded engineered ceramic lining portfolio supporting mine reliability, predictive maintenance, and longer equipment service intervals for mineral processing operations.

- January 2026: Multotec Pty Ltd featured among leading suppliers delivering engineered ceramic lining systems addressing abrasive slurry transport and plant uptime optimization.

- January 2026: The Weir Group PLC continued expanding integrated wear-management solutions combining ceramic linings with engineered maintenance services for mining customers globally.

- January 2026: Bradken Pty Limited recognized for advanced ceramic lining systems supporting higher throughput, wear reduction, and maintenance optimization across mining applications.

Analyst View / Opinion

- Mining and mineral processing industries will remain the largest revenue contributors due to rising demand for wear-resistant equipment in slurry handling, grinding, and ore transportation applications.

- Alumina-based ceramic liners are expected to maintain market leadership owing to their favorable balance of cost, hardness, abrasion resistance, and broad industrial compatibility.

- Adoption of ceramic liners in power generation and cement plants will accelerate as operators prioritize maintenance cost reduction and extended equipment life.

- Hybrid liner solutions combining ceramic and rubber materials will gain traction for applications requiring both impact resistance and abrasion protection.

- Asia-Pacific will continue to dominate market demand, supported by large-scale mining activities, industrial expansion, and infrastructure development in China, India, and Southeast Asia.

- Digital monitoring of wear patterns and predictive maintenance integration will become an important value-added differentiator among leading ceramic liner suppliers.

- Energy efficiency benefits from reduced friction and improved material flow will increasingly influence procurement decisions in bulk material handling industries.

- Replacement demand from aging industrial infrastructure will contribute a significant share of market growth, particularly in mature mining and power-generation regions.

- Customization capabilities for complex equipment geometries and high-wear zones will become a key competitive factor for manufacturers.

- Strategic partnerships between ceramic material producers, engineering firms, and mining equipment OEMs will intensify as suppliers seek long-term maintenance and replacement contracts.

Target Audience

| INDUSTRY | WHO SHOULD BUY THIS REPORT? | REASON TO BUY THIS REPORT |

| Ceramic Liner Manufacturers | Product Development Managers, R&D Engineers, Business Development Teams | Evaluate market demand, emerging material innovations, competitive positioning, and application trends for ceramic liner solutions across industries. |

| Mining & Mineral Processing Companies | Plant Managers, Maintenance Engineers, Processing Operations Teams | Assess ceramic liner adoption to reduce equipment wear, improve operational reliability, and extend service life in abrasive mineral handling applications. |

| Cement Manufacturers | Plant Engineering Teams, Maintenance Heads, Procurement Managers | Analyze wear protection solutions for mills, chutes, cyclones, and conveying systems to minimize downtime and maintenance costs. |

| Power Generation Companies | Asset Reliability Managers, Boiler Maintenance Teams, Operations Engineers | Understand ceramic liner demand for coal handling systems, ash conveying equipment, and high-abrasion process environments to improve plant efficiency. |

| Steel & Metal Processing Companies | Production Managers, Maintenance Engineers, Equipment Reliability Teams | Evaluate advanced ceramic lining solutions for material handling systems, blast furnaces, transfer chutes, and other high-wear industrial equipment. |

| Oil & Gas & Petrochemical Companies | Process Engineers, Asset Integrity Managers, Procurement Teams | Assess corrosion- and abrasion-resistant ceramic liners for pipelines, slurry transport systems, reactors, and processing equipment operating under harsh conditions. |

| Material Handling & Bulk Processing Equipment Manufacturers | Design Engineers, Product Development Teams, OEM Partnership Managers | Identify opportunities to integrate ceramic liners into conveyors, hoppers, feeders, cyclones, and transfer systems to enhance equipment durability and lifecycle performance. |

| Industrial Maintenance & EPC Service Providers | Maintenance Planning Teams, Reliability Consultants, Project Engineers | Benchmark ceramic liner technologies and identify retrofit opportunities that improve operational uptime while lowering long-term maintenance expenditures. |

| Ceramic Raw Material & Advanced Ceramics Suppliers | Technical Sales Teams, Materials Scientists, Market Intelligence Managers | Analyze future demand for alumina, zirconia, silicon carbide, and other advanced ceramic materials used in wear-resistant lining applications. |

| Investors, Private Equity & Consulting Firms | Investment Analysts, Strategy Consultants, Industrial Market Intelligence Teams | Evaluate market growth potential, technology advancements, competitive landscape, investment opportunities, and long-term demand across key ceramic liner end-use industries. |

Why Choose DATAM?

- Data-Driven insights: Dive into detailed analyses with granular insights such as pricing, market shares and value chain evaluations, enriched by interviews with industry leaders and disruptors.

- Post-Purchase Support and Expert Analyst Consultations: As a valued client, gain direct access to our expert analysts for personalized advice and strategic guidance, tailored to your specific needs and challenges.

- White Papers and Case Studies: Benefit quarterly from our in-depth studies related to your purchased titles, tailored to refine your operational and marketing strategies for maximum impact.

- Annual Updates on Purchased Reports: As an existing customer, enjoy the privilege of annual updates to your reports, ensuring you stay abreast of the latest market insights and technological advancements. Terms and conditions apply.

- Specialized Focus on Emerging Markets: DataM differentiates itself by delivering in-depth, specialized insights specifically for emerging markets, rather than offering generalized geographic overviews. The approach equips our clients with a nuanced understanding and actionable intelligence that are essential for navigating and succeeding in high-growth regions.

- Value of DataM Reports: Our reports offer specialized insights tailored to the latest trends and specific business inquiries. The personalized approach provides a deeper, strategic perspective, ensuring you receive the precise information necessary to make informed decisions. The insights complement and go beyond what is typically available in generic databases.

What DATAM Uniquely Provides

- Granular analysis of ceramic liner demand across mining, cement, steel, power generation, and bulk material handling industries globally.

- Detailed benchmarking of leading manufacturers based on technology capability, production integration, innovation pipeline, and competitive positioning.

- Plant-level investment tracking covering mining expansions, mineral processing facilities, and industrial modernization projects influencing future demand.

- Comprehensive raw material intelligence evaluating alumina, zirconia, energy costs, manufacturing trends, and procurement risk dynamics.

- Country-wise regulatory assessment linking industrial policies, mining investments, sustainability initiatives, and equipment modernization with ceramic liner adoption.

- Technology roadmap covering advanced ceramics, digital wear monitoring, predictive maintenance, modular designs, and manufacturing automation developments.

- Strategic opportunity mapping identifying high-growth regions, emerging end-use sectors, investment hotspots, and future competitive landscape evolution.