Bunker Fuel Market Overview

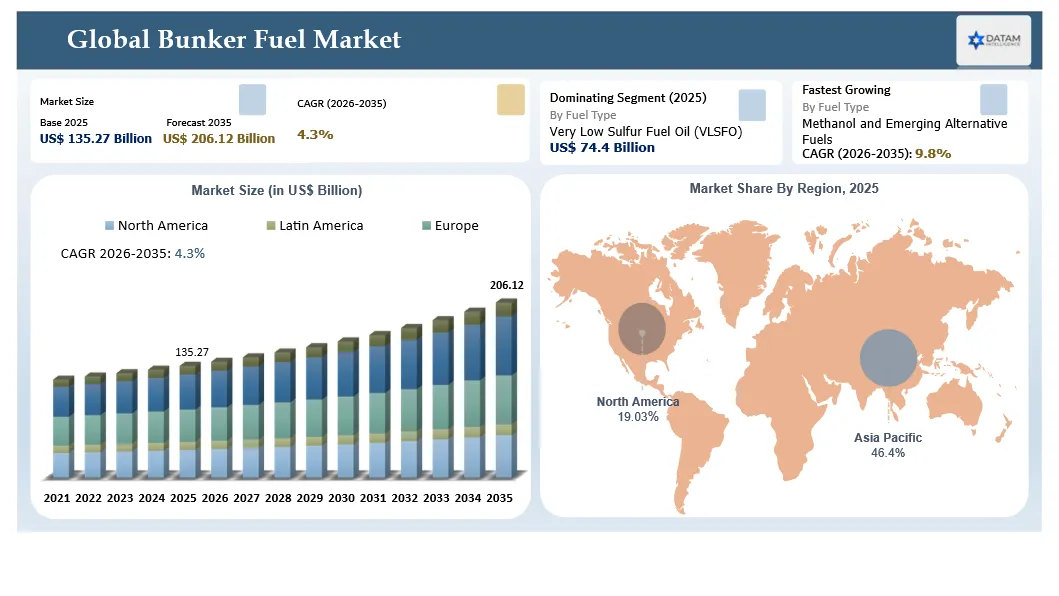

The global bunker fuel market is estimated at US $135.27 billion in 2025 and is expected to reach US $206.12 billion by 2035, growing with a CAGR of 4.3% during the forecast period 2026-2035. Bunker fuel remains a critical operating input for international shipping, port logistics and offshore vessel operations. The market is increasingly shaped by compliance-grade fuels, voyage optimization, price-risk management and alternative marine fuel readiness rather than simple residual fuel supply.

Global shipping carries over 80% of world trade, but maritime trade growth is expected to slow to 0.5% in 2025 after 2.2% growth in 2024, before averaging around 2% annually during 2026-2030. This creates a mixed bunker demand environment. Fuel volumes remain structurally tied to global trade, but buyer priorities are shifting toward efficiency, route risk, fuel quality, delivery certainty and carbon compliance. Singapore remains the most important bunkering hub, with marine fuel sales reaching 56.77 million tonnes in 2025, a 3.4% increase from 2024. This hub-level data demonstrates how port competitiveness, reliable supply and multi-fuel readiness directly influence bunker fuel demand.

Environmental regulation is the main disruption. IMO’s Net-Zero Framework approved at MEPC 83 in April 2025 introduces a new fuel standard and global GHG pricing mechanism for large ocean-going ships above 5,000 gross tonnage, which account for around 85% of international shipping CO2 emissions. This pushes bunker buyers to evaluate VLSFO, MGO, LNG, biofuel blends, methanol and future ammonia pathways as part of procurement strategy. LNG is already more mature than most alternative fuels, with around 800 LNG-capable vessels in service, 600 more on order, bunkering available in 222 ports and 62 dedicated bunker vessels reported in 2026.

The market outlook to 2035 will be shaped by fuel grade substitution, alternative fuel infrastructure, refinery sulfur economics, geopolitical route changes, port availability, carbon intensity documentation and digital bunker procurement. Buyers need actionable insight on where compliant fuels are available, which suppliers can support long-term contracts, how fuel quality affects engine reliability and how carbon rules affect voyage economics.

| Metric | Details |

| 2025 Market Size | US$ 135.27 Billion |

| 2035 Projected Market Size | US$ 206.12 Billion |

| CAGR (2026-2035) | 4.3% |

| Largest Market | Asia-Pacific |

| Fastest Growing Market | Europe |

| Largest Fuel Segment | Very Low Sulfur Fuel Oil and compliant low sulfur marine fuels |

| Fastest Growing Fuel Segment | LNG bunker fuel, biofuel blends and methanol-ready supply |

| By Fuel Type | VLSFO, HSFO, MGO, MDO, LNG, biofuel blends, methanol and emerging alternative fuels |

| By Vessel Type | Container vessels, bulk carriers, tankers, gas carriers, cruise vessels, offshore support vessels and general cargo vessels |

| By Distribution Channel | Oil majors, integrated suppliers, independent bunker traders, port physical suppliers and digital procurement platforms |

| By Region | North America, Europe, Asia-Pacific, South America, Middle East and Africa |

| Report Insights Covered | Market size, forecast, buyer decision criteria, fuel transition, port hub analysis, pricing, supply chain, regulation, procurement models and competitive landscape |

Bunker Fuel Market Key Takeaways

- The market is estimated at US$ 135.27 billion in 2025 and is projected to reach US$ 206.12 billion by 2035, expanding at a CAGR of 4.3% during 2026-2035.

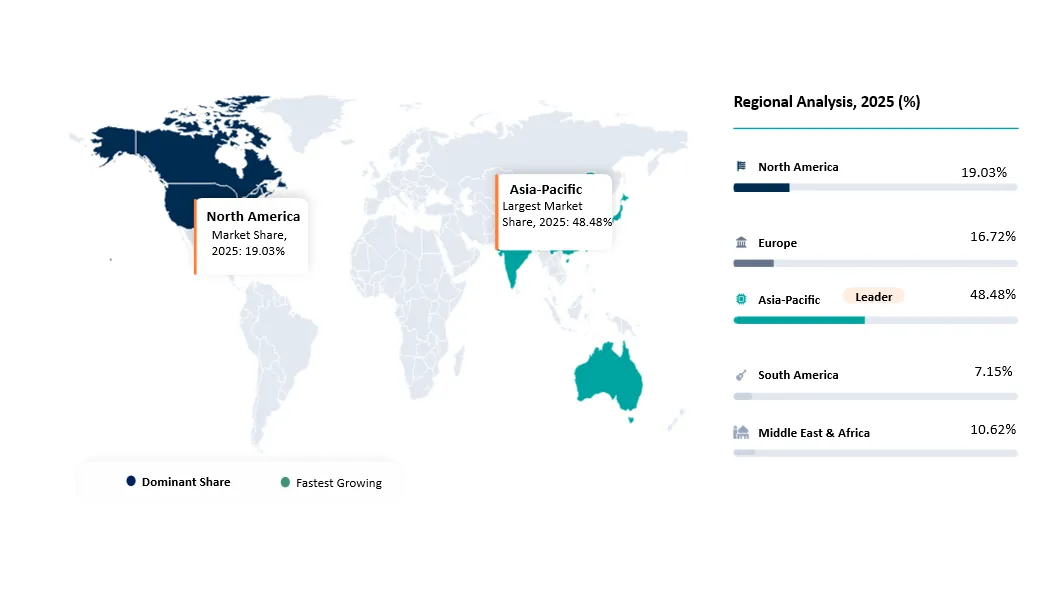

- Asia-Pacific is the largest regional market, supported by Singapore, China, South Korea, Japan and Southeast Asian trade lanes. Public market estimates place Asia-Pacific at about 45.6% of global bunker demand in 2025.

- Europe is the fastest growing region because EU ETS, FuelEU Maritime, alternative fuel corridor investments and stricter carbon accounting are changing bunker procurement faster than in most other regions.

- VLSFO and compliant low sulfur fuels remain the largest fuel category because IMO 2020 sulfur rules continue to shape mainstream bunker procurement for vessels without scrubbers or alternative fuel engines.

- LNG bunker fuel, biofuel blends and methanol-ready supply are the fastest growing fuel transition categories as dual-fuel vessels, green corridors and long-term decarbonization rules increase demand for alternative fuels.

- Singapore sold 56.77 million tonnes of marine fuel in 2025, reinforcing the importance of port-level supply reliability, digital bunker operations, fuel testing and multi-fuel infrastructure.

- Large ocean-going ships above 5,000 gross tonnage account for around 85% of international shipping CO2 emissions under IMO’s regulatory framing, making this vessel class the key compliance target for bunker fuel transition.

- Fuel procurement is moving from spot price buying toward risk-managed sourcing, where shipowners and charterers evaluate fuel quality, lead time, carbon intensity, supplier credit, delivery mode and regulatory documentation.

Bunker Fuel Market Industry Trends and Strategic Insights

- Bunker buyers are shifting from single-fuel procurement toward multi-fuel planning covering VLSFO, HSFO with scrubbers, MGO, LNG, biofuel blends and methanol where port infrastructure exists.

- Fuel availability is stable at a macro level but increasingly localized, with prompt supply risks in specific ports and grades creating operational exposure for voyage planners.

- Alternative fuel adoption is being determined by lane-level infrastructure rather than vessel capability alone. Dual-fuel vessels need reliable availability at recurring bunkering ports to use low-carbon fuel consistently.

- Digital bunker procurement platforms are gaining buyer attention because fuel remains one of the largest voyage cost items and price volatility can materially affect freight margins.

- Fuel quality, sulfur compliance, viscosity, catalytic fines, stability and contamination risk are becoming stronger buyer decision factors because off-spec fuel can create engine damage, dispute costs and voyage delays.

- Carbon compliance is creating demand for lifecycle emissions documentation, mass balance claims, sustainable biofuel certification and auditable bunker delivery records.

Why does this report matter in 2026?

In 2026, bunker fuel procurement is becoming a strategic cost, compliance and operational resilience decision. Shipping companies are dealing with slower trade growth, rerouted voyages, fuel price volatility, carbon rules, alternative fuel uncertainty and tighter customer expectations around emissions. A bunker buyer can no longer evaluate fuel only by delivered price. The decision now includes fuel grade availability, port lead time, supplier reliability, carbon intensity, engine compatibility, documentation quality and regulatory exposure.

This report matters because it converts fuel transition uncertainty into actionable market intelligence. It helps bunker suppliers identify where fuel grade demand is moving, helps shipowners assess procurement risk across major ports and supports investors evaluating LNG, biofuel, methanol and port infrastructure opportunities. It also supports refiners and traders assessing how sulfur rules, scrubber economics and regional price spreads are reshaping demand for residual fuel, distillates and alternative marine fuels.

Bunker Fuel Market White Space & Investment Opportunities

- Expansion of alternative fuel bunkering infrastructure at strategic ports serving container, tanker and cruise routes.

- Digital bunker procurement platforms that combine pricing, availability, credit risk, delivery tracking and claims management.

- Low-carbon bunker fuel certification services covering biofuel sustainability documentation, carbon intensity reporting and mass balance verification.

- Fuel quality testing and advisory services for VLSFO stability, catalytic fines, biofuel blending, methanol handling and LNG custody transfer.

- Port-based storage and blending hubs that can supply VLSFO, B30 blends, LNG and methanol from the same commercial platform.

- Voyage-level bunker optimization tools using weather data, speed planning, cargo load and port availability to reduce fuel burn and emissions.

Bunker Fuel Future Market Transformation

The bunker fuel market is expected to transform from a petroleum residual fuel supply business into a multi-fuel marine energy ecosystem. Conventional bunker fuels will remain important through 2035, but the growth layer will increasingly come from compliant low sulfur fuels, LNG, biofuel blends, methanol and future ammonia readiness. This transformation is not uniform. LNG has the strongest near-term infrastructure base, biofuel blends can use existing engines in many cases, methanol is scaling through container liner commitments and ammonia remains early due to safety, engine and infrastructure challenges.

Digital transformation will also reshape buying behavior. Shipowners and charterers are expected to rely more on digital procurement, predictive fuel consumption, real-time price intelligence and supplier scorecards. The strongest suppliers will offer fuel molecules, documentation, delivery reliability, carbon data and advisory support. Ports that can offer multi-fuel bunkering, efficient barge availability and low dispute rates will become preferred procurement hubs.

Bunker Fuel Market Buyer Decision-Making Criteria

Bunker buyers evaluate suppliers based on delivered price, credit terms, availability, fuel quality, delivery lead time, port coverage, dispute handling, documentation and compliance support. In 2026, carbon and alternative fuel readiness are becoming additional decision layers. Shipowners operating under EU ETS, FuelEU Maritime or charterer sustainability clauses increasingly need proof of fuel quality, emissions factors, certification and timely bunker delivery notes. Buyers also prefer suppliers with multi-port coverage because route disruptions can force unplanned bunkering in alternative hubs.

Bunker Fuel Market Economic & Investment Analysis

Bunker fuel represents one of the largest variable operating costs in maritime transport. Even small price changes can affect voyage profitability, chartering economics and freight rates. The market’s investment case is linked to port infrastructure, fuel storage, blending capacity, bunker barges, digital procurement tools, testing services and alternative fuel supply chains. Investment is moving toward assets that reduce compliance uncertainty and create optionality across fuel pathways. LNG bunker vessels, methanol storage, biofuel blending, certified fuel documentation and digital fuel optimization tools are becoming more attractive than simple commodity distribution capacity.

The macro backdrop is mixed. UNCTAD expects maritime trade growth to slow to 0.5% in 2025 before averaging 2% annually over 2026-2030, which means volume growth alone will not define winners. Margin will increasingly come from differentiated service, lower claims risk, multi-fuel capability and better data. Singapore’s 56.77 million tonnes of 2025 bunker sales shows that high-quality hub infrastructure can continue to attract global demand even during a volatile trade environment.

Bunker Fuel Investment Trends in the Market

- Higher investment in LNG bunker vessels, small-scale LNG terminals and port-based LNG supply to serve dual-fuel vessel growth.

- Growing funding for biofuel blending systems, sustainable feedstock certification, B24, B30 and B100 bunker trial supply chains.

- Development of methanol bunkering barges and ship-to-ship methanol transfer procedures at strategic container hubs.

- Investments in fuel testing labs and advisory services to address VLSFO quality, biofuel stability, methanol handling and claims disputes.

- Increasing use of bunker procurement platforms and data tools to reduce price exposure, improve credit control and optimize bunker lift timing.

Strategic Indicators For Bunker Fuel Market

High Regulation Impact

The market is strongly regulation driven because IMO sulfur limits, EU ETS, FuelEU Maritime and the IMO Net-Zero Framework directly affect fuel choice and procurement documentation. The move toward GHG pricing for large ships above 5,000 gross tonnage will accelerate demand for compliant fuels, fuel intensity reporting and alternative marine fuels.

High Investment Activity

Investment is rising in LNG bunkering, methanol bunkering, biofuel blending, digital fuel procurement and port infrastructure. The strongest capital allocation is focused on assets that can serve multiple fuels and support shipowners through the transition period rather than assets tied to one fuel pathway.

Supply Chain Disruption

Bunker supply is exposed to refinery outages, geopolitics, route disruptions, port congestion, barge availability and localized tightness in VLSFO, HSFO or LSMGO. Buyers are increasingly using multi-port procurement planning to reduce operational exposure.

Pricing Volatility

Bunker pricing is influenced by crude oil, refinery margins, sulfur spreads, regional inventories, freight disruptions, sanctions and local port availability. Price volatility increases the value of hedging, indexed contracts and digital bunker intelligence.

Procurement Pressure

Shipowners and charterers face pressure to reduce delivered fuel cost while proving emissions compliance. This creates demand for suppliers that can provide reliable delivery, transparent pricing, strong documentation and credit support.

New Technology Adoption

AI and digital analytics are entering bunker fuel procurement through voyage consumption forecasting, speed optimization, route planning, bunker price prediction and supplier performance monitoring.

Regional Expansion Opportunity

Asia-Pacific remains the largest hub base, Europe leads compliance-driven fuel transition, North America is expanding LNG and methanol infrastructure and the Middle East is using Fujairah and Oman to strengthen regional fuel security.

Government Policy Support

Policy support is concentrated around green corridors, low-carbon fuel incentives, port decarbonization and maritime emission reduction frameworks. These policies are creating demand for alternative fuel supply agreements and bunkering infrastructure.

Pricing Intelligence

Bunker procurement increasingly uses hub benchmarks such as Singapore, Rotterdam, Fujairah, Houston and Zhoushan. Buyers compare delivered price, sulfur spread, lead time, credit cost and deviation cost before lifting fuel.

AI Impact Analysis

AI can improve fuel procurement by forecasting consumption under different speed, weather and route conditions. Machine learning studies show strong potential for predicting ship fuel consumption using voyage reports, climate data and sea-state inputs.

Disruption Analysis

The disruption is the transition from commodity fuel supply to a data-rich, compliance-heavy and multi-fuel procurement ecosystem. The winners will be suppliers that combine fuel availability, delivery reliability, compliance documentation and digital tools.

HS Code Reporter Trade Flow

| HS Code | Reporter | Trade Flow | 2025 Trade Value | Interpretation |

| 2710 | Singapore | Import / Re-export | High | Major bunkering hub with large marine fuel inflows and high bunker sales volume. |

| 2710 | China | Export / Domestic Supply | High | Large LSFO and bonded bunker fuel supply base supporting Zhoushan, Shanghai and other Chinese ports. |

| 2710 | Netherlands | Import / Export | High | Rotterdam remains a key European fuel trading, storage and blending hub. |

| 2710 | UAE | Export / Bunkering | High | Fujairah is a major Middle East bunker and oil storage hub for ships transiting the Indian Ocean. |

| 2710 | United States | Domestic Supply / Export | Medium-High | Gulf Coast refining and Houston bunkering support tanker, container and cruise fuel demand. |

Bunker Fuel Market Dynamics

Driver Impact Analysis

| Driver | Market Growth Impact (%) | Demand Concentration | Impacted Use Case | Strategic Impact |

| Global Seaborne Trade and Route Complexity | 24% | Asia-Pacific, Europe | VLSFO, MGO and LNG Supply | Sustains fuel demand and raises value of hub availability and route planning. |

| IMO and EU Emissions Regulations | 23% | Europe, Global Fleet | Low Sulfur and Alternative Fuels | Accelerates fuel switching, documentation and carbon intensity reporting. |

| Growth of Dual-Fuel Vessel Orderbook | 19% | Container, Gas Carrier, Cruise | LNG and Methanol Bunkering | Creates long-term fuel demand commitments at ports with alternative fuel infrastructure. |

| Digital Bunker Procurement and Voyage Optimization | 15% | Global | Spot and Contract Procurement | Improves price visibility, reduces consumption and supports supplier benchmarking. |

| Port Infrastructure Expansion | 14% | Singapore, Rotterdam, Fujairah, Houston, Zhoushan | Physical Bunkering | Improves delivery reliability and increases hub competitiveness. |

Driver: Compliance-Grade Fuel Demand and Alternative Fuel Optionality

A major driver for the Bunker Fuel market is the need to operate vessels under increasingly strict emissions rules while keeping voyage economics competitive. VLSFO and MGO remain essential for sulfur compliance, while HSFO remains relevant for scrubber-equipped vessels. LNG, biofuel blends and methanol are gaining attention because shipowners want fuel optionality before long-term regulatory costs become fully visible. IMO’s Net-Zero Framework for large ships above 5,000 gross tonnage strengthens the business case for fuel transition planning because it links fuel choice directly to emissions intensity and potential pricing exposure.

Restraint Impact Analysis

| Restraint | Drag on Market Growth (%) | Primary Impact Area | Impacted Use Case | Strategic Impact |

| Alternative Fuel Infrastructure Gaps | 21% | Port Supply | LNG, Methanol and Biofuel Bunkering | Limits real fuel switching despite vessel readiness. |

| Fuel Price Volatility | 18% | Procurement | Spot Bunker Buying | Increases voyage cost risk and pushes buyers toward hedging and indexed contracts. |

| Fuel Quality and Compatibility Risk | 16% | Operations | VLSFO, Biofuel Blends, Methanol | Creates engine risk, claims disputes and need for stronger testing. |

| Regulatory Uncertainty and Documentation Burden | 15% | Compliance | Carbon Reporting and Alternative Fuels | Raises administrative cost and slows adoption of new fuels. |

| Refinery and Supply Concentration | 11% | Supply Security | Regional Bunker Availability | Creates localized tightness and delivery delays. |

Restraint: Alternative Fuel Supply is Still Lane-Specific

The main restraint is that alternative fuel availability is highly uneven by trade lane. LNG has moved beyond the pilot stage, but still depends on port access, bunker vessel availability and engine compatibility. Methanol is scaling through container vessel commitments, but actual bunkering capacity remains limited to a smaller number of ports. Biofuel blends can use existing infrastructure in many cases, but sustainable feedstock availability, certification and price spreads limit widespread use. Buyers therefore need port-by-port intelligence rather than broad fuel category assumptions.

Bunker Fuel Market Segmentation Analysis

The global Bunker Fuel market is segmented by fuel type, vessel type, distribution channel, buyer segment, procurement model, compliance category and region. Each segmentation reflects a different buyer decision point. Fuel type determines compliance and engine compatibility. Vessel type determines consumption intensity and fuel flexibility. Distribution channel determines supply reliability. Procurement model determines price exposure. Compliance category determines carbon reporting and fuel documentation burden.

By Fuel Type: VLSFO and Low Sulfur Marine Fuels Continue to Lead Compliance-Grade Demand

VLSFO remains the largest mainstream fuel category because most vessels need sulfur compliant fuel and many do not operate with scrubbers. Buyers evaluate VLSFO based on availability, delivered price, stability, viscosity, catalytic fines and compatibility with onboard fuel management systems. HSFO remains important where scrubbers are installed because the HSFO-VLSFO spread can create meaningful savings. MGO and LSMGO are essential for emission control areas, ports and vessels requiring distillate fuels. LNG is the fastest growing transition fuel category because the 2026 fleet base includes roughly 800 LNG-capable vessels in service and 600 on order, supported by bunkering availability across 222 ports. Biofuel blends and methanol remain attractive for emissions reduction but require stronger supply certification and port readiness.

By Vessel Type: Container Ships, Bulk Carriers and Tankers Drive the Core Consumption Base

Container vessels represent a high-value bunker fuel demand base because they run scheduled services, require predictable bunker planning and are often first movers in alternative fuel adoption. Bulk carriers and tankers remain volume-critical because they operate across long-haul routes and consume large quantities of fuel. Tankers are also exposed to geopolitical route changes and fuel quality requirements across major oil trading routes. Cruise vessels require high reliability, low emissions at port and strong supplier service standards. Offshore support vessels create specialized demand near oil and gas operating regions, where fuel delivery reliability is tied to offshore logistics and production continuity. Buyer intent varies by vessel class, with container lines prioritizing route-based fuel strategies and bulk operators focusing more on cost and availability.

By Distribution Channel: Independent Traders and Integrated Suppliers Compete on Coverage, Credit and Risk Management

The bunker distribution ecosystem includes oil majors, integrated marine fuel suppliers, independent bunker traders, local physical suppliers and digital procurement platforms. Oil majors and integrated suppliers compete through product reliability, port coverage, alternative fuel capability and balance sheet strength. Independent traders compete through flexibility, relationships, credit support and the ability to source across multiple ports. Physical suppliers control local delivery assets such as barges, terminals and storage tanks. Digital platforms are gaining attention because they improve price visibility, purchase governance and documentation tracking. Buyers increasingly combine multiple channel types to reduce supply risk. The strongest suppliers will be those that can provide reliable fuel, fast confirmation, transparent pricing, credit flexibility and claims support.

By Buyer / End User: Shipowners and Charterers Are Shifting Toward Risk-Managed Fuel Procurement

Shipowners, charterers, fleet operators, cruise operators, offshore vessel owners and logistics companies have different procurement priorities. Shipowners focus on engine compatibility, long-term fuel strategy and compliance cost. Charterers focus on voyage economics, bunker adjustment factors and delivered fuel price. Fleet operators prioritize multi-port supply, digital documentation and price risk management. Cruise operators focus on low emissions near ports, supplier reliability and passenger-facing sustainability commitments. Offshore oil and gas operators focus on fuel availability near production basins and support vessel reliability. The market is shifting from transactional procurement to data-driven buying, where fuel choice is linked to freight contracts, emissions obligations, route risk and vessel technology.

By Procurement Model: Index Linked Contracts and Long-Term Supply Agreements Gain Relevance

Spot procurement remains common because bunker prices fluctuate daily and buyers often optimize around port calls. However, volatility and regulatory complexity are pushing larger buyers toward index linked contracts, forward purchasing, hedging and long-term supply agreements. Alternative fuels require even more structured procurement because suppliers need demand visibility to justify infrastructure investments. Green fuel offtake agreements are emerging for biofuels, methanol and LNG-linked low-carbon supply. Buyers are increasingly using procurement models that combine spot flexibility with contract security. The actionable insight is that suppliers should segment customers by fuel risk maturity. Small operators may remain spot-focused, while large fleets need indexed pricing, carbon documentation and supply assurance across specific trade lanes.

By Compliance Category: IMO, EU ETS and FuelEU Maritime Create a New Compliance-Based Segmentation

The market is increasingly segmented by compliance exposure. Ships trading into Europe face EU ETS and FuelEU Maritime obligations, while global deep-sea vessels face IMO decarbonization rules. Vessels operating in emission control areas need lower sulfur and lower particulate fuels. Ships with scrubbers can continue using HSFO where permitted, but they remain exposed to port restrictions and washwater rules. Dual-fuel vessels need compliant fuels plus infrastructure availability. Bunker suppliers that can provide proper documentation, certification and emissions data will gain buyer preference. Compliance segmentation will become more important than traditional fuel type alone because two buyers purchasing the same fuel may have different reporting, cost and route exposure depending on vessel size, geography and charter terms.

By Bunkering Hub Type: Global Hubs Win Through Volume, Multi-Fuel Readiness and Dispute Control

Bunker hubs can be segmented into global mega hubs, regional hubs, transit hubs, offshore energy hubs and emerging green corridors. Singapore leads through scale, with 56.77 million tonnes of marine fuel sales in 2025. Rotterdam, Fujairah, Houston and Zhoushan remain strategically important because of trade lane position, storage, blending and supplier concentration. Emerging alternative fuel hubs are competing through LNG, biofuel and methanol capabilities. Buyers prefer hubs with transparent pricing, prompt delivery, low congestion, reliable sampling and strong dispute resolution. Hub competitiveness increasingly depends on multi-fuel readiness, because dual-fuel vessels need assurance that LNG, methanol or certified biofuel blends are available at predictable ports. Ports that combine conventional fuel reliability with green fuel optionality will capture long-term growth.

Bunker Fuel Market Geographical Penetration

Asia-Pacific leads the Bunker Fuel market due to its position in global manufacturing, container shipping, shipbuilding and major bunkering hubs. Europe is the fastest growing region because regulation is forcing faster adoption of low-carbon fuel strategies and digital documentation. North America is becoming more important for LNG and methanol infrastructure. The Middle East remains critical through Fujairah, Oman and Red Sea route exposure. South America and Africa are smaller but strategically important for biofuel supply, offshore support vessels and regional cargo trades.

Asia-Pacific Bunker Fuel Market Landscape

Asia-Pacific is the largest regional market because it includes Singapore, China, South Korea, Japan, India, Malaysia and Indonesia, all of which are linked to dense trade lanes and high port call activity. Singapore sold 56.77 million tonnes of marine fuel in 2025, confirming its role as the global benchmark hub for bunker volume, pricing, fuel quality and alternative fuel trials. China is increasing its bonded bunker fuel position through Zhoushan, Shanghai and other coastal hubs, with April 2026 reports showing bonded bunker sales growth due to LSFO supply and competitive pricing. The region’s buyer intent is concentrated around supply reliability, short lead times, competitive delivered pricing and access to LNG, biofuel and methanol pilots.

Singapore Bunker Fuel Market Outlook

Singapore remains the most important bunker fuel hub globally. Its 2025 marine fuel sales of 56.77 million tonnes provide a strong demand signal for port authorities, suppliers, testing companies and digital procurement platforms. The hub is also central to alternative fuels because Singapore supports LNG bunkering, biofuel blends and methanol readiness. Buyers use Singapore as a pricing and quality reference because the port combines high supplier density, regulated bunker delivery, fuel testing and digitalization. Future growth will depend on maintaining conventional fuel reliability while adding low-carbon fuels with proper certification and safe handling procedures.

China Bunker Fuel Market Trends

China is strengthening its bunker fuel position through LSFO supply, bonded bunkering, port infrastructure and shipbuilding linkages. Zhoushan and Shanghai are increasingly important for international vessels, while Sinopec’s Global Bunkering Business Centre launch in April 2026 signals a stronger push toward coordinated global service. China’s bunker opportunity is supported by domestic refining capacity, coastal trade and large export-oriented manufacturing flows. Methanol bunkering is also gaining relevance, with Chinese suppliers and port operators participating in green methanol supply chain development. Buyer interest is centered on competitive pricing, LSFO availability, reliable delivery and support for methanol-ready vessels.

Europe Bunker Fuel Market Outlook

Europe is the fastest growing region because fuel procurement is directly affected by EU ETS, FuelEU Maritime, alternative fuel corridors and port decarbonization policies. Rotterdam remains one of the world’s most important fuel storage, blending and trading hubs. European buyers are more likely to ask for emissions documentation, sustainable biofuel certification and carbon cost calculations. Biofuel bunkering, LNG and methanol supply are growing in selected ports, but availability remains lane-specific. European procurement teams increasingly evaluate fuel on a total compliance cost basis rather than only delivered price.

North America Bunker Fuel Market Outlook

North America is a strategically important bunker market through Houston, New York, Los Angeles, Long Beach, Vancouver and Gulf Coast ports. Demand comes from containers, tankers, cruise vessels, offshore support vessels and inland marine operations. The Port of Houston achieved a first ship-to-ship methanol bunkering milestone in 2026, showing that North America is moving from discussion to execution in alternative marine fuels. The Gulf Coast has strong refinery, LNG and petrochemical infrastructure, making it a key area for future LNG and methanol bunker supply. Buyers in North America focus on reliable port availability, regulatory compliance, weather resilience and fuel quality.

Middle East and Africa Bunker Fuel Market Outlook

The Middle East is anchored by Fujairah, one of the world’s major bunker and oil storage hubs. The region benefits from proximity to crude supply, refinery output and Indian Ocean trade lanes. Oman is emerging as a potential LNG bunkering hub through the Marsa LNG project, which has been framed as a Middle East LNG bunkering platform. Africa is smaller but important for West African offshore operations, South African route diversions and longer voyages around the Cape of Good Hope during Red Sea disruption. Buyer demand in this region centers on availability, geopolitical risk management and port lead times.

South America Bunker Fuel Market Outlook

South America’s bunker fuel opportunity is linked to Brazil, Argentina, offshore oil operations, grain exports, iron ore shipments and regional coastal shipping. Brazil is strategically important because Petrobras is active in bio-bunker fuel supply, including a 2026 agreement to supply B24 bio-bunker fuel blend to Odfjell with deliveries from Rio Grande. This shows how South America can participate in the market through low-carbon feedstock and port-based blending, even if total bunker volume remains smaller than Asia-Pacific or Europe. Buyer intent centers on reliable availability, biofuel certification, export corridor support and price competitiveness.

Bunker Fuel Market Competitive Landscape

- Competition is moving from conventional fuel supply toward multi-fuel services that include VLSFO, HSFO, MGO, LNG, biofuel blends and methanol readiness.

- Large integrated energy companies compete through global supply coverage, refinery access, LNG capability and balance sheet strength.

- Independent bunker traders compete through flexibility, credit support, port relationships and ability to source niche fuels across many locations.

- Port-based physical suppliers are gaining value where they control barges, terminals, blending assets and local delivery windows.

- Digital platforms are increasing competitive pressure by improving price transparency, supplier comparison and documentation management.

- Alternative fuel partnerships are becoming a key differentiator because shipowners need confidence that fuel will be available on recurring lanes.

Key Companies of Bunker Fuel Market

- Shell Marine

- TotalEnergies Marine Fuels

- BP Marine

- ExxonMobil Marine Fuels

- Chevron Marine Products

- PetroChina International

- Sinopec Fuel Oil Sales

- CHIMBUSCO

- Bunker Holding

- World Fuel Services

- TFG Marine

- Vitol

- Gunvor Group

- KPI OceanConnect

- Monjasa

- Minerva Bunkering

- Peninsula

- ENOC

- Marubeni

- Petrobras

Bunker Fuel Market Major Pain Points

- High exposure to oil price volatility and sudden regional price spreads.

- Localized fuel availability tightness for VLSFO, HSFO and LSMGO in specific ports.

- Fuel quality risk, including instability, off-spec sulfur, catalytic fines and contamination.

- Limited alternative fuel availability outside major hubs and selected green corridors.

- Regulatory documentation burden for EU ETS, FuelEU Maritime, IMO reporting and sustainability claims.

- Credit risk and counterparty exposure in bunker procurement.

- Operational risk from delayed bunker delivery, port congestion and weather disruption.

- Uncertainty around which alternative fuel pathway will scale fastest across each trade lane.

Bunker Fuel Market Recent Developments

- April, 2026: Sinopec Fuel Oil Sales Co. Ltd. officially launched China’s first Global Bunkering Business Centre to coordinate enquiries, quotations, bunker deliveries, contract execution and after-sales support for global shipowners.

- April, 2026: CHIMBUSCO completed its first ship-to-ship green methanol bunkering operation at Ningbo Port, strengthening China’s methanol bunkering capability for large methanol dual-fuel vessels.

- April, 2026: Singapore, Los Angeles and Long Beach renewed their Green and Digital Shipping Corridor MoU during Singapore Maritime Week, supporting the next phase of alternative fuel trials and port digitalization.

- February, 2026: Petrobras agreed to supply B24 bio-bunker fuel blend to Odfjell, with supply from Rio Grande Terminal and up to 12,000 metric tonnes planned throughout 2026.

- January, 2026: Vopak supported a green methanol bunkering supply chain from China to Singapore, with Singapore methanol bunkering licensing valid from January 1, 2026 for five years.

- May, 2026: CMB.TECH increased its stake in TFG Marine from 10% to 15% and committed bunker fuel requirements for its fleet and affiliates through the joint venture from June 1, 2026.

Analyst View / Opinion on Bunker Fuel Market

- The bunker fuel market is shifting from a volume and price-led trading market to a compliance, infrastructure and risk-managed procurement market.

- VLSFO will remain the core compliance fuel through the forecast period, but LNG, biofuel blends and methanol will account for the strongest strategic growth layer.

- The next phase of competition will be defined by port coverage, multi-fuel capability, documentation quality, supply reliability and digital procurement support.

- Companies with integrated supply, alternative fuel partnerships and strong credit capability will outperform commodity-only bunker suppliers.

- Ports that can combine conventional fuel reliability with LNG, biofuel and methanol readiness will become preferred bunkering hubs for dual-fuel fleets.

- Long-term market leadership will depend on the ability to convert regulatory pressure into practical fuel solutions that shipowners can use on real trade lanes.

Bunker Fuel Market Target Audience

| Industry | Who Should Buy This Report? | Reason To Buy This Report |

| Bunker Suppliers | Physical suppliers, fuel traders, integrated marine fuel teams | To understand demand by fuel grade, port hub, vessel type and procurement model. |

| Shipowners and Operators | Fleet managers, procurement heads, technical managers | To assess fuel availability, price risk, compliance exposure and alternative fuel readiness. |

| Charterers and Logistics Firms | Cargo owners, chartering teams, freight procurement teams | To understand bunker adjustment factors, fuel risk and low-carbon shipping options. |

| Ports and Terminal Operators | Port authorities, terminal operators, storage companies | To identify infrastructure opportunities in LNG, methanol, biofuel and fuel testing. |

| Oil Majors and Refiners | Marine fuel divisions, refinery planners, trading desks | To evaluate demand shifts from residual fuels to compliant and alternative fuels. |

| Technology Providers | Bunker platforms, fuel analytics firms, AI route optimization companies | To identify growth opportunities in digital fuel procurement and consumption forecasting. |

| Investors and Consultants | Private equity, infrastructure investors, strategy consultants | To screen assets across bunkering infrastructure, low-carbon fuels and procurement platforms. |

Why Choose DATAM?

- Data-driven insights: Detailed analysis of bunker fuel demand, port hub dynamics, fuel grade migration, pricing intelligence and procurement risk.

- Post-purchase support and expert analyst consultations: Clients receive direct analyst access to refine assumptions, validate regional opportunities and support strategy decisions.

- White papers and case studies: Quarterly add-ons can cover LNG bunkering, methanol supply chains, biofuel blending, digital procurement and port decarbonization.

- Annual updates on purchased reports: Clients receive updated market intelligence as regulations, fuel prices and alternative fuel infrastructure evolve.

- Specialized focus on emerging markets: DataM provides specific insights for Asia-Pacific, Middle East, South America and Africa instead of generic global coverage.

- Value of DataM Reports: The report is tailored to buyer questions around fuel choice, port availability, regulatory compliance and investment opportunity.

What DATAM Uniquely Provides

- Detailed 10-year market predictions by fuel type, vessel type, distribution channel, buyer segment, procurement model and region.

- Bunker buyer decision intelligence covering fuel quality, price risk, carbon documentation, supplier selection and port-level availability.

- Regulatory analysis across IMO, EU ETS, FuelEU Maritime, emission control areas and alternative fuel certification.

- Strategic market insights covering AI impact, disruption analysis, BCG Matrix, pricing intelligence, trade flow analysis and investment trends.

- White-space analysis across LNG bunkering, methanol supply chains, biofuel blends, digital procurement, fuel testing and multi-fuel port infrastructure.

- Country-level recommendations for suppliers, shipowners, investors and port authorities.

Questions This Report Answers

- How will bunker fuel demand evolve as seaborne trade slows in 2025 and recovers during 2026-2030?

- Which fuel grades will create the strongest value between VLSFO, HSFO, MGO, LNG, biofuel blends and methanol?

- Which ports are best positioned to win multi-fuel bunkering demand?

- How will IMO and EU regulations reshape fuel procurement, emissions documentation and supplier selection?

- Where are the strongest investment opportunities in LNG bunkering, biofuel blending, methanol infrastructure and digital procurement?

- Which companies are best positioned to capture bunker fuel transition demand and what strategies are they using?