Building Automation Market Overview

As per DMI analysis, the Global building automation market was valued at US$ 117.2 billion in 2025 and is expected to reach US$255.5 billion in 2033, growing at a CAGR of 10.2% during the forecast period (2026-2033).

The global shift toward building automation is being structurally driven by the scale of building energy consumption and the increasing need for efficient, intelligent control of building operations across residential, commercial, industrial, and public infrastructure assets. According to the International Energy Agency, buildings account for ~30% of global final energy consumption and 26% of energy-related CO₂ emissions, making them one of the largest and most addressable sectors for efficiency improvement. This creates a strong economic and regulatory incentive for building owners and operators to adopt automation systems that enable real-time monitoring, control, and optimization of energy and operational performance.

From an infrastructure perspective, the scale of opportunity continues to expand rapidly. The United Nations Environment Programme estimates that global building floor area is expected to double by 2060, equivalent to adding an entire city the size of Paris every week. This expansion spans commercial buildings, residential complexes, industrial

facilities, and public infrastructure, all of which require increasingly sophisticated automation systems to manage energy consumption, operational complexity, and

sustainability requirements.

In addition to new construction, the aging building stock globally is a critical driver for automation adoption. According to Johnson Controls, around 35% of buildings in the EU are more than 50 years old, with 75% classified as energy inefficient by the European Commission. Similarly, in the United States, approximately 68% of office space was built

before 2000, and aging infrastructure could potentially erode up to US$ 500 billion in value by 2029. These factors are accelerating retrofit-driven deployment of building

automation systems to improve energy performance, extend asset life, and maintain asset value.

Energy cost pressure further strengthens the case for automation. According to the International Energy Agency, global electricity demand grew by ~2.5% in 2025, with buildings contributing a significant share. At the same time, the World Bank highlights continued volatility in electricity pricing across regions, increasing the need for real-time monitoring, demand optimization, and energy management at the building level. Finally, the building automation market is being driven by the convergence of energy efficiency requirements, aging infrastructure, regulatory pressure, and digital transformation, positioning automation systems as a foundational layer for modern, sustainable, and intelligent building operations across all asset types.

AI Impact Analysis

AI begins to have an impact on building automation in more subtle yet commercially significant ways. Designing, manufacturing, and servicing products in such a way that leverages AI capabilities such as design optimization, process control, predictive maintenance, quality analysis, and demand sensing is transforming the way the offering is designed, engineered, and serviced after purchase. It results in the emergence of a higher-performance layer within an already existing value chain.

From a buyer perspective, the tangible value proposition will be derived through such applications of AI as reduced wastage, accelerated product cycles, more accurate diagnostics, and lower error rates while operating sophisticated equipment. For suppliers, embedding intelligence into products coupled with performance information provides the ability to establish more sustainable customer relationships than their competitors based purely on hardware specs.

As far as commercialization goes, sales reps may assist their customers in simulation and product configuration while after-sales personnel leverage performance information to better manage renewals, parts, and services..

Building Automation Market Industry Trends and Strategic Insights

- The system segment will remain the most commercially relevant segment due to its depiction of capital deployment, upgrade priority, and assessment of automation value for different control layers within the Building Automation sector.

- Buyers’ focus will be increasingly on operational improvements, with an emphasis on HVAC control, lighting control, and energy management in particular, instead of the wide range of capabilities associated with smart buildings.

- The European continent will continue to dictate trends in terms of standards, retrofitting, sustainability-driven automation investments, and market entry by competitors.

- Leading suppliers will maintain their competitive edge by leveraging technical prowess and strong delivery capacity, through product excellence, specialization, integration ability, and partnership ecosystems to safeguard prices and speed up buying decisions.

Market Scope

| Metrics | Details | |

| 2025 Market Size | US$ 117.2 billion | |

| 2035 Projected Market Size | US$ 255.5 billion | |

| CAGR (2026-2035) | 10.2% | |

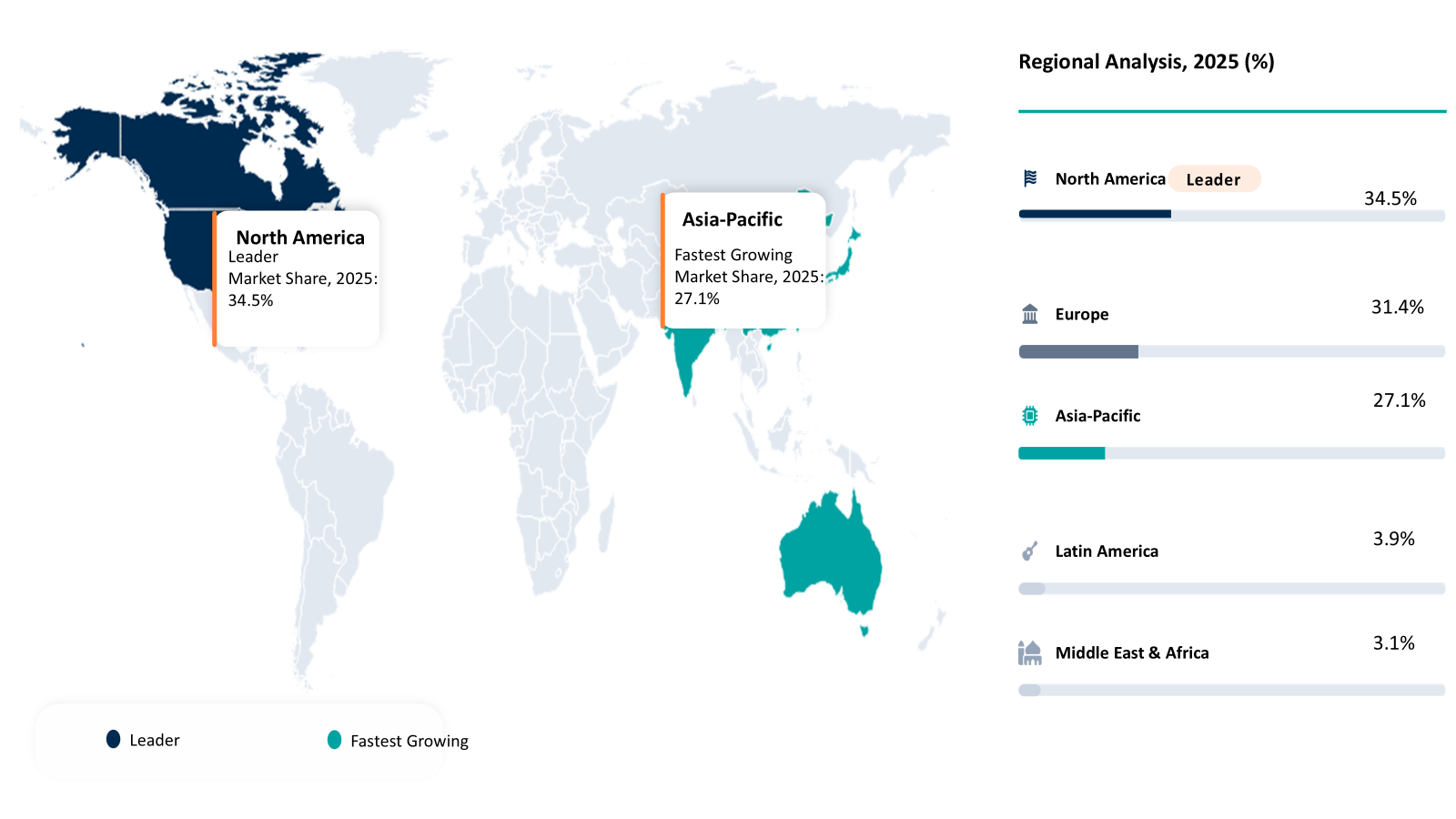

| Largest Market | North America | |

| Fastest Growing Market | Asia-Pacific | |

| By System | HVAC Control, Lighting Control, Security and Access Control, Fire and Life Safety, Energy Management | |

| By Building Type | Commercial Offices, Hospitals, Industrial Facilities, Retail Buildings, Residential Complexes | |

| By Deployment Model | Wired, Wireless, Hybrid | |

| By Offering | Hardware, Software, Services | |

| By End User | Building Owners, Facility Managers, Real Estate Developers, Industrial Operators, Public Infrastructure | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

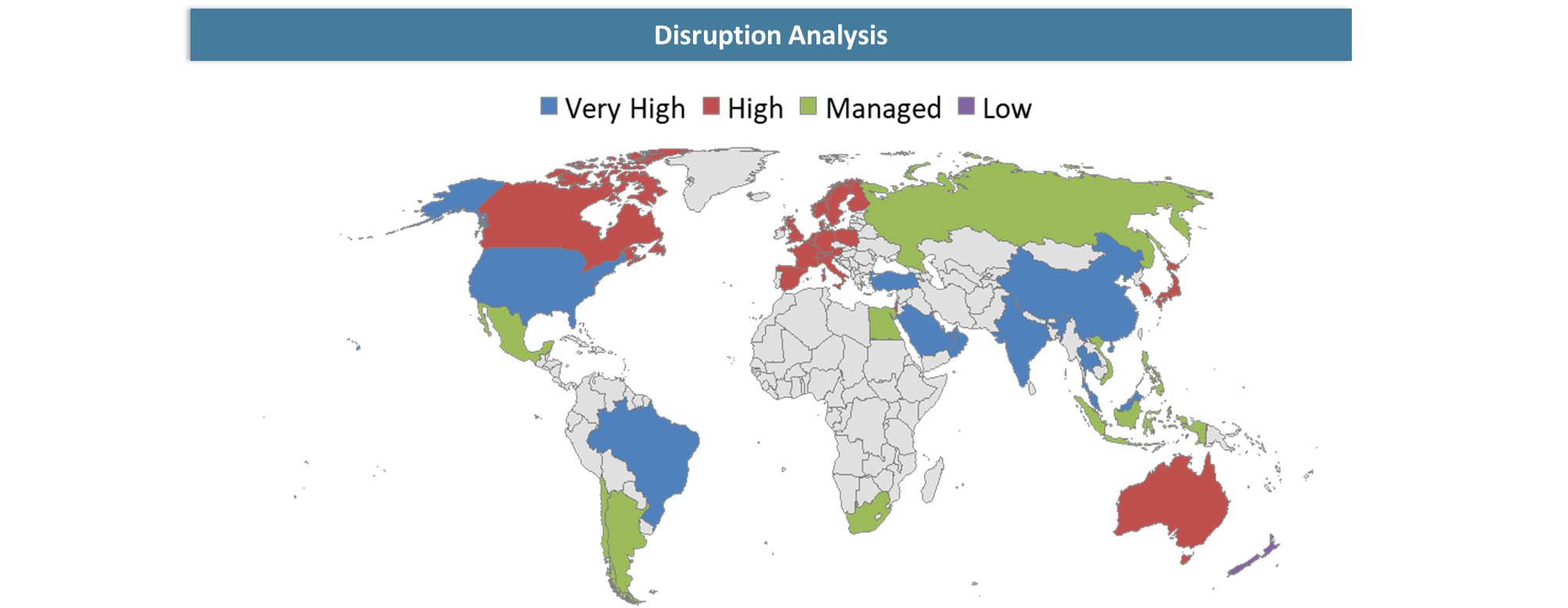

Disruption Analysis

Shift Toward Outcome-Driven Automation and Execution-Led Competition

The primary disruptive force impacting the building automation market is the transition from the paradigm of feature-oriented selling to that of tangible operational benefits. This disruption is based on the reality that buildings represent roughly 30 percent of worldwide final energy use, thereby ensuring that building automation remains firmly anchored to energy, carbon, and monetary results and not merely convenience. In essence, consumers are no longer accepting general assertions regarding smart buildings but are focusing on the potential of systems to save energy in heating, ventilation, air conditioning, and lighting; enhance operational efficiency; and yield an obvious return on investment in current facilities.

The second disruption is being felt through the retrofit reality of the building portfolio, particularly in Europe. According to the European Commission, 85% of buildings in the European Union were constructed before 2000, and 75% of the building stock is poorly performing in terms of energy use, with only 1% of buildings being renovated every year. This has implications for building automation technology, as the future growth drivers will not be entirely on new builds but largely on existing buildings that require a control layer on top of them.

In addition to that, another factor influencing the development of the market is the growing disparity between the rate of implementation of the solutions into large facilities and underpenetrated midsize assets. According to the National Renewable Energy Laboratory, approximately 60 percent of the commercial buildings larger than 50,000 square feet are equipped with BMS technology, while 13 percent of commercial facilities smaller than 50,000 square feet use such a solution. This demonstrates the new battlegrounds in which commercial companies are operating - not only acquiring landmark facilities but making BMS installation and management more accessible for underpenetrated assets.

Cybersecurity and operational resilience present another disruption. The NIST definition of BAS as operational technology that manages HVAC systems, fire systems, lighting, access control, security, and other utility systems indicates that such solutions are not just isolated facilities anymore. With BAS turning into an integrated operational level, consumers now consider cybersecurity and other aspects of vendor performance while choosing partners in the field. Consequently, the market is gradually moving towards vendors who are more focused on execution than innovation branding.

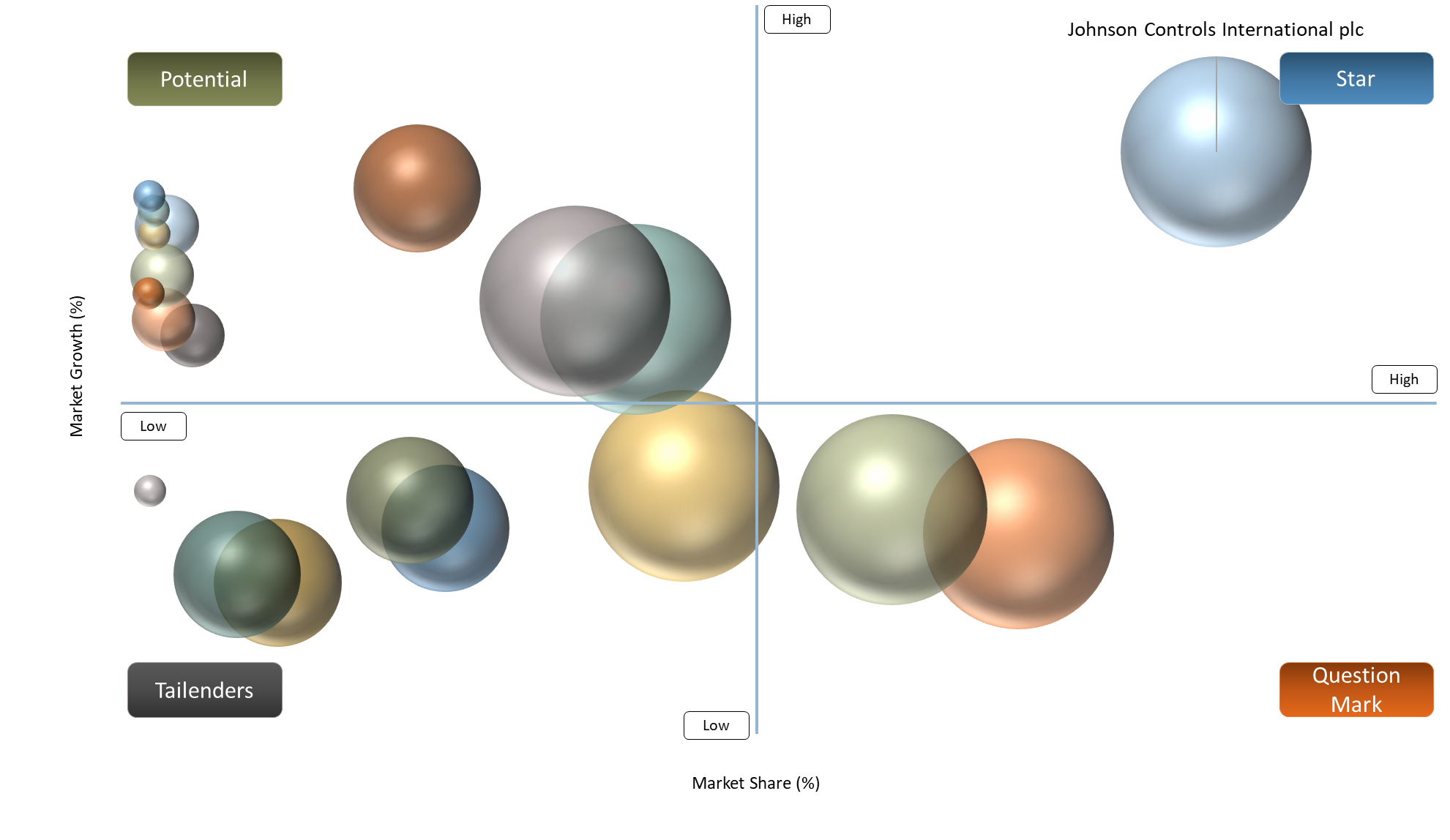

BCG Matrix: Company Evaluation

From the perspective of BCG Strategy Alignment, leaders in the Building Automation sector tend to be vendors with both momentum and control of integration ecosystems. Examples of such include Johnson Controls International plc, Honeywell International Inc., Siemens AG, Schneider Electric SE, and ABB Ltd. These companies have an excellent position if they match their offerings in terms of product depth, integration capabilities, digital platform, and lifecycle support. A second group includes companies such as Carrier Global Corporation, Legrand SA, Delta Electronics, Inc., and Trane Technologies plc. These companies leverage their existing installed base along with their channels to ensure a constant stream of revenue from lifecycle services. Finally, there is a new breed of emerging players and niche vendors including Distech Controls Inc., BuildingIQ, Inc., and KMC Controls, Inc. These players are making headway by focusing on specific applications.

Market Dynamics

Shift Toward Measurable Operating Value and Application-Specific Buying Criteria

The main driver for growth in the building automation industry can be found in the transition from marketing broader concepts around smart buildings to making investments linked to results concerning energy savings, costs, and regulation compliance. With buildings responsible for nearly 30% of energy consumption globally and approximately 26% of greenhouse gas emissions related to energy production and consumption, the connection between automation decisions and energy efficiency remains strong. From a practical perspective, customers increasingly require system capabilities to reduce energy consumption in HVAC and lighting by 10-25%, making return on investment visibility one of the key criteria for choosing suppliers.

The second wave of demand arises from stricter procurement processes. Instead of focusing solely on control capabilities, customers consider integration effort, compatibility with retrofits, cybersecurity preparedness, and validity of savings promises from suppliers. All these considerations become particularly important against the backdrop of a situation when more than 70% of buildings in advanced economies will stay in service until at least 2050. Thus, expenditures are concentrated mainly on areas like HVAC controls and energy management systems.

Ecosystem maturity is also contributing towards market growth. The development of system integration players, energy service providers, and IoT connectivity layers is lowering barriers to entry and enhancing execution certainty. This becomes even more pertinent in an industry where fewer than 15 percent of small and medium commercial buildings have adopted sophisticated automation systems, indicating a sizable opportunity that becomes attainable only when deployment risks are minimized. As enabling infrastructure advances, automation uptake is moving beyond high-end projects into wider, economically sensible building types.

Finally, end-user criteria are becoming more demanding regarding operational relevance and scalability. Users are becoming more selective about non-customizable solutions that necessitate manual input or reengineering following implementation. On the contrary, users are gravitating towards interoperable systems that are easily scalable, capable of integrating with existing infrastructure, and continuously optimized. Gradually, such a criterion is raising the bar on demand for solution providers with robust execution abilities, sector experience, and end-to-end accountability, as well as commercially sound segmentation by system architecture, building category, and application.

Integration Burden, Compliance Friction, and Extended Enterprise Buying Cycles

The most critical constraint facing the building automation industry is that buyer engagement takes longer to turn into implementation compared to what market dynamics would imply. The problem is not about value appreciation but rather the challenge posed by the implementation process of installing automation systems into already-existing buildings. In Europe, for example, about 85% of all buildings are older than 2000, 75% of all buildings perform poorly on energy consumption front, and the annual energy renovation rate is just about 1%.

The problem becomes particularly apparent in markets where retrofit solutions constitute a higher proportion of business volume, compelling suppliers to integrate building automation systems into legacy heating, ventilation, and air conditioning systems (HVAC), energy management, and lighting without disturbing ongoing operations. The same scenario applies to small buildings, where almost 60% of commercial buildings larger than 50,000 square feet use Building Automation Systems (BAS). However, less than 13% of small- and medium-sized commercial buildings with less than 50,000 square feet are using BAS solutions. Such a difference can be attributed to the high costs of installation, integration, validation processes, and delayed enterprise-level decisions.

Segmentation Analysis

The global Building Automation Market is segmented based on the system, building type, deployment model, offering, end user, and region/countries.

System-Led Value Stratification Driving Building Automation Economics

System-level is the most commercially significant prism in the building automation industry due to its direct impact on the allocation of investments relative to operation costs, risks, and regulations. Buildings consume ~30% of the global energy supply, while HVAC systems comprise 40-60% of all buildings' energy expenditure. Hence, decision-making on the system level is crucial both from the perspectives of cost-saving potential and carbon footprint reduction. Indeed, companies do not invest in platforms but rather in concrete improvements that provide tangible benefits, leading to competitive advantages at the system level.

Two different economic strategies are apparent under the current market conditions HVAC control and energy management. The former strategy is associated with early adoption since it corresponds with the preexisting infrastructure and operations, providing energy savings up to 10-20% without high integration risks and offering an average payback period of 2-3 years. As a result, HVAC control can serve as the first step to implementation when retrofits prevail at 70-80% of projects.

On the other hand, Energy Management is another step in value unlock for a different set of customers. Customers get into Energy Management phase where basic efficiencies achieved through controls are no longer enough, and where pressure for regulation, ESG, and portfolio costs become too high. Such solutions allow for further optimization by means of analytics, continuous monitoring, and system integration, and thus involve larger investments, longer adoption phases, and higher contracts, yet they involve partnerships focused on multi-year performance.

What is interesting, though, is that the whole market dynamic is shifting towards layered value proposition, in which control systems provide penetration and volumes for sales, whereas Energy Management solutions capture higher-value demand based on performance optimization. Companies able to orchestrate both levels, and help their customers move from control deployment stage to performance optimization one, will benefit greatly from the trend.

Geographical Penetration

Europe Is Setting the Competitive Tempo for the Building Automation Market

Europe is becoming the benchmark for the building automation market, driven by regulatory pressure, increasing energy prices, and the urgent need for modernization due to aging building stock. EU buildings consume about 40% of total energy consumed and contribute 36% of greenhouse gases emitted by buildings. Meanwhile, 75% of buildings in Europe have been constructed using energy-inefficient technology, but annual energy renovation stands at only 1%. In such a situation, building owners resort to improving building management systems by using automation and control technology without having to renovate buildings completely.

One trend to watch in Europe is proof-based procurement. Instead of general smart-building positioning, buyers will be asking if the technology is able to integrate with existing infrastructure, deliver tangible efficiency savings, and operate within strict performance targets related to energy efficiency. The reason why it is important is that 85% of all EU buildings have been built prior to the year 2000. As a result, compatibility becomes an integral part of the buying decision instead of an ancillary benefit offered by vendors.

Germany requires special consideration since it is a country that represents an example of an environment where the pressure on improving energy efficiency, renovating public buildings, and upgrading municipal infrastructure has become increasingly pressing recently. Based on recent developments and investments in the German building sector, there seems to be increased pressure on municipalities and owners of property requiring renovations and improvements that could contribute to better efficiency. This allows us to conclude that Germany can be regarded as a good indicator of suppliers’ ability to operate under technically challenging conditions.

The general idea is that the European Union can become a benchmark for the future development of the building automation industry in the context of stricter requirements in terms of carbon and energy efficiency. Successful markets in Europe manage to thrive in these conditions because of the suppliers’ ability to meet the needs of existing buildings, government pressure toward improvement, and stricter purchasing criteria. Therefore, when it comes to consulting services, it is important to consider Europe from the perspective of what is yet to come.

Germany Building Automation Market Trends

Germany is becoming one of the most important players in Europe in terms of building automation systems, influenced by heavy industry, expensive energy prices, and efficiency legislation. Buildings consume a large part of the country's energy, and there is growing pressure to reduce energy usage and emissions, which means buildings need to become optimized through automation rather than rebuilt entirely. These factors are driving up demand for HVAC systems control, energy management, and building systems integration that will result in noticeable improvements.

The key feature of the German market is its results-oriented purchasing process. The buying side places a high value on the reliability of solutions, their compatibility with existing infrastructure, adherence to local standards, and reliable performance in operation. The choice of vendors is sometimes based not only on the capabilities of products themselves but also on their integration, expertise and local presence.

Success of any commercial endeavor in the US now depends very much on the strength of the ecosystem. Germany is an example of a transition to an ecosystem-based approach to competition, where system integration specialists, engineering houses, and service partners assume a significant importance for vendor success. Those suppliers who manage to harmonize their products with effective implementation and regulation, as well as lifecycle services, will prove themselves superior to other companies that depend only on their unique technological solution. Therefore, Germany is considered a benchmark of those suppliers capable of scaling in highly disciplined environments.

Netherlands Is Emerging as a Strategic Innovation Market for Building Automation

The Netherlands represents an important market opportunity in the building automation industry thanks to its sustainability aspirations, developed digital technology, and openness to smart-building deployment. The Dutch market is shaping a promising environment for solutions associated with energy optimization, occupant-based controls, building management integration, and service digitization. Consequently, the relevance of the country as a target market increases as far as suppliers consider it as a platform for promoting their more complex products, not just the control ones.

This target market is especially important for strategic analysis because of the quality adoption trends related to commercial and mixed-use real estate properties. Consumers demonstrate a growing interest in the interoperability of systems, which integrates such components as energy management, building analytics, and smart controls under a single operating environment. It creates a good environment for the development of more sophisticated solutions that combine high-level performance, efficiency, and sustainability outcomes in a single package.

Competitive Landscape

- The competition within the building automation industry has become increasingly influenced by a gap between the players that provide a wide platform versus those that focus on applications. Firms like Johnson Controls International plc, Honeywell International Inc., Siemens AG, Schneider Electric SE, ABB Ltd., Carrier Global Corporation, Legrand SA, Delta Electronics, Inc., Bosch Building Technologies GmbH, Trane Technologies plc, Daikin Industries, Ltd., Mitsubishi Electric Corporation, Cisco Systems, Inc., and Signify N.V. are known for their competitive edge based on the width of their offering, reach into the installation base, channel penetration, and capability to handle multi-system buildings.

- On the other hand, manufacturers like Lutron Electronics Co., Inc., Distech Controls Inc., Crestron Electronics, Inc., KMC Controls, Inc., Automated Logic Corporation, and BuildingIQ, Inc. may fortify their standing via product depth, speed of implementation, alignment with applications, or better capabilities of controlling and optimizing. Consequently, the industry cannot be assessed solely on which one has a broader range of products, but on the ability to protect the entire customer journey from planning and implementation to analysis, support, and results following implementation. Manufacturers capable of creating stronger positions within HVAC Control and Energy Management Systems tend to have easier times maintaining prices, deepening business connections, and increasing market share.

Key Developments

- April 2025 -Johnson Controls highlighted the economic case for its OpenBlue platform through a Forrester Total Economic Impact study, reinforcing its position around measurable efficiency, cost savings, and building-performance outcomes rather than stand-alone controls messaging.

- November 2024 - Johnson Controls expanded AI features in OpenBlue, including enhanced autonomous controls and simplified workflows, showing a stronger push toward lower manual intervention and smarter building operations.

- June 2025 - Honeywell launched Honeywell Connected Solutions, an AI-powered platform integrating critical building software and technologies into a single interface, strengthening its commercialization around unified building operations and energy management.

- May 2025 - Honeywell was selected as the building automation provider for LG Energy Solution’s North American EV battery plant, underscoring its traction in large-scale industrial and mission-critical facilities.

- March 2024 - Siemens used Light + Building 2024 to showcase new products, software, services, and partnerships under its smart infrastructure portfolio, reinforcing its strategy around integrated building ecosystems rather than isolated components.

- March 2024 - Siemens also advanced Building X with release enhancements focused on streamlined operations, stronger security, and improved sustainability tracking, supporting its positioning in digital building operations.

- December 2024 - Schneider Electric introduced EcoStruxure Building Activate for small and mid-size buildings, signaling a stronger push into easier-to-deploy automation for underpenetrated assets with stated payback of less than two years.

- May 2025 - Schneider Electric launched its Impact Buildings Program in Dubai, showing how it is using reference sites to demonstrate integrated energy and automation performance in real operating environments.

- February 2025 - ABB announced the integration of its InSite energy management system into Samsung SmartThings and SmartThings Pro, strengthening its position in connected energy management and smart building interoperability.

- July 2024 - Bosch Building Technologies stated plans for further growth in the building automation sector, indicating a clearer strategic emphasis on expanding its role in automation-led building solutions.

- January 2025 - Trane Technologies completed the acquisition of BrainBox AI, adding autonomous HVAC controls and generative AI building technology to deepen its energy optimization and intelligent building capabilities.

White Space Opportunities

DataM identifies an area of white space in enterprise AI agents beyond some of the most obvious avenues in procurement processes. While many companies continue to chase down big name accounts, there can be underpenetrated customer demand in niche spaces for highly specialized use cases in which trustworthiness and implementation ease are valued more than sheer size. It is typically more difficult to construct an effective business case around pure breadth of reach rather than solution packages that address specialized needs and their deployment.

The second white space opportunity is not in technology but rather in commercial packaging. Suppliers that make it easy for clients to buy, implement, and use their technologies stand a much better chance of success than companies focused merely on broad reach. This is because buyers do not necessarily need to see evidence of cutting-edge capabilities in order to derive value from an AI agent product but rather orchestration capability and workflow compatibility.

DMI Opinion

As per DataM, the enterprise AI agent market is no longer defined by the creation of demand, but by how effectively suppliers can turn interest into sustainable revenue without increasing the deployment difficulty for customers beyond their value. Enterprise buyers have become more interested in tightly regulated task agents that will meet the company's permissions and audit requirements, as well as align its workflows and escalations. Under these circumstances, competitive strength comes not through visibility or breadth of offerings, but through credibility, fit, and performance.

As per DataM, most vendors in the marketplace are focused on capabilities of models rather than recognizing the significant role played by orchestration, tooling, life-cycle management, and training in driving adoption and revenue. As a result, enterprise customers are finding the greatest success in more limited use-cases, including support workflows, operations coordination, and enterprise services where ROI can be easily demonstrated. Consequently, the enterprise AI agent market should be viewed as a precision-execution strategy opportunity, as suppliers who lower adoption costs and maximize business impact will be best positioned to succeed.

Why Choose DataM?

- Technological Developments: Deals with advancements like HVAC control systems, lighting automation, energy management solutions, access control technologies, sensor devices, artificial intelligence, IoT systems, cloud computing, digital twins, and predictive analytics.

- Market Positioning of Major Competitors: Provides market positioning of major players on the basis of integration capabilities, scalability, interoperability, analytics, services, and compatibility for diverse applications.

- Application Scope of Building Automation Market: Discusses applications including HVAC systems, lighting automation, energy management, access control, occupancy-based automation, and facility management.

- Market Trends & Dynamics: Focuses on market trends such as increased use of smart buildings, retrofit requirements, carbon neutrality focus, AI-driven analytics, interoperability, and regional dynamics.

- Competitive Strategies: Provides an analysis of competitive strategies such as platform expansion, ecosystem approach, services-first model, enhanced interoperability, and application-specific solutions.

- Market Pricing & Accessibility: Discusses factors such as project-based pricing, subscription services, implementation costs, integration costs, maintenance costs, and regulations affecting market entry.

- Market Penetration & Growth Opportunities: Discovers expansion opportunities in terms of retrofits, mid-market segment, regional expansion, partnerships, and scalable services approach.

Target Audience 2026

- Product strategy teams

- Corporate strategy and market intelligence teams

- Business development leaders

- Sales and channel leaders

- Investors and private equity firms

- Procurement and sourcing teams

- Technology and operations leaders

- Consulting and advisory teams.