Bioprinting & Tissue Engineering Devices Market Size & Industry Outlook

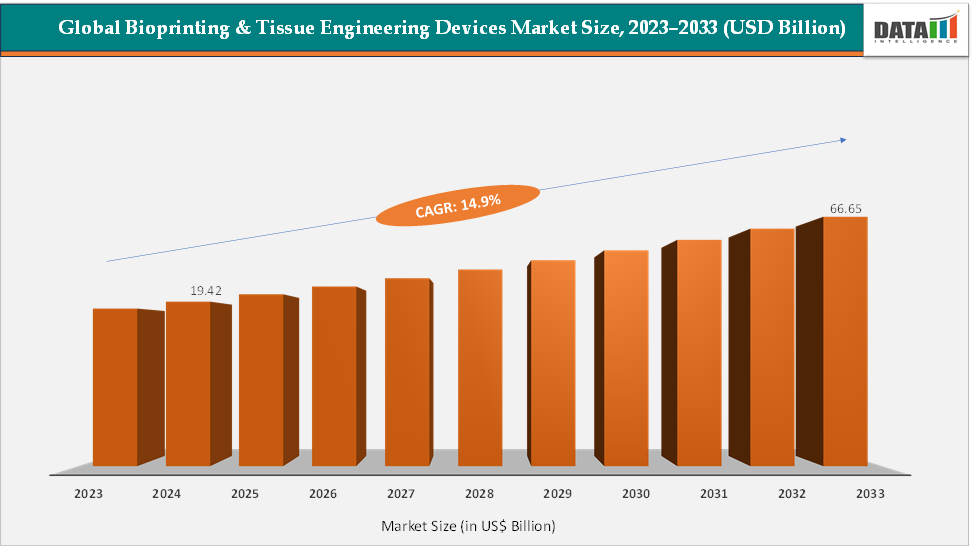

The global bioprinting & tissue engineering devices market size reached US$ 19.42 Billion in 2024 from US$ 17.08 Billion in 2023 and is expected to reach US$ 66.65 Billion by 2033, growing at a CAGR of 14.9% during the forecast period 2025-2033. The market is experiencing rapid growth due to rising demand for regenerative medicine, personalized healthcare, and advanced drug testing models. Continuous innovations in bioinks, printing technologies, and automation have enhanced tissue reproducibility and scalability. Growing adoption of bioprinted tissues for pharmaceutical research, reduced animal testing, and supportive regulatory initiatives are further accelerating market expansion. Additionally, strong collaborations between biotech firms and research institutions are fueling technological advancements and commercialization in this field.

Key Market Highlights

- North America dominated the bioprinting and tissue engineering devices market with the largest revenue share of 42.87% in 2024.

- The Asia Pacific is the fastest-growing region and is expected to grow at the fastest CAGR of 14.7% over the forecast period.

- Based on application, the tissue engineering & regenerative medicine segment led the market with the largest revenue share of 34.04% in 2024.

- The major market players in the bioprinting & tissue engineering devices market are CELLINK, 3D Systems, Inc., CollPlant Biotechnologies Ltd., Organovo Holdings Inc., Regemat 3D, regenHU, CYFUSE BIOMEDICAL K.K., Poietis Biosystems, and ARTBioprint, among others

Market Dynamics

Drivers: Organ and tissue shortages are significantly driving the bioprinting & tissue engineering devices market growth

Organ and tissue shortages are a significant driver of the bioprinting and tissue engineering devices market, spurring advancements in regenerative medicine and personalized healthcare solutions. The global demand for organ transplants far exceeds supply, with over 121,000 individuals awaiting organ transplants in the United States alone, and approximately 17 people dying each day while waiting for a life-saving organ. This crisis has led to a surge in research and development efforts focused on creating viable alternatives to traditional organ transplantation.

Bioprinting technologies enable the fabrication of complex, three-dimensional tissue structures using living cells, biomaterials, and growth factors. These advancements hold the potential to revolutionize organ transplantation by providing customized, patient-specific tissue constructs that can integrate seamlessly with the recipient's body, reducing the risk of immune rejection and eliminating the need for donor organs.

The pressing issue of organ and tissue shortages is a pivotal factor propelling the bioprinting and tissue engineering devices market forward, by offering hope for patients in need of organ transplants and paving the way for the future of personalized medicine.

Restraints: Regulatory challenges for clinical translation are hampering the bioprinting & tissue engineering devices market growth

Regulatory challenges for clinical translation are significantly hampering the growth of the bioprinting & tissue engineering devices market. Since bioprinted tissues combine living cells, biomaterials, and device components, they do not fit neatly into existing regulatory categories of medical devices, biologics, or combination products, leading to complex and prolonged approval processes. The US FDA and EMA have yet to establish standardized pathways for evaluating the safety, efficacy, and reproducibility of bioprinted organs, causing uncertainty for developers and investors. Companies like Organovo and Poietis have faced delays in bringing bioprinted therapeutic tissues to market, highlighting how evolving yet inconsistent regulatory frameworks can slow commercialization. This lack of clear guidance increases development costs, prolongs timelines, and limits broader clinical adoption of bioprinting technologies.

Additionally, the absence of standardized manufacturing protocols and quality control measures for bioinks and scaffolds challenges compliance with Good Manufacturing Practice (GMP) and Good Laboratory Practice (GLP) requirements, essential for ensuring product safety and efficacy. These regulatory hurdles not only delay the progression of bioprinted devices from laboratory settings to clinical applications but also increase development costs, thereby slowing market growth and limiting patient access to potentially transformative therapies.

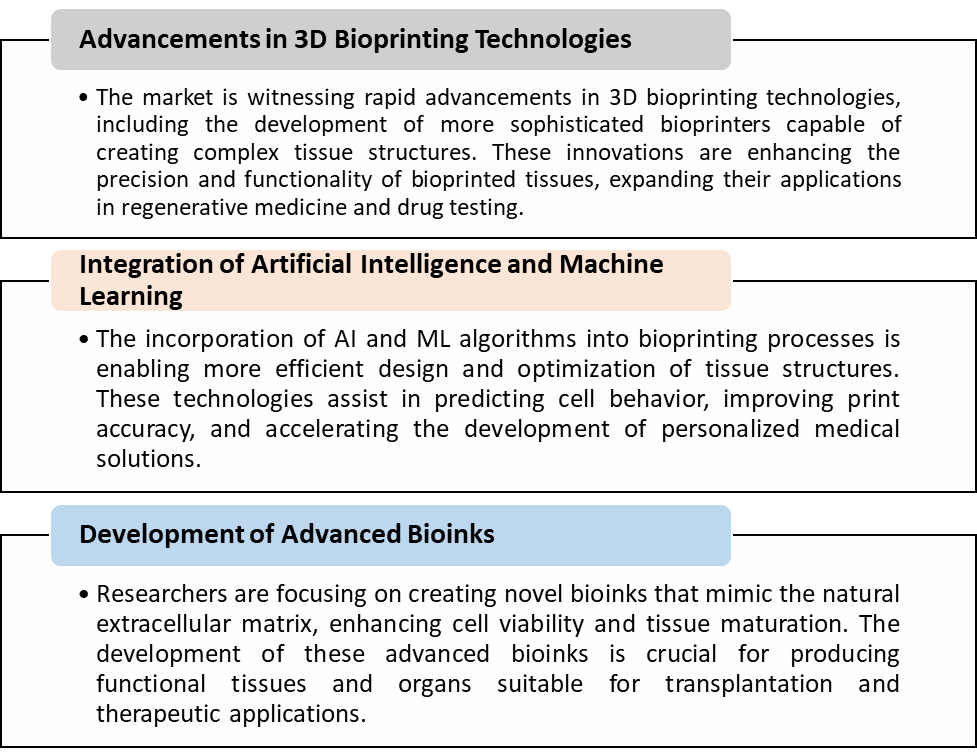

Emerging Trends and Strategic Opportunities:

For more details on this report – Request for Sample

Bioprinting & Tissue Engineering Devices Market, Segmentation Analysis

The global bioprinting & tissue engineering devices market is segmented based on product type, material, application, end-user, and region.

Application: The tissue engineering & regenerative medicine segment is dominating the bioprinting & tissue engineering devices market with a 34.04% share in 2024

Based on application, the tissue engineering & regenerative medicine segment is dominating the bioprinting & tissue engineering devices market due to its direct impact on clinical applications and unmet medical needs. This segment focuses on creating patient-specific tissues, grafts, and implants that can replace or repair damaged organs, addressing conditions such as chronic wounds, cartilage degeneration, and organ failure. FDA-approved products like Apligraf and Dermagraft have already demonstrated clinical viability for skin regeneration, paving the way for advanced bioprinted constructs.

Companies such as Organovo (with its exVive liver tissues), CELLINK/BICO, and 3D Systems are spearheading innovations in bioprinted cartilage, bone, and skin tissues. Moreover, the growing shortage of donor organs and ageing populations in developed regions amplify the need for functional, implantable tissues. With strong clinical adoption potential, high-value applications, and accelerating R&D investments, the tissue engineering and regenerative medicine segment continues to lead the market’s growth trajectory.

The drug discovery, development & toxicology testing segment is the fastest-growing segment in the bioprinting & tissue engineering devices market, with a 23.78% share in 2024

The drug discovery, development & toxicology testing segment is emerging as the fastest-growing area in the bioprinting & tissue engineering devices market, driven by the pharmaceutical industry’s increasing shift toward human-relevant 3D tissue models. Bioprinted tissues replicate the physiological complexity of human organs, providing more accurate data on drug efficacy and toxicity than traditional 2D cultures or animal models.

Novel product launches and developments are further boosting the market growth. For instance, in June 2025, TissueLabs, a Swiss company specializing in biofabrication technologies, launched TissuePro, a new extrusion-based bioprinter designed for advanced applications in drug development and related fields. The release builds on the success of the company’s earlier system, TissueStart, which became a widely used entry-level platform for labs exploring tissue engineering.

Companies like Organovo have pioneered this space with their exVive Human Liver Tissue, used for drug metabolism and toxicity screening, while CELLINK/BICO offers bioprinters and bioinks tailored for pharmaceutical R&D. As drug development costs and timelines continue to rise, bioprinted tissue models enable faster decision-making, reduce late-stage failures, and align with global efforts to minimize animal testing, making this segment the most dynamic and rapidly expanding within the bioprinting market.

Bioprinting & Tissue Engineering Devices Market Geographical Analysis

North America is expected to dominate the global bioprinting & tissue engineering devices market with a 42.87% in 2024

The North America region is the dominant region in the bioprinting & tissue engineering devices market. The presence of major bioprinter manufacturers, bioink developers, and academic-industry collaborations fosters continuous innovation and rapid translation from research to clinical applications. Together, these factors create a robust ecosystem that not only drives market growth but also positions the North America as a global leader in bioprinting and tissue engineering technologies.

US Bioprinting & Tissue Engineering Devices Market Trends

For instance, kidney disease alone affects over 35.5 million Americans, with approximately 815,000 living with kidney failure and more than 260,000 relying on a kidney transplant. Despite over 90,000 people on the transplant waiting list, only 28,492 kidney transplants were performed in 2024, highlighting a persistent shortage of donor organs. This critical gap drives demand for alternative solutions, such as 3D bioprinted tissues and organs, to reduce reliance on dialysis and improve patient outcomes.

The US also leads in technological innovation, with companies like Organovo successfully developing functional liver tissue for drug testing, reducing reliance on animal models, and 3D Systems collaborating with TISSIUM to achieve FDA-approved bioabsorbable devices for peripheral nerve repair. Recent FDA guidelines for 3D-bioprinted tissues and organ-assist devices have streamlined regulatory pathways, accelerating product approvals and encouraging commercial adoption.

The Asia Pacific region is the fastest-growing region in the global bioprinting & tissue engineering devices market, with a CAGR of 14.7% in 2024

The Asia-Pacific (APAC) region is the fastest-growing market for bioprinting & tissue engineering devices, driven by rapid technological adoption, expanding research infrastructure, and strong government support for regenerative medicine. Countries such as China, Japan, South Korea, and India are leading this surge through heavy investments in biotechnology and 3D bioprinting research. For instance, Japan’s Cyfuse Biomedical has developed its proprietary Regenova bioprinter for scaffold-free cell assembly, while South Korea’s Rokit Healthcare launched its Dr. Invivo 4D6 bioprinter and recently patented a multi-bioink multi-organ printing system in 2024.

Similarly, India’s Pandorum Technologies made global headlines with its advancements in bioprinted corneal and liver tissues aimed at clinical translation. China’s growing investment in regenerative medicine, backed by government initiatives like the Made in China 2025 plan, has led to new research centers focused on organ regeneration and stem-cell bioprinting. Rising healthcare expenditure, a growing burden of chronic diseases, and an increasing emphasis on personalized medicine are further accelerating adoption. Together, these factors make Asia-Pacific the most dynamic and rapidly expanding region in the global bioprinting and tissue engineering landscape.

Europe Bioprinting & Tissue Engineering Devices Market Trends

Europe is witnessing strong growth in the bioprinting & tissue engineering devices market, driven by robust regulatory support and a growing focus on regenerative medicine. The European Union’s harmonized Medical Device Regulation (MDR) and funding initiatives such as Horizon Europe are accelerating the translation of lab-based research into clinical applications. Recent developments like CELLINK’s 2023 partnership with Paralab to expand bioprinting access in Portugal and Spain, and the EU-funded NEOLIVER project (2025) to develop the first autologous bioprinted liver, highlight Europe’s commitment to innovation and commercialization.

Additionally, countries such as Germany, the UK, France, and the Netherlands are leading in academic-industry collaborations, while the region’s push to replace animal testing under new EU regulations is boosting the demand for bioprinted tissue models. Combined with an aging population and the rising prevalence of chronic diseases, these factors position Europe as a rapidly expanding hub for bioprinting and tissue engineering advancements.

Bioprinting & Tissue Engineering Devices Market Competitive Landscape

Top companies in the bioprinting & tissue engineering devices market include CELLINK, 3D Systems, Inc., CollPlant Biotechnologies Ltd., Organovo Holdings Inc., Regemat 3D, regenHU, CYFUSE BIOMEDICAL K.K., Poietis Biosystems, and ARTBioprint,among others.

Market Scope

| Metrics | Details | |

| CAGR | 14.9% | |

| Market Size Available for Years | 2022-2033 | |

| Estimation Forecast Period | 2025-2033 | |

| Revenue Units | Value (US$ Bn) | |

| Segments Covered | Product Type | Bioprinters, Bioinks, and Others |

| Material | Synthetic Materials, Natural Materials, Scaffolds, and Protein-Based Materials | |

| Application | Tissue Engineering & Regenerative Medicine, Drug Discovery, Development & Toxicology Testing, Biomedical Research & Academic Applications, Therapeutic Applications, and Others | |

| End-User | Hospitals & Clinics, Academic & Research Institutes, Biopharmaceutical Companies, and Contract Manufacturing Organizations | |

| Regions Covered | North America, Europe, Asia-Pacific, South America and the Middle East & Africa | |

The global bioprinting & tissue engineering devices market report delivers a detailed analysis with 67 key tables, more than 65 visually impactful figures, and 159 pages of expert insights, providing a complete view of the market landscape.

Suggestions for Related Report

For more biotechnology-related reports, please click here