Biomass Pellets Market Overview

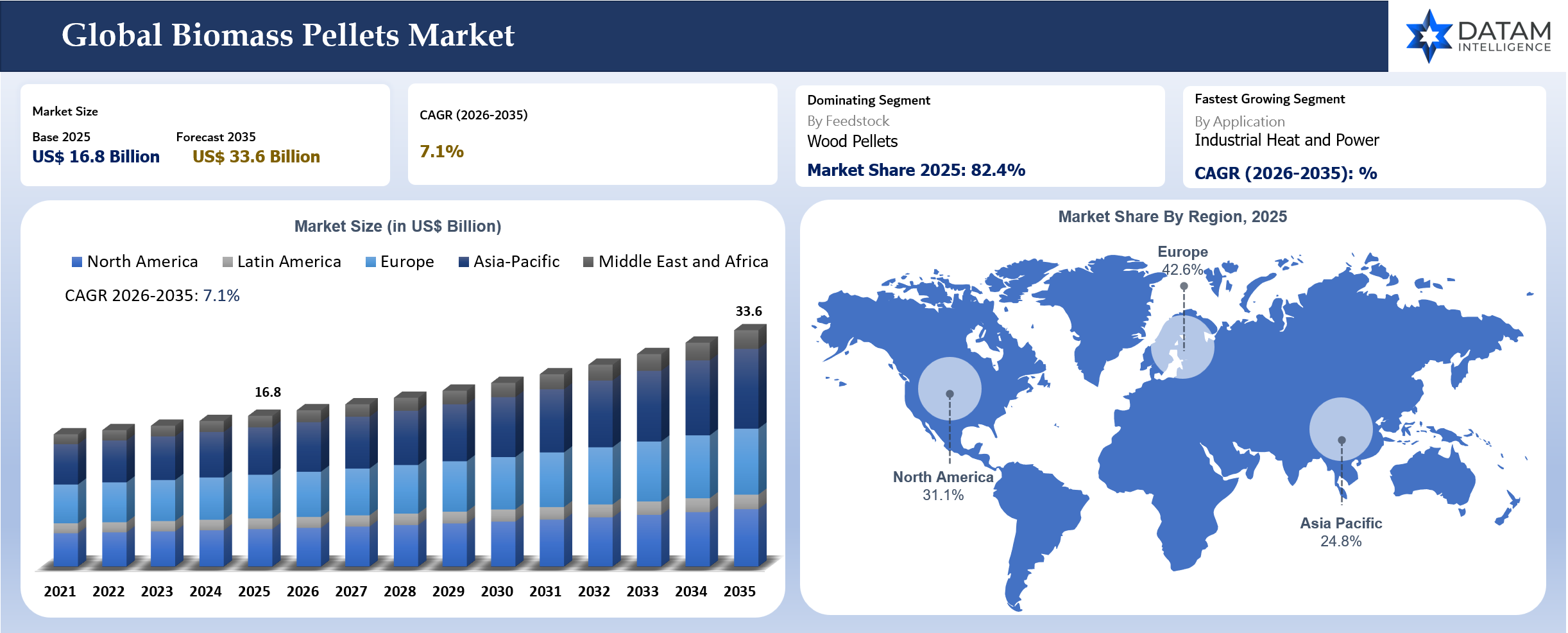

The global biomass pellets market reached US$ 16.8 billion in 2025 and is expected to reach US$ 33.6 billion by 2035, growing at a CAGR of 7.1% during 2026-2035. Biomass pellets are used in power generation, industrial heat, district heating, residential heating and commercial boiler systems. Demand is driven by energy transition policies, coal replacement, dispatchable renewable power needs and heating decarbonization.

Wood pellets dominate the market because they have established production, handling, storage and combustion systems. Industrial pellets are used by power producers and large heat users, while premium residential pellets are consumed in pellet stoves and small boilers. Agricultural residue pellets are gaining interest but face higher quality variation, ash content and logistics constraints.

Sustainability scrutiny is becoming one of the strongest market forces. Buyers are demanding certified feedstock, traceability, carbon accounting and evidence that pellets are not linked to harmful forestry practices, which is changing procurement behavior, especially in Europe and UK.

Key Takeaways

- Wood pellets dominated the biomass pellets market with 82.4% share in 2025, supported by established supply chains, power generation use and residential heating systems.

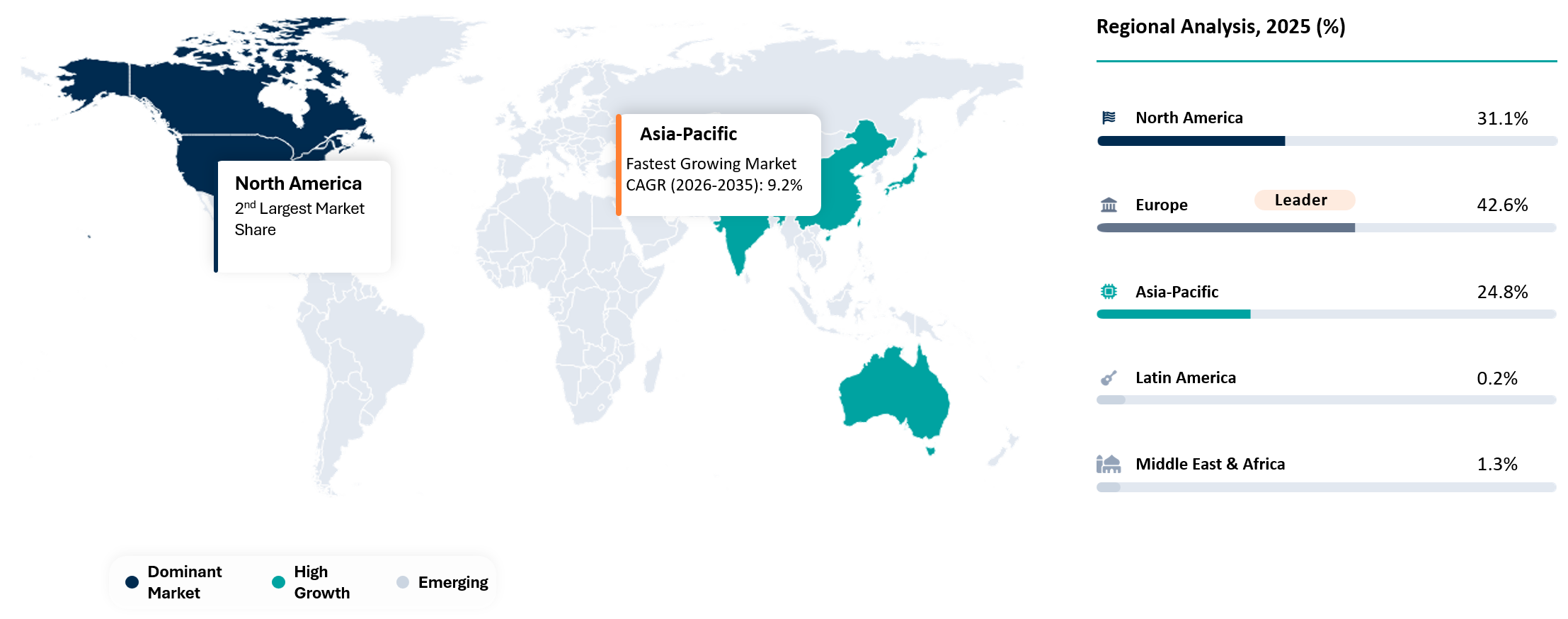

- Europe dominated demand with 42.6% share in 2025, driven by district heating, power generation, residential heating and renewable energy policy support.

- Asia-Pacific is the fastest-growing region with a projected CAGR of 8.1% during 2026-2035, led by Japan, South Korea and industrial decarbonization demand.

- Industrial-grade pellets dominated by application value in 2025 because utility-scale power and heat users purchase large volumes under long-term contracts.

- Residential heating pellets remain important in Europe and North America where pellet stoves and small boilers support heating demand.

- Supplier differentiation is moving toward certified sourcing, low-ash quality, moisture control, port logistics, contract reliability and sustainability documentation.

Market Scope

| Metrics | Details | |

| 2025 Market Size | US$ 16.8 Billion | |

| 2035 Projected Market Size | US$ 33.6 Billion | |

| CAGR (2026-2035) | 7.1% | |

| Largest Market | Europe, 42.6% market share in 2025 | |

| Fastest Growing Market | Asia-Pacific, 8.1% CAGR between 2026 and 2035 | |

| Dominating Feedstock | Wood Pellets, 82.4% market share in 2025 | |

| Fastest Growing Application | Industrial Heat and Power, 8.3% CAGR between 2026 and 2035 | |

| By Feedstock | Forest Residues, Sawmill Residues, Wood Chips, Agricultural Residues, Energy Crops and Others | |

| By Grade | Industrial Grade, Premium Residential Grade and Commercial Heating Grade | |

| By Application | Power Generation, Industrial Heat, District Heating, Residential Heating, Commercial Heating and Others | |

| By Distribution Channel | Long-Term Supply Contracts, Spot Sales, Distributor Sales and Retail Sales | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

Why Does This Report Matter In 2026?

Biomass pellet buyers enter 2026 with two competing pressures: they need dispatchable renewable energy and they must prove feedstock sustainability. Utilities and industrial customers value pellets because they can be stored, transported and burned in existing or converted assets. However, public scrutiny around forest sourcing, carbon accounting and subsidies is rising.

The strongest change is the move from volume procurement to sustainability-verified procurement. Buyers increasingly need ENplus, SBP or equivalent certification, transparent sourcing records and lower-risk feedstock strategies. Suppliers that cannot prove origin and chain of custody may lose access to premium European and Japanese customers.

Strategic Indicators For Biomass Pellets

High Regulation Impact

Regulation affects biomass pellets through renewable energy subsidies, sustainability criteria, forestry rules, emissions limits and import certification. European and UK buyers face the strongest scrutiny because public funding and carbon claims are closely examined. Japan and South Korea also require sustainability documentation for imported biomass.

High Investment Activity

Investment is concentrated in pellet mills, port terminals, drying systems, debarking, storage silos, bagging lines and certification systems. Asia-Pacific demand is encouraging exporters to secure long-term contracts. Producers are also investing in quality control to meet industrial and premium heating specifications.

Supply Chain Disruption

Supply-chain risk is tied to forest residues, sawmill output, drying energy, rail access, port capacity, shipping rates and certification. Pellet producers depend heavily on regional wood supply. Weather, wildfires, mill closures and logging restrictions can affect feedstock availability.

Pricing Volatility

Biomass pellet prices depend on wood residue cost, energy for drying, ocean freight, certification cost, currency movement and heating demand. Residential pellets also face winter seasonality. Industrial contract pricing is more stable but depends on long-term fuel and policy assumptions.

Procurement Pressure

Buyers are under pressure to secure certified pellets while controlling fuel cost. Power generators need reliable bulk shipments and sustainability documentation. Residential distributors need low moisture, low ash and consistent pellet durability. Procurement teams increasingly evaluate origin risk and supplier transparency.

New Technology Adoption

Technology adoption is focused on torrefied pellets, steam-treated pellets, advanced drying, quality monitoring and digital chain-of-custody systems. Better moisture control improves combustion efficiency and reduces shipping cost. Digital traceability can strengthen buyer confidence.

Import-Export And Pricing Intelligence

Industrial pellet pricing depends on feedstock cost, drying energy, pellet durability, ash level, moisture content, certification, port access, ocean freight and contract structure. Export suppliers serving Japan, South Korea, the UK and Europe must compete not only on price but on proof of sourcing. Buyers increasingly require certification, chain-of-custody records and origin transparency before accepting long-term supply.

Residential pellet pricing follows a different pattern. Heating demand is seasonal, weather-sensitive and influenced by retail inventory planning. Premium residential pellets require lower ash, lower fines, higher durability and consistent heating value. Local distribution matters more than ocean freight in these markets, although feedstock cost and sawmill residue availability still affect pricing.

| HS Code | Reporter | Trade Flow | 2025 Trade Value | Interpretation |

| 440131 | U.S. | Export | US$ 1.93 Billion | U.S. exports support European and Asian industrial pellet demand through large-scale port-linked supply chains. |

| 440131 | Canada | Export | US$ 1.37 Billion | Canada exports serve Japan, South Korea and Europe but face stronger scrutiny around forest sourcing and certification. |

| 440131 | UK | Import | US$ 2.28 Billion | UK imports reflect industrial biomass demand and reliance on overseas pellet supply for power generation. |

| 440131 | Japan | Import | US$ 1.68 Billion | Japan imports are tied to biomass power procurement and long-term renewable fuel contracts. |

| 440131 | South Korea | Import | US$ 569 Million | South Korea imports support renewable power obligations and industrial biomass co-firing. |

AI Impact Analysis

AI can support biomass pellet production through feedstock forecasting, mill optimization and quality control. Producers can use data to predict moisture variation, drying energy needs and pellet durability. It improves consistency and reduces waste. Supply-chain analytics can improve shipment planning. Industrial buyers rely on bulk vessels and port scheduling. Better forecasting can reduce demurrage risk, inventory shortages and contract penalties.

AI-supported traceability can also strengthen sustainability documentation. Buyers increasingly need proof of origin and chain of custody. Digital records can reduce audit burden and improve trust.

Disruption Analysis

Disruption is coming from sustainability scrutiny, energy policy shifts and Asian import growth. Europe remains large, but policy debates can affect long-term demand. Japan and South Korea are becoming more important importers as they use biomass for renewable power.

Feedstock scrutiny is reshaping supplier selection. Buyers want residue-based and certified material rather than vague sustainability claims. Producers with transparent sourcing will have an advantage. Industrial heat offers a new growth route. Heavy industry and district heating systems may use pellets where electrification is difficult. Growth depends on fuel economics and policy support.

BCG Matrix: Company Evaluation

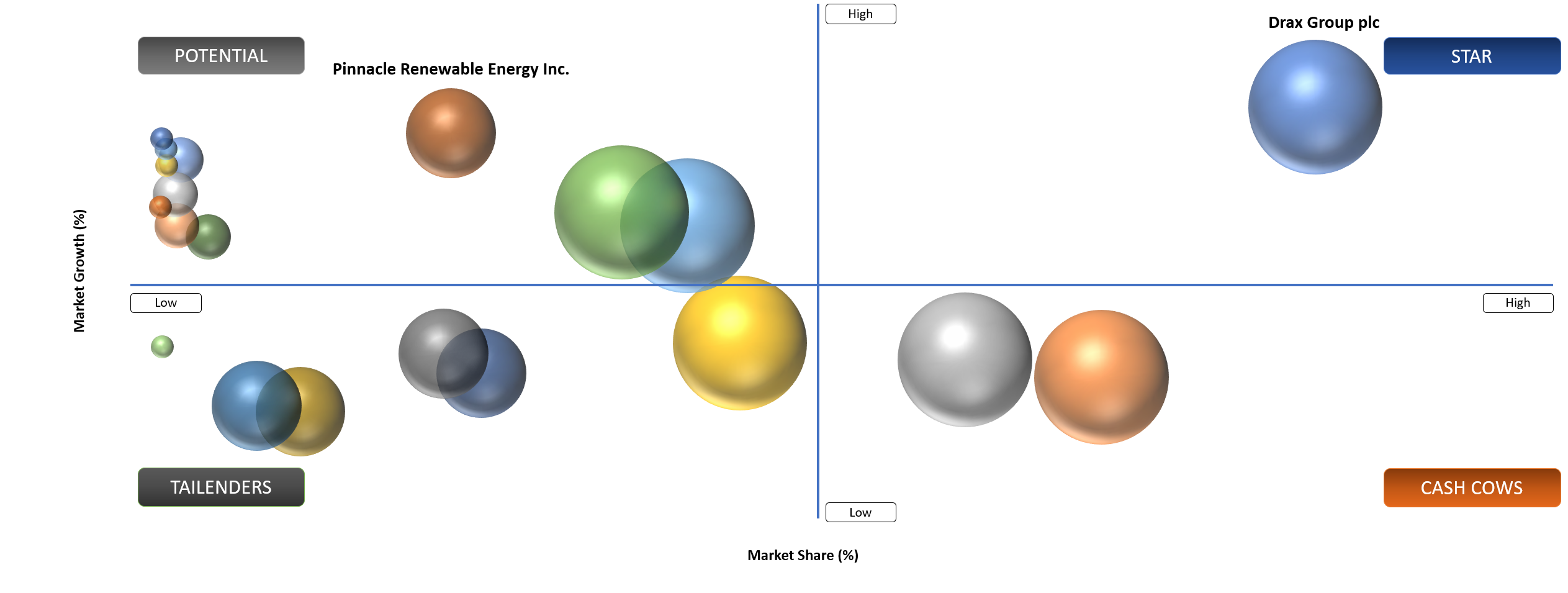

Star

Star players include Drax Group plc, Enviva Inc., Graanul Invest AS, Lignetics, Inc., Pinnacle Renewable Energy, Fram Renewable Fuels and Highland Pellets LLC. Strong players have feedstock access, certification, export logistics and long-term customer relationships.

Potential

Potential players include regional pellet mills, agricultural residue pellet producers and industrial heat-focused suppliers. Growth depends on quality control, certification and ability to serve local or export demand reliably.

Market Dynamics

Driver Impact Analysis

| Driver | Market Growth Impact | Demand Concentration | Impacted Use Case | Strategic Impact |

Renewable power policies sustain industrial pellet demand | 3.4% | Europe, Japan and South Korea | Utility-scale biomass power | Supports long-term supply contracts |

Heating decarbonization supports premium pellet demand | 2.7% | Europe and North America | Residential and commercial heating | Sustains seasonal retail demand |

Industrial heat users seek coal alternatives | 2.5% | Asia-Pacific and Europe | Boilers and process heat | Creates new demand beyond power generation |

Certification improves buyer confidence | 2.1% | Europe and Japan | Industrial and premium pellets | Rewards traceable suppliers |

Renewable Power Policies Sustain Industrial Pellet Demand

Renewable power policy remains the central demand driver because industrial pellet consumption is often supported by power-generation incentives, renewable portfolio requirements or energy-transition targets. Biomass pellets provide dispatchable renewable power where wind and solar output fluctuate. Utilities and independent power producers value pellets because fuel can be stored, shipped and used in converted or dedicated boilers.

Japan and South Korea are important growth markets because imported biomass supports renewable power procurement and energy diversification. The markets rely on long-term fuel contracts and strict supplier documentation. Industrial buyers need fuel with predictable moisture, ash, calorific value and sustainability certification. Suppliers that can provide consistent shipping and transparent origin records are better positioned.

Europe and UK remain large demand centers, but policy support is becoming more conditional. Subsidy arrangements are moving toward tighter sustainability requirements, lower operating hours and stronger scrutiny of sourcing claims. It does not remove industrial pellet demand, but it changes the basis of competition. Verified supply and credible documentation are becoming as important as fuel price.

Industrial heat also strengthens demand beyond power generation. Food processing, paper, textiles, district heating and cement applications can use biomass pellets where coal or fuel oil replacement is commercially and technically practical. Growth will be strongest where policy support, boiler compatibility and feedstock availability align.

Restraint Impact Analysis

| Restraint | Drag On Market Growth | Primary Impact Area | Impacted Use Case | Strategic Impact |

Sustainability scrutiny affects policy support | 3.3% | Europe and UK | Power generation pellets | Raises documentation and reputational risk |

Feedstock availability limits production growth | 2.8% | North America and Europe | Wood pellet mills | Increases sourcing competition |

Freight cost volatility affects delivered pricing | 2.4% | Export markets | Industrial pellet contracts | Raises landed cost uncertainty |

Ash and moisture variation affect combustion quality | 1.9% | Heating and industrial users | Premium and industrial pellets | Requires tighter quality control |

Sustainability Scrutiny Affects Policy Support

Sustainability scrutiny is the strongest restraint because biomass pellets depend on the credibility of feedstock sourcing and carbon accounting. Buyers, regulators, investors and communities increasingly question whether imported wood pellets deliver real climate benefits when forest regrowth, shipping emissions and biodiversity impacts are considered. The scrutiny can directly affect subsidies, customer contracts and supplier reputation.

Drax-related investigations and policy debates show how quickly sustainability risk can become commercial risk. Industrial buyers that rely on biomass support must prove that pellets come from eligible sources and meet chain-of-custody requirements. A supplier with weak documentation can face contract challenges even if the physical product meets combustion specifications.

Certification does not fully remove the restraint. Buyers increasingly want stronger evidence behind certificates, including feedstock category, harvest location, residue share and audit quality. Producers using sawmill residues, forest thinnings or low-grade roundwood must document sourcing clearly. Claims that are too broad can become reputational liabilities.

Sustainability scrutiny also affects future investment. New pellet mills, port terminals and long-term offtake contracts may face more diligence from lenders and customers. Projects with transparent feedstock supply, local community support and credible certification will attract stronger interest. Producers that cannot prove sourcing quality may be pushed toward lower-value markets.

Segment Analysis

Industrial Wood Pellets Will Continue To Dominate Demand

Industrial wood pellets will continue to dominate because utilities and large heat users purchase bulk volumes under long-term contracts. The customers need stable fuel quality, vessel-scale logistics, port storage, certification and reliable delivery. Industrial pellets may not require the same visual quality as residential products, but they must meet energy, ash and moisture specifications that support predictable combustion.

Power generation remains the largest industrial use. Biomass pellets are used in converted coal plants, dedicated biomass plants and co-firing systems where permitted. Demand depends heavily on renewable energy policy, subsidy structures, grid needs and fuel economics. A change in policy support can affect purchasing volumes more quickly than normal retail demand shifts.

Industrial pellets also support process heat. Factories and district heating systems can use pellets where electrification is difficult or where biomass boilers are already installed. The demand is more local and more varied than utility demand. Suppliers that can serve both long-term utility contracts and regional heat customers have a more balanced market position.

Premium Residential Pellets Depend On Quality And Winter Availability

Premium residential pellets serve households using pellet stoves and small boilers. Demand is strongest in Europe and North America where cold climates, rural heating needs and established stove markets support seasonal purchases. Consumers evaluate pellets through heat output, ash content, dust, bag quality and stove performance. A low-quality pellet can create maintenance problems and customer complaints quickly.

Seasonality makes this segment different from industrial demand. Retailers and distributors must build inventory before winter and mild weather can leave excess stock. Cold winters can create shortages and price spikes. Producers serving residential customers need flexible storage, reliable bagging and strong distributor relationships.

Premium certification and quality consistency are important. Residential buyers may not review sustainability documents deeply, but they respond to stove performance and ash behavior. Suppliers with low-moisture, low-fines and consistent pellets can build brand loyalty even in a commodity-like heating market.

Agricultural Residue Pellets Create Opportunity But Face Quality Barriers

Agricultural residue pellets are gaining interest because they can turn crop residues into useful fuel and reduce open-field burning in some regions. India is one of the most relevant markets because rice straw, husk, cotton stalk and other residues are available in large volumes. The feedstocks can support industrial boilers and co-firing when logistics and quality are managed properly.

Quality barriers remain significant. Agricultural residues often have higher ash, chlorine, potassium and silica content than wood pellets. The properties can increase slagging, fouling, corrosion and maintenance requirements in boilers. Buyers need clear fuel specifications and may require boiler modifications before adopting agricultural pellets at scale.

Aggregation is another challenge. Crop residues are dispersed, seasonal and bulky before densification. Producers need collection systems, drying, storage and pelletizing capacity near feedstock sources. Growth will depend on local supply chains and industrial buyers willing to accept non-wood pellet specifications.

Black Pellets Offer Higher Energy Density But Need Commercial Proof

Black pellets, including torrefied and steam-treated pellets, offer improved water resistance, higher energy density and better handling characteristics compared with standard white pellets. The features can make them more compatible with coal logistics and storage systems. Utilities evaluating coal replacement may find black pellets attractive where handling and storage compatibility matter.

Commercial adoption remains limited compared with white pellets. Production cost, scale, technology reliability and buyer qualification remain barriers. Utilities need assurance that black pellets can be supplied consistently and burned safely in existing systems. Without stable production scale, buyers hesitate to build procurement strategies around the product.

Black pellets could become more attractive if industrial users need biomass fuel with better transport efficiency and storage stability. Growth will depend on technology providers proving cost competitiveness and long-term supply reliability. For now, black pellets remain a strategic opportunity rather than the main demand base.

Market Segmentation

- By Product

- White Pellets

- Black Pellets

- Torrefied Pellets

- Steam Exploded Pellets

- Agricultural Pellets

- Mixed Biomass Pellets

- Others

- By Feedstock

- Forest Residues

- Branches

- Tops

- Thinnings

- Low-Grade Roundwood

- Sawmill Residues

- Sawdust

- Wood Shavings

- Wood Chips

- Bark Residues

- Recycled Wood

- Untreated Construction Wood

- Pallet Wood

- Industrial Wood Residues

- Agricultural Residues

- Rice Husk

- Wheat Straw

- Corn Stover

- Cotton Stalk

- Sugarcane Bagasse

- Palm Kernel Shell

- Others

- Energy Crops

- Miscanthus

- Switchgrass

- Short Rotation Coppice

- Others

- Forest Residues

- By Grade

- Industrial Grade

- Utility Grade Pellets

- CHP (Combined Heat and Power) Grade Pellets

- Premium Residential Grade

- Commercial Heating Grade

- Industrial Grade

- By Application

- Power Generation

- Dedicated Biomass Power Plants

- Coal Co-Firing

- Converted Coal Power Plants

- Industrial Heat

- Cement Kilns

- Food Processing Boilers

- Textile Boilers

- Paper and Pulp Boilers

- District Heating

- Residential Heating

- Pellet Stoves

- Small Boilers

- Commercial Heating

- Schools

- Hospitals

- Hotels

- Public Buildings

- Others

- Power Generation

- By Distribution Channel

- Long-Term Supply Contracts

- Spot Sales

- Distributor Sales

- Retail Sales

- Direct Industrial Sales

- By End-User

- Utilities

- Independent Power Producers

- Industrial Boiler Operators

- District Heating Operators

- Residential Consumers

- Commercial Facilities

- Government and Municipal Facilities

- Others

Geographical Penetration

U.S. Biomass Pellets Market Trends

U.S. is a major wood pellet export base, especially from the Southeast. Production is supported by forest resources, sawmill residues, port access and long-term contracts with European and Asian buyers. Domestic residential heating demand exists but exports are the larger strategic story. Pellet producers need reliable feedstock access and port logistics. Weather and mill residue supply can affect output. Sustainability certification is increasingly important. Export customers want chain-of-custody records and evidence that pellet production does not rely on harmful forestry practices.

India Biomass Pellets Market Landscape

India is an emerging biomass pellet market due to industrial fuel switching and agricultural residue management. Demand is linked to boilers, small industries and policy interest in reducing crop residue burning. Agricultural residue pellets are more relevant in India than in many Western markets. Rice husk, straw, cotton stalk and other residues can be used, but ash content and logistics need careful management. Growth depends on local aggregation, pellet quality and boiler compatibility. Industrial buyers need reliable fuel supply before switching from coal or furnace oil.

Japan Biomass Pellets Market Outlook

Japan is a major import market because biomass supports renewable power generation and energy diversification. Utilities and power producers rely on imported pellets from North America and Asia-Pacific suppliers. Japanese buyers place strong emphasis on certification, long-term contracts and sustainability documentation. Supplier transparency is therefore a core procurement requirement. Demand growth is tied to renewable policy and plant utilization. Importers need stable shipping, quality control and supplier credibility.

Competitive Landscape

- Competition is split between industrial pellet exporters, residential pellet producers, regional mills, feedstock aggregators, certification-led suppliers and biomass power companies. Industrial suppliers compete on certified capacity, port logistics, contract reliability, vessel-loading capability and feedstock security. Residential suppliers compete on pellet quality, ash level, bagging, brand trust and winter availability.

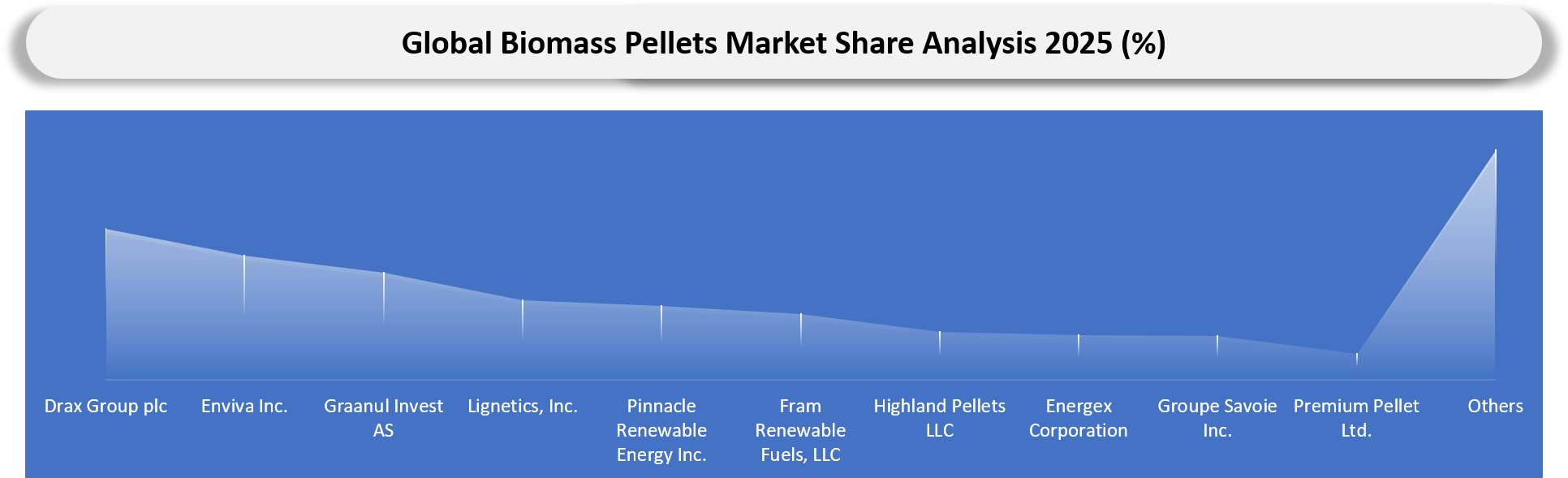

- Drax, Enviva, Graanul Invest, Pinnacle Renewable Energy, Lignetics, Fram Renewable Fuels and Highland Pellets are important because they serve either industrial export markets or heating markets with established production and distribution networks. Drax and Enviva are especially visible because large-scale export and power generation demand expose them to sustainability, financing and policy scrutiny.

- Regional pellet mills can compete strongly where local heating demand or industrial boiler demand exists. The producers may not match the export scale of larger players, but they can offer lower freight exposure and closer customer relationships. Local mills are also important in agricultural residue markets where feedstock collection is regional.

- Competitive benchmarking should track certified production capacity, feedstock mix, residue share, port access, long-term contracts, financial stability, moisture control, ash content, pellet durability and audit transparency. Suppliers with strong documentation and diversified customer bases will be better positioned than supplier’s dependent on one subsidy-driven buyer.

Key Companies

- Drax Group plc

- Enviva Inc.

- Graanul Invest AS

- Lignetics, Inc.

- Pinnacle Renewable Energy Inc.

- Fram Renewable Fuels, LLC

- Highland Pellets LLC

- Energex Corporation

- Groupe Savoie Inc.

- Premium Pellet Ltd.

- Stora Enso Oyj

- UPM-Kymmene Corporation

- AS Graanul Invest

- CM Biomass Partners A S

- Valfei Products Inc.

- German Pellets GmbH

- Zilkha Biomass Energy LLC

- Amandus Kahl GmbH and Co. KG

- CPM Holdings, Inc.

- Andritz AG

Company Coverage Preview

Drax Group plc is one of the most visible biomass pellet companies because it operates pellet production assets and uses pellets in large-scale power generation. The company’s position is strategically important but also highly scrutinized due to sustainability claims, subsidies and sourcing transparency.

Enviva Inc. remains an important producer in USA wood pellet export market. Its position is tied to long-term supply agreements, production assets and export logistics. The company’s financial restructuring history also makes it important for evaluating supplier risk in the industrial pellet market.

Pinnacle Renewable Energy, Graanul Invest, German Pellets, Lignetics and several regional producers are relevant across industrial and heating pellet markets. Competitive strength depends on feedstock access, certification, port logistics and contract reliability.

Major Pain Points

- Sustainability scrutiny can affect policy support, buyer confidence and investor appetite.

- Forest biomass claims require stronger evidence as regulators and NGOs question feedstock origin.

- Feedstock competition from pulp, board, paper and bioenergy producers can raise wood residue costs.

- Ocean freight volatility affects delivered costs for Europe, Japan and South Korea.

- Industrial buyers need certified supply at scale, but certification alone may not satisfy emerging traceability expectations.

- Pellet quality variation in moisture, ash and fines can reduce boiler efficiency and increase maintenance.

- Agricultural residue pellets face higher ash and corrosion risk compared with wood pellets.

- Residential heating demand is seasonal and can create inventory risk for distributors.

- Export-oriented producers face financial exposure when long-term contracts become mispriced.

- Port storage, dust control and fire prevention remain operational risks in bulk pellet handling.

Recent Developments

- June 2026: Drax agreed to acquire Bluefield Solar Income Fund in a deal valued at about GBP 561 million, supporting its wider diversification strategy as the company manages long-term exposure to biomass subsidy changes and renewable power portfolio transition.

- February 2026: Drax announced plans to reduce Canadian biomass use at its UK power station and shift future UK fuel sourcing toward U.S. wood pellets from 2027, making sourcing origin and sustainability verification a central procurement issue.

- November 2025: UK government agreed a new support arrangement for Drax covering 2027 to 2031, reducing biomass generation support while requiring tighter sustainability conditions and lower operating hours compared with the current subsidy regime.

- August 2025: UK Financial Conduct Authority opened an investigation into historical statements made by Drax about biomass sourcing, increasing scrutiny of wood pellet traceability, sustainability claims and investor-facing disclosure.

- March 2025: Biomass pellet buyers in Japan and South Korea increased long-term contract scrutiny around certified sourcing, moisture control, ash performance and supplier reliability as imported pellet volumes remained central to renewable power procurement.

Analyst View And Opinion

- Industrial wood pellets will remain the largest demand base, but future growth will be more dependent on sustainability verification than headline renewable energy policy alone.

- Japan and South Korea will continue gaining importance as import markets because both need dispatchable renewable fuel and long-term biomass procurement.

- Europe and UK will remain important but face stronger scrutiny around subsidies, forest sourcing and carbon accounting.

- U.S. pellet exports will remain strategically important because of port access, feedstock availability and established industrial contracts.

- Canada will face more intense sourcing scrutiny where pellet production is linked to old-growth forest concerns or contested feedstock categories.

- Residential pellet demand will remain stable in cold-climate markets but will continue to be weather-sensitive and seasonal.

- Agricultural residue pellets can grow in India and other crop-producing markets, but ash quality and feedstock aggregation must improve before large-scale adoption.

- Black pellets have long-term potential but need stronger commercial proof and cost competitiveness before they become a mainstream product group.

- Pellet producers with transparent chain-of-custody systems will win better customer access as buyers move from certificate checks to deeper supplier audits.

- Financial resilience will become more important in supplier selection because large industrial buyers need assurance that producers can honor long-term contracts.

Target Audience

| Industry | Who Should Buy This Report? | Reason To Buy This Report |

| Pellet Producers | Strategy Teams, Export Managers | Track demand by region, grade and application |

| Utilities | Fuel Procurement Teams | Evaluate industrial pellet supply and sustainability risk |

| District Heating | Fuel Managers | Assess biomass pellet economics and supply stability |

| Residential Heating Suppliers | Distributors, Retailers | Understand premium pellet demand and seasonal risks |

| Industrial Boilers | Plant Managers | Evaluate fuel switching and pellet quality requirements |

| Investors | Renewable Energy Investors | Assess pellet production, policy and sustainability exposure |

What DataM Uniquely Provides

- DataM separates industrial pellets, residential heating pellets, commercial heating pellets, agricultural pellets and black pellets so clients can assess demand by fuel quality and buyer type.

- DataM maps feedstock supply across forest residues, sawmill residues, recycled wood, agricultural residues and energy crops to identify sourcing risk and regional opportunity.

- DataM provides import-export intelligence through HS 440131 and related biomass fuel codes, with country-level interpretation for U.S., Canada, UK, Japan and South Korea trade flows.

- DataM benchmarks suppliers by certified capacity, feedstock transparency, port access, long-term contracts, financial strength and customer concentration.

- DataM tracks policy exposure across renewable power incentives, heating decarbonization, biomass sustainability rules and import certification requirements.

- DataM evaluates pellet pricing through feedstock cost, drying energy, freight, certification, moisture, ash, durability and contract structure.

- DataM supports buyers with procurement-risk mapping around sustainability claims, forest sourcing, chain-of-custody audits and supplier solvency.

- DataM provides country-level insight for India’s agricultural residue pellet opportunity, including crop residue availability, boiler compatibility and industrial fuel switching.