Biodegradable Engine Oil Market Overview

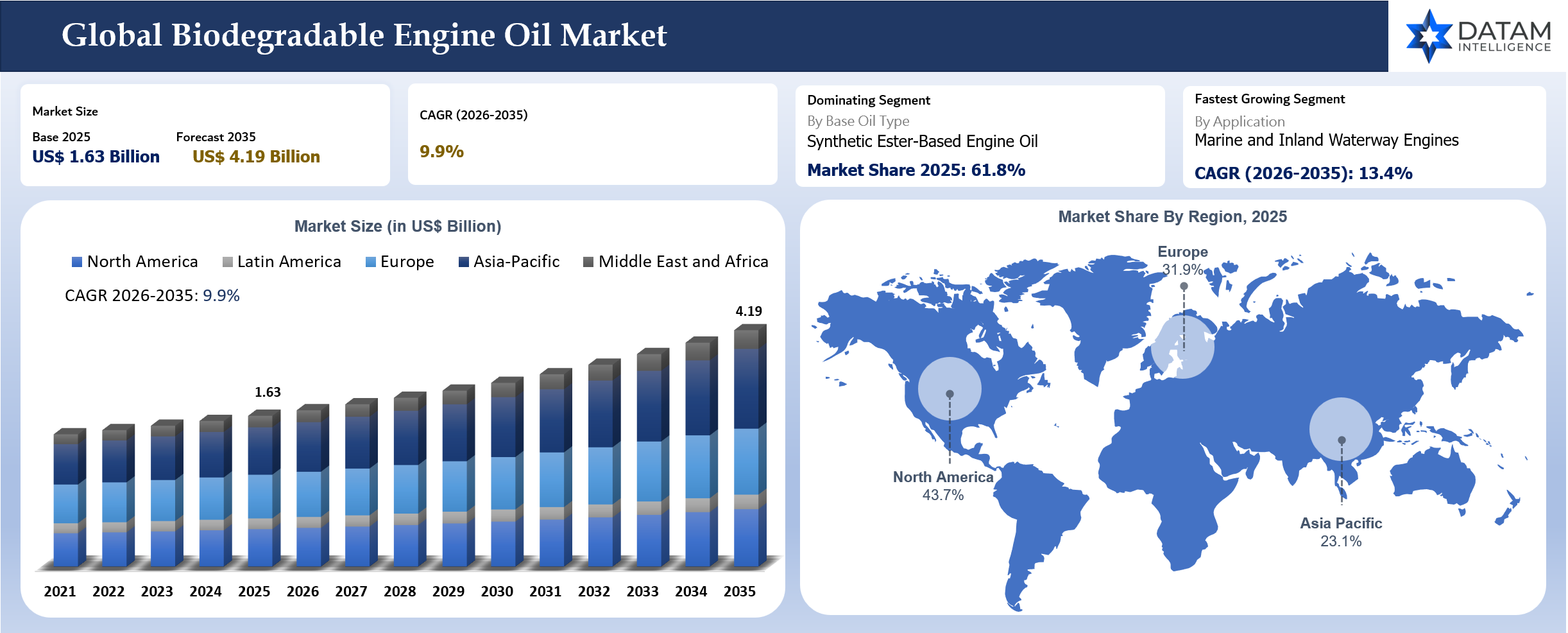

The global biodegradable engine oil market reached US$ 1.66 billion in 2025 and is expected to reach US$ 4.10 billion by 2035, growing at a CAGR of 9.9% during 2026-2035. The market is gaining relevance as marine, forestry, agriculture, construction, and environmentally sensitive equipment operators seek lubricants with lower environmental persistence. Demand is strongest where engine oil leakage, spill risk, or disposal exposure affect soil, water, or sensitive habitats.

Biodegradable engine oil remains a specialized segment within the broader engine oil market. It is not yet a universal replacement for conventional mineral or synthetic oils because performance requirements, OEM approvals, oxidation stability, cold-flow behavior, and drain intervals must be carefully managed. Adoption is strongest where regulation, customer sustainability commitments, or environmental liability justify premium pricing.

Base oil selection is central to product positioning. Vegetable oil-based, synthetic ester and biosynthetic base oils offer different balances of biodegradability, lubricity, thermal stability and cost. Synthetic ester-based engine oil is gaining attention because they can offer stronger oxidation stability and low-temperature performance than basic vegetable oil formulations.

Key Takeaways

- Synthetic ester-based biodegradable engine oils dominated the market with 46.2% share in 2025, supported by stronger thermal stability, lubricity and performance consistency in demanding engines.

- Europe dominated regional demand with 38.7% share in 2025, driven by stricter environmental expectations, marine regulations, forestry operations and wider acceptance of eco-labelled lubricants.

- Marine and inland waterway applications are expected to be the fastest-growing use area during 2026-2035, supported by vessel leakage risk, port sustainability programs and environmentally acceptable lubricant requirements.

- Agriculture and forestry remain strong demand pockets because equipment operates near soil, crops, forests and waterways where oil leakage can create environmental exposure.

- Premium pricing remains a barrier in price-sensitive fleets, especially where regulation does not mandate biodegradable or environmentally acceptable lubricants.

- Supplier differentiation is moving toward OEM approvals, oxidation stability, cold-weather performance, long drain intervals, ecolabel certification and local technical support.

Market Scope

| Metrics | Details |

| 2025 Market Size | US$ 1.66 Billion |

| 2035 Projected Market Size | US$ 4.10 Billion |

| CAGR During 2026-2035 | 9.9% |

| Largest Market | North America, 43.7% Market Share in 2025 |

| Fastest Growing Market | Asia-Pacific, 12.8% CAGR between 2026 and 2035 |

| Dominating Base Oil Type | Synthetic Ester-Based Engine Oil, 61.8% Market Share in 2025 |

| Fastest Growing Application | Marine and Inland Waterway Engines, 13.4% CAGR between 2026 and 2035 |

| By Base Oil Type | Vegetable Oil-Based, Synthetic Ester-Based, PAG-Based, Biosynthetic Base Oil-Based and Blended Bio-Based Oils |

| By Engine Type | Diesel Engines, Gasoline Engines, Two-Stroke Engines, Four-Stroke Engines and Hybrid Equipment Engines |

| By Application | Marine, Agriculture, Forestry, Construction, Mining, Municipal Fleets, Landscaping, Industrial Engines and Others |

| By Distribution Channel | OEM Fill, Aftermarket, Fleet Contracts, Distributor Sales and Online Sales |

| By Region | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa |

Why Does This Report Matter In 2026?

Biodegradable engine oil buyers enter 2026 with stronger pressure to reduce environmental risk without compromising engine protection. Fleet operators working near water, forests, farms and urban public spaces are under closer scrutiny from regulators, insurers and customers. A lubricant failure can create both equipment downtime and environmental liability.

The strongest market shift is the move from basic bio-based oil claims toward performance-proven biodegradable lubricants. Buyers need engine oils that can handle oxidation, viscosity stability, deposits, wear protection and cold starts. The market will grow where suppliers prove that environmental performance and engine reliability can work together.

Strategic Indicators For Biodegradable Engine Oil

High Regulation Impact

Regulation affects demand through marine discharge rules, forestry policies, municipal procurement, environmental liability and ecolabel frameworks. Vessel operators and contractors working near waterways face stronger pressure to use environmentally acceptable lubricants. European buyers often evaluate biodegradable lubricants through eco-label and procurement standards.

High Investment Activity

Investment is concentrated in synthetic esters, biosynthetic base oils, additive packages, long-drain formulations and OEM approval programs. Suppliers are developing products that meet biodegradability expectations while improving oxidation resistance and engine cleanliness. Fleet trials and field validation are becoming more important.

Supply Chain Disruption

Supply-chain risk is tied to vegetable oil feedstocks, synthetic ester capacity, additives and specialty blending. Feedstock availability can be affected by agricultural conditions and competing demand from food and biofuels. Synthetic ester products face capacity and cost constraints but offer stronger performance consistency.

Pricing Volatility

Biodegradable engine oils carry premium pricing due to specialty base oils and additives. Prices are influenced by vegetable oils, esters, energy, additive chemistry and certification costs. Buyers should compare oil price with environmental risk reduction, disposal cost, spill response exposure and equipment protection.

Procurement Pressure

Fleet managers need biodegradable oils that perform under real engine conditions. Procurement teams evaluate cost, drain interval, OEM approval, cold-flow behavior and local availability. A product that is biodegradable but shortens drain intervals can create higher total cost.

New Technology Adoption

Technology adoption is focused on biosynthetic base oils, advanced ester chemistry, ashless additives and performance monitoring. Used oil analysis can help fleets validate drain intervals and engine protection. Better additive technology can improve oxidation stability and cleanliness.

Import Export And Pricing Intelligence

Pricing is assessed separately for vegetable oil-based engine oils, synthetic ester-based engine oils, PAG-based engine oils and biosynthetic base oil formulations. Synthetic ester-based products usually command a premium because they offer better oxidation stability, low-temperature behavior and high-load performance than basic vegetable oil formulations. Vegetable oil-based products can offer strong biodegradability but may face thermal stability and drain interval limitations in demanding engines.

Premium pricing is justified only where the product reduces environmental liability, supports contract compliance or protects equipment in sensitive operating environments. Marine operators, forestry contractors, municipal fleets and agriculture users are more likely to accept higher cost when leakage risk is visible and when customers, regulators or landowners require lower-impact fluids. Price-sensitive fleets will continue using conventional oil unless the buyer can prove avoided spill cost, longer drain life or procurement compliance value.

| HS Code | Reporter | Trade Flow | 2025 Trade Value | Interpretation |

| 340399 | Germany | Export | US$ 893.99 Million | Germany exports reflect demand for specialty biodegradable and high-performance lubricants used in marine, forestry and industrial equipment. |

| 340399 | U.S. | Export | US$ 1.09 Billion | U.S. exports indicate active bio-based lubricant production and specialty fleet demand in environmentally sensitive applications. |

| 340399 | Japan | Export | US$ 491.67 Million | Japan exports are linked to eco-positioned lubricants and specialty formulations used by industrial and transport customers. |

| 340399 | China | Import | US$ 777.34 Million | China imports reflect premium demand for biodegradable lubricants in marine, municipal and industrial use cases. |

| 340399 | India | Import | US$ 214.53 Million | India imports show early-stage demand for biodegradable lubricant formulations in agriculture, ports and municipal fleets. |

AI Impact Analysis

AI can support biodegradable engine oil development by improving formulation screening. Models can compare base oil, additive and viscosity combinations before lab trials. It can shorten development cycles for products that need both biodegradability and engine protection.

Fleet analytics can improve adoption by validating oil drain intervals and engine performance. Used-oil analysis data can help identify oxidation, wear metals and viscosity changes. It is important because buyers often worry that biodegradable oils may not perform as consistently as conventional lubricants. AI can also support demand forecasting for specialty lubricants. Marine, forestry and municipal fleets have project-based buying patterns. Better forecasting can reduce stockouts and improve distributor planning.

Disruption Analysis

Disruption is coming from environmental liability and performance improvements. Biodegradable engine oils are moving from a niche sustainability claim toward a risk-reduction tool in sensitive environments. Marine and forestry operators are most likely to adopt when spills create visible consequences.

Synthetic ester and biosynthetic base oils are improving performance expectations. Better oxidation stability and cold-flow behavior can reduce buyer hesitation. Suppliers that gain OEM approvals will accelerate adoption.

Price remains disruptive in the opposite direction. Conventional oils are cheaper and well understood. Biodegradable oils must prove total cost value through environmental risk reduction, compliance, drain intervals and equipment protection.

BCG Matrix: Company Evaluation

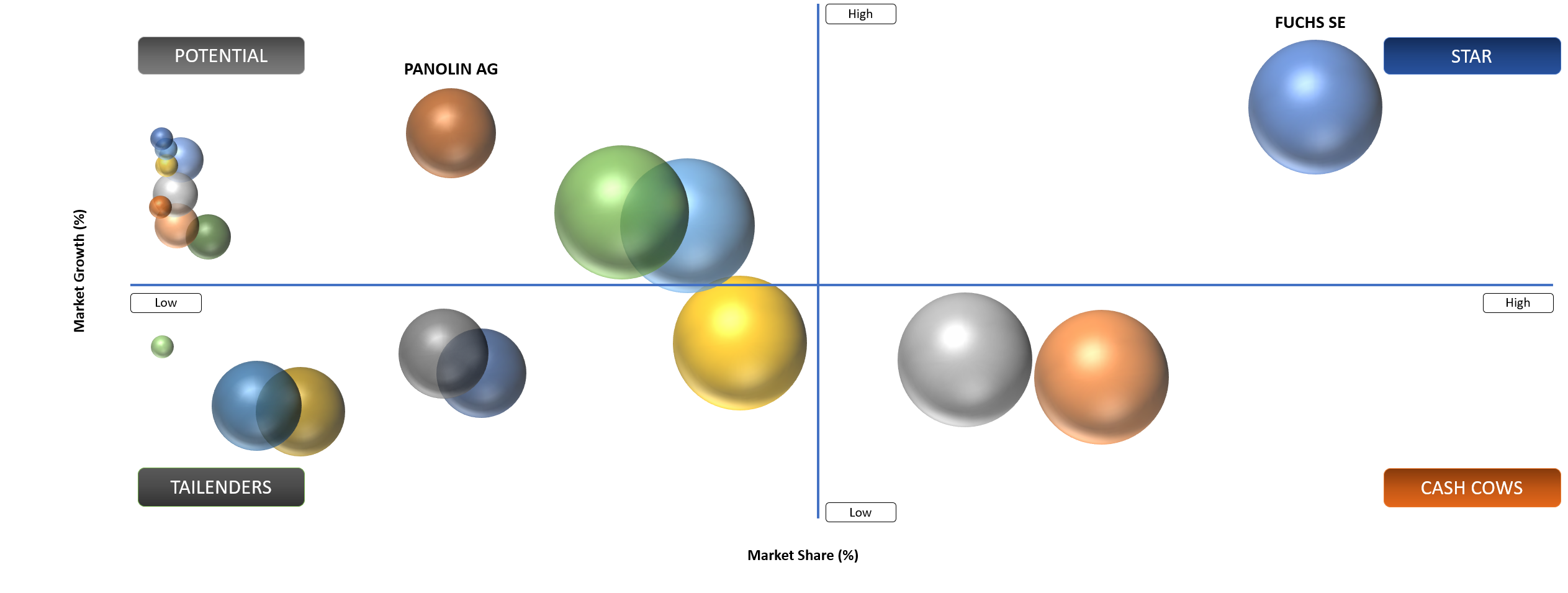

Star

Star players include FUCHS SE, Shell plc, TotalEnergies SE, Chevron Corporation, BP p.l.c., Exxon Mobil Corporation, Panolin AG and Klüber Lubrication. The companies combine formulation depth, technical support and access to industrial and fleet customers.

Potential

Potential players include biosynthetic base oil developers, regional biodegradable lubricant blenders and marine lubricant specialists. Growth depends on certification, field performance, distributor reach and OEM approval progress.

Market Dynamics

Driver Impact Analysis

| Driver | Market Growth Impact | Demand Concentration | Impacted Use Case | Strategic Impact |

Environmental liability drives adoption near waterways | 3.4% | Europe, North America and Japan | Marine and inland waterway engines | Supports premium environmentally acceptable oils |

Forestry and agriculture require lower soil contamination risk | 2.8% | Europe, U.S., Canada and India | Tractors, harvesters and forestry machines | Expands demand in off-road fleets |

Synthetic esters improve product performance | 2.5% | Europe, Japan and North America | Heavy-duty biodegradable engine oils | Reduces performance concerns |

Municipal procurement supports bio-based lubricants | 2.1% | Europe and North America | Public works fleets | Creates stable institutional demand |

Environmental Liability Drives Adoption Near Waterways

Environmental liability is the strongest practical driver because fleets operating near water, forests, farms and public spaces face higher reputational and cleanup exposure when oil leakage occurs. Conventional engine oil spills can create soil and water contamination concerns that are difficult to manage after the event. Biodegradable engine oils become commercially attractive when buyers can connect lubricant selection with reduced spill impact and better environmental risk management.

Marine and inland waterway applications are the clearest demand pocket. Workboats, small vessels, port service equipment and waterway maintenance fleets operate in areas where leakage can immediately affect water quality. Buyers in these applications are not only comparing lubricant price. They are evaluating environmental claims, biodegradation behavior, equipment protection, cold-start performance and availability through marine supply channels.

Forestry and agriculture create similar adoption logic. Tractors, harvesters, forwarders, chippers and irrigation engines often operate directly in soil, crop fields or forest terrain. A small oil leak can become more visible and more sensitive in these settings than in a closed industrial plant. Contractors working on public land, certified forests or near protected watersheds are more likely to consider biodegradable oils because customer contracts and land access rules can influence lubricant choice.

Municipal procurement adds another layer of demand. Public works fleets, park maintenance equipment, landscaping machinery and waterway service vehicles are increasingly expected to demonstrate lower environmental impact. Biodegradable engine oil adoption will grow fastest where public procurement language, spill-risk policies and sustainability reporting move from voluntary preference to documented buying criteria.

Restraint Impact Analysis

| Restraint | Drag On Market Growth | Primary Impact Area | Impacted Use Case | Strategic Impact |

| Premium pricing limits fleet-wide conversion | 3.1% | Price-sensitive fleets | Agriculture and construction | Slows adoption without regulation |

| Limited OEM approvals create buyer hesitation | 2.7% | Heavy-duty engines | Diesel engines and marine engines | Requires longer validation cycles |

| Oxidation stability concerns affect confidence | 2.3% | High-temperature engines | Long-drain applications | Raises need for field trials |

| Limited distributor availability restricts adoption | 1.8% | Emerging markets | Aftermarket sales | Creates regional access gaps |

Premium Pricing Limits Fleet-Wide Conversion

Premium pricing remains the main restraint because biodegradable engine oils rely on specialty base oils and additive systems that cost more than conventional mineral oil products. Synthetic ester formulations can improve performance but add cost, while vegetable oil-based products may be cheaper but may not satisfy demanding engine requirements. Fleet managers therefore compare lubricant cost with engine protection, drain interval, spill exposure and operating conditions.

Many fleets still view biodegradable engine oil as a targeted product for sensitive environments rather than a full fleet replacement. A construction company may adopt it for machines working near water but continue using conventional oil for highway or yard equipment. The selective adoption limits total market penetration even where awareness is improving. Buyers need a clear business case before converting entire fleets.

OEM approval gaps also reinforce price resistance. Buyers are cautious when a biodegradable oil does not have the same approval depth as conventional products. Warranty concerns, drain interval uncertainty and technician familiarity can slow switching. Lubricant suppliers must provide field trial data, used oil analysis support and clear maintenance guidance to reduce hesitation.

Distributor availability can also affect adoption. A fleet may accept premium pricing if the oil is available reliably, but limited regional distribution makes conversion difficult. Emergency top-ups, remote worksites and mixed fleets require practical supply. A high-performing biodegradable oil will struggle commercially if customers cannot obtain it consistently through normal maintenance channels.

Segmentation Analysis

Synthetic Ester-Based Engine Oils Will Continue To Lead Premium Demand

Synthetic ester-based biodegradable engine oils will continue to lead premium demand because they offer a stronger balance of biodegradability, lubricity, thermal stability and low-temperature performance than basic vegetable oil formulations. Engine applications need stable viscosity, oxidation resistance and deposit control. Synthetic esters support these requirements better in heavy-duty and marine engines where operating temperatures and duty cycles are demanding.

Marine and forestry buyers value synthetic ester products because equipment often operates under high load and variable weather conditions. The customers cannot compromise engine protection only to meet environmental goals. A lubricant that supports biodegradation while maintaining drain interval confidence has a stronger chance of adoption. Synthetic esters therefore sit at the premium end of the market.

Product positioning must remain application-specific. A marine diesel engine, forestry harvester and municipal mower do not need the same formulation. Suppliers that offer guidance on viscosity grade, drain interval and used oil analysis can build trust faster than suppliers relying only on biodegradability claims. Field validation remains essential because fleet managers want proof under actual operating conditions.

Marine Engines Are Becoming The Most Visible Adoption Area

Marine engines represent the most visible opportunity because environmental exposure is immediate when equipment operates on or near water. Workboats, port service vessels, inland waterway fleets, dredging support equipment and coastal service engines all carry higher spill sensitivity. Buyers in these applications need engine oils that reduce environmental persistence without weakening engine protection.

Regulatory and customer pressure make marine demand different from normal aftermarket demand. Port authorities, vessel operators and marine contractors may need to show better environmental practices when bidding for projects or operating in sensitive waterways. Biodegradable engine oil can support this positioning when it meets performance needs and is available through marine supply networks.

Growth will depend on approvals and field performance. Marine buyers are cautious because engine downtime is costly and service windows can be limited. Suppliers that offer technical support, emergency availability and used oil monitoring can convert more customers. Marine demand will remain premium and selective, but it can influence broader acceptance across other environmentally sensitive fleets.

Agriculture And Forestry Equipment Create Ground-Level Spill-Risk Demand

Agriculture and forestry equipment creates a different but equally practical demand base. Tractors, harvesters, forwarders, chippers and irrigation engines operate on land where leakage can enter soil, crops, drainage channels or forest floors. Biodegradable engine oils are attractive where operators want to reduce environmental impact and protect contracts tied to sustainable land management.

Forestry contractors are especially relevant because equipment may work near watersheds, public forests or certified forestland. Buyers in these settings may face stricter expectations from landowners, regulators or large customers. Lubricant choice becomes part of a wider environmental-management approach that includes hydraulic fluids, chain oils, greases and engine oils.

Agriculture adoption is more cost-sensitive. Farmers and contractors often work on tight margins, so biodegradable oils must prove value through risk reduction, equipment protection or procurement requirements. Adoption will be stronger among larger fleets, export-oriented farms, organic producers and operators working near water-sensitive land.

Municipal Fleets Support Institutional Demand For Lower-Impact Lubricants

Municipal fleets provide a stable institutional opportunity because public agencies often manage parks, waterways, roadsides, drainage systems and public facilities. Equipment used in these areas can leak oil in places visible to the public. Biodegradable engine oil supports sustainability policies and can reduce concern around spills in high-visibility public spaces.

Public procurement can gradually normalize adoption. Once a city or regional authority writes lower-impact lubricant preferences into tenders, suppliers gain a repeatable route to market. The opportunity is not limited to engine oil because municipalities often review hydraulic fluids, greases and two-stroke oils together. Engine oil can become part of a broader green fleet maintenance package.

Budget pressure remains a constraint. Municipal buyers must justify higher lubricant costs, especially when equipment is older or lightly used. Clear reporting on spill-risk reduction, disposal practices and maintenance performance can help move adoption from pilot use to standard purchasing.

Final Market Segmentation

- By Base Oil Type

- Vegetable Oil-Based Engine Oil

- Rapeseed Oil-Based

- Sunflower Oil-Based

- Soybean Oil-Based

- Castor Oil-Based

- Synthetic Ester-Based Engine Oil

- Saturated Ester-Based

- Complex Ester-Based

- Polyol Ester-Based

- PAG-Based Engine Oil

- Biosynthetic Base Oil-Based Engine Oil

- Blended Bio-Based Engine Oil

- Others

- Vegetable Oil-Based Engine Oil

- By Engine Type

- Diesel Engines

- Heavy-Duty Diesel Engines

- Light-Duty Diesel Engines

- Marine Diesel Engines

- Off-Highway Diesel Engines

- Gasoline Engines

- Two-Stroke Engines

- Four-Stroke Engines

- Hybrid Equipment Engines

- Diesel Engines

- By Viscosity Grade

- SAE 5W-30

- SAE 10W-30

- SAE 10W-40

- SAE 15W-40

- SAE 20W-50

- Others

- By Application

- Marine Engines

- Inland Waterway Vessels

- Coastal Vessels

- Port Service Equipment

- Agriculture Equipment

- Tractors

- Harvesters

- Irrigation Engines

- Forestry Equipment

- Harvesters

- Forwarders

- Chippers

- Construction Equipment

- Excavators

- Loaders

- Compactors

- Mining Equipment

- Municipal Fleets

- Landscaping Equipment

- Industrial Engines

- Others

- Marine Engines

- By Distribution Channel

- OEM Fill

- Aftermarket

- Fleet Contracts

- Distributor Sales

- Online Sales

Geographical Penetration

U.S. Biodegradable Engine Oil Market Landscape

The U.S. market is shaped by marine operations, forestry, agriculture, municipal fleets and environmental procurement. Adoption is strongest where equipment operates near waterways, protected land or public infrastructure. Buyers often require performance evidence before switching.

Federal and state procurement can support bio-based lubricants where environmental policies are active. Municipal fleets use these products in parks, waterways and public works equipment. However, price remains a major barrier for broad aftermarket adoption. Supplier education is important. Fleet managers need assurance on drain intervals, engine cleanliness and warranty compatibility. Used-oil analysis can help build confidence.

India Biodegradable Engine Oil Market Landscape

India is an emerging market where adoption is still early. Agriculture, inland waterways, ports, municipal equipment and construction fleets provide future opportunity. Price sensitivity remains high, so products must demonstrate clear risk reduction or regulatory value.

Agricultural machinery offers long-term potential because oil leakage near soil and crops can create environmental exposure. However, adoption will require affordable formulations and distributor availability. Marine and port equipment may adopt earlier where sustainability standards or international customer requirements apply. Local blending partnerships can improve affordability and access.

Japan Biodegradable Engine Oil Market Outlook

Japan is a premium market where environmental responsibility, marine activity and quality expectations support biodegradable lubricant adoption. Buyers prioritize reliability and technical documentation. Marine and municipal applications are important because equipment often works near sensitive coastal and urban environments. Suppliers need strong certification and performance data. Japanese customers may adopt higher-performance synthetic ester products where quality and reliability justify premium pricing. Long-term supplier trust is important.

Competitive Landscape

- Competition is split between global lubricant companies, specialty biodegradable lubricant brands, bio-based base oil developers and regional lubricant blenders. Global companies compete through technical service, OEM relationships, distributor reach and broad product portfolios. Specialty players compete through biodegradability credentials, marine and forestry expertise, ecolabels and tailored performance claims.

- FUCHS, Shell, TotalEnergies, BP, Chevron, Exxon Mobil, PANOLIN, RSC Bio Solutions, Renewable Lubricants and Klüber Lubrication compete across overlapping lubricant categories. Not every company is focused specifically on biodegradable engine oil, but their broader biodegradable and environmentally acceptable lubricant portfolios influence buyer trust and channel access. Engine oil adoption often starts after customers first convert hydraulic fluids, gear oils or greases in sensitive applications.

- Synthetic ester capability is becoming a key differentiator. Suppliers that can offer better oxidation stability, cold-flow performance and longer drain confidence have stronger positioning in marine, forestry and construction fleets. Vegetable oil-based suppliers may compete in lower-cost or lighter-duty applications but face performance limits in demanding engines.

- Competitive benchmarking should track biodegradability evidence, toxicity profile, OEM approvals, viscosity grade coverage, drain interval data, ecolabel status, used oil analysis support, distributor availability and application-specific field references. Suppliers with credible performance evidence will have a stronger position than brands relying on sustainability language alone.

- FUCHS SE is one of the most important companies in biodegradable lubricants because it serves industrial, automotive, marine and specialty applications with a broad formulation base. Its advantage comes from technical depth, OEM relationships and product development across environmentally sensitive lubrication needs.

- Shell plc participates through advanced lubricant technology, fleet relationships and global distribution. Shell’s strength is its ability to support large customers with technical service, used-oil analysis and performance validation. Its position is important where biodegradable lubricants need to meet heavy-duty operating conditions.

- TotalEnergies SE is relevant through specialty lubricants and industrial lubricant portfolios. The company can serve marine, industrial and fleet customers where environmental performance and equipment protection must be balanced. Its strength comes from global technical service and established customer access.

Key Companies

- FUCHS SE

- Shell plc

- TotalEnergies SE

- Chevron Corporation

- Exxon Mobil Corporation

- BP p.l.c.

- PANOLIN AG

- Klüber Lubrication München SE and Co. KG

- Renewable Lubricants, Inc.

- RSC Bio Solutions, LLC

- LIQUI MOLY GmbH

- Motul S.A.

- Valvoline Inc.

- Petroliam Nasional Berhad

- Idemitsu Kosan Co., Ltd.

- ENEOS Corporation

- Repsol S.A.

- Phillips 66 Company

- Quaker Houghton

- Morris Lubricants

Major Pain Points

- Premium pricing limits fleet-wide conversion when regulation or customer contracts do not require biodegradable oil.

- OEM approval gaps create hesitation among fleet managers responsible for warranty and engine reliability.

- Oxidation stability concerns remain in high-temperature engines and long-drain applications.

- Vegetable oil-based products can face cold-flow and thermal stability limitations in demanding duty cycles.

- Distributor availability is uneven in emerging markets and remote work zones.

- Mixed fleets create maintenance complexity when some equipment uses biodegradable oil and some uses conventional oil.

- Fleet technicians may resist switching if product handling, labeling and drain guidance are unclear.

- Biodegradable claims require documentation because buyers need proof on biodegradation, aquatic toxicity and environmental performance.

- Used oil disposal practices can reduce the environmental benefit if fleets do not manage waste streams properly.

- Price-sensitive agriculture and construction operators need stronger evidence before paying a premium.

Recent Developments

- May 2026: FUCHS expanded customer-facing communication around its PLANTO biodegradable lubricant portfolio for environmentally sensitive machinery applications, supporting demand from forestry, agriculture, waterway and municipal fleet operators.

- February 2026: PANOLIN strengthened its positioning in biodegradable and environmentally acceptable lubricant solutions for construction, forestry, marine and hydropower equipment where spill risk and environmental compliance remain high procurement priorities.

- November 2025: RSC Bio Solutions expanded market support for its biodegradable lubricant portfolio across marine, industrial and offshore applications, reinforcing demand for environmentally acceptable lubricants used near water and sensitive operating zones.

- June 2025: Nandan Petrochem’s Velvex expanded its lubricants and AdBlue market presence at Excon 2025, strengthening visibility with construction equipment fleets and off-highway vehicle buyers that are gradually reviewing lower-impact lubricant options.

- March 2025: Renewable Lubricants continued promoting bio-based lubricant formulations for engine, hydraulic, gear and industrial applications, supporting demand from fleets looking to reduce petroleum-based lubricant exposure in sensitive environments.

Analyst View And Opinion

- Biodegradable engine oil will remain a premium specialty market rather than a universal replacement for conventional engine oil during the forecast period.

- Marine, forestry, agriculture and municipal fleets will remain the strongest adoption areas because operating environments create visible soil and water exposure.

- Synthetic ester-based formulations will gain share where fleet managers require biodegradability and engine protection under demanding duty cycles.

- Vegetable oil-based products will retain a role in lighter-duty or cost-sensitive applications, but performance limitations will restrict adoption in high-load engines.

- OEM approvals, field trial data and used oil analysis will decide adoption speed because fleet managers need proof before changing engine maintenance practices.

- Europe will remain the most mature market because environmental procurement and eco-labelled lubricants are more established.

- Asia-Pacific will grow from a smaller base as ports, inland waterways, municipal fleets and agriculture operators face stricter sustainability expectations.

- Public-sector procurement can create repeatable demand if tenders include lower-impact lubricant preferences for parks, waterways and municipal equipment.

- Biodegradable engine oil suppliers should position the product around environmental risk reduction and uptime protection rather than sustainability language alone.

- Strategic partnerships with equipment distributors and maintenance service providers will be important because end-users need practical access and technical guidance.

Target Audience

| Industry | Who Should Buy This Report? | Reason To Buy This Report |

| Lubricant Manufacturers | Product Managers, Strategy Teams | Identify biodegradable formulation opportunities |

| Marine Operators | Fleet Managers | Evaluate environmentally acceptable engine oil options |

| Agriculture and Forestry | Equipment Owners, Procurement Teams | Assess oil options for sensitive operating environments |

| Municipal Fleets | Sustainability and Procurement Teams | Support bio-based procurement programs |

| Base Oil Suppliers | Technical Sales Teams | Track demand for ester and biosynthetic base oils |

| Investors | Specialty Chemicals Investors | Evaluate premium lubricant growth pockets |

What DataM Intelligence Uniquely Provides

- DataM Intelligence maps biodegradable engine oil demand by sensitive operating environment, including marine waterways, forests, agriculture fields, municipal public spaces and construction zones near water.

- DataM Intelligence separates vegetable oil-based, synthetic ester-based, PAG-based and biosynthetic formulations so clients can evaluate performance and pricing by base oil route.

- DataM Intelligence compares biodegradable engine oil with conventional mineral and synthetic engine oils across drain interval, oxidation stability, cold-flow performance, toxicity profile and total cost of ownership.

- DataM Intelligence provides procurement intelligence covering OEM approval gaps, ecolabel needs, distributor availability, field trial requirements and used oil analysis adoption.

- DataM Intelligence supports supplier benchmarking across biodegradability evidence, toxicity data, viscosity range, technical service, field validation and regional distribution strength.

- DataM Intelligence evaluates pricing pressure by base oil cost, additive complexity, certification cost, production scale and channel margin.

- DataM Intelligence helps clients identify where biodegradable engine oil is a mandatory compliance purchase, where it is a risk-reduction purchase and where adoption remains discretionary.