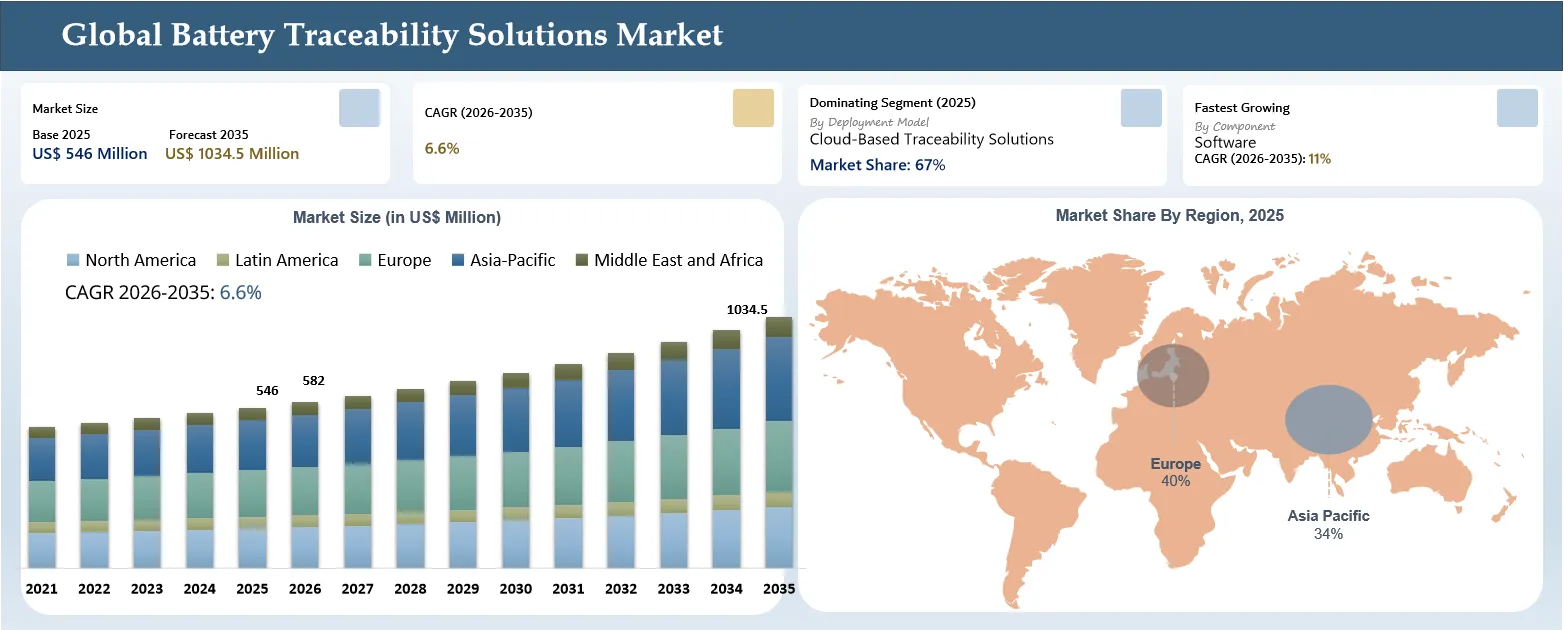

Battery Traceability Solutions Market Size & Forecast 2035

The global Battery Traceability Solutions market reached USD 546 million in 2025 and is expected to reach USD 1034.5 million by 2035, growing with a CAGR of 6.6% during the forecast period 2026-2035, due to increased demand for end-to-end visibility in battery supply chains in light of fast-growing markets of electric vehicles, energy storage systems, and lithium-ion battery production. Battery traceability systems allow secure tracking of raw materials, battery components, production processes, performance, and recycling of batteries using digital battery passports, blockchain, Internet-of-things-based systems, and other advanced information management solutions. Increased focus on responsible sourcing of critical minerals, legislation requiring lifecycle traceability of batteries and sustainability reporting are expected to drive adoption among automotive companies, battery manufacturers, recyclers and energy storage companies. Such solutions are helpful for improving supply chain visibility, carbon footprint tracking, regulatory compliance and circular management of batteries. Companies are becoming more and more interested in implementing advanced traceability solutions that will help them authenticate materials used, optimize recycling process and improve battery ecosystem visibility. Some problems related to a lack of standardized data and technology complexity could prevent market development.

Key Takeaways

- The primary driver is regulatory demand for battery passports that have an influence on the market by 35%, since the annual production of batteries in Europe is over 800 GWh and more than 17 million EVs were sold worldwide in 2024.

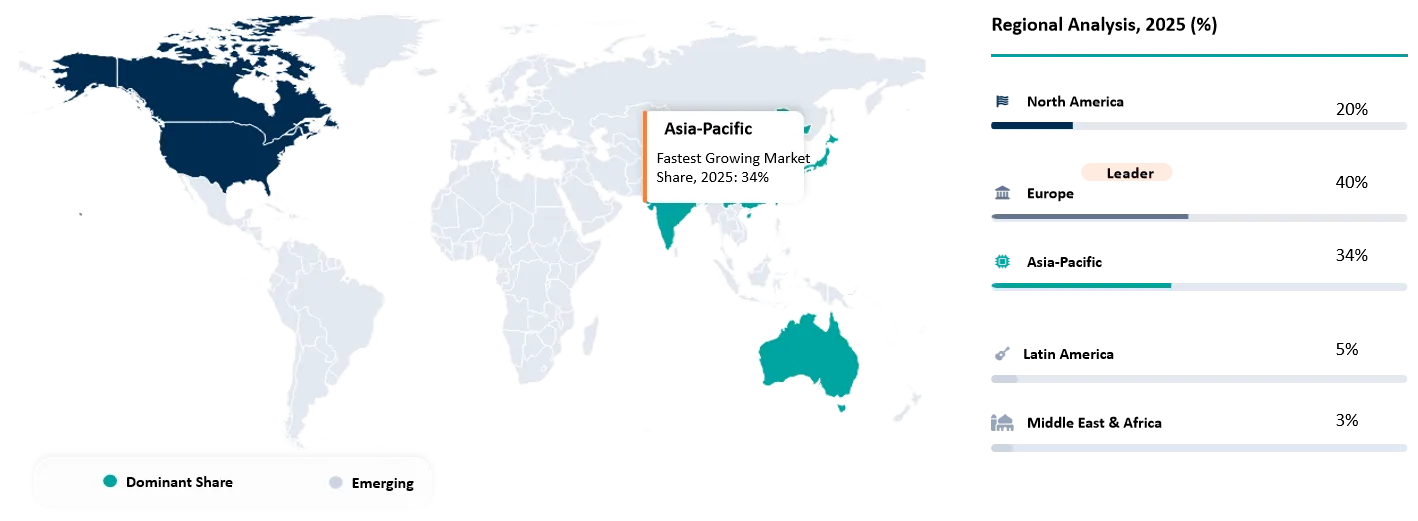

- Europe is dominating the market with a market share of 40% in 2025, because of the EU Battery Regulation that requires batteries to have digital passports by February 2027. The Asia-Pacific region is the fastest-growing.

- The battery passport regulations have the most significant growth influence at 35%, whereas end-of-life lifecycle management has an impact at 25%, blockchain technology integration at 20%, and IoT/BMS data tracking at 17%.

- By 2030, battery cell production capacity within Germany and France will be more than 300 GWh and 150 GWh respectively, whereas the overall production capacity announced in Europe will be above 1.8 TWh.

Battery Traceability Solutions Market Industry Trends and Strategic Insight

- Regulations such as the European Union’s Battery Regulation are forcing the implementation of digital battery passports by requiring companies to keep accurate records about the content, carbon footprint, and lifecycle of batteries.

- Geopolitical risks and dependence on highly concentrated mineral resources have resulted in an effort to implement tracing systems for tracking the origin, pathway, and ecological footprint of their raw materials.

- The implementation of AI and machine learning is becoming common in traceability systems for the prediction of battery degradation, optimization of recycling/reuse, and generation of insights into quality and efficiency.

- Integrating IoT sensor technology, along with the embedded BMS systems, is now providing real-time data on temperature, health, and utilization of the batteries for use in traceability programs.

- Battery traceability is transforming from merely being a compliance activity into a key digital layer that forms the base for transparency, circularity, and creation of value throughout its lifecycle. Leadership in the market space would require having interoperable platforms, advanced analytics capabilities, and flexibility to adapt to global regulations.

Battery Traceability Solutions Market Scope

| Metrics | Details | |

| 2025 Market Size | USD 546 Million | |

| 2035 Projected Market Size | USD 1034.5 Million | |

| CAGR (2026-2035) | 6.6% | |

| Largest Market | Europe | |

| Fastest Growing Market | Asia-Pacific | |

| By Component | Software, Hardware, Services | |

| By Technology | Blockchain, Internet of Things (IoT), Artificial Intelligence & Machine Learning (AI/ML), Cloud Computing, Digital Twin, RFID, QR Code/Barcode, Near Field Communication (NFC), Others | |

| By Deployment Mode | Cloud, On-Premises, Hybrid | |

| By Battery Type | Lithium-ion Batteries, Sodium-ion Batteries, Lead-acid Batteries, Nickel-based Batteries, Solid-state Batteries, Others | |

| By Traceability Stage | Raw Material Sourcing, Component Manufacturing, Cell Manufacturing, Battery Pack Assembly, Logistics & Distribution, In-use Monitoring, Second-life Applications, Recycling & End-of-Life, Others | |

| By Application | Electric Vehicles (EVs), Battery Energy Storage Systems (BESS), Consumer Electronics, Industrial Equipment, Aerospace & Defense, Marine, Medical Devices, Power Tools, Others | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

Battery Traceability Solutions Market Disruption Analysis

Data Standardization and Interoperability Challenges Reshaping Battery Traceability Ecosystems

The disruption in the Battery Traceability Solutions Market is becoming more and more tied to the issue of non-standardized data and interoperability frameworks across the entire global battery value chain. As the technologies that support battery traceability shift from being just tools for complying with regulations towards becoming digital ecosystems, the difficulty of sharing consistent and credible lifecycle data by all parties involved, including mining companies, refiners, battery makers, automotive OEMs, logistics companies, secondary use organizations, and recyclers, becomes increasingly apparent. The incompatibility of data architectures, non-interoperable software solutions, and inconsistent reporting are causing issues and raising costs when implementing battery traceability solutions across the battery value chain. According to the Global Battery Alliance (GBA), battery passports will need standardized and comparable data structures to have truly circular battery value chains.

In response, battery manufacturers, software providers, and automakers are restructuring their data management approaches, putting in place new data infrastructure that is built on the foundation of an open approach, standard battery data models, and cross-platform traceability capabilities. Global industry initiatives like the Global Battery Alliance Battery Passport Program and the Catena-X Battery Passport Standard are facilitating the process of developing unified approaches to data exchange. For example, the pilots carried out by the Global Battery Alliance under the initiative included the participation of battery manufacturers that made up over 80% of the global EV batteries market.

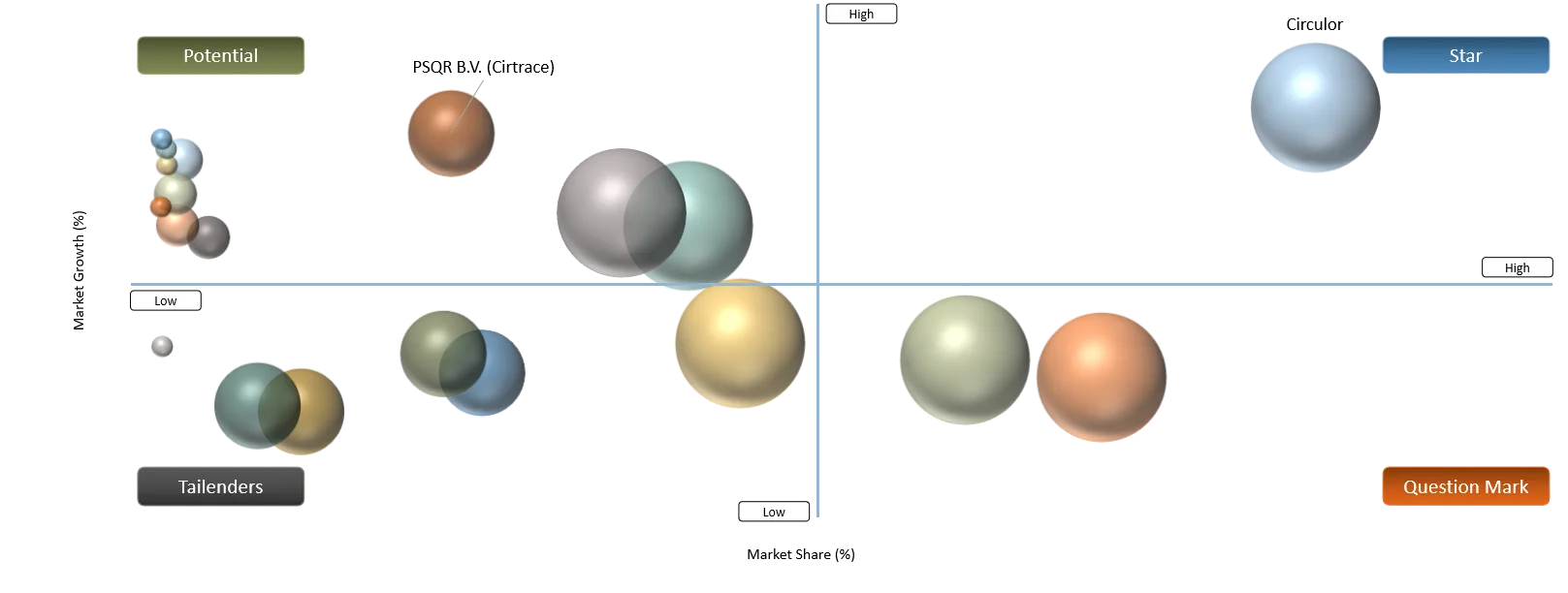

Battery Traceability Solutions Market BCG Matrix: Company Evaluation

Stars include Circulor, Minespider GmbH, Siemens AG, and SAP SE as they offer high market visibility, presence of battery traceability solutions, and active participation in developing digital battery passports, which are essential amid the battery regulation changes. The stars mentioned above have managed to get partnerships with battery makers, automobile original equipment manufacturers, and suppliers of minerals. Question Mark companies such as OPTEL Group, AVL List GmbH, IBM Corporation, Circularise B.V., and Kezzler AS are selected due to their evident technological competencies and usage within battery traceability solutions; however, they are at the same time relatively new players in the marketplace dominated by enterprise software and battery passport solution suppliers.

Potential Leaders include PSQR B.V. (Cirtrace), Bosch Connected Industry, Tata Elxsi Ltd., and Infosys Limited. These companies stand to gain from rising demands for battery passports, traceability of manufacturing, and digitized supply chain services. The strengths of these firms include industrial digitization, engineering know-how, and business integration capabilities, although their offerings in the battery traceability space are still comparatively early in the process of commercialization. Tailenders in the industry consist of companies like Accenture plc, Wipro Limited, as well as emerging battery traceability service providers that provide their services mostly for consultation and digital transformation of their clients.

Battery Traceability Solutions Market Market Dynamics

Driver Impact Analysis

| Driver | Market Growth Impact (%) | Demand Concentration | Impacted Use Case | Strategic Impact |

Blockchain technology and distributed ledger technology have become increasingly popular in the domain of tracking batteries due to their unalterable and transparent nature, which fosters trust and allows multi-stakeholder data sharing. | 20% | High among battery manufacturers, automotive OEMs, critical mineral suppliers, and recycling networks

| Material provenance verification, digital battery passports, ESG compliance, supplier authentication | Establishes trusted chain-of-custody records, improves data integrity, reduces fraud risk, and enables cross-enterprise traceability ecosystems |

Increasing deployment of IoT sensors and battery management systems, traceability systems have been receiving an abundance of operational data. | 17% | High among EV battery manufacturers, energy storage operators, fleet managers, and industrial battery users | Battery health monitoring, lifecycle analytics, predictive maintenance, second-life assessment | Enables real-time battery intelligence, enhances lifecycle optimization, and supports data-driven asset management strategies |

Regulations for the battery passport are generating massive demand for traceability systems and the exchange of data. | 35% | Very High across battery manufacturers, automotive OEMs, suppliers, logistics providers, & recyclers | Regulatory compliance, battery passports, carbon footprint reporting, lifecycle documentation | Acts as the primary market catalyst by making battery traceability a mandatory requirement, accelerating platform adoption and digital infrastructure investment |

The increasing number of end-of-life batteries is driving the need for lifecycle management systems to facilitate collection, reconditioning, second-life applications, and recycling. | 25% | High among recyclers, battery manufacturers, EV OEMs, and energy storage companies | Battery collection, refurbishment, second-life deployment, recycling and material recovery | Strengthens circular economy models, improves recovery efficiency of critical minerals, and supports sustainable battery value chains |

Regulations for the battery passport are generating massive demand for traceability systems and the exchange of data.

The advent of battery passports regulation is proving to be the key factor driving the deployment of battery traceability solutions across the world. Regulatory requirements are demanding that battery manufacturers, automotive OEMs, and participants in their supply chains deploy digital solutions that are able to track details such as battery materials, manufacturing process, carbon footprint information, percentage of recycled materials, past performance information, and end-of-life disposal paths. In accordance with the European Union Battery Regulation, all industrial and electric vehicle batteries offered on the EU market should have a digital battery passport starting from February 2027. The increasing need for traceability platforms that will be able to gather, authenticate, manage, and share data throughout battery ecosystem lifecycles is arising because of this requirement. According to the European Commission, the yearly battery production capacity in Europe exceeds 800 GWh.

Meanwhile, there has been an acceleration in the growth of electric vehicle manufacturing and batteries. In 2024, there were more than 17 million electric vehicles sold globally, which comprised more than 20% of the total vehicles sold in the world, while battery demand crossed 1 TWh for the first time ever. For instance, in November 2025, New Electronics highlighted that the adoption of EU Battery Passport legislation was spurring increased demand for battery traceability solutions as firms began to adopt cell-level data tracking capabilities in order to comply with and adhere to the requirements.

Restraint Impact Analysis

| Restraint | Drag on Market Growth (%) | Primary Impact Area | Impacted Use Case | Strategic Impact |

Lack of universal standards for data has led to increased complexity and higher costs in integration, while also restricting data coherence between miners, OEMs, and recyclers. | 10% | Data Interoperability & Regulatory Compliance | Battery Passport Management, Supply Chain Traceability, Lifecycle Data Exchange | Delays large-scale deployment, increases implementation costs, and slows the development of unified battery traceability ecosystems. |

The multi-layered and geographically widespread structure of battery value chains makes it practically hard to gather, verify, and keep accurate data for all of the suppliers involved. | 9% | Supply Chain Visibility & Data Verification | Raw Material Traceability, Supplier Monitoring, ESG Reporting | Reduces transparency across battery supply networks and creates challenges in maintaining end-to-end traceability and compliance. |

The rapid increase in the production of EVs and battery storage units creates vast amounts of data in their lifecycle that require a robust digital architecture to handle and analyze. | 7% | Data Infrastructure & Scalability | Battery Lifecycle Management, Battery Health Monitoring, Digital Battery Passports | Increases infrastructure investment requirements and creates scalability challenges for traceability platform providers. |

Inconsistencies in digital preparedness within the supply chain, specifically the upstream mining and raw materials suppliers, lead to critical data gaps and hinder end-to-end visibility. | 8% | Digital Adoption & Data Collection | Critical Mineral Provenance Tracking, Responsible Sourcing Verification, Supplier Compliance | Creates information gaps in battery passports, weakens traceability reliability, and limits full lifecycle transparency. |

Lack of universal standards for data has led to increased complexity and higher costs in integration, while also restricting data coherence between miners, OEMs, and recyclers.

One of the challenging hurdles limiting the expansion of the Battery Traceability Solutions Market is the lack of universally accepted data standards and interoperability models throughout the entire battery lifecycle. The traceability of batteries relies on the smooth flow of information between mining companies, material processors, battery makers, vehicle manufacturers, logistics firms, second-life operators, and recyclers. Nevertheless, the data associated with batteries is stored in disparate enterprise systems and software applications, which leads to major integration difficulties and higher implementation costs. In light of the growing pressure from the battery passport regulations, the industry players are facing the necessity to make considerable investments into data mapping and system integration efforts ahead of the implementation of traceability solutions due to the lack of standardized data models. Moreover, the global deployment of electric vehicle batteries had risen to about 1.2 TWh by 2025, experiencing almost a 30% growth compared to last year, according to the IEA, which only served to highlight the need for standardization of lifecycle data in order to exchange such data within international value chains.

Fast-growing production of batteries and fragmented digital systems are raising compliance and implementation costs and delaying the process of creating a traceability system for batteries. For instance, in November 2025, according to Proactive Investors, there is a need for interoperable digital product passports due to fragmented traceability systems for batteries within the European Union, the United States, and China, to overcome issues related to compliance and data sharing.

Battery Traceability Solutions Market Segment Analysis

The global Battery Traceability Solutions market is segmented based on solution type, technology, component, deployment model, application, end-use, and region.

Cloud-Based Traceability Solutions Dominating Deployment Models Through Scalability and Cross-Value-Chain Data Connectivity

Cloud-based traceability solutions remain the key segment in the deployment model of the Battery Traceability Solutions Market because of their capability of aggregating data in bulk, exchanging information in real time, and ensuring connectivity in the complex battery value chain. The requirements for centralized solutions that can manage the data related to battery passports, carbon footprint, material origins, and lifecycle are increasingly felt by battery producers, automotive OEMs, material suppliers, logistic companies, and recyclers. The deployment model based on on-premise architecture does not offer similar advantages compared to the cloud-based model. The increasing quantity of battery data is adding even more pressure on the need for cloud infrastructure systems.

As stated by the International Energy Agency (IEA), the battery demand in 2025 exceeded 1.3 TWh and is expected to grow quickly until 2026. The EU Battery Regulation will require digital battery passports for electric vehicle batteries and industrial batteries as of February 2027, forcing companies in the market to develop platforms that can manage large amounts of data. This confluence of increased battery production, intensifying data requirements, and mandated digitalization makes cloud-based traceability systems a lucrative solution and the market leader in the Battery Traceability Solutions Market.

Battery Traceability Solutions Market Geographical Penetration

Regulatory Leadership and Battery Passport Implementation Driving Europe’s Dominance in the Battery Traceability Solutions Market

Europe region dominates the regional market for battery traceability technology on account of its pioneering legislation and sustainable practices, with a market share of 40% in 2025, as well as digital battery passports. Europe has set the highest standards for battery transparency through the European Union Battery Regulation, which requires tracking throughout the product life cycle, carbon footprint assessment, reporting of recycled materials, and implementation of battery passports in electric vehicles and industry batteries. Such measures have prompted significant investment in digital traceability solutions, blockchain-based data exchange platforms, and battery life cycle management technologies within the automotive, battery production, and recycling industries. The presence of leading automakers, battery gigafactories, and circular economy programs has enhanced Europe's leadership position in battery traceability. Regional supremacy is bolstered by fast-growing battery manufacturing and digitization driven by regulation. Based on estimates by the European Commission, over 1.8 TWh of capacity for the manufacture of battery cells has been announced in Europe by 2030, with a large proportion being put into production between 2025 and 2026.

In 2025, Europe was responsible for about 20% of global sales of electric vehicles, and investments in batteries continued to exceed €180 billion, which created demand for traceability systems able to track material origin and life cycle management. For instance, in June 2026, CeLLife Technologies, a Finnish-based battery analytics and battery lifecycle intelligence company, raised USD 4.6 million in funding to deploy its battery analytics platform in Europe and North America. This funding will be utilized for expanding the capabilities of battery analytics, battery traceability, and battery passports.

Germany Battery Traceability Solutions Market Trends

Germany holds the leading share in the European Battery Traceability Solutions Market due to its vast network of automobile manufacturing industry, heavy investments in battery production facilities, and adoption of battery passport schemes and supply chain transparency programs. Some of the largest players in Europe in terms of the automotive and battery industry are located in Germany, and these players are currently implementing traceability solutions in order to meet the requirements of the European Union Battery Regulation and increase lifecycle traceability within battery value chains. These trends in Germany have been supplemented by programs like Catena-X, where battery producers, automakers, suppliers, and recyclers exchange their data in a standardized way. According to the European Automobile Manufacturers' Association (ACEA), in 2025, Germany registered about 27% of all battery electric vehicles in the European Union, retaining the leadership among EV markets in the region. In addition, in 2030, there is forecasted to be more than 300 GWh per year of battery cell manufacturing capacity installed in Germany, with most installations taking place in 2025-2026.

For instance, in October 2025, Minespider, a German-based company that provides traceability and provenance services for batteries and minerals, partnered with MineHub Technologies, a Canada-based digital supply chain platform provider, to connect their platforms and improve traceability, provenance, and digital product passports for batteries and critical minerals. This partnership will help satisfy the increasing regulatory demands for transparency and sustainability in supply chains in Europe.

France Battery Traceability Solutions Market Outlook

France is emerging as an player in the European Battery Traceability Solutions Market owing to the rising investments in the manufacture of batteries, high-level support from the French government for battery value chains to get localized, and increased use of digital traceability systems. The country is establishing itself as one of the most important pillars in the battery ecosystem of Europe by means of setting up big gigafactories, battery recycling projects, and getting involved in the EU battery passports programs. The availability of battery manufacturing companies, automobile Original Equipment Manufacturers (OEMs), and industrial technology firms is leading to the establishment of traceability systems that will allow tracking the material of batteries, the production process of batteries, carbon footprint data, and end-of-life management activities. As per the government of France and the European Battery Alliance, France is expected to provide in excess of 150 GWh of annual production capacity for batteries by 2030, with various large-scale projects progressing towards commercialization and scaling stages in 2025-2026.

Furthermore, France registered one of the largest markets for electric vehicles in Europe, with registrations for battery electric vehicles crossing the 290,000 mark in 2025. For instance, in March 2025, EODev, a French-based company that develops hydrogen fuel cell power systems, acquired EVE System, a French-based battery management and diagnostics technology company, to boost its battery monitoring, lifetime management, and energy storage analytics.

Battery Traceability Solutions Market Competitive Landscape

- There are three major participant groups in the market battery passport and traceability platform vendors, industrial software and digital manufacturing solutions vendors, and consulting and system integration companies. Among the leaders in the development of battery passports, blockchain-based traceability and supply chain transparency technologies are Circulor, Minespider GmbH, Circularise B.V., Kezzler AS and PSQR B.V. (Cirtrace). Among the leaders providing industrial software and manufacturing execution systems to improve battery traceability are such companies as Siemens AG, SAP SE, IBM Corporation, Bosch Connected Industry, AVL List GmbH. Tata Elxsi Ltd., Infosys Limited, Accenture plc, and Wipro Limited specialize in implementation and integration services, which makes the market a very ecosystem-oriented one, in which the level of regulatory readiness, interoperability, digital battery passport technology, and battery lifecycle data management play an important role.

- Key players include Circulor, Minespider GmbH, Siemens AG, AVL List GmbH, OPTEL Group, SAP SE, IBM Corporation, Circularise B.V., Kezzler AS, PSQR B.V. (Cirtrace), Tata Elxsi Ltd., Infosys Limited, Accenture plc, Wipro Limited, and Bosch Connected Industry.

Key Developments

- April 2025: Powin, a U.S.-based company that provides energy storage system integration services, entered into a collaboration with Circulor, a UK-based supply chain traceability solutions company, to utilize digital battery passports in utility-scale energy storage systems.

- March 2026: CATL and BMW Group have entered into an agreement, an MoU, for the progress of pilot projects related to battery passports with respect to cross-border data sharing and carbon footprint traceability via the Catena-X ecosystem.

- May 2025: Acculon Energy selected Rockwell Automation and Circulor to integrate a battery traceability and digital battery passport system into their battery manufacturing process.

- October 2025: Evolium Technologies, Cling Systems, and Traced announced a partnership across Europe for improved traceability of lithium batteries using Digital Product Passports (DPP).

- April 2025: NTT DATA successfully demonstrated interoperability between the Japanese Battery Traceability Platform and the European Catena-X system. This helped to achieve a secure exchange of battery-related information between Japan and Europe, including cross-border battery data exchange, product carbon footprint exchange, and battery traceability standardization throughout the battery life cycle.

- February 2026: Circularise, a Netherlands-based company that specializes in the provision of traceability technology services along the supply chain, joined as a partner of BatteryPass-Ready, a program geared towards getting ready for the EU Battery Passport. This partnership is aimed at improving secure data exchange, digital product passports, and battery life cycle traceability within the supply chain.

- December 2025: The Stakeholder Engagement Programme for Battery Pass-Ready was initiated to assist battery makers, suppliers, recyclers, and technology providers in getting ready for EU Battery Passport regulation.

Key Procurement Priorities and Buyer Evaluation Criteria

- Companies deploying Battery Traceability Solutions have begun making decisions about technology suppliers depending on whether they can offer solutions that guarantee the complete traceability of batteries throughout their lifecycle, including the secure tracing of raw materials, battery cells, manufacturing, use, recycling, and compliance reporting.

- The procurement decision-making process is becoming more and more affected by the increasing use of battery passports, digital product passports (DPPs), the EU Battery Regulation, and sustainability reporting, necessitating solutions that enable standardized data collection, validation, and exchange in the battery value chain.

- The buying companies judge the suppliers according to their abilities for accuracy in data, ability to interoperate with enterprise systems already in use, secure data exchange, distributed ledger technology, connection with the network of the suppliers, and real-time visibility of miners, battery producers, and recyclers.

- Organizations will be assessed according to their industry relations, technological competence, deployment experience, scalability, and potential to support future battery technology such as advanced lithium-ion batteries, future generation batteries, and energy storage systems.

Why Choose DataM?

- Technological Innovations: Focuses on developments in battery traceability techniques through battery passport systems, digital twin technology, artificial intelligence-based tracking, blockchain-powered database management, RFID tags, QR codes, Internet of Things-based tracking, and cloud computing-based lifecycle management.

- Product Performance & Market Positioning: An assessment of the unique capabilities of leading solutions providers in offering end-to-end traceability, data precision, integration, regulatory compliance, analytics, and scalable software architecture in serving the needs of battery manufacturers, electric vehicle OEMs, energy storage providers, and recyclers.

- Real-World Evidence: Illustrates practical implementations of battery traceability solutions in electric cars, stationary batteries, battery recycling centers, and battery manufacturing plants. Shows practical benefits, including better compliance with regulations, supply chain transparency, counterfeiting protection, predictive maintenance, and better critical battery material recovery.

- Market Updates & Industry Changes: Traces all industry developments such as implementation of battery passport system, development of global battery standards, digital supply chain solutions, strategic technology alliances, investment in traceability systems and creation of battery recycling ecosystems in Europe, North America, and Asia-Pacific region.

- Competitive Strategies: Discusses how some of the major companies improve their market position using analytics based on artificial intelligence, blockchain technology, cloud traceability systems, partnerships with battery makers and automobile makers, acquisitions, and digital lifecycle management.

- Pricing & Market Access: Describes reasons for different pricing due to deployment methods, features provided by the software, difficulty of integrating with the existing systems, battery capacity, and subscription models, as well as evaluates market availability via enterprise software companies, battery management software providers, industrial IoT platforms, and technology collaborations.

- Market Entry & Expansion: Points out the growth prospects due to strict battery regulation, high volumes of EV production, efforts for circular economy, use of batteries in their second life, and critical minerals recycling programs, among others, along with growth strategies like regulatory harmonization across regions, cloud deployment, partnering with ecosystems, and lifecycle intelligence through AI.

Target Audience 2026

- Battery Manufacturers and Cell Producers

- Automotive OEMs and Electric Vehicle Manufacturers

- Critical Mineral Suppliers and Miners

- Energy Storage System (ESS) Providers

- Battery Recyclers and Second-Life Operators

- Logistics and Supply Chain Service Providers

- Technology and Software Providers