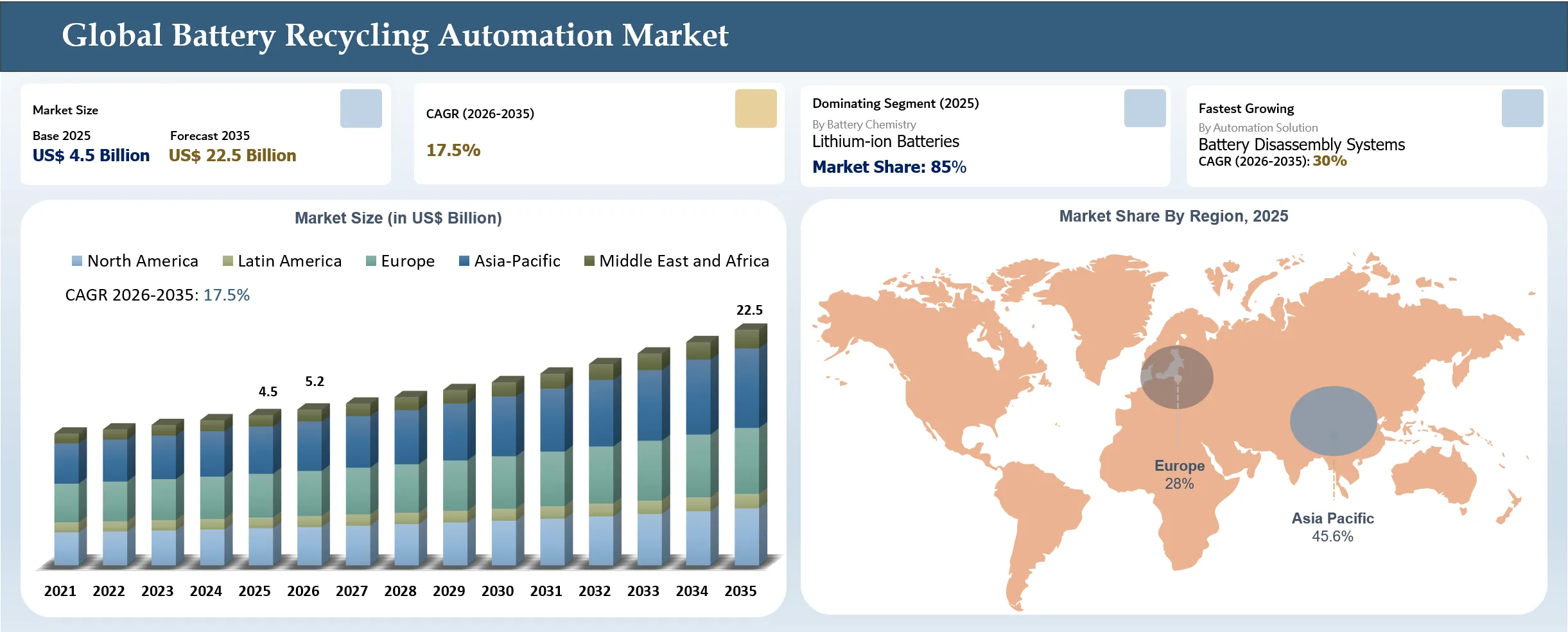

Battery Recycling Automation Market Size

The global battery recycling automation market reached US$ 4.5 billion in 2025 and is expected to reach US$ 22.5 billion by 2035, growing with a CAGR of 17.5% during the forecast period 2026-2035, due to the fast growth in the market owing to an increase in the use of automated battery recycling systems to address the growing demand for recycled lithium-ion batteries arising from their end-of-life stage in electric vehicles, consumer electronic devices, and energy storage applications. Technologies for advanced automation like robots, artificial intelligence, machine vision, automated disassembly systems, and sensor technology for sorting materials have enabled improvements in the efficiency, safety, and yield of critical battery materials such as lithium, nickel, cobalt, and graphite in the recycling process. Automating the battery recycling process has gained momentum among manufacturers and recyclers owing to the need to set up closed-loop battery supply chains, reduce dependence on virgin raw materials, and meet battery recycling regulations. However, some of the major challenges that continue to influence the growth in the market include capital intensity and difficulties in automating different types of battery chemistries and standardizing batteries.

Key Takeaways

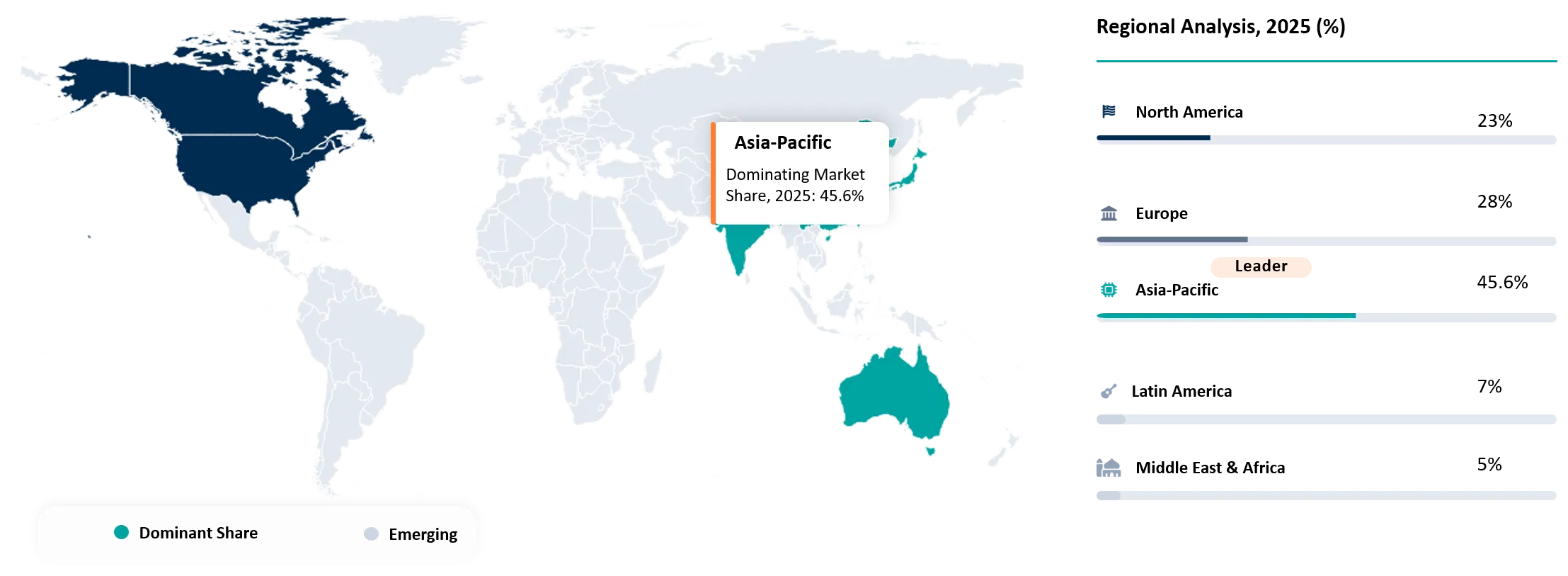

- Asia-Pacific is the dominant market, holding 45.6% of the total revenue share in 2025. This can be attributed to the existence of strong manufacturing capability in EVs, as well as extensive circular economy initiatives of governments.

- Retired power battery waste production in China is predicted to amount to 1.04 million tons by 2025. This will jump up to 3.5 million tons by 2030, with more than 150 licensed recyclers in China serving the purpose.

- Incorporation of specialized robots in battery disassembly contributes significantly towards the growth of the industry, with its growth rate standing at 30%. It is an automated process that significantly increases disassembly rates and improves the safety of employees.

- The lithium-ion battery technology division was highly dominant in the market by holding a 85% market share in the year 2025. This dominance has been due to the large application of batteries in various devices.

Battery Recycling Automation Market Industry Trends and Strategic Insight

- The battery recycling companies are moving away from manual labor-intensive methods towards automated systems that are able to manage batteries in packs, modules, and cells.

- AI-based machine vision systems have become an essential technology trend for automated battery recycling plants since they allow for real-time battery chemistry, battery package, battery cell, and dangerous materials recognition.

- Due to their complex nature and varied designs, there is an increased demand for the use of robotic technology in depowering, removing casings, extracting modules, and separating cells of EV batteries.

- Sensor-based sorting systems that are becoming more advanced to achieve higher efficiency in materials recovery. In battery recycling automation systems, sensor technology applications such as X-rays, spectroscopy, and electrical characterization systems are increasing.

- The increasing commercial use of electric cars is necessitating the development of recycling facilities that have automated processing capabilities.

- Differences in battery chemistry, form factors, packaging, and proprietary designs from manufacturers are increasing the need for flexible automation platforms.

Battery TIC Market Scope

| Metrics | Details | |

| 2025 Market Size | US$ 4.5 Billion | |

| 2035 Projected Market Size | US$ 22.5 Billion | |

| CAGR (2026-2035) | 17.5% | |

| Largest Market | Asia Pacific | |

| Fastest Growing Market | Europe | |

| By Component | Hardware, Software, Services | |

| By Automation Level | Semi-Automated, Fully Automated | |

| By Automation Solution | Battery Sorting & Identification Systems, Battery Discharging Systems, Battery Disassembly Systems, Material Handling Systems, Shredding & Crushing Systems, Material Separation & Recovery Systems, Inspection & Quality Control Systems, Others | |

| By Battery Chemistry | Lithium-ion Batteries, Lead-acid Batteries, Nickel-based Batteries, Sodium-ion Batteries, Others | |

| By Recycling Process | Mechanical Recycling, Hydrometallurgical Recycling, Pyrometallurgical Recycling, Direct Recycling, Others | |

| By End User | Dedicated Battery Recyclers, Battery Manufacturers, Automotive OEMs, Electronics Manufacturers, Metal & Material Recovery Companies, Others | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

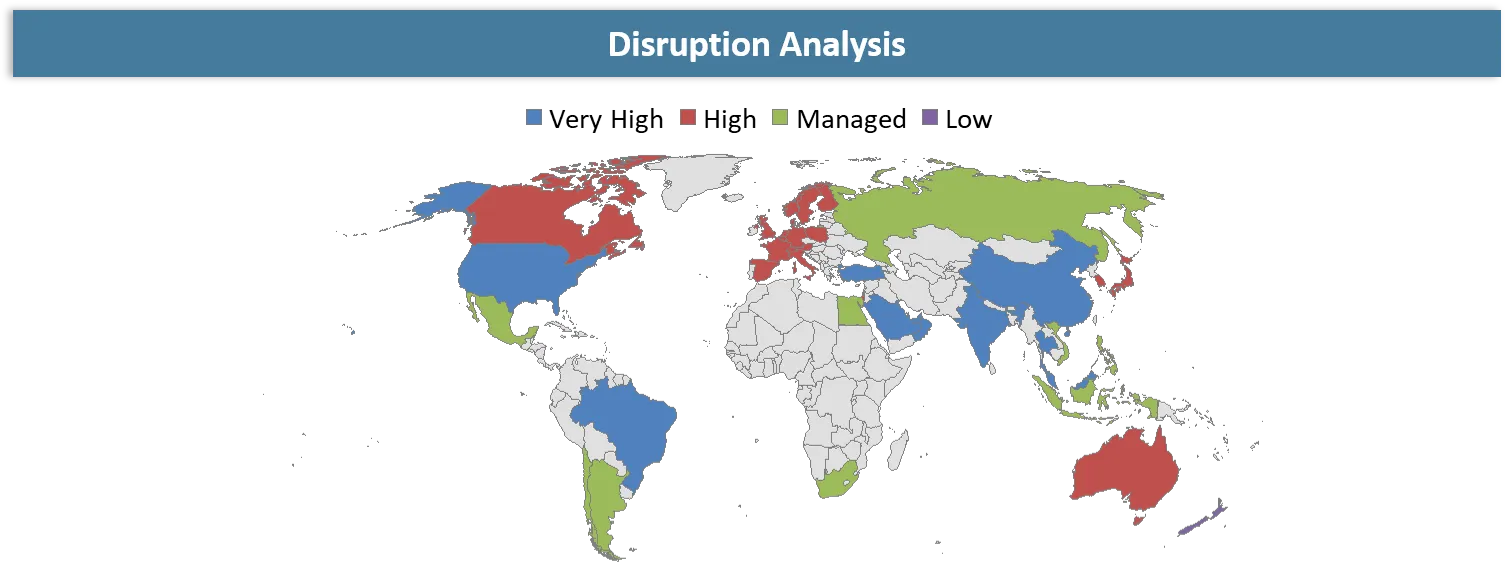

Battery Recycling Automation Market Disruption Analysis

Lack of Battery Design Standardization Disrupting Automation Scalability in Battery Recycling Operations

Battery Recycling Automation Market Disruption is caused mainly by the rise in diversification in Lithium-ion battery constructions and lack of standardization in EV manufacturers. Due to diverse designs from traditional recycling streams, modern EV batteries come with different designs in terms of cells, modules, packs, fasteners, thermal management, and electronic components. The differences present challenges to automation systems in dismantling and sorting operations. This makes it difficult for companies to design automated systems that will work universally for all types of batteries and increases the need for tailored solutions and artificial intelligence technology.

According to the International Energy Agency (IEA), the number of electric vehicles purchased is expected to keep increasing steadily, putting great pressure on the recycling industry to develop ways of processing a variety of battery formats. This is made difficult by the fact that there is no universal format for batteries, making the development of automated processes more challenging. Also, there have been changes in the techniques used by battery makers in terms of the methods of combining cells and packs to improve performance and energy density. These new technologies, which include structural battery packs and integrated batteries, limit access to modules and cells, posing further difficulties for the automation of the disassembly process.

As per the National Renewable Energy Laboratory (NREL), battery design variations and chemistries are key challenges that hinder automated recycling processes. Therefore, recycling automation firms are embracing adaptive robot technology, artificial intelligence battery recognition systems, and modular battery dismantling systems that will be able to accommodate several battery types without having to re-engineer their equipment. There is also the trend of battery recycling firms and automobile manufacturers collaborating to ensure designs of batteries have easy dismantling capabilities.

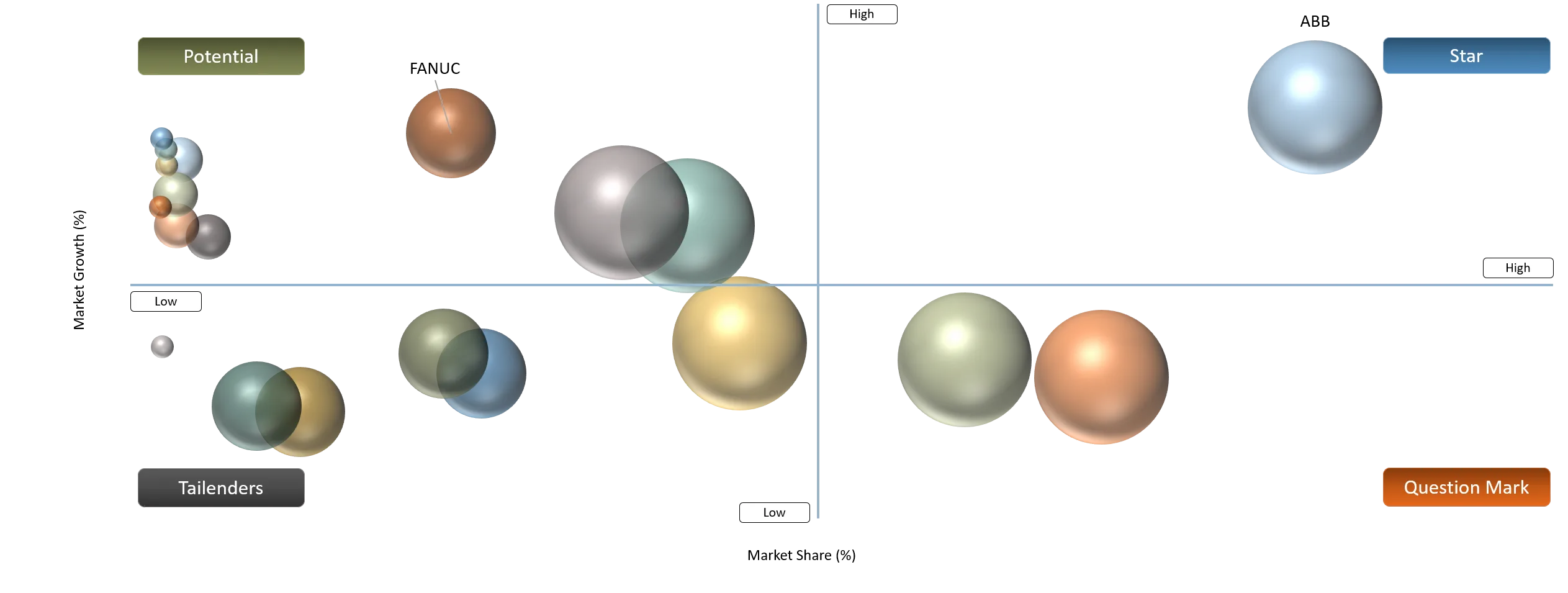

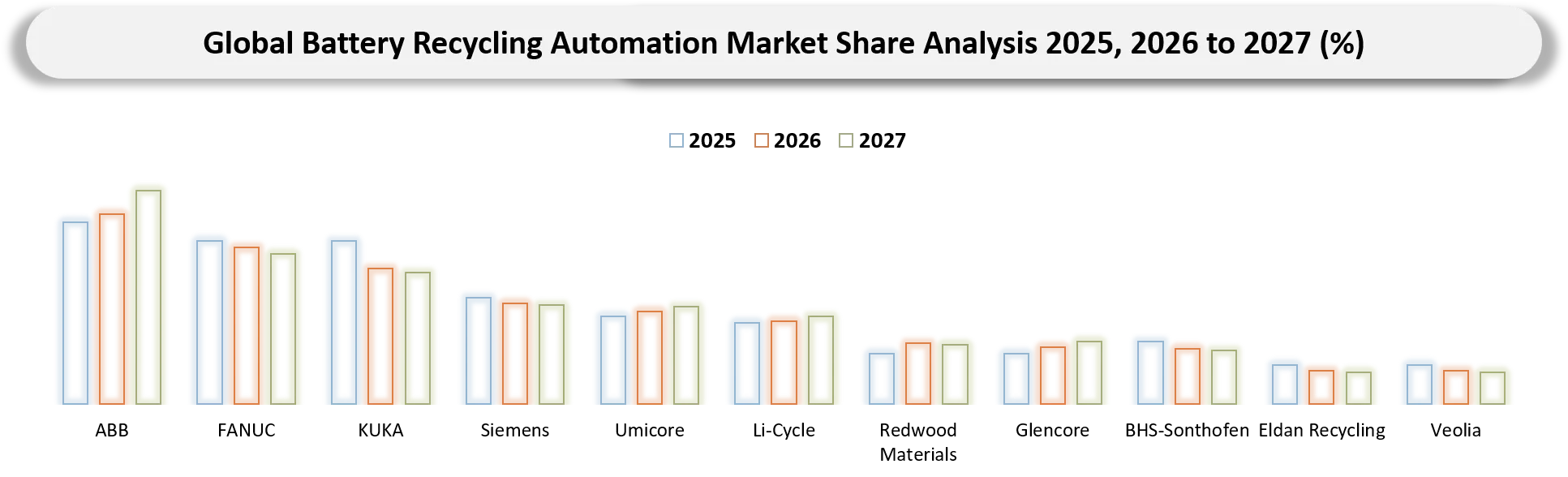

Battery Recycling Automation Market BCG Matrix: Company Evaluation

Stars in the battery recycling automation industry are ABB, Siemens, and Li-Cycle owing to their strengths in industrial automation, process digitization, and battery recycling plants for lithium-ion batteries. Such companies have capabilities in material handling, robotics, process optimization, and high-volume battery recycling operations. The advantages that ABB and Siemens enjoy are their industrial automation ecosystem. However, Li-Cycle has scalable battery recycling centers, which use automated processes of battery shredding and material separation for batteries from electric vehicles. Question Mark firms are Redwood Materials, Umicore, and Tomra since they are quickly developing their automation processes of battery recycling, although they are operating in a market that is still developing automation approaches. Redwood Materials and Umicore are enhancing their automation systems for closed-loop recycling and recovery of batteries, whereas Tomra is enhancing its approach through sensor sorting technology based on artificial intelligence.

Potential candidates for inclusion are FANUC, KUKA, Bosch Rexroth, and Glencore, who have superior technological capacities but are relatively weak in their direct control in the automated recycling of batteries. The companies FANUC and KUKA have the advantage of being experts in robotics, allowing them to automate battery disassembly and handling operations. Tailenders include BHS-Sonthofen, Eldan Recycling, and Veolia since their participation is mostly concentrated in recycling machinery, mechanical solutions, and environmental services rather than automated recycling systems for batteries.

Battery Recycling Automation Market Dynamics

Driver Impact Analysis

| Driver | Market Growth Impact (%) | Demand Concentration | Impacted Use Case | Strategic Impact |

Increased Deployment of Robotic Systems for Battery Disassembly Processes. | 30% | Automotive EV battery recycling facilities, large-scale recycling hubs, battery manufacturing ecosystems, and end-of-life battery processing centers | Automated battery pack dismantling, module separation, cell extraction, hazardous component handling, and high-volume recycling operations | Accelerates the transition from manual dismantling toward scalable automated recycling lines. Improves worker safety, processing accuracy, throughput capacity, and recovery efficiency of lithium-ion battery materials. |

Increasing regulation from the government about battery collection, recycled material content, and producer responsibility is fueling investment in recycling technology. | 25% | Europe, North America, China, and regions establishing battery circular economy frameworks | Battery collection systems, compliance-driven recycling facilities, closed-loop battery supply chains, and recycled material recovery operations | Strengthens investment in automated recycling infrastructure by creating mandatory recycling targets and encouraging battery manufacturers and automotive OEMs to adopt advanced recycling technologies. |

The identification and machine vision systems powered by artificial intelligence are playing a critical role in automation through battery classification, chemistry recognition, and defect identification. | 22% | Advanced recycling plants, AI-enabled sorting facilities, automated material recovery operations, and mixed battery processing centers | Battery identification, automated sorting, chemistry detection, quality inspection, and process optimization | Enables flexible recycling operations capable of handling diverse battery chemistries and designs. Improves material purity, reduces contamination, and enhances recovery rates of critical minerals. |

The growing number of lithium-ion battery chemistries, such as NMC, LFP, NCA, and other emerging technologies like solid-state, is contributing to an increased need for flexible automation solutions. | 25% | EV battery recycling, energy storage system recycling, consumer electronics battery recycling, and next-generation battery recovery facilities | Multi-chemistry battery processing, adaptive robotic dismantling, automated separation, and direct recycling applications | Drives development of modular and adaptable automation platforms capable of processing evolving battery architectures. Supports long-term scalability and reduces equipment replacement requirements as battery technologies advance. |

Increased Deployment of Robotic Systems for Battery Disassembly Processes

The increased deployment of robotic technologies in the process of battery dismantling has emerged as a major catalyst propelling the global Battery Recycling Automation Market, as recyclers and automotive companies are looking for more efficient and safer ways to dismantle and recycle used lithium-ion batteries. Manual techniques of battery dismantling are being outpaced by the intricacies of modern EV batteries, which include high-voltage systems, various cell assemblies, glues and other bonding materials, and dangerous substances. Consequently, robotic techniques of battery disassembly have become popular due to their ability to safely and accurately dismantle batteries. Moreover, innovations in AI, machine vision, and industrial robotics technology have improved the ability of automated disassembly systems to detect battery parts, fine-tune processing conditions, and handle different battery types. Businesses are now incorporating robotic arms, automated guided systems, and AI recognition systems into recycling plants to increase productivity and extract valuable metals such as lithium, nickel, cobalt, and graphite.

The movement toward intelligent robotic recycling systems has facilitated higher efficiency, lower reliance on human labor, and the creation of sustainable closed-loop battery value chains. For instance, in May 2026, the Springer Fachmedien Wiesbaden GmbH Company, a German-based science and specialist publishing company, published an article on the development of the battery disassembly system based on artificial intelligence technology, which included optical perception, adaptive robotics, and process knowledge.

Restraint Impact Analysis

| Restraint | Drag on Market Growth (%) | Primary Impact Area | Impacted Use Case | Strategic Impact |

The current shortage of batteries that have already been retired is still prevalent in many areas because electric vehicle fleets are still young. Insufficient use of automated recycling technology may pose challenges to the profitability of the operation. | 20% | Battery Feedstock Availability & Recycling Economics | End-of-life EV battery collection, automated sorting, and recycling plant utilization | Limited availability of retired batteries reduces automation ROI, delaying large-scale deployment of automated recycling facilities and affecting operational profitability. |

Automated process of battery disassembly still faces problems associated with hazards such as residual electricity, thermal runaway, and chemical exposure, among others. | 25% | Safety Management & Process Reliability | Robotic battery dismantling, module separation, cell extraction, and hazardous battery handling | Safety risks increase system complexity, requiring additional protective equipment, advanced sensors, and safety protocols, which slows commercialization of fully automated recycling systems. |

Maintenance and operational needs of automated systems such as robots, sensors, and processing machines are quite complex. | 20% | Equipment Reliability & Operational Cost | Robotic disassembly lines, AI-based inspection systems, automated sorting, and material recovery equipment | High maintenance requirements, frequent calibration, software updates, and skilled workforce needs increase operating expenses and reduce adoption among small and medium-sized recyclers. Advanced robotic battery disassembly systems require continuous optimization due to variations in battery designs and operating conditions. |

Development and commercialization process of automated systems for battery recycling is long because of the need for validation and safety considerations. | 25% | Technology Maturity & Commercialization Timeline | AI-enabled robotic recycling platforms, automated battery dismantling systems, and industrial-scale recycling facilities | Extended testing cycles, regulatory validation, and reliability requirements delay market penetration and increase R&D investment. Robotics-based battery disassembly remains an evolving field due to challenges related to battery design diversity and automation feasibility. |

Maintenance and operational needs of automated systems such as robots, sensors, and processing machines are quite complex

One of the critical limitations that limits the implementation of automatic technologies for battery recycling is the complexity of the maintenance and operational procedures of automated devices, including robots, sensors, AI-powered control modules, and special processing equipment. Automated plants for battery recycling should be continuously monitored, calibrated, software-updated, and maintained. Integration of robots into the battery disassembling process requires the use of complex elements like vision systems, robotic arms, adaptive instruments, and sensor-based control systems. Research conducted in 2025 and published by Springer Nature showed that the automation of the EV battery disassembly process still remains problematic due to the heterogeneity of batteries and the necessity of using advanced robot systems adapted to the industrial environment.

For instance, in December 2025, Schneider Electric, a French-based energy management and industrial automation technologies firm, pointed out that closed industrial automation systems are posing considerable operational issues to smaller manufacturers, causing loss of productivity, increased maintenance complexity, and low system flexibility.

Battery Recycling Automation Market Segmentation Analysis

The global battery recycling automation market is segmented based on component, automation level, automation solution, battery chemistry, recycling process, end user, and region.

Lithium-ion Batteries Dominating the Battery Recycling Automation Market by Battery Chemistry

The lithium-ion battery segment accounts for the major share of 85% in 2025 in the Battery Recycling Automation Market on account of the increasing use of electric vehicles (EVs), consumer electronics, and energy storage systems, leading to an increase in the amount of used lithium-ion batteries that need to be recycled using automated processes. Lithium-ion batteries account for the largest share in the global rechargeable battery market owing to their high energy density and longevity, coupled with extensive use in EVs, cell phones, laptops, and energy storage systems. The growing disposal of lithium-ion batteries from electric vehicles is boosting investments into automated recycling solutions. The rise in the use of EVs is anticipated to create a huge future demand for spent lithium-ion batteries, which is fueling the demand for automated recycling solutions such as robotic dismantling, automated battery diagnostics, AI sorting, and closed-loop material recycling.

The adoption of lithium-ion batteries across electric vehicles, portable electronics, and renewable energy storage application segments is keeping this category in the lead position as the most lucrative segment of the Battery Recycling Automation Market with a market share of around 85% in 2025.

Battery Recycling Automation Market Geographical Penetration

Rapid Expansion of Battery Recycling Infrastructure and Automation Adoption in Asia-Pacific Region

Asia Pacific region is dominating the Battery Recycling Automation Market with the market share of 45.6% in 2025, owing to the favorable environment created by the robust electric vehicle (EV) manufacturing industry in the region, increase in battery manufacturing capacity, increase in government support towards circular economy programs, and availability of leading battery manufacturing companies in regions such as China, Japan, South Korea, and India. The large-scale lithium-ion battery manufacturing infrastructure in the region is driving the demand for automated recycling processes such as robotic disassembly, automated sorting, AI-driven battery inspection, and material recovery.

For instance, in December 2025, ACE Green Recycling, a battery recycling technology firm based in the US, increased its battery recycling process automation in Asia through the use of advanced recycling machinery in Taiwan and Thailand. The implementation of GMPS and zero-emission recycling processes in the firm will increase efficiency in the processing of lead and lithium batteries and will aid in large-scale materials recovery.

China Battery Recycling Automation Market Trends

China holds the dominant position in the Asia-Pacific battery recycling automation market due to its huge electric vehicle (EV) ecosystem, high lithium-ion battery production, large amount of end-of-life batteries, and high acceptance of battery recycling automation technologies. The presence of battery makers, recyclers, and material processors helps China adopt automated solutions including robotic battery dismantling, artificial intelligence-powered sorting, automatic testing, and digital battery tracking systems. China has accounted for more than two-thirds of the global lithium-ion battery recycling capacity due to the use of sophisticated recycling technologies and efficient processing. Rapid growth in the NEV market in China is also increasing the need for recycling facilities that are highly automated. By 2025, the amount of power battery retired in China will amount to about 1.04 million tonnes and could surge to 3.5 million tonnes by 2030 according to The Climate Watch, thus generating high demands for automated facilities to handle the disassembling, recycling, and battery management.

There is an established recycling ecosystem in China that comprises over 150 qualified lithium-ion battery recyclers in China. For instance, in June 2025, Contemporary Amperex Technology Co. (CATL), a China-based company that manufactures batteries, is collaborated with TEDA Holdings and formed Tianjin Brunp TEDA Recycling Technology Co. Ltd in Tianjin, China, aimed at creating a NEV battery recycling ecosystem. This enterprise is involved in the creation of comprehensive recycling systems of batteries, integration of processes, carbon asset management, and green energy solutions.

India Battery Recycling Automation Market Outlook

India is emerging as a significant growth market within the Asia Pacific Battery Recycling Automation Market owing to factors such as the swift rise in the adoption of electric vehicles, the increase in demand for lithium-ion batteries, the establishment of battery recycling facilities in the nation, and governmental measures promoting circular economy principles. The nation's growing EV market and the need for extraction of critical minerals from the batteries have led organizations to use automation in the process of battery collection, sorting, dismantling, and material recovery. As per the Ministry of Heavy Industries (2025), the EV adoption in India continues to grow thanks to various governmental schemes. The growing amount of lithium-ion batteries that have been thrown away, recyclers are being driven towards automation through AI-based battery sorting, robotics for dismantling processes, and hydrometallurgical technology. According to the WRI India, by 2030, it is anticipated that there will be an accumulation of 128 GWh of lithium-ion battery waste in India with substantial growth happening between 2025 and 2026.

For instance, in February 2026, Epic Energy, a India-based energy solutions firm, partnered with REFNIC, a brand from Zetrance Technology, to build a lithium-ion battery recycling and second-life battery assembly plant in Maharashtra, India. The joint venture involves designing, engineering, integrating, installing, and commissioning a lithium-ion battery shredding plant with the ability to process 500 kg per hour to produce black mass and a second-life battery assembly plant with an installation processing capacity of around 10 MWh per month.

Battery Recycling Automation Market Competitive Landscape

- Participants in the Battery Recycling Automation Market are in three different types: industrial automation and robots suppliers; companies which deal with battery recycling and materials recovery, and automated sorting and processing technology suppliers. Companies like ABB, FANUC, KUKA, Siemens, and Bosch Rexroth, which are automation industry leaders, offer automated handling, robotization, artificial intelligence-powered automation, control systems, and digital manufacturing solutions to increase the efficiency of battery disassembling, enhance safety for workers, and improve the scalability of the process. Specialized battery recycling companies such as Umicore, Li-Cycle, Redwood Materials, and Glencore are engaged in large-scale lithium-ion batteries recycling, processing black mass, and recovery of valuable metals such as lithium, nickel, cobalt, and manganese. Companies like BHS-Sonthofen, Eldan Recycling, Tomra, and Veolia specialize in automated shredding, sorting, separating, and waste processing.

- Key players are ABB, FANUC, KUKA, Siemens, Umicore, Li-Cycle, Redwood Materials, Glencore, BHS-Sonthofen, Eldan Recycling, Veolia, Bosch Rexroth, and Tomra.

Key Developments

- February 2026: R3 Robotics, a Luxembourg-based robotics firm, secured a total funding of €20 million to develop automated disassembly services for decommissioned electric vehicles, such as lithium-ion batteries, electric drives, and power electronics.

- March 2026: PeakAmp, an India-based company that works with battery circularity and lifecycle management, partnered with Chargeup to design a lifecycle management framework for EV batteries by combining battery data platforms with EOL management capabilities.

- May 2026: Maxvolt Energy, an India-based lithium battery maker, has unveiled plans for a $73 million expansion project, with its main emphasis on battery energy storage systems (BESS), electric vehicle battery production, and lithium-ion battery recycling.

- June 2025: Welsbach Technology Metals Acquisition Corp. (WTMA), a U.S.-based special purpose acquisition company, and Evolution Metals LLC were approved by shareholders, resulting in an integration that will be concentrating on critical minerals, lithium-ion battery recycling, and advanced material processing technologies.

- June 2026: GreenMet, an India-based critical minerals and battery recycling company, and Silox, a Belgium-based chemical technology company, set up a joint venture to develop a state-of-the-art lithium-ion battery recycling facility in India.

- July 2025: VinFast, a Vietnam-based automobile company, collaborating with an Indian battery recycling technology firm, BatX Energies, set up a platform for the recycling and mining of critical metals from high-voltage EV batteries.

- September 2025: EVE Energy, a China-based lithium-ion battery maker, entered into collaboration with Miracle Automation Engineering Co., Ltd., another Chinese company offering intelligent equipment solutions, for the creation of a closed-loop battery recycling ecosystem from manufacturing, application, recycling to regeneration.

Key Procurement Priorities and Buyer Evaluation Criteria

- The purchasing decision-making process has been affected by the fast growth in the use of electric vehicles (EVs), growing waste from batteries, the need for critical minerals recovery, and circular economy regulations, leading to buyers preferring automation systems that are able to handle large battery recycling projects.

- When buyers are choosing technology providers for their battery recycling facilities, they take into account issues like the degree of automation, recycling capacity, efficiency of recovery, safety, capability to recycle different kinds of batteries, and ease of integration with other systems.

- In procurement evaluations, more consideration is being given to supplier capabilities that offer scalable and adaptive automation solutions in terms of meeting demands for batteries in the future, which could include not only lithium-ion or sodium-ion batteries but also advanced battery chemistries.

- The buyers are favoring those sellers who have the capability to show that they have increased efficiency in recycling, low cost of operation, enhanced safety for their employees, and sustainability in their recovery processes.

Why Choose DataM?

- Technological Innovations: This section examines the progress made in the development of recycling automation technologies for batteries such as AI-powered robot disassembly, machine vision systems, automated sorting, digital twins, process monitoring using IoT, material handling automation, and intelligent process control.

- Product Performance & Market Positioning: Considers the means by which the top automation companies distinguish themselves through their robotic accuracy, throughput capability, knowledge of battery chemistry, software intelligence, system integration, and scalability.

- Real-World Evidence: Focuses on the use of automated battery recycling technologies in commercial recycling plants, battery manufacturing plants, and critical minerals recovery plants, showing positive impacts like increased metal recoveries, decreased reliance on labor, increased safety levels, less contamination, and minimized process costs.

- Market Updates & Industry Changes: Highlights important milestones, such as the commercialization of AI-powered recycling systems, growth of automated recycling centers, collaborations between automation firms and battery recyclers, development of intelligent recycling facilities, and changes in battery recycling regulations in North America, Europe, and Asia-Pacific.

- Competitive Strategies: Examines how successful firms bolster their competitive edge by developing proprietary automation systems, artificial intelligence-based sorting systems, partnering with battery companies and car manufacturers, incorporating robotics, expanding production, and creating fully automated recycling processes.

- Pricing & Market Access: Elucidates pricing disparity considering the level of automation, processing capacity, intricacy of the robotic system, software, and integrations required, while evaluating the market penetration using industrial automation, recycling equipment, engineering services, and technology partnerships in the battery recycling business chain.

- Market Entry & Expansion: Highlights the growth opportunities resulting from the increase in the number of dead batteries in EVs, shortage of labor, regulatory requirement on recycling, need for critical minerals, and circular economy approach, as well as approaches like regional expansion of facilities, AI-powered process innovation, strategic partnerships, and adoption of automated solutions.

Target Audience

- Battery Recycling Companies

- Electric Vehicle (EV) Manufacturers and Automotive OEMs

- Lithium-ion Battery Manufacturers

- Battery Recycling Plant Operators

- Industrial Automation and Robotics Companies

- Automotive Tier-1 and Tier-2 Suppliers

- Metal Recovery and Mining Companies