Bank Kiosk Ecosystem Market Overview

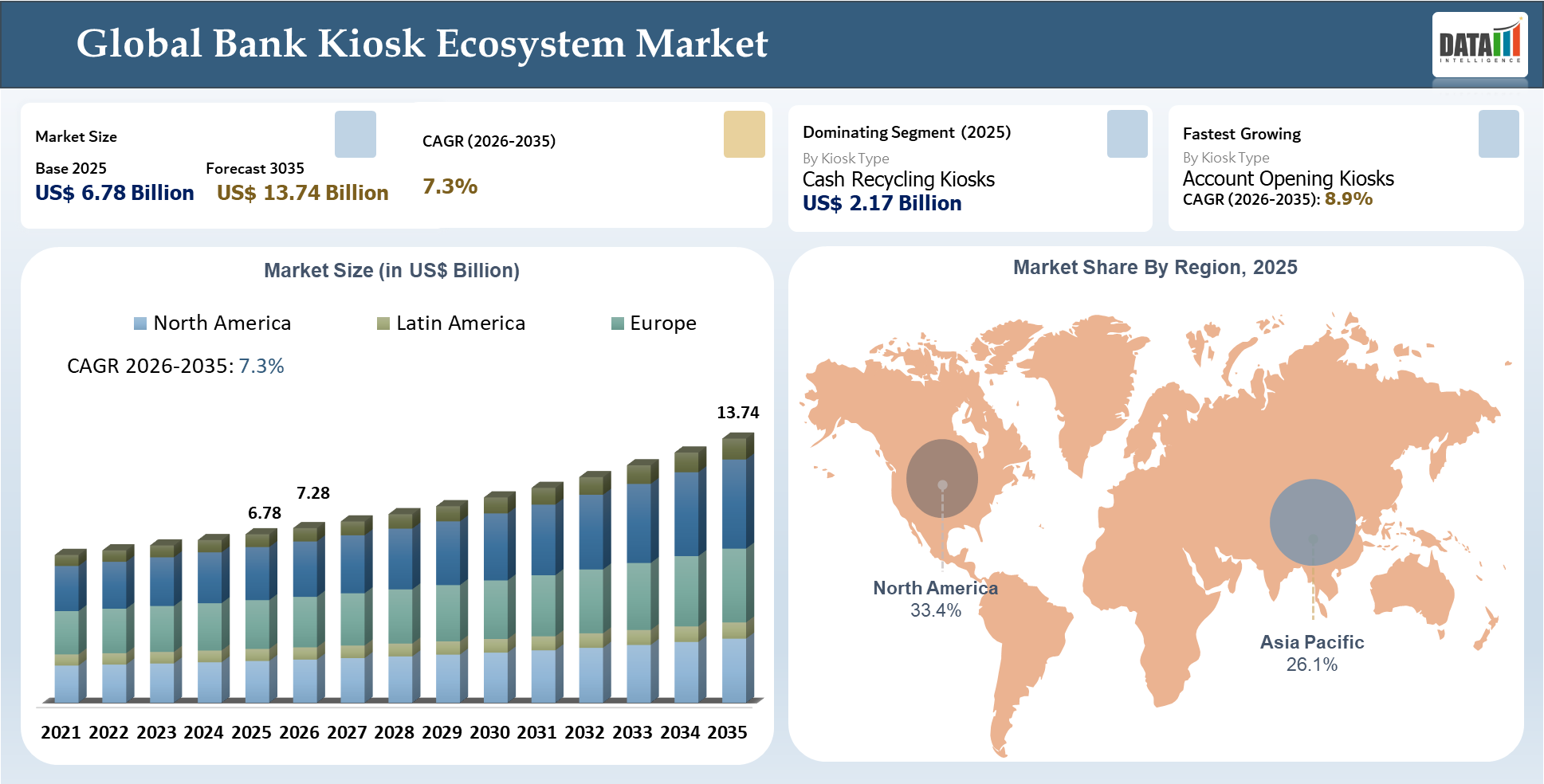

The global bank kiosk ecosystem market was valued at US$ 6.78 Billion in 2025 and is expected to grow into US$ 13.74 Billion by 2035, exhibiting a CAGR of 7.3% from 2026 to 2035. The major drivers behind this growth are kiosk usage for branch transformation, assistive self-service, cash automation, and digital onboarding purposes. As banks increasingly look to evolve their physical service offering model, there is a growing need for kiosks to be incorporated as part of the bank's banking infrastructure to help facilitate customer transactions, minimize reliance on tellers, and make services available in and out of the branch.

Several key dynamics are fueling market growth, namely the adoption of cash recycling kiosks, account opening kiosks, cheque deposit kiosks, card issuance kiosks, and video banking kiosks to name but a few. In addition, the need for branch efficiency, onboarding efficiency, financial inclusion, and hybrid service delivery are all helping boost market demand. Moreover, with the increasing evaluation of the operating value of kiosks compared to hardware alone, the ability to integrate systems, lifecycle support services, software compatibility, security features, and reliability are all set to be key differentiators going forward.

AI Impact Analysis

AI is now influencing the bank kiosk ecosystem market not through developing a new market segment but rather through enhancing the design, deployment, operations, and monetization of kiosks throughout their life cycles. Value chains are incorporating AI in various stages, including design optimization, software orchestration, predictive maintenance, remote diagnostics, fraud monitoring, transaction analytics, and demand forecasting. These improvements positively impact performance in branches and non-branch banking.

In terms of benefits for banks, the value proposition lies in the potential to cut down kiosk downtime, optimize cash and consumables management, identify potential system failures prior to service disruptions, ensure precise diagnoses, and help employees handle complicated self-service networks with lower error rates. From a customer perspective, transactions can be made easier, uptime can be optimized, and service interventions can be carried out more efficiently. Thus, suppliers offering a combination of intelligent software, device-level data, and services have an edge over those emphasizing only hardware requirements.

Commercialization processes are also affected. Pre-sales teams can assist customers in simulating deployments, providing analytics on usage, and optimizing network configuration. Post-sales teams can leverage the data gathered from the installed base in managing renewals, upgrading strategies, spare parts management, and expanding service revenue.

Bank Kiosk Ecosystem Market Key Takeaways

- The kiosk type continues to be the key decision variable since it captures the bank’s approach to capital investment, functional compatibility, and vendor selection criteria based on transaction capabilities, environment, and life cycle economics within the overall bank kiosk system.

- The demand is shifting towards high utility self-service solutions like cash recycling kiosks, account opening kiosks, and multi-function services kiosks which can offer demonstrable efficiency improvements, branch operations savings, and better customer throughput without resorting to a digital transformation strategy.

- The Asia Pacific region has taken the lead in setting the pace of competition with countries like India, Japan, and China dictating the product design, cost/performance parameters, deployment approaches, and market strategies for vendors rolling out their self-service solutions across urban and rural areas.

- Successful vendors will continue to differentiate themselves through ecosystem strength, which encompasses hardware, software, service support, cash handling prowess, and banking relationships.

Market Scope

| Metrics | Details | |

| 2025 Market Size | US$ 6.78 Billion | |

| 2035 Projected Market Size | US$ 13.74 Billion | |

| CAGR (2026-2035) | 7.3% | |

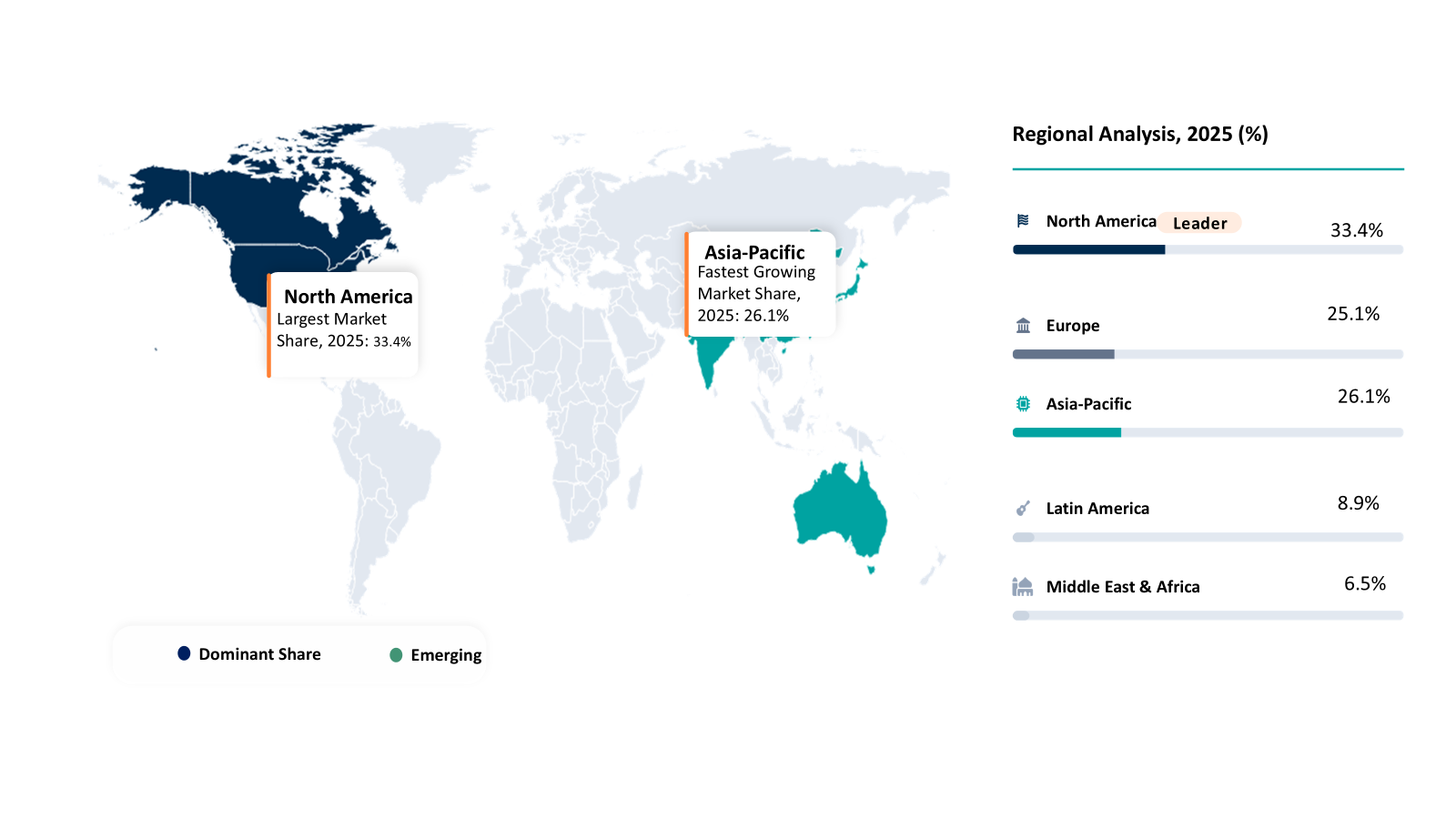

| Largest Market | North America | |

| Fastest Growing Market | Asia-Pacific | |

| By Kiosk Type | Cash Recycling Kiosks, Account Opening Kiosks, Cheque Deposit Kiosks, Card Issuance Kiosks, and Video Banking Kiosks | |

| By Function | Cash Handling, Customer Onboarding, Bill Payment, and Identity Verification | |

| By Deployment Site | Branches, Retail Locations, Transport Hubs, and Corporate Campuses | |

| By Technology | Biometric Authentication, Remote Assistance, Document Scanning, and NFC and QR Payment | |

| By End-User | Banks, Credit Unions, Fintech and Neobanks, and Government Banking Services | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

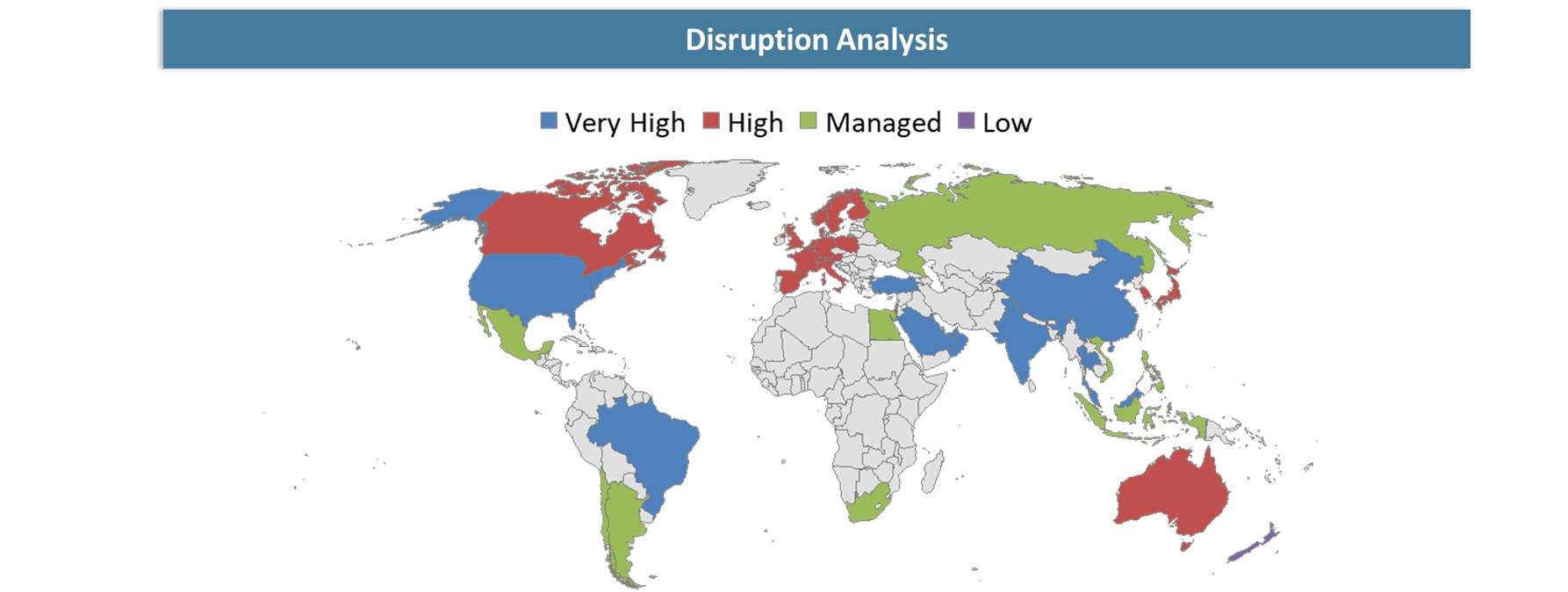

Disruption Analysis

Shift from Technical Differentiation to Outcome-Led Channel Execution, Integration Readiness, and Lifecycle Accountability

The real disruption in the ecosystem of the global bank kiosk market is the change from equipment purchasing to outcome-oriented channel economics. Purchasers are no longer paying vendors just because they provide additional features in their installed ATMs, recyclers, or onboarding kiosks. Instead, they want to know whether these devices can help them cut the costs of branch servicing, maintain high uptime rates, facilitate digital onboarding, and achieve continuous efficiency gains through service delivery.

The second disruption comes through services gaining control of the banking self-service channel. The value proposition is no longer confined to hardware solutions but has expanded into software solutions, outsourcing, monitoring, and lifecycle management. According to KAL’s report in 2025/26, 19% of all banks already outsource their whole ATM networks, while another 24% are planning to do the same. At the same time, NCR Atleos' report states 14% growth of ATM hardware revenues in 2025 associated with the greater services opportunity at hand.

Thirdly, there is disruption caused by the redeployment of networks amid unequal cash and branch realities. Banks are becoming digital, but access matters just the same. In the UK, for example, the number of bank branches dropped from 10,410 in 2019 to 6,870 in 2024, a drop of 34%, but regulators and banks keep investing in the access ecosystem, including banking hubs and enhanced self-service facilities. Simultaneously, physical self-service presence continues to matter: as recently as 2024, Japan still has 117,526 ATMs, and according to the World Bank, ATM penetration rates were material both in Japan and India in 2023. This means the winning model is not “digital replaces kiosk,” but “digital and kiosk channels get rebalanced around cost, access, and resilience.”

The final disruption is the emergence of convergence in regulations and models of operation. RBI guidelines for digital banking units up to 2025 refer to cash recycler, service terminal, card issuance via self-service kiosks, documents uploading, and KYC system through videos in defining a next generation branch. This shows a shift in the market, in that kiosks are now seen not as standalone systems but as banking infrastructures that are connected within the processes of onboarding, servicing, and assisted digitalization.

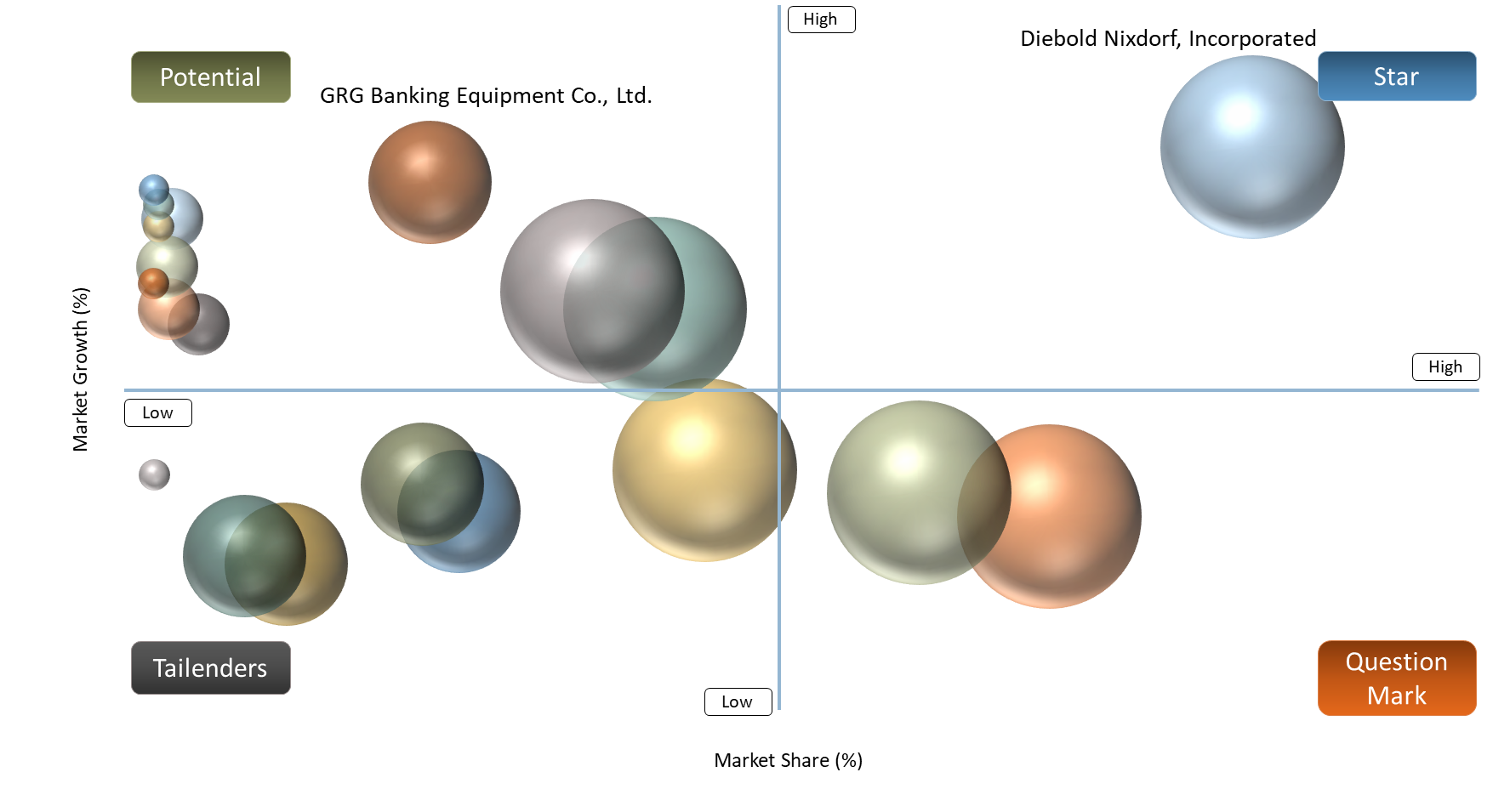

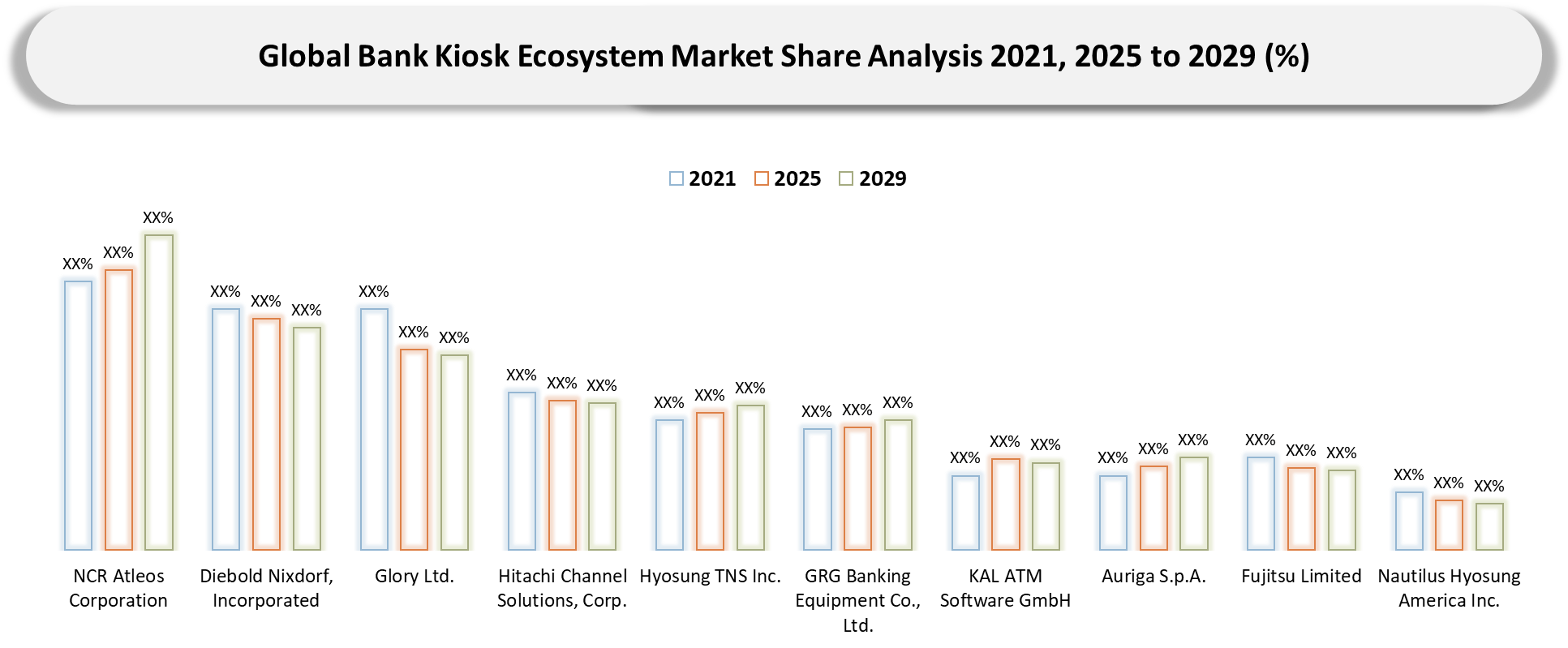

BCG Matrix: Company Evaluation

From a BCG perspective, Stars in the bank kiosk ecosystem market refer to the providers that are able to create synergies between growth and control within the surrounding banking self-service ecosystem. Such businesses do not necessarily rely on the hardware alone; rather, their success depends on a combination of product breadth, software solutions, speed of service, system integration, and channels. Companies such as NCR Atleos Corporation, Diebold Nixdorf, Incorporated, and Glory Ltd. may be seen as Stars provided that they can use installed base advantages to increase their wallet share via upgrades, managed services, cash automation, and branch transformation. What is important about these businesses is that they define what banks require from a comprehensive self-service partner.

Cash Cows are incumbent players with an established installed base and good replacement cycles and service revenues that tend to span across several regions. It is quite possible that these businesses will not be leaders in the most promising market segments; however, they still remain commercially sound owing to maintenance agreements and software support services, among others.

Question Marks consist of niche players or adjacents that focus on certain spaces within white spaces, like account opening terminals, cash recyclers, or service-assisted systems. They offer a lot of potential, but their ability to scale up will depend on whether they fit the regulatory environment, ecosystems, and implementation.

Dogs are usually vendors who operate mainly in undifferentiated hardware volumes, limited-service systems, or poorly integrated ecosystems.

Market Dynamics

Banks Are Using Kiosks to Redesign Service Footprints Around Smaller Branches, Assisted Self-Service, and Remote Expert Access

Kiosks represent one such tool that banks have begun to introduce as part of their structural adaptation, as opposed to a channel improvement, to evolving branch economics. In Australia, less than 1% of interactions between consumers and their banks take place at physical branches, while almost 17 billion digital log-ins occur annually. These figures clearly indicate why banks are rethinking their approaches based on smaller, less costly physical facilities that incorporate aspects of self-service and digital support. The response in the UK is not the elimination of physical access to banking facilities but the redesign of such access. As a result, there will be a total of 350 banking hubs by 2029 in the UK, with 179 already up and running. This demonstrates a definite trend towards redesigning banking based on smaller and more efficient service formats. In this context, kiosks play a critical role in designing such services, as in the case of Bank of Baroda.

That explains why the banks have started considering the kiosks as part of the basic service structure of their hybrid banking concept where ordinary services can be handled through self-service, while the specialized services can be handled by the employees and the remote professionals. The need for multifeatured kiosks, assisted self-service devices, and remote banking solutions is growing.

Long Procurement Cycles, Integration Complexity, and Reliability Validation Continue to Slow Adoption

However, adoption in the bank kiosk ecosystem market is hindered less by supply and more by the complexity and risk of bank decision making. Investment decisions in kiosks tend to go through various levels of approval within the institution, including IT security and compliance departments, as well as channel management. Further, legacy core infrastructure presents a major problem. According to a recent survey, 55% of all banks cited restrictions in their core as the most significant barrier to meeting business objectives. As a result, the introduction of new solutions in form of connected self-service kiosks poses extra risk, since the solutions need to integrate well with the existing payment, authentication, and monitoring systems. In addition, reliability challenges are bound to occur. For instance, UK banking statistics indicate that Barclays had 33 disruptions in 2023-2025, followed by HSBC and Santander with 32 incidents each, illustrating the difficulties of working with complicated and obsolete technologies.

Segmentation Analysis

The global bank kiosk ecosystem market is segmented based kiosk type, function, deployment site, technology, end-user, and region.

Kiosk Type Is the Most Commercially Meaningful Lens in the Bank Kiosk Ecosystem Market

The Kiosk Type dimension is the one that is most relevant for decision-making within the market of bank kiosk ecosystems due to its connection to budgeting, risk assessment, and investment returns by banks. Decisions about procurement can be better clarified based on use-case-related formats as compared to those associated with broad portfolio approaches. In this respect, Cash Recycling Kiosks and Account Opening Kiosks stand out as separate sources of value. First, Cash Recycling Kiosks are still gaining momentum due to their ease and speed of deployment. Their importance stems from the existing base of ATM systems that number well above 3 million globally, making them an upgradeable option that allows for reducing the costs related to money management.

Account Opening Kiosks, on the other hand, emerge in a digitally transformed environment that emphasizes speed of deployment, regulation, and customer experience. This choice is underpinned by the forecast of digital onboarding accounting for over 70% of new accounts in advanced banking sectors, thus boosting the need for assisted self-service solutions. In terms of commercial success, while less easy to deploy, Account Opening Kiosks are more strategically valuable for suppliers since they boost efficiency and improve regulatory compliance.

Geographical Penetration

Asia-Pacific Leading Bank Kiosk Ecosystem Advancement Through Operating Model Transformation and Deployment-Driven Execution Leadership

The Asia-Pacific region is shaping the competitive dynamics of the bank kiosk ecosystem market since it represents the true shift in banks' approach towards services delivery compared to simple expansion of demand. Many banks in the region are undergoing reconfiguration of their branches network with consideration of both cost optimization and client accessibility, driving the use of multifunctional kiosks, assisted self-service technology, and banking node enabled by remote technologies. This trend is directly correlated with the persistence of cash payment culture along with widespread use of digital technology, resulting in a hybrid ecosystem where the role of the kiosk becomes especially important. It is worth noting that the size of the current installed base is quite impressive; for example, India already has more than 222,000 ATM units as of 2023 according to the World Bank data. Thus, the Asia-Pacific region is a promising location for testing business models with an ability for fast scaling up the business. In this sense, buyers' priorities include speedy implementation, integration capability, and provision of localized support services.

India Bank Kiosk Ecosystem Market Trends

India represents a key market for the bank kiosk industry due to the importance of factors such as financial inclusion, digitization, and cost-efficient rollout. Kiosks operate as a means of carrying out cash transactions and digital banking services for bank customers in semi-urban and rural settings, through what banks call "branch-lite" models. It is also backed by favorable policy; the Reserve Bank of India requires the rollout of Digital Banking Units, which will be composed of devices such as cash recyclers, kiosks, and video KYC machines. On the other hand, transaction dynamics are continuously changing in India with the number of digital payments made standing at 130 billion transactions in the year ending March 2024, representing the fast-paced adoption of digital services even as users seek physical locations for their transactions and digital banking processes. The two dynamics require banks to procure kiosks that are both affordable and integrated with digital transaction and compliance operations.

Japan Bank Kiosk Ecosystem Market Outlook

Japan is an example of a mature and technologically advanced sector of the bank kiosk ecosystem market, in which the focus shifts from growth to efficiency, dependability, and automation. The Japanese banking market features such characteristics as high service standards, an aging population, and staffing difficulties. All these factors drive the implementation of modern technologies in order to preserve service levels while becoming less dependent on human capital. This assumption can be proved by analyzing the number of self-service terminals installed in Japan: according to expert estimates, the number reached 117,526 in 2024, which proves a well-established self-service network, which has been evolving towards multifunctional terminals and those able to recycle cash. Under such conditions, the role of kiosks changes to become an element designed to increase productivity rather than a means of completing a certain transaction. In addition, Japan can be called an ideal market for premiumization initiatives because buyers are more concerned about reliability, precise workflows, and flawless integration into the banking infrastructure.

Competitive Landscape

- The competition in the market for bank kiosk ecosystems has been characterized by a clear structural demarcation between those who have been able to exploit economies of scale in their operations and those who have chosen to focus more on their core competencies. The competitive edge, however, seems to be shifting from supplying the devices themselves towards taking control of the entire ecosystem where the solutions can thrive. In this regard, large organizations like NCR Atleos Corporation, Diebold Nixdorf, Incorporated, and Glory Ltd. have relied on the strength of their portfolios, strong installed base, wide distribution networks, and customer base to influence buying behavior in the industry. On the other hand, specialized organizations compete based on their closer alignment with use cases, fast deployment, and high responsiveness within specific types of bank kiosks or operational environments.

- Also, market positioning is being driven by the ability of the suppliers to deliver an end-to-end customer experience. While product quality still matters, banks are looking at suppliers who can offer smooth onboarding, integration into the bank’s infrastructure, workflow management, responsiveness, and lifecycle management. Suppliers who have been able to position themselves well in lucrative markets like Cash Recycling Kiosks and Account Opening Kiosks will usually be more able to negotiate prices, increase account relevance, and grow their market share.

Key Developments

- April 2026: NCR Atleos Corporation was selected by Founders Federal Credit Union for its ATM as a Service (ATMaaS) model to modernize member self-service, signaling continued momentum in managed self-service banking infrastructure.

- February 2026: NCR Atleos Corporation became the target of a US$6.6 billion acquisition by The Brink’s Company, a deal that underscores the strategic value of ATM, cash access, and self-service banking infrastructure within broader cash-management networks.

- February 2026: Diebold Nixdorf, Incorporated reported a new ~US$12 million managed services contract for a U.S. financial institution and a ~US$15 million two-year services contract in France, showing stronger monetization of lifecycle banking services beyond equipment sales.

- December 2025: Diebold Nixdorf, Incorporated launched the DN Series 300 and 350, positioning the new self-service banking terminals around higher cash capacity, smaller footprint, and lower operating cost.

- December 2025: Diebold Nixdorf, Incorporated announced that Capital Bank deployed its VCP-Pro 7 multivendor self-service software, highlighting rising bank demand for software-led operational efficiency and deployment flexibility.

- December 2025: KAL ATM Software GmbH released its 2025/26 ATM Software Trends Report, which found that 51% of banks reported increased ATM reliance, reinforcing the continued strategic role of self-service banking channels.

- October 2025: Diebold Nixdorf, Incorporated announced that Bank AlJazira became the first bank in the Middle East to implement its latest-generation self-service software on Windows 11, highlighting the push toward software modernization and security readiness in bank self-service fleets.

- August 2025: Diebold Nixdorf, Incorporated unveiled its Branch Automation Solutions portfolio, expanding from device supply into a broader services suite aimed at improving physical-channel efficiency and omnichannel banking delivery.

- July 2025: NCR Atleos Corporation and Lloyds Banking Group advanced a branch modernization program using note and coin technology and end-to-end service support to reduce counter traffic and improve branch efficiency.

- July 2025: Diebold Nixdorf, Incorporated completed an Interactive Teller Machine (ITM) deployment with Kuwait International Bank, showing continued momentum for assisted self-service formats in branch transformation.

- January 2025: Glory Ltd. was confirmed by RBR Data Services as the global leader in retail cash recycling solutions excluding Japan with 44% market share, rising to 68% including Japan, reinforcing its scale and strength in cash automation.

- July 2024: Glory Ltd. partnered with OXXO to deploy CASHINFINITY cash recyclers supporting “virtual ATM” banking services in stores, illustrating how kiosk and cash-automation capabilities are extending beyond conventional branch formats.

White Space Opportunities

Based on DataM analysis, one of the white space markets within the bank kiosk ecosystem market could be considered as a space where large and visible deployments are not feasible or profitable. Although there is much focus among the existing players on tier-1 banks, under penetration of demand in the form of high friction use cases, such as branch-lite scenarios, assisted self-service in semi-urban locations, and intensive onboarding scenarios, exists, and here the buyers' needs lie in ensuring reliable and easily implemented services.

Another white space market would be deployment enablement and commercial packaging. Increasingly, banks prefer vendors who facilitate easy adoption through such factors as onboarding, compliance, workflow setup, and post-deployment services. It is even more relevant in terms of account opening kiosks.

Finally, mid-tier banks still remain an area with under penetration, and, hence, vendors should consider partnerships in order to reach out to the customers. Moreover, differentiation is slowly moving from hardware to data and services, specifically around monitoring and analytics.

DMI Opinion

However, according to DataM, the key question of the bank kiosk ecosystem market is not related to the existence of market interest but rather concerns the ability of the suppliers in translating market interest into sustainable revenue without increasing delivery complexity faster than customer benefits. It seems that the market currently favors those vendors who have demonstrated their commitment to making the adoption of their products operationally viable through integrability, lifecycle, and demonstrable results for banking businesses.

Based on DataM observations, too often, the participants of the bank kiosk ecosystem market overvalue broad product positioning stories and undervalue the deployment mechanics. In reality, bank kiosk ecosystems are emerging as connected banking infrastructure, which is essential for compliance, service continuity, and process management. This is why vendors that invest in delivery capabilities, customer service, and delivery transparency are likely to secure higher shares than vendors who base their strategy solely on hardware scale.

According to DataM analysis, the bank kiosk ecosystem market is essentially an execution-focused infrastructure play, where sustainable outperformance can be achieved by mitigating adoption barriers.

Why Choose DataM?

- Innovation and Technology in Banking Kiosks: Explores innovations in self-service banking technology, ranging from cash recycling kiosks, account opening kiosks, interactive tellers, multifunction kiosks, remote service integration, authentication solutions, and workflow intelligence.

- Performance of Competitors in Real-World Banking Environments: Reviews the performance of competing companies in actual banking settings in branch automation, assisted self-service, onboarding, and cash management. This research highlights the capabilities of leading suppliers in terms of integration maturity, uptime performance, workflow compatibility, service delivery, regulatory compliance, and scalability.

- Real-World Adoption of Banking Kiosks: Finds real-world examples of bank kiosks being deployed in branch lite branches, digital banking facilities, assisted services, financial inclusion initiatives, and alternative banking channels.

- Key Industry Developments & Market News: Highlights key industry developments, including those around new kiosks, branch transformation projects, deployment of self-service options, software improvements, service alliances, and regulations affecting each of the major regions including North America, Asia Pacific, Europe, India, and Japan.

- Business Growth Strategy: Covers the growth strategy of key companies through increased product depth, software functionality, service capability, partner channels, and ecosystem positioning.

- Value Creation Strategy: Hardware, Software, Service and Outsourcing: Covers the value creation strategies in areas of hardware, software, service, outsourcing, lifecycle support services.

- Market Penetration & Growth Strategy: Details white space opportunities from under-penetrated banks, branch transformation programs, assisted digital services, and regional growth approaches, together with a discussion of scaling strategies to support integration, reach and execution credibility.

Target Audience

- Product strategy teams

- Corporate strategy and market intelligence teams

- Business development leaders

- Sales and channel leaders

- Investors and private equity firms

- Procurement and sourcing teams

- Technology and operations leaders

- Consulting and advisory teams.