Overview of the Global Baking Oven Industry

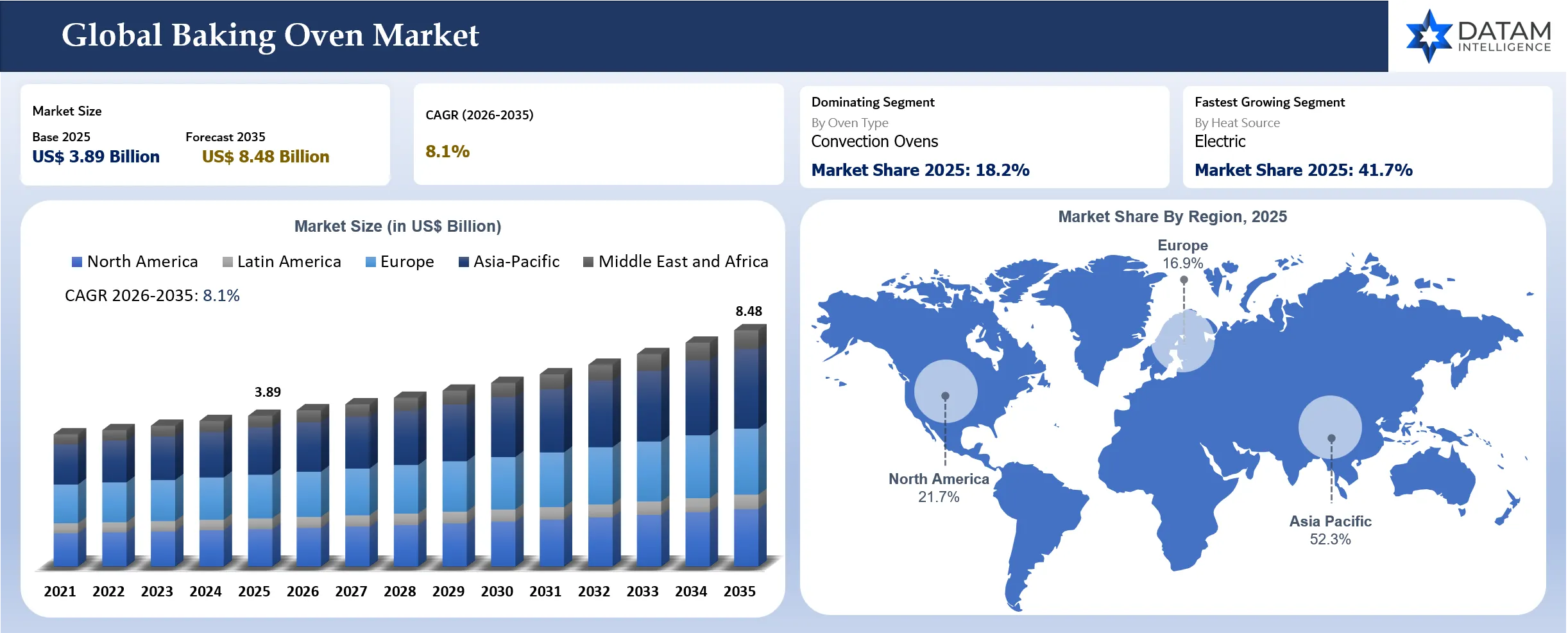

The global baking oven industry reached US$ 3.89 billion in 2025 and is projected to reach US$ 8.48 billion by 2035 at a CAGR of 8.1% during 2026 to 2035. From simple capacity additions, demand now is shaped by operating economics of heat. Larger bakeries are checking every zone of their ovens for fuel consumption, loss of product, line stops and sanitation stops. Energy recovery is no longer just a concept but has become an economic decision due to the fact that baking is one of the energy-intensive processes in producing breads, biscuits, and snacks. Operators are therefore asking suppliers for proof of heat transfer efficiency, airflow control, exhaust recovery, insulation performance and service response before approving a new line.

Technology buying has also become more practical. Bakery plants are not adopting digital systems because they want dashboards. They are adopting connected controls because a weak burner, uneven airflow, poor steam injection or a drifting temperature sensor can waste hours of production. Labor pressure has made the case stronger. Baking Business reported that automation investment helped ease some labor challenges in the 2025 State of the Industrial Baking Industry study. Smart controls, recipe locking, automated loading and remote diagnostics are therefore becoming a way to protect repeatability when experienced line operators are hard to replace. Smaller retail bakeries are moving in the same direction through compact ovens with programmable profiles and simpler maintenance interfaces.

Key Takeaways

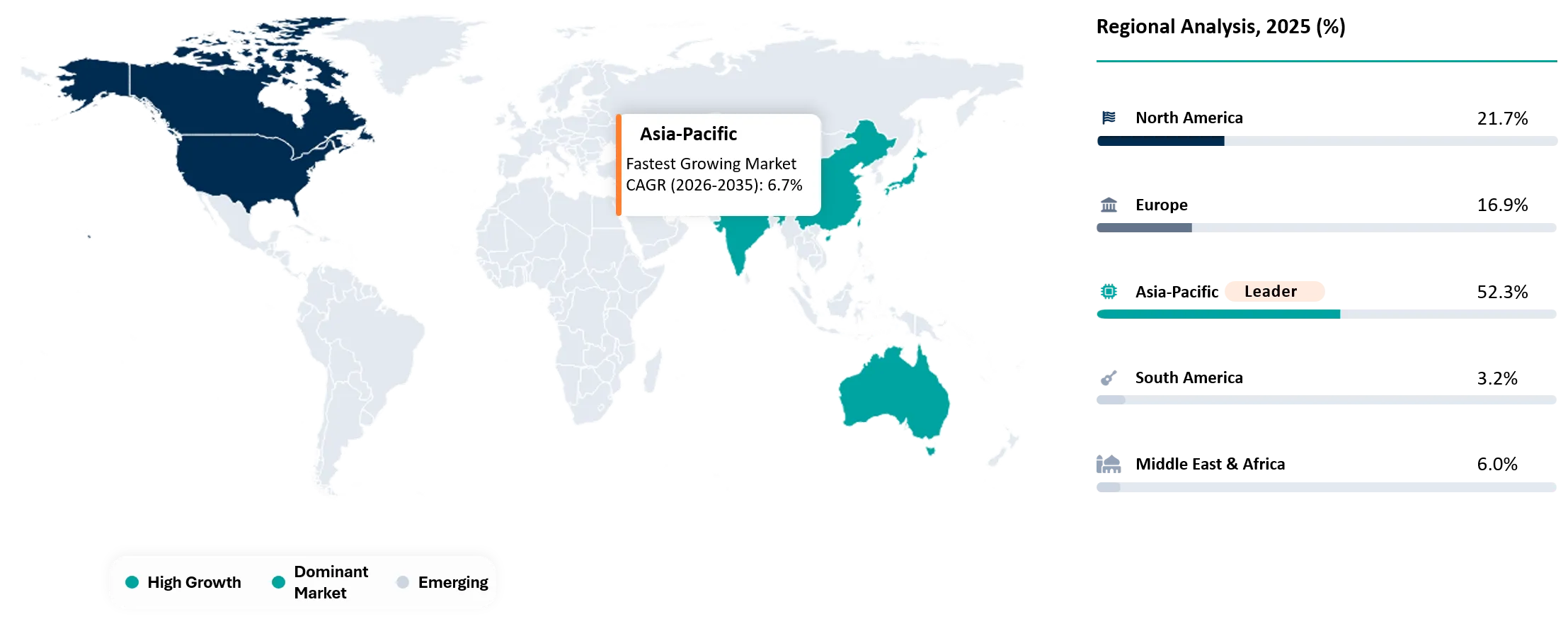

- Asia-Pacific is largest region in the global baking oven market with a market share of 52.3% in 2025.

- Convection baking ovens have been leading in the market with a market share of around 18.2% in 2025.

- The increasing trend of utilizing energy-efficient, automated, and smart baking technology has been identified as one of the key factors driving innovations and productivity in the global baking oven market.

- Some of the key vendors operating in the market include Middleby Corporation, Welbilt Inc., and Ali Group, which are making themselves dominant in the market through constant development in large-scale commercial baking equipment and energy-efficient products.

- Many commercial bakeries are progressively shifting from traditional gas-operated ovens to energy-efficient electric and hybrid models due to the need to lower energy usage and adhere to the increasingly stringent carbon emission regulations. The use of improved heat recovery systems and insulated oven chambers has enabled industrial bakers to save 15% to 25% of the energy costs incurred in the process of baking.

- Suppliers are designing baking ovens that come with IoT sensors and artificial intelligence-based temperature controls. Smart ovens with built-in remote monitoring features are now allowing many bakeries to boost productivity and decrease wastage.

Market Scope

| Metrics | Details | |

| 2025 Market Size | US$ 3.89 Billion | |

| 2035 Projected Market Size | US$ 8.48 Billion | |

| CAGR (2026-2035) | 8.1% | |

| Largest Market | Asia-Pacific | |

| Fastest Growing Market | North America | |

| By Oven Type | Rack Ovens, Reel Ovens, Deck Ovens, Tunnel Ovens, Rotary Ovens, Convection Ovens, Hybrid Ovens, Combi Ovens, Others | |

| By Heat Source | Gas Fired, Electric, Dual Energy, Indirect Fired Thermal Oil, Steam Assisted | |

| By Automation Level | Manual, Semi-Automatic, Fully Automatic | |

| By Capacity | Small Batch, Medium Throughput, High Throughput Industrial | |

| By Baking Format | Bread and Rolls, Cookies and Biscuits, Crackers, Cakes and Pastries, Pizza Bases and Flatbreads, Wafers and Cones, Pet Food and Specialty Snacks, Others | |

| By Purchase Type | New Installation, Retrofit and Line Expansion, Oven Zone Upgrade and Electrification | |

| By End-User | Commercial Food Service, Hospitality and Institutional, Corporate Offices, Residential, Industries, Supermarket and Hypermarket, Others | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

Why Bakery Equipment Decisions Matter More in 2026

The rising need for baked products, bakery products, frozen foods, and convenience foods around the globe is raising the demand for modern baking equipment that can provide consistent product quality, high production rate, and cost-effective process. On the other hand, the energy efficiency regulations, CO2 emission reduction policies, and food safety regulations in North America, Europe, and Asia-Pacific region have compelled the firms to adopt new-age electric, hybrid, and intelligent baking ovens. Its a fast transforming the market from traditional thermal treatment systems to digitally enabled, environmentally friendly and production-efficient baking solutions that have higher commercial value.

On another front, baking oven makers are under tremendous pressure to develop scalable and technologically distinctive systems that meet the changing production needs of industrial bakeries, foodservice companies and specialty food processors. Major developments in IoT-based monitoring systems, AI-driven temperature management, modular baking system using conveyors, impingement heating systems, and energy recovery systems are fast changing the dynamics of competition in the market. Buyers, investors and food processing stakeholders now require deeper visibility into energy consumption optimization, baking consistency performance, automation integration capabilities, predictive maintenance systems, hygienic equipment design, production flexibility, aftermarket service networks and compliance with global food processing standards to evaluate long-term operational efficiency, minimize production downtime and identify commercially competitive baking oven technology providers.

Strategic Indicators For Baking Oven Market

White Space and Investment Opportunities

Retrofit electrification kits remain underdeveloped for mid-sized bakeries that need lower emissions but cannot replace full tunnel lines at once. Many plants still operate older gas zones with acceptable mechanical life but weak controls and poor exhaust recovery. Supplier opportunities sit in staged upgrades that add electric zones, heat recovery modules, burner tuning, insulation packages and digital monitoring without forcing a full line shutdown. Regional service networks are a white space in India, Southeast Asia, Mexico and the Gulf. As bakery chains grow into these regions, they often bring in their high-end equipment but fail to manage local airflow tuning, burner servicing, sensors and training of operators. A service network provider that offers mobile teams, spares and remote diagnostics can help them minimize downtime and be integrated into the customer relationship.

A second white space relates to recipe optimization software. Industrial bakers are looking for repeatable recipes for breads, cookies, pizza bases, frozen snacking goods and gluten free products. AI-driven bake libraries, recipe transfer validation and performance subscription can enable suppliers to move away from sales to performance-based revenues. Efficient compact systems for cloud kitchens, convenience stores and retailers will continue to appeal because fresh baking moves ever closer to the consumer. These potential buyers need small footprint, quick recovery, safe ventilation, ease of cleaning and consistency of results with a minimum number of staff. Such equipment addresses a different set of customers than large tunnel systems.

Future Transformation of Baking Oven by 2035

By 2035, baking oven will operate as connected production assets rather than standalone chambers. Suppliers will sell ovens with recipe control, energy dashboards, quality records, predictive maintenance support and service agreements built into the offer. Industrial buyers will expect ovens to communicate with mixers, proofers, depositors, conveyors, cooling tunnels and packaging lines so plant managers can trace problems across the full production flow. Electric and hybrid heating will gain share where energy rules and utility economics support upgrades. Stronger suppliers will compete on lifecycle cost, uptime evidence, sanitation design and digital process control rather than heat capacity alone.

Buyer Decision-Making Criteria for Industrial and Commercial Bakery Operators

Industrial bakeries, foodservice chains and retail bakery operators evaluate suppliers through energy use, temperature consistency, throughput, cleaning access, automation readiness and service reach. Reliable product color and texture remain the first gate. Winning factors usually come later through lifecycle cost, installation speed, spare-part availability, validation support and the ability to handle more than one product format. Large bakery groups want global engineering consistency across plants. Smaller operators need financing flexibility, simple controls and fast maintenance support because skilled technicians are scarce in many markets.

Regulatory and Compliance Pressure on Bakery Thermal Equipment

Regulatory pressure is rising because ovens sit at the intersection of energy use, emissions, worker safety and food safety. European manufacturers and bakery operators face tighter expectations around industrial energy efficiency and low-emission production. U.S. buyers are paying closer attention to combustion safety, ventilation and sanitation design. China is pushing food equipment manufacturers toward smarter and more efficient factory systems. India is adding more scrutiny around electrical safety and equipment certification. The related requirements slow some imports but they also favor suppliers with documented engineering, installation support and clear compliance files.

Economic and Investment Analysis for Bakery Oven Buyers

Investment decisions are being shaped by energy prices, labor availability, chain bakery expansion, financing costs, stainless steel pricing and the pace of food-processing modernization. Higher interest rates can delay greenfield projects but high fuel bills still support upgrades that cut waste heat and downtime. Buyers increasingly model total lifecycle cost over several years because a lower purchase price can disappear quickly through gas use, unplanned maintenance and rejected batches. Capital is therefore moving toward automated tunnel systems, high-efficiency rack units, electric or hybrid zones, heat recovery modules, remote monitoring and regional service networks that protect uptime.

Investment Trends in Bakery Oven and Thermal Automation

Investment is moving away from basic capacity and toward equipment that can prove operating savings. Industries are opting for oven solutions that reduce fuel intensity, ensure consistent product quality, and reduce reliance on limited qualified personnel. Key capital allocation trends involve automatic tray loaders, upgrades of tunnel lines, IoT sensing, predictive maintenance systems, electric heating zones, hybrid fuel systems, heat recovery solutions, modular ovens and parts inventory close to major bakery centers. Capital allocation is also taking place in flexible solutions capable of producing bread, pastries, cookies, pizza crusts, frozen snacks and unique products in short production runs. Increased product diversity in retail and food service chains means increased value placed on quick changeover and consistency of settings.

Supply Chain Disruption Affecting Ovens, Controls and Heating Components

Supply risk now reaches beyond steel fabrication. Burners, PLCs, sensors, industrial controls, motors, fans, insulation and electrical assemblies can delay installations when one component is missing. German and Italian premium suppliers are exposed to long lead times for precision controls and heating assemblies while North American assemblers depend on Asian electrical components for many digital functions. Red Sea shipping pressure and tariff uncertainty can raise landed costs in Gulf and African projects. Buyers are responding by asking for spare-parts commitments, alternative component options and regional service support before signing equipment contracts.

Pricing Volatility

Equipment pricing is being reset by stainless steel costs, electrical components, skilled fabrication labor, freight and emissions-related redesign. Custom tunnel lines in the U.S. carry higher engineering and installation costs than standard catalog equipment. European suppliers in Italy and Germany maintain price premiums through reliability, hygiene design and compliance support. Chinese manufacturers are competing aggressively in Asia and Africa with lower-cost modular ovens. Procurement teams are therefore asking for indexed raw-material clauses, longer quote validity, documented energy payback and clearer spare-part pricing.

Procurement Pressure Across Foodservice Chains and Industrial Bakeries

Procurement teams are under pressure to reduce capital cost without creating future operating risk. Large food manufacturers in the U.S. and UK increasingly approve ovens based on lifecycle economics rather than lowest upfront cost. European buyers are narrowing supplier lists around automation, heat recovery and combustion controls. Indian and Indonesian operators still need financing flexibility and scalable layouts because many plants expand in phases. Vendors that cannot guarantee service response, spare-part availability and fast commissioning lose ground even when their base price looks attractive.

Technology Adoption in Smart Ovens, Heat Recovery and Predictive Maintenance

Technology adoption is strongest where it solves daily production problems. IoT-enabled systems help supervisors see burner drift, airflow imbalance, door losses, belt issues and temperature variation before quality drops. AI-assisted controls can recommend profile changes when dough hydration, line speed or product mix changes. Heat recovery systems are gaining attention because exhaust losses are a visible cost in bread and biscuit production. Digital twin research in bakery operations points to practical use cases such as real-time energy monitoring, predictive maintenance, waste heat recovery and renewable energy integration.

Regional Expansion Opportunities Beyond Traditional Bakery Hubs

Asia-Pacific provides the strongest expansion opportunity because China, India and Indonesia combine urban foodservice demand with packaged bakery production and supermarket expansion. Import demand is strongest where local plants need automated tunnel lines or premium systems for frozen bakery and quick-service restaurant supply chains.

The Gulf is becoming a more strategic destination for high-capacity systems. Saudi Arabia and UAE are investing in food-security infrastructure, hospitality supply chains and modern retail formats. European ovens often win premium projects because buyers want hygiene design, throughput reliability and service-backed commissioning. Local partnerships remain important because installation windows are tight and maintenance support can decide repeat orders.

Government Policy Support for Energy Efficiency and Food Processing Modernization

Policy support is linked to factory efficiency, food processing investment and cleaner industrial heat. China’s smart manufacturing agenda supports automated food equipment and domestic production capability. European decarbonization programs are encouraging bakery plants to examine electric zones, hybrid systems and heat recovery. India’s food-processing incentives support organized bakery capacity and equipment upgrades. U.S. manufacturing and energy-efficiency programs indirectly support smart thermal automation through broader factory modernization and energy transition spending.

Import-Export and Pricing Intelligence for Industrial Bakery Equipment

Global trade patterns favor high-value exports from Germany, Italy and the U.S. for automated tunnel systems, modular bakery lines and precision thermal equipment. Asian importers continue buying premium European systems where product consistency and commissioning support matter. Regional assembly is becoming more attractive because it can reduce tariff exposure, shipping cost and service delays.

Pricing is increasingly tied to automation depth, energy performance, hygiene design and digital controls rather than oven size alone. European OEMs defend premium positions through engineering reliability and regulatory alignment. Asian suppliers compete through affordability and faster modular delivery. Buyers now compare lifecycle efficiency, predictive maintenance savings, utility consumption and local service capability before deciding whether a premium quote is justified.

| HS Code | Reporter | Trade Flow | 2025 Trade Value | Interpretation |

| 851410 | Germany | Export | USD 1.42 Billion | Germany remains the leading exporter of industrial electric ovens and thermal bakery systems with strong EU and Middle East penetration |

| 851419 | Italy | Export | USD 986 Million | Italy continues strengthening premium bakery machinery exports driven by artisan and industrial bakery automation demand |

| 851410 | United States | Import | USD 812 Million | Rising imports indicate strong replacement demand for energy-efficient industrial baking systems across commercial food manufacturing |

| 851419 | China | Export | USD 1.18 Billion | China is expanding global market share through competitively priced commercial baking ovens and modular thermal systems |

AI Impact Analysis Across Bakery Production and Oven Maintenance

AI is becoming useful where it reduces variation and unplanned downtime. High-volume plants can use sensor data to compare heat balance, belt speed, airflow, humidity and product color against target profiles. Machine-learning tools can flag burner inefficiency, fan wear, sensor drift and likely quality defects before operators see visible product loss. Predictive maintenance matters because a stoppage during bread or biscuit production can waste dough, labor and packaging schedules. Value will depend on clean plant data and operator trust rather than software claims alone.

Disruption Analysis Across Electrification, Labor and New Bakery Formats

Electrification and hybrid heating are disrupting equipment planning because many plants cannot meet carbon goals through fuel switching alone. They need staged upgrades, heat recovery and more precise controls. Labor pressure is another disruption. Automation is being justified less as a futuristic project and more as insurance against missed production schedules. New bakery formats are also changing equipment design. Cloud kitchens, grocery in-store bakeries, convenience stores and small premium bakeries want compact ovens with digital recipes and simple maintenance. Large industrial plants want connected tunnel lines and automated loading. Suppliers that can serve both ends of this spectrum will have a wider route to growth.

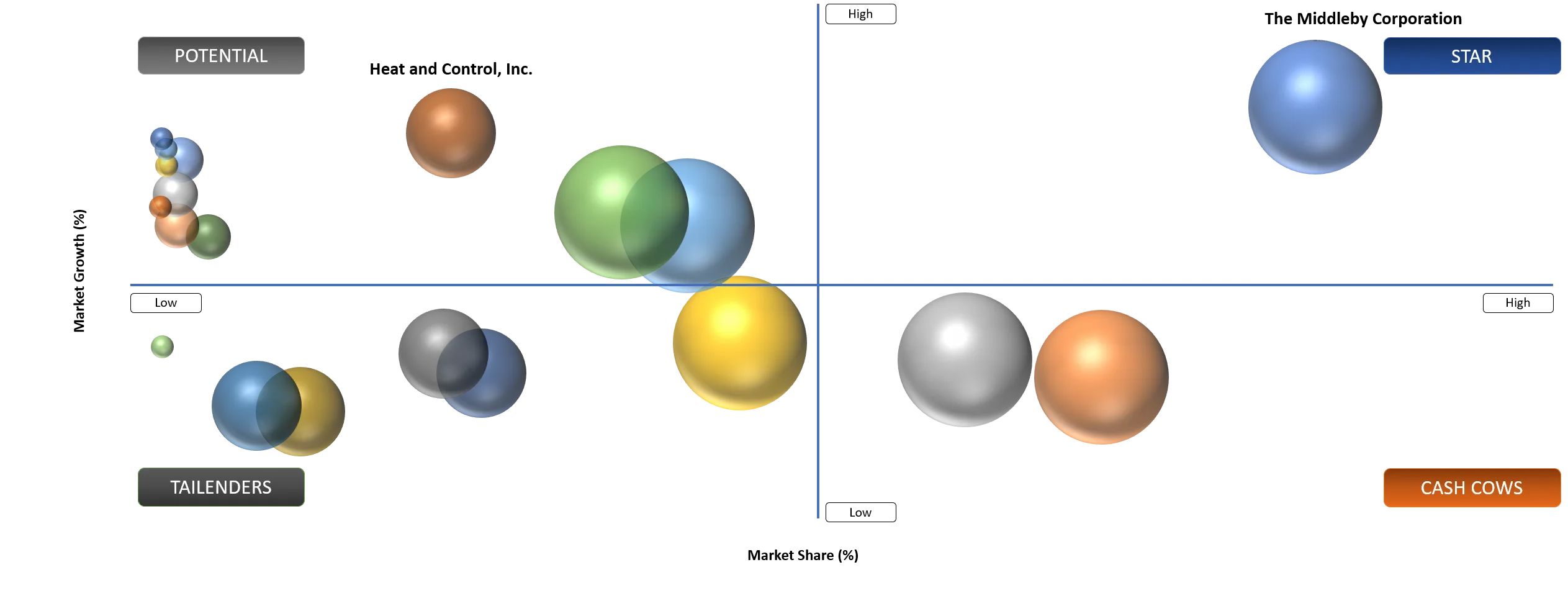

BCG Matrix Evaluation Based on Product Breadth, Service Strength and Digital Readiness

Star

Star players are the suppliers with broad product portfolios, proven industrial engineering and credible digital upgrades. Middleby, GEA, Bühler, Reading Bakery Systems, Markel Food Group, MIWE, Kaak and Rademaker are well positioned where customers need automated lines, thermal consistency and service support. The related strength comes from engineering depth, installed base, application knowledge and the ability to support complex bakery projects across multiple regions.

Potential

Potential players include specialized oven makers and regional suppliers serving artisan bakeries, hotels, institutional kitchens and small food processors. The related companies can win through customization, local service and affordable systems but they face limits in international commissioning, automation depth and financing support. Suppliers that add digital controls, energy documentation and service partnerships can move upward in value. Low-cost fabricators that remain focused on basic heat chambers will face margin pressure from both premium integrated systems and lower-cost Asian competition.

Market Dynamics

Driver Impact Analysis

| Driver | Market Growth Impact (%) | Demand Concentration | Impacted Use Case | Strategic Impact |

Rising Demand for Automated and Energy-Efficient Baking Systems | 5.00% | North America, Western Europe, Japan, South Korea and large-scale industrial bakery clusters | Continuous bread production, commercial baking automation, energy optimization in food processing | Rising Demand for Automated and Energy-Efficient Baking Systems |

Expanding Consumption of Packaged Bakery and Ready-to-Eat Products | 5.30% | Urban consumer markets across Asia-Pacific, North America and the Middle East | Bread, cakes, pastries, frozen bakery products and quick-service restaurant applications | Expanding Consumption of Packaged Bakery and Ready-to-Eat Products |

Increasing Investments in Smart Bakery Manufacturing and Industry 4.0 Integration | 4.60% | Advanced food manufacturing hubs in Germany, U.S., China and Italy | Automated temperature control, IoT-enabled baking systems, predictive maintenance | Increasing Investments in Smart Bakery Manufacturing and Industry 4.0 Integration |

Growing Expansion of Quick-Service Restaurants, Artisan Bakeries and Foodservice Chains | 4.20% | Rapidly urbanizing economies and metropolitan foodservice ecosystems | Pizza ovens, convection ovens, deck ovens and multi-functional commercial baking equipment | Growing Expansion of Quick-Service Restaurants, Artisan Bakeries and Foodservice Chains |

Driver: QSR, Retail Bakery and Convenience Formats Are Reshaping Oven Demand

Quick-service restaurants, supermarket bakeries and convenience stores are changing the product brief for commercial ovens. Chains do not only need speed. They need repeatable output from staff with different skill levels and high turnover. Programmable convection systems, rapid-bake units and compact deck or combi formats allow outlets to standardize buns, pizza bases, pastries, sandwiches and snacks across many locations. Store operators also want easy cleaning and remote fault alerts because a failed oven during peak hours can reduce sales immediately.

Food delivery and cloud kitchen models add another layer. Kitchen space is expensive in dense cities so operators favor smaller electric systems with fast heat recovery and flexible menus. Retailers are also using in-store baking to pull customers toward fresh bread and snack counters. Equipment suppliers that understand store-level workflows can create value through training, simple interfaces and service contracts. The shift is not only about selling more units. It is about designing ovens that support decentralized fresh-food production.

Restraint Impact Analysis

| Restraint | Drag on Market Growth (%) | Primary Impact Area | Impacted Use Case | Strategic Impact |

High Energy Consumption and Rising Utility Costs | 4.50% | Industrial baking operations and operating expenditure | Continuous commercial baking, large-scale food production facilities | Increases production costs and limits profitability for small and medium-sized bakeries |

High Initial Capital Investment for Advanced Baking Ovens | 4.10% | Equipment modernization and production scalability | Automated tunnel ovens, smart baking systems, high-capacity industrial bakeries | Delays technology adoption and expansion plans among emerging bakery manufacturers |

Complex Maintenance Requirements and Downtime Risks | 3.70% | Equipment reliability and operational continuity | Continuous baking lines, multi-deck industrial ovens | Reduces production efficiency and increases maintenance-related operational disruptions |

Shortage of Skilled Workforce for Automated Baking Systems | 3.40% | Smart oven operation and process optimization | AI-enabled baking systems, programmable industrial ovens, precision baking applications | Slows digital transformation and limits efficient utilization of advanced baking technologies |

Restraint: Energy Cost and Modernization Barriers in Bakery Plants

Bakery ovens run for long hours and often sit at the center of a plant’s energy bill. Gas volatility, electricity tariffs and emissions rules make older systems harder to justify even when they still run mechanically. A poorly insulated chamber, drifting burner or weak airflow system can waste fuel and create inconsistent product quality at the same time. Industrial bakers are therefore reviewing heat recovery, zone controls, exhaust management and preventive maintenance as part of the same modernization decision.

Financing remains the barrier for small and mid-sized operators. Advanced electric, hybrid and connected systems cost more upfront than conventional units. Import duties, installation work and operator training can add further pressure in emerging markets. The payback case is strongest when vendors can show lower utility use, less scrap, faster changeover and fewer service calls. Leasing, staged retrofits and performance-linked service contracts can help suppliers unlock buyers that want modernization but cannot absorb a full replacement project immediately.

Segmentation Analysis

The industry should be assessed through operating use cases rather than equipment labels alone. Industrial plants need continuous systems with stable thermal profiles, automated loading and strong sanitation access. Foodservice chains need repeatable small-footprint units. Retail bakeries need versatile equipment for short runs and visible freshness. Each use case has a different buying logic and therefore requires a different supplier proposition.

By End-User

Industrial Bakery Lines Require Heat Discipline, Uptime and Repeatable Quality

Industrial bakeries use advanced ovens because their economics depend on continuous output and low waste. Bread, buns, cookies, crackers, cakes, frozen pizza and snack products often move through long lines where one weak zone can affect texture, color and moisture. Grupo Bimbo and other large bakery groups operate extensive manufacturing networks that rely on automated tunnel, rotary rack and conveyor systems to keep product standards consistent across regions.

Modern industrial ovens increasingly include computerized temperature control, humidity management, automated loading, energy recovery and connected diagnostics. The related features are not luxury additions. They reduce operator dependence and help plants react to ingredient variation, line speed changes and maintenance issues. Industry discussion around IBIE 2025 also points to faster adoption of automation because labor constraints have changed how bakers justify projects.

Frozen bakery and ready-to-bake products add further complexity. A plant may need to produce high volumes while switching between SKUs more often than in the past. Predictive maintenance and IoT monitoring help reduce line stoppage while heat recovery and better insulation support lower energy intensity. Suppliers with recipe transfer support and fast service response will be more valuable than vendors selling only mechanical capacity.

By Baking Format

Artisan, Retail and Specialty Baking Needs Flexible Heat Control

Premium bakeries, cafes and hotel kitchens need ovens that can deliver crust, steam, color and texture without large industrial footprints. Demand for sourdough, laminated pastries, gluten-free products and regional specialty items has pushed buyers toward deck ovens, convection systems and steam-assisted formats with tighter process control. Many smaller operators now expect programmable profiles and touch-screen controls because consistency matters even when production is limited.

Social media has changed product cycles. A bakery can see sudden demand for a seasonal pastry, stuffed bread, premium cookie or specialty pizza base and needs equipment that adapts quickly. Online ordering and local delivery have also created demand for compact commercial systems that can sit inside small kitchens. Energy-efficient ovens with simple controls are therefore moving into boutique bakeries, supermarket counters and semi-commercial food businesses that once relied on basic equipment.

Market Segmentation

- By Oven Type

- Rack Ovens

- Reel Ovens

- Deck Ovens

- Tunnel Ovens

- Rotary Ovens

- Convection Ovens

- Hybrid Ovens

- Combi Ovens

- By Heat Source

- Gas Fired

- Electric

- Dual Energy

- Indirect Fired Thermal Oil

- Steam Assisted

- By Automation Level

- Manual

- Semi Automatic

- Fully Automatic

- By Capacity

- Small Batch

- Medium Throughput

- High Throughput Industrial

- By Baking Format

- Bread and Rolls

- Cookies and Biscuits

- Crackers

- Cakes and Pastries

- Pizza Bases and Flatbreads

- Wafers and Cones

- Pet Food and Specialty Snacks

- By Purchase Type

- New Installation

- Retrofit and Line Expansion

- Oven Zone Upgrade and Electrification

- By End-User

- Commercial Food Service

- Bakeries

- Restaurants and Cafés

- Pizzerias

- Cloud Kitchens

- Others

- Hospitality and Institutional

- Hotels and Resorts

- Hospitals and Healthcare Facilities

- Educational & Institutions

- Others

- Corporate Offices

- Residential

- Industries

- Supermarket and Hypermarket

- Others

- Commercial Food Service

Geographical Analysis

North America: Automation, Labor Relief and Connected Bakery Lines

North America remains an advanced buying environment because bakery operators are dealing with labor scarcity, high wages, supermarket in-store baking and large packaged-food production networks. U.S. and Canadian buyers are interested in programmable controls, remote diagnostics, predictive maintenance and energy optimization because these tools reduce daily operating risk. Food safety expectations also favor equipment with cleanable surfaces, controlled temperatures and reliable production records.

Automation investment is now tied directly to workforce realities. Baking Business reported that automation and higher wages helped ease labor challenges in the 2025 industrial baking study. Large bakeries still need experienced technicians but connected systems reduce the number of manual checks needed on every shift. Retail and foodservice chains are also adopting smaller programmable units that allow less-experienced staff to produce consistent baked items.

U.S. Market: Replacement Demand, Flour Consumption and Store-Level Fresh Baking

The U.S. remains a high-value equipment market because bread, pizza, pastries, cookies and snack foods are deeply embedded in retail and foodservice consumption. USDA-linked flour consumption data continues to show a large base for wheat-based products. Large bakery groups, supermarket chains, fast-food operators and convenience stores are using equipment upgrades to protect freshness, consistency and labor productivity. Replacement demand is also being supported by aging gas-fired equipment that lacks heat recovery and digital controls.

Sustainability and operating cost are reshaping purchase justification. U.S. buyers increasingly ask whether a new oven can lower fuel use, reduce scrap and simplify maintenance. Cloud kitchens and delivery-focused foodservice formats are expanding demand for compact electric systems that fit small kitchens and support several menu items. Domestic equipment innovation is focusing on connected controls, AI-assisted temperature logic, cloud-based monitoring and sanitation-friendly design.

Asia-Pacific: Packaged Bakery Expansion Meets Industrial Automation

Asia-Pacific combines consumer expansion with manufacturing build-out. China, India and Indonesia are seeing more packaged bakery, convenience food, cafe and quick-service restaurant activity. The region also contains a wide equipment spectrum from low-cost local machines to premium imported tunnel systems. Urban chains are pushing bakeries toward consistent output and larger batch sizes while retailers want fresh products closer to consumers. The following combination supports both industrial lines and compact retail formats.

Japan Market: Convenience Store Baking and Precision Equipment Demand

Japan is a distinctive market because convenience stores play a large role in daily food retail. Fresh bread, pastries and ready-to-eat products require compact ovens that fit limited back-of-store space while delivering reliable color and texture. Japanese buyers also value clean design, low noise, energy efficiency and precise controls. Steam-assisted and multifunction systems are well suited to bakeries that need quality consistency without large production areas.

Bakery franchises, cafes and specialty shops in Japan are adding programmable systems because product quality is central to the customer experience. Smaller kitchens need fast preheat, safe ventilation and simple cleaning. Interest in Western baked products sits alongside local preferences for softness, freshness and visual presentation. Suppliers that combine compact design with service reliability can build strong repeat business in this market.

Competitive Landscape

- Competition is split between global food equipment groups, industrial bakery specialists, regional oven manufacturers and low-cost fabricators. Premium suppliers compete through engineering reliability, automation depth, sanitation design and service coverage.

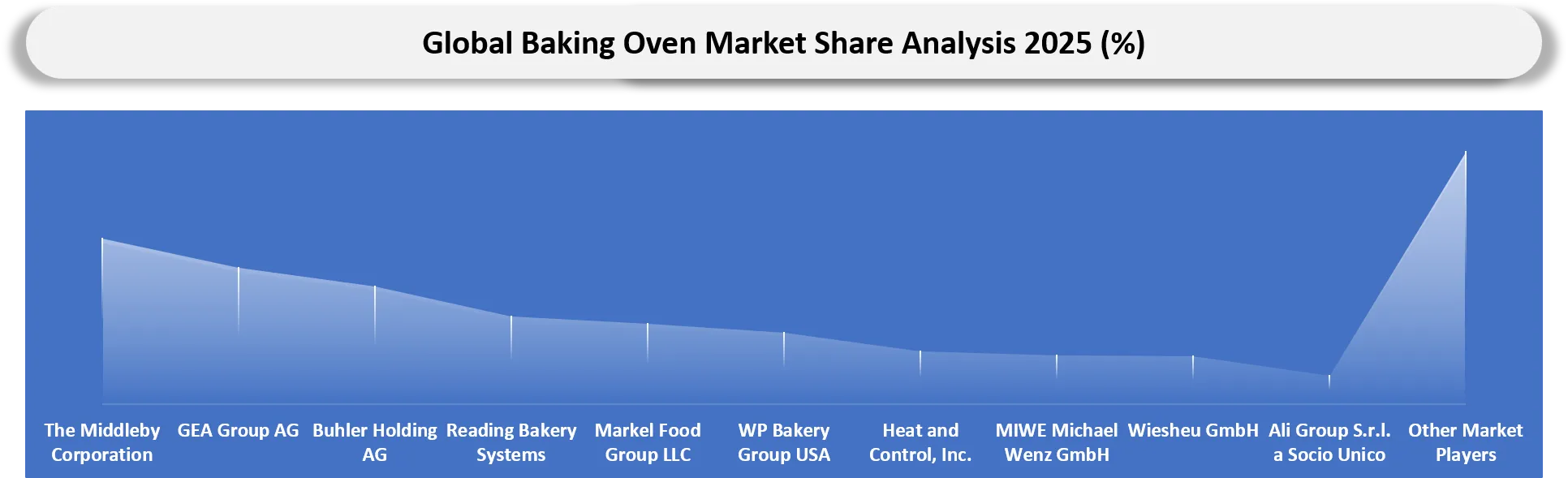

- Key participants include The Middleby Corporation, GEA Group AG, Bühler Holding AG, Reading Bakery Systems, Markel Food Group LLC, Heat and Control, MIWE, Kaak Group, Baker Perkins, Revent, Salva Industrial, Spooner Industries and Rademaker.

- Differentiation is moving toward hybrid heating, heat recovery, predictive maintenance, remote diagnostics, recipe controls and modular line integration. Suppliers that can document utility savings and uptime performance have a stronger sales case.

- Strategic focus is shifting from equipment delivery to lifecycle support. Bakery operators want commissioning help, operator training, spare parts, calibration support and upgrade paths that keep lines useful for longer.

Coverage Preview and Competitive Positioning

The Middleby Corporation remains one of the most influential suppliers in this category because it combines commercial foodservice equipment, bakery processing assets and industrial line expertise. The company’s bakery strategy has been strengthened through acquisitions and a broad portfolio that includes tunnel systems, conveyor ovens, proofing, depositing and automated workflows. Middleby’s advantage sits in the ability to serve chains and industrial plants with connected controls, energy-focused engineering and service-backed installations. Its position is strongest where customers want integrated production systems rather than a single oven purchase.

Key Companies

- The Middleby Corporation

- GEA Group AG

- Buhler Holding AG

- Reading Bakery Systems

- Markel Food Group LLC

- WP Bakery Group USA

- Heat and Control, Inc.

- MIWE Michael Wenz GmbH

- Wiesheu GmbH

- Ali Group S.r.l. a Socio Unico

- Kaak Group B.V.

- Spooner Industries Limited

- Baker Perkins Ltd

- Revent International AB

- Salva Industrial S.A.

- Sveba Dahlen Group

- J4 s.r.o.

- Memak Endustriyel Gida Makinalari Sanayi ve Ticaret A.S.

- Davron Technologies, Inc.

- Rademaker B.V.

Major Pain Points in Bakery Equipment Procurement and Operation

- Industrial ovens consume large amounts of electricity or gas so utility volatility can quickly weaken bakery margins.

- Advanced tunnel, rack and hybrid systems require high upfront capital which slows modernization among small and mid-sized bakeries.

- Food safety rules, sanitation expectations and emission requirements are raising documentation and engineering demands for manufacturers.

- End users want heat recovery, low-emission design and digital controls but many plants lack the budget or staff to upgrade everything at once.

- Burner issues, conveyor wear, fan imbalance, sensor drift and control failures can disrupt production and create costly product waste.

- Large production lines still struggle with even heat distribution, airflow balance and moisture control across changing product formats.

- Skilled technicians remain hard to recruit which makes training, remote support and predictive maintenance more valuable.

Recent Developments

- March 2026: Heat and Control, Inc. developed high-efficiency baking and thermal processing systems, focusing on automation, reduced waste and optimized heat transfer for industrial bakery applications.

- March 2026: Revent International AB launched energy-efficient rack ovens with improved airflow technology and digital interfaces, targeting artisan and retail bakery segments globally.

- March 2026: The Middleby Corporation expanded automated baking oven portfolio integrating IoT-enabled controls, enhancing industrial bakery throughput, energy efficiency and predictive maintenance capabilities globally.

- February 2026: Bühler Holding AG strengthened modular baking solutions with advanced automation and sustainability features, enabling scalable industrial bakery operations and reducing energy consumption significantly.

- February 2026: Davron Technologies, Inc. advanced custom industrial oven solutions for bakery applications, focusing on precision thermal control, process optimization and high-volume production efficiency.

- February 2026: Wiesheu GmbH introduced advanced in-store baking ovens with smart controls and energy optimization, targeting retail bakeries and foodservice operators across Europe.

- January 2026: GEA Group AG introduced energy-efficient industrial baking systems with digital monitoring platforms, supporting sustainable production and automated bakery line optimization across Europe and North America.

- January 2026: MIWE Michael Wenz GmbH expanded professional deck and rack oven portfolio emphasizing energy-efficient baking, digital control integration and artisan bakery performance optimization worldwide.

- January 2026: Rademaker B.V. enhanced integrated bakery systems combining oven technologies with automated production lines, improving efficiency, flexibility and product consistency globally.

Analyst Insights on Bakery Equipment Strategy Through 2035

DataM Intelligence views this category as attractive because demand is tied to structural changes in food production rather than simple store openings. Frozen bakery, supermarket fresh programs, quick-service restaurants and convenience retail are all pushing operators toward better heat control and faster equipment recovery. Replacement demand is also rising because older gas systems often lack heat recovery, digital diagnostics and recipe repeatability.

Asia-Pacific leads volume opportunity because packaged bakery and organized foodservice are expanding across China, India, Indonesia and other urban markets. North America and Europe set premium specification expectations through automation, safety standards, energy efficiency and connected maintenance. The Middle East is becoming more attractive for high-capacity systems as food-security policy and hospitality demand support modern bakery infrastructure.

By 2035, winning suppliers will combine thermal engineering, digital controls, recipe support, spare-part reach and credible energy-performance evidence. Low-cost fabrication alone will face margin pressure. Suppliers that invest in automation, multi-product flexibility, service contracts and retrofit pathways will capture stronger retention and better margins across industrial and commercial bakery accounts.

Target Audience

| INDUSTRY | WHO SHOULD BUY THIS REPORT? | REASON TO BUY THIS REPORT |

| Commercial Bakery Chains | Bakery Production Managers, Operations Heads, Equipment Procurement Teams | Analyze demand trends for industrial baking ovens across bread, pastry, cake and frozen bakery production lines |

| Food Processing Companies | Thermal Processing Engineers, Plant Managers, Manufacturing Heads | Evaluate high-capacity baking oven solutions for large-scale processed food and ready-to-eat product manufacturing |

Quick Service Restaurants (QSRs) & Foodservice Chains | Kitchen Operations Teams, Franchise Development Managers, Culinary Equipment Buyers | Assess commercial oven technologies for fast, energy-efficient and standardized food preparation operations |

| Industrial Oven Manufacturers | Product Development Teams, Heating Technology Engineers, Strategic Planning Departments | Understand evolving demand for convection, rotary rack, deck and tunnel baking oven technologies |

| Frozen Food Manufacturers | Frozen Bakery Production Teams, Industrial Engineers, Automation Specialists | Identify baking oven requirements for high-throughput frozen pizza, snacks and bakery product manufacturing |

Hospitality & Hotel Groups | Executive Chefs, Central Kitchen Managers, Procurement Departments | Evaluate versatile baking oven systems for premium bakery, confectionery and large-scale catering applications |

Confectionery & Snack Manufacturers | Food Innovation Teams, Production Supervisors, Process Engineering Departments | Analyze precision baking solutions for cookies, biscuits, crackers and snack product consistency |

Industrial Automation & Smart Kitchen Technology Providers | Industry 4.0 Teams, Automation Engineers, Digital Manufacturing Consultants | Assess integration opportunities between baking ovens, IoT systems, AI-driven controls and smart factory operations |

Energy & Utility Solution Providers | Energy Efficiency Consultants, Sustainability Teams, Industrial Utility Managers | Study energy-efficient baking oven technologies, heat recovery systems and low-emission industrial baking solutions |

Investors, Private Equity & Consulting Firms | Investment Analysts, Food Industry Consultants, Market Intelligence Teams | Evaluate growth opportunities, competitive benchmarking and technology adoption trends in the global baking oven market |

WHY CHOOSE DATAM?

- White Papers and Case Studies: Benefit quarterly from our in-depth studies related to your purchased titles, tailored to refine your operational and marketing strategies for maximum impact.

- Annual Updates on Purchased Reports: As an existing customer, enjoy the privilege of annual updates to your reports, ensuring you stay abreast of the latest market insights and technological advancements. Terms and conditions apply.

- Specialized Focus on Emerging Markets: DataM differentiates itself by delivering in-depth, specialized insights specifically for emerging markets, rather than offering generalized geographic overviews. The approach equips our clients with a nuanced understanding and actionable intelligence that are essential for navigating and succeeding in high-growth regions.

- Value of DataM Reports: Our reports offer specialized insights tailored to the latest trends and specific business inquiries. The personalized approach provides a deeper, strategic perspective, ensuring you receive the precise information necessary to make informed decisions. The insights complement and go beyond what is typically available in generic databases.

WHAT DATAM UNIQUELY PROVIDES

- Tracks industrial bakery oven replacement cycles across commercial, frozen bakery and foodservice production ecosystems globally.

- Maps real-time investment activity among bakery automation manufacturers, thermal processing OEMs and food-processing infrastructure developers.

- Provides detailed benchmarking of tunnel, deck, rack and conveyor oven technologies across industrial bakery applications.

- Analyzes regional procurement behavior for energy-efficient, AI-enabled and low-emission baking systems among commercial operators.

- Tracks bakery equipment M&A activity influencing integrated thermal processing and automated production line consolidation strategies.

- Evaluates supply-chain dependencies for burners, industrial steel, electronic controls and precision thermal management components.

- Delivers country-level trade intelligence covering industrial oven exports, imports, pricing dynamics and competitive manufacturing positioning.

QUESTIONS THIS REPORT ANSWERS

- What is the current and forecast market size of the global baking oven market through 2035?

- Which end-users are driving demand growth and why?

- Which regions and oven types present the highest growth and investment opportunities in the global baking oven market?

- How are investments in smart baking technologies, energy-efficient systems and automation reshaping production models and competitive dynamics?

- How do food safety regulations, energy efficiency standards and geopolitical supply chain risks impact baking oven manufacturing and deployment?

- Which heating technologies are shaping next-generation baking oven manufacturing?