Global Autosomal Dominant Polycystic Kidney Disease (ADPKD) Market: Industry Outlook

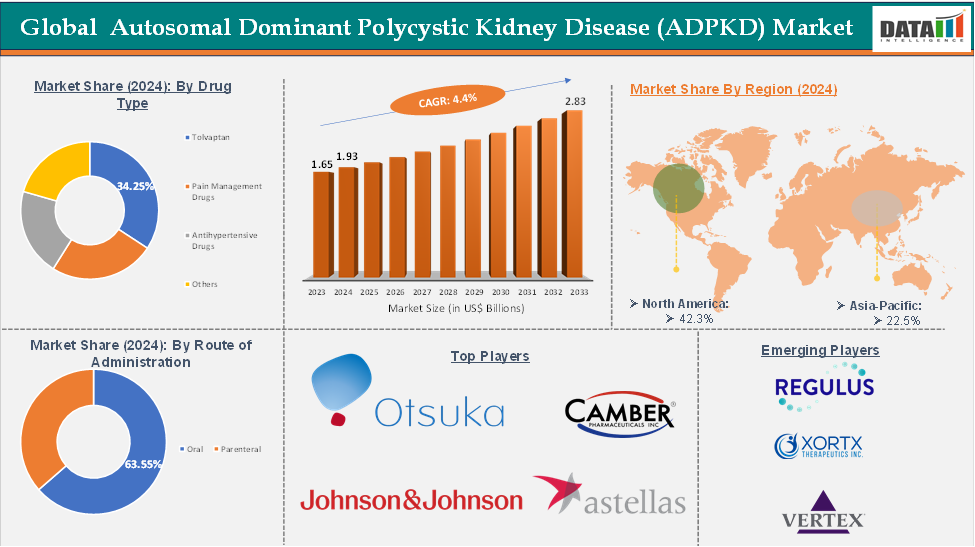

The global autosomal dominant polycystic kidney disease (ADPKD) market reached US$ 1.65 Billion in 2023, with a rise of US$ 1.93 Billion in 2024 and is expected to reach US$ 2.83 Billion by 2033, growing at a CAGR of 4.4% during the forecast period 2025-2033.

The global autosomal dominant polycystic kidney disease (ADPKD) market is experiencing significant transformation due to increasing disease prevalence, medical research advancements, and a growing focus on rare and genetic disorders. ADPKD is the most common inherited kidney disorder, affecting millions worldwide and often leading to end-stage renal disease, necessitating dialysis or kidney transplantation. Advancements in diagnostic tools and understanding of the disease's genetic and molecular basis have contributed to early diagnosis and personalized treatment approaches.

The market has seen promising developments with the approval of disease-modifying drugs like Tolvaptan, which have demonstrated efficacy in slowing cyst growth and preserving kidney function. Pharmaceutical companies are increasingly investing in this space, encouraged by orphan drug incentives and regulatory support across key regions like North America and Europe.

North America remains the leading region in terms of market share, supported by a well-established healthcare infrastructure, favorable reimbursement policies, and strong awareness levels among healthcare providers and patients. Asia-Pacific is expected to witness the fastest growth due to rising healthcare expenditure, improved access to specialized treatments, and a growing patient pool.

Global Autosomal Dominant Polycystic Kidney Disease (ADPKD) Market: Executive Summary

Global Autosomal Dominant Polycystic Kidney Disease (ADPKD) Market Dynamics: Drivers & Restraints

Driver: Rising prevalence of genetic kidney disorders

The rise in the prevalence of genetic kidney disorders, particularly autosomal dominant polycystic kidney disease (ADPKD), is driving market growth. ADPKD, a leading cause of end-stage renal disease, affects millions globally. As awareness and diagnostic tools improve, more cases are identified earlier, leading to higher prevalence rates. This, combined with increased screening through family history and genetic testing, creates a demand for targeted therapies and long-term disease management strategies. This growing patient pool prompts governments and healthcare providers to prioritize ADPKD in broader kidney health initiatives.

For instance, over 200 genetic kidney diseases account for 70% of children and 10% of adults with stage 5 Chronic Kidney Disease (CKD5), necessitating renal replacement therapy like dialysis and transplantation, with an overall prevalence of 60-80% per 100,000.

Driver: Advancements in therapeutic options

The global autosomal dominant polycystic kidney disease market is experiencing significant changes due to advancements in therapeutic options. The first disease-modifying therapy, Tolvaptan, has been approved, targeting ADPKD by inhibiting vasopressin, reducing cyst growth, and preserving kidney function. This innovation has improved patient outcomes and opened the door for further research into targeted treatments.

Clinical trials are also exploring gene therapies, anti-inflammatory agents, and cyst-reducing compounds, paving the way for more effective and personalized treatment strategies. These developments are driving interest from pharmaceutical companies, encouraging investment, and creating a dynamic market environment.

Restraint: High cost of treatment and monitoring

The global autosomal dominant polycystic kidney disease (ADPKD) market faces significant challenges due to high treatment costs and ongoing monitoring. Disease-modifying therapies like Tolvaptan are expensive, particularly in low- and middle-income countries. Continuous monitoring through advanced imaging and specialist consultations contributes to long-term healthcare expenses.

As the disease progresses, many patients require dialysis or kidney transplantation, further increasing costs. Limited reimbursement policies and out-of-pocket expenses hinder patient access to necessary treatments, even in developed regions. This economic barrier affects treatment adherence and slows the adoption of novel therapies, impacting market growth.

Opportunity: Development of gene-based and targeted therapies

The global autosomal dominant polycystic kidney disease (ADPKD) market is poised for a transformative opportunity in gene-based and targeted therapies. ADPKD, a monogenic disorder caused by mutations in the PKD1 or PKD2 genes, is a prime candidate for innovative treatments. Advances in gene editing technologies like CRISPR-Cas9, RNA interference, and antisense oligonucleotides are paving the way for precise, disease-modifying interventions.

Pharmaceutical companies are developing targeted molecules and biologics to inhibit the molecular pathways driving cyst growth, fibrosis, and inflammation in ADPKD. These breakthroughs have the potential to dramatically alter disease progression and improve long-term outcomes. With increasing R&D investment, strategic partnerships, and personalized medicine interest, the development of gene-based and targeted therapies is poised to revolutionize the treatment landscape.

For more details on this report, Request for Sample

Global Autosomal Dominant Polycystic Kidney Disease (ADPKD) Market Segment Analysis

The global autosomal dominant polycystic kidney disease (ADPKD) market is segmented based on drug type, route of administration, distribution channel, and region.

Drug Type:

The tolvaptan segment from the drug type is expected to hold 34.25% of the autosomal dominant polycystic kidney disease (ADPKD) market

Tolvaptan is the first FDA-approved disease-modifying therapy for Autosomal Dominant Polycystic Kidney Disease (ADPKD), aimed at slowing its progression. It inhibits vasopressin V2 receptors, reducing fluid accumulation in kidney cysts and slowing cyst growth, preserving kidney function over time. Clinical trials like TEMPO 3:4 and REPRISE have shown their efficacy in delaying kidney function decline in patients at risk of rapid disease progression.

Tolvaptan's approval marked a major therapeutic breakthrough, driving increased physician awareness, stimulating further research, and expanding the commercial potential of the ADPKD market. However, its high cost and risk of liver toxicity necessitate careful patient selection and regular monitoring, making its use most impactful in specialized care settings.

Global Autosomal Dominant Polycystic Kidney Disease (ADPKD) Market - Geographical Analysis

North America dominated the global autosomal dominant polycystic kidney disease (ADPKD) market with the highest share of 42.3% in 2024

North America is driving the growth of the global autosomal dominant polycystic kidney disease (ADPKD) market due to its advanced healthcare infrastructure, high prevalence of diagnosed cases, and early adoption of novel treatment options. The region benefits from strong R&D activity, favorable regulatory frameworks from the U.S. FDA, and high public awareness. Advanced imaging technologies and comprehensive insurance coverage support disease management in early and late stages, making North America a mature and innovation-driven market for ADPKD.

For instance, in May 2025, Lupin Limited, a global pharma company, announced the launch of Tolvaptan Tablets in the US, with the company holding the exclusive first-to-file status and 180-day generic drug exclusivity, following approval from the US FDA.

Asia-Pacific is the global autosomal dominant polycystic kidney disease (ADPKD) market with a market share of 22.5% in 2024

The Asia Pacific region is gaining momentum in the global ADPKD market due to increased disease awareness, healthcare expenditure, and diagnostic access. Countries like China, Japan, South Korea, and India are improving kidney disease screening programs and integrating genetic testing for earlier diagnosis. Government initiatives and public-private partnerships are promoting the development of ADPKD treatments. The growing middle class and large patient population create commercial opportunities for pharmaceutical companies to introduce novel therapies, positioning the region as a high-potential area for future ADPKD market expansion.

For instance, in February 2024, Rege Nephro Co., Ltd., a Kyoto University start-up, developed tamibarotene, a retinoic acid receptor agonist, as a clinical treatment for autosomal dominant polycystic kidney disease (ADPKD). The company-sponsored clinical trial, which will begin in mid-April 2024 or later in Japan, will recruit subjects in phases to ensure patient safety. The trial will begin in Japan once safety and tolerability are assured.

Global Autosomal Dominant Polycystic Kidney Disease (ADPKD) Market - Key Players

The major global players in the Autosomal Dominant Polycystic Kidney Disease (ADPKD) market include Otsuka Pharmaceutical Co., Ltd, Camber Pharma, Astellas Pharma, and Johnson & Johnson, among others.

Global Autosomal Dominant Polycystic Kidney Disease (ADPKD) Market – Key Developments

In January 2025, Regulus Therapeutics Inc., a biopharmaceutical company focused on developing innovative microRNA-targeted medicines, announced positive clinical and regulatory updates from its ADPKD program. The company has reported positive topline results from an interim analysis of the fourth cohort of its Phase 1b Multiple Ascending Dose study of farabursen (RGLS8429) for ADPKD treatment and a successful End-of-Phase 1 meeting with the FDA.

Global Autosomal Dominant Polycystic Kidney Disease (ADPKD) Market: Scope

Metrics | Details | |

CAGR | 4.4% | |

Market Size Available for Years | 2022-2033 | |

Estimation Forecast Period | 2025-2033 | |

Revenue Units | Value (US$ Bn) | |

Segments Covered | Type | Tolvaptan, Pain Management Drugs, Antihypertensive Drugs, Others |

Route of Administration | Oral, Parenteral | |

| Distribution Channel | Hospital Pharmacies, Retail Pharmacies, Online Pharmacies |

Regions Covered | North America, Europe, Asia-Pacific, South America, and the Middle East & Africa | |

DMI Insights:

The global autosomal dominant polycystic kidney disease (ADPKD) market is expected to grow from US$ 1.93 billion in 2024 to US$ 2.83 billion by 2033, at a CAGR of 4.4%. This growth is driven by the increasing prevalence of genetic kidney disorders and the need for long-term management strategies. The market is dominated by North America, with robust R&D ecosystems, reimbursement frameworks, and high diagnostic capabilities. The Asia-Pacific region presents an emerging growth frontier due to healthcare investments, specialized diagnostics, and patient awareness. However, the high cost of novel treatments and monitoring remains a challenge, especially in developing regions. The future of ADPKD is promising, with gene-based and precision therapies opening new doors for disease intervention.

The global autosomal dominant polycystic kidney disease market report delivers a detailed analysis with 67+ key tables, more than 55+ visually impactful figures, and 185 pages of expert insights, providing a complete view of the market landscape.