Automotive Engineering Services Market Size

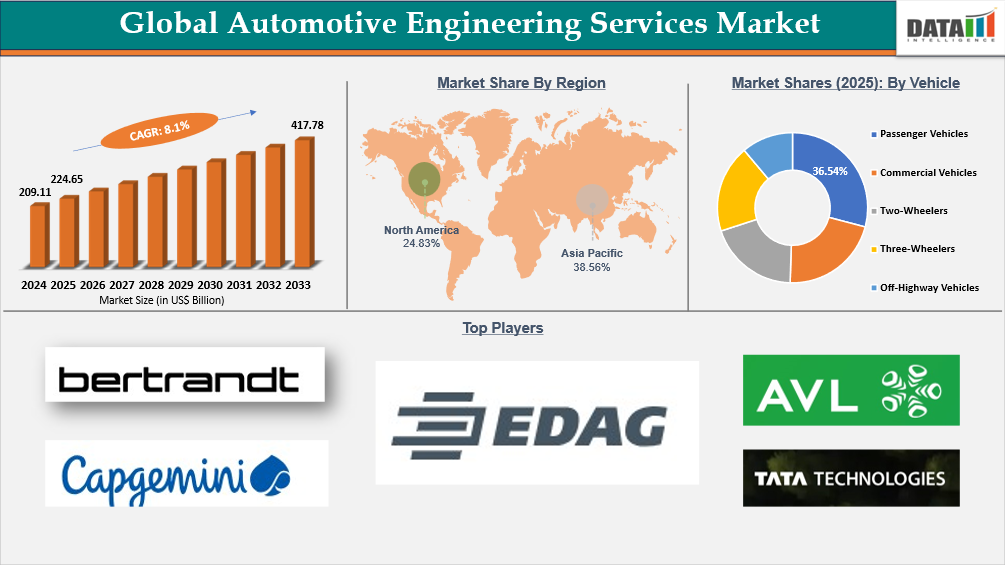

According to DMI analysis, The global automotive engineering services market size was valued at US$ 224.65 billion in 2025 and is projected to reach US$ 417.78 billion by 2033, expanding at a CAGR of 8.1% during the forecast period (2026–2033).

The rising adoption of EVs and connect vehicles is generating demand for technically advanced engineering services, including digital, autonomous, cloud, and cybersecurity. Vehicle manufacturers are becoming increasingly complex, and to mitigate this, they are seeking various specialized engineering service providers to develop and deliver these complex products.

Lately, in January 2026, L&T Technology Services (LTTS) announced to provide a strategic and long-term R&D contract with a renowned global automotive OEM, clearly indicating that service providers are involved in the development of the next generation of mobility solutions. The new deal also represents the involvement of such firms in the development of faster and cost-effective solutions for the OEMs. The EV revolution, with connected and autonomous vehicles promising a bright future for the automotive engineering services market in the years to come.

Automotive Engineering Services Industry Trends and Strategic Insights

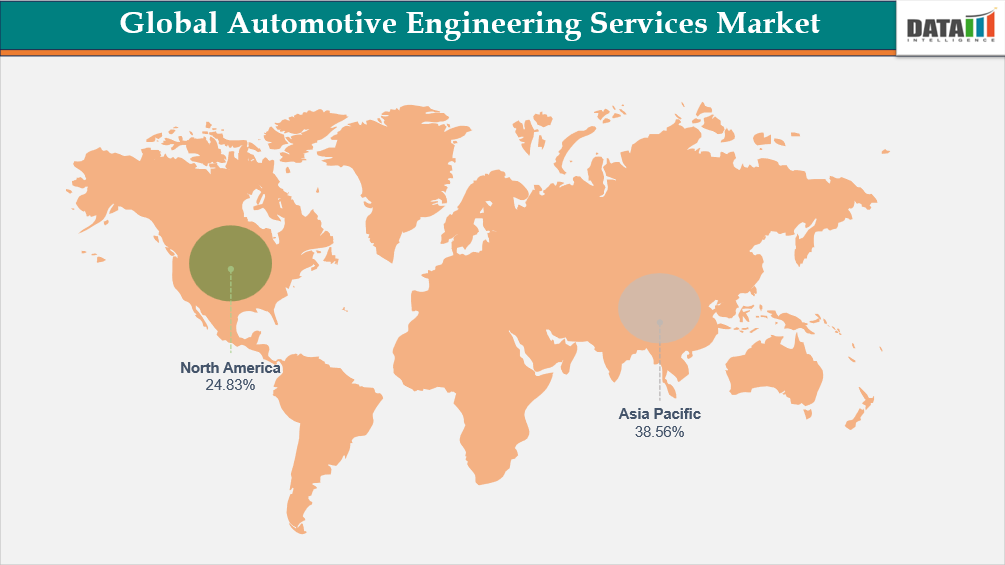

- Asia-Pacific led the global automotive engineering services market with 38.56% in 2025, driven by high vehicle production, growing EV adoption, and a strong presence of engineering service hubs.

- By vehicle type, passenger vehicles dominated the automotive engineering services market with 36.54%, driven by high production volumes, advanced technology integration, and rising demand for electrification and connected vehicle systems.

Global Automotive Engineering Services Market Size and Future Outlook

- 2025 Market Size: US$ 224.65 Billion

- 2033 Projected Market Size: US$ 417.78 Billion

- CAGR (2026–2033): 8.1%

- Dominating Market: Asia-Pacific

- Fastest Growing Market: North Americaey

Key Takeaways

- Asia-Pacific remains the leading regional market, supported by strong vehicle production, expanding EV adoption, and the presence of major automotive engineering hubs across China, India, Japan, and South Korea.

- North America is projected to witness the fastest growth, driven by increasing investments in software-defined vehicles, autonomous driving technologies, and advanced mobility platforms.

- Electrification and connected mobility trends are accelerating demand for specialized engineering services covering battery systems, charging technologies, software integration, and cybersecurity.

- ADAS, autonomous driving, and simulation-based validation are emerging as key investment areas as OEMs focus on enhancing vehicle safety and reducing development cycles.

- Outsourcing of engineering activities is gaining momentum as manufacturers seek cost optimization, faster product development, and access to specialized expertise.

- Digital engineering, virtual testing, and software-defined vehicle architectures are becoming critical purchasing factors, with OEMs increasingly prioritizing partners offering integrated capabilities across electronics, connectivity, and vehicle lifecycle engineering.

Market Scope

| Metrics | Details | |

| By Service | Product Engineering & Vehicle Architecture, Mechanical Engineering, Powertrain & Thermal Systems Engineering, Battery & Charging Engineering, Electrical/Electronics (E/E) & Software Engineering, ADAS / Automated Driving Engineering, CAE / Simulation & Virtual Engineering, Prototyping & Rapid Engineering, Testing, Validation & Certification Support, Manufacturing & Industrial Engineering Support, Program/Project Management & Engineering Consulting | |

| By Vehicle | Passenger Vehicles, Commercial Vehicles, Two-Wheelers, Three-Wheelers, Off-Highway Vehicles | |

| By Propulsion | ICE, Hybrid Electric Vehicle (HEV), Plug-in Hybrid (PHEV), Battery Electric Vehicle (BEV), Fuel Cell Electric Vehicle (FCEV), Alternative fuels | |

| By Service Delivery | In-house Engineering (OEM/Tier Captive), Outsourced Engineering Services | |

| By Application | Powertrain & Propulsion Engineering, Battery & Charging Systems, ADAS & Safety Systems, E/E Architecture & Electronics, Infotainment, Cockpit & Connectivity, Chassis, Body & Structures, Interiors & Ergonomics / HMI, Simulation & Virtual Engineering | |

| By End-User | Original Equipment Manufacturers (OEMs), Tier-1 Suppliers, Tier-2 & Tier-3 Suppliers, EV/AV New Entrants & Startups, Mobility / Autonomous Tech Players, Contract Manufacturers / Vehicle Integrators | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Norway, Netherlands, Sweden, Denmark, Belgium, Switzerland, Austria, Poland, Finland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Egypt, Turkey, Qatar, Kuwait, Oman, Bahrain | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Market Share, Market Growth | |

For More Detailed Information, Request for Sample

Market Dynamics

Boom in EV Design & Battery Engineering Needs

The rising sales of electric vehicles in the global market are favorably affecting the demand for automotive engineering services, which supports the need for specialized automotive engineering services for automotive manufacturers in relation to electric vehicle designs that are efficient in terms of their performance. According to the IEA, there were sales of over 17 million electric cars in the global market in 2024, with the sales share accounting for over 20% compared to previous years. The sales of an additional 3.5 million electric vehicles in 2023 exceeded those sold in the global market in 2020.

With the increase in the growth rate of EVs, there is a bigger need for the development of more sophisticated battery technology. Now, automotive engineering service suppliers have been assisting many car manufacturers in enhancing the battery system in terms of safety, longevity, and efficiency. With the increase in the need for EV production, specialized services like testing, simulation, and validation are becoming important players in the automotive engineering service market, which is witnessing growth directly related to the level of complexity in battery technology.

Segmentation Analysis

The global automotive engineering services market is segmented based on service, vehicle, propulsion, service delivery, application end-user and region.

Passenger Vehicles Fuel Growth in Automotive Engineering Services Due to High Production and Advanced Technology Integration

Passenger vehicles account for a considerable share in the automotive engineering services market in terms of revenue due to the sheer production volume of automotive devices, the level of technology used in these devices, and the strong R&D activities associated with these devices. With the increased complexity in the design of passenger cars with the integration of Electrification, ADAS, connectivity solutions, and software-based automotive devices, the demand for software-based automotive services has increased. With a higher revenue-generation potential compared to commercial vehicles, the passenger vehicle segment is the largest share for automotive engineering services.

Continuing this trend, "Capgemini was positioned as a Leader in Everest Group’s 2025 Software-Defined Vehicle (SDV) Engineering Services PEAK Matrix," announced on January 14, 2026. The accolade acknowledges Capgemini's commitment to SDV platforms and AI-enabled tools and centers of excellence for full-stack development across embedded systems, cloud, and validation.

Geographical Penetration

DOMINATING MARKET:

Asia-Pacific Leads Global Automotive Engineering Services Market with 38.56% Driven by EV Growth

Asia-Pacific market for automotive engineering services remains at the top position with strong growth trajectory for electric vehicle uptake in this region. Government incentives are propelling the automotive market forward, with China being the biggest market in this region, especially driven by strong growth for electric vehicle uptake, thus fueling the market for automotive engineering services, with more investments being made in software and vehicle electrification technologies.

India Automotive Engineering Services Market Outlook

India’s automotive engineering service market is also witnessing the trend of increasing investment in state-of-the-art R&D and validation infrastructure. Tata Elxsi recently inaugurated its new Tata Elxsi + NI Mobility Innovation Centre (TENMIC) facility, situated in Bengaluru, India, in July 2024. The center will serve the automotive industry in some of the key areas of software-defined vehicles, electric vehicles, and advanced testing solutions.

China Automotive Engineering Services Market Trends

China’s automobile engineering services industry is being driven by increased growth in the adoption of EV technology. 2024 is the fourth year of increased sales of electric vehicles. So far, they have recorded over one-third of new purchases of vehicles. Government trade-in programs are also boosting the trend from conventional vehicles to electric vehicles. With this increased adoption of new technology, the industry is witnessing increased engineering services too.

Regulatory Analysis

The dynamics of the global automotive engineering services market can be understood in terms of the complex environment that is put in place to govern areas like emissions, safety, and homologation. The need to certify to standards like Euro 7, Bharat Stage, ISO 26262 functional safety standards, or ISO/SAE 21434 cybersecurity standards is one of the major factors. Variability is one of the cost and time factors for something like EVs, ADAS, or connected car.

The automotive industry is under immense pressure due to stringent regulations concerning environments and safety, which forces OEMs to move towards engineering service providers in these regions like Europe, North America, and Asia Pacific. The regulations like UNECE Regulations, FMVSS, homologation tests, etc., have emphasized tests and approval procedures for meeting certain requirements. With EV and Autonomous advancements, regulation is also moving forward to highlight the need for these engineering services and regulatory compliances.

Competitive Landscape

- The global automotive engineering services market operates under high competitive pressures because of the high rate of technological evolution as well as the robust demand for electric vehicles.

- Market share is held by a few players such as Bertrandt AG, Capgemini SE, L&T Technology Services Limited, IAV GmbH, Tech Mahindra Limited, Harman International Industries, Inc., Continental AG, etc.

- Competition emerges for players based on their innovativeness, their engineering skill sets, and their cost advantage to serve the varied needs of the OEMs. There is tremendous pressure to invest in R&D to create basic skills sets in software development, ADAS, connectivity solutions, simulation tools, etc. Differentiation of service through integrated digital platforms and advanced data analytics is emerging as a key aspect of competition.

Recent Developments

- May 2026: Capgemini expanded its automotive engineering capabilities through AI-driven software-defined vehicle (SDV) development services, supporting connected mobility and autonomous driving programs.

- April 2026: AKKA Technologies strengthened electric vehicle engineering and battery management system capabilities, accelerating OEM electrification and vehicle platform modernization initiatives.

- March 2026: Tata Technologies enhanced digital engineering solutions for software-defined vehicles, supporting vehicle connectivity, embedded systems and intelligent mobility transformation projects.

- February 2026: Infosys expanded automotive engineering service offerings focused on autonomous driving technologies, cloud-based vehicle architectures and next-generation mobility platforms.

- December 2025: HCLTech advanced model-based engineering and digital twin capabilities supporting electric vehicle development, predictive maintenance and lifecycle optimization programs.

- November 2025: Alten Group increased investments in ADAS validation and embedded software engineering services, enhancing vehicle safety and intelligent transportation capabilities.

- October 2025: KPIT Technologies expanded partnerships with global automakers to accelerate software-defined vehicle development, battery engineering and autonomous mobility innovations.

- September 2025: LTTS strengthened electric powertrain and connected vehicle engineering solutions, supporting next-generation mobility and smart transportation ecosystems.

- August 2025: Bertrandt AG enhanced simulation and testing capabilities for autonomous and electric vehicles, improving vehicle performance, safety and regulatory compliance.

- July 2025: EDAG Group expanded end-to-end automotive engineering services covering lightweight vehicle design, e-mobility solutions and digital manufacturing technologies for global OEMs.

Why Choose DataM

- Latest Data & Forecasts – Comprehensive, up-to-date insights and projections through 2033. Coverage includes global value by service, vehicle, propulsion, service delivery, application end-user and region. Scenario forecasts with region-level splits (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa) and sensitivity to factors such as regulatory reclassification and raw-material costs.

- Regulatory Intelligence – Actionable analysis of regulatory frameworks that materially affect Automotive Engineering Services commercialization, revenue by country, allowable label claims, permitted doses, import/export controls and advertising restrictions.

- Competitive Benchmarking – Standardized profiling and benchmarking of leading pharma and nutraceutical players, contract manufacturers and e-commerce specialists active in the market.

- Geographic & Emerging Market Coverage – Region-by-region market sizing, growth drivers, reimbursement dynamics, cultural/consumer behavior and market access considerations. Focus on high-growth or regulatory-uncertain markets.

- Actionable Strategies – Identify opportunities for launching innovative products, while leveraging strategic partnerships and supply chain integration for maximum ROI.

- Pricing & Cost Analysis – In-depth assessment of price trends, raw material costs and sustainability-driven cost efficiencies across regional markets.

- Expert Analysis – Insights from industry experts such as product specialists, regulatory affairs professionals and key manufacturing companies.

Why Purchase the Report?

- To visualize the global automotive engineering services market segmentation based on service, vehicle, propulsion, service delivery, application, end-user and region, as well as understand key commercial assets and major industry participants.

- Identify growth opportunities by analyzing emerging trends, partnerships, and technology developments across the automotive ecosystem.

- Excel data sheet with numerous market-level data points covering all segments of the automotive engineering services market.

- PDF report consists of comprehensive analysis supported by exhaustive qualitative interviews and in-depth industry research.

- Product and service mapping available in Excel format covering key offerings of leading market players.

- The global automotive engineering services market report provides approximately 78 tables, 78 figures and 181 pages of detailed market intelligence.

Target Audience

- Automotive OEMs (Original Equipment Manufacturers)– Global and regional vehicle manufacturers developing passenger cars, commercial vehicles, EVs, and next-generation mobility solutions, requiring engineering support across design, development, testing, and validation.

- Tier 1 & Tier 2 Automotive Suppliers– Component and system suppliers specializing in powertrain, chassis, electronics, interiors, ADAS, and battery systems, seeking engineering services for product development, optimization, and compliance.

- Electric Vehicle (EV) & New Mobility Players– EV startups, battery manufacturers, charging infrastructure providers, and mobility-as-a-service companies building electric, autonomous, connected, and shared mobility platforms.

- Autonomous & ADAS Technology Developers– Companies focused on autonomous driving, advanced driver-assistance systems, sensor fusion, AI software, and vehicle perception technologies requiring simulation, validation, and system integration services.

- Investors & Financial Institutions – Venture capital firms, private equity funds, strategic investors, and banks investing in automotive innovation, EV ecosystems, autonomous technologies, and smart mobility solutions.

- Testing, Validation & Certification Providers – Organizations involved in vehicle testing, crash analysis, NVH testing, durability validation, emissions testing, and functional safety certification.

- Engineering & R&D Centers– Automotive R&D hubs, innovation labs, and technology centers conducting advanced research in vehicle dynamics, lightweight materials, electrification, connectivity, and software-defined vehicles.

Related Reports :

- Automotive Electronics Market

- Automotive Artificial Intelligence Market

- Advanced Driver Assistance Systems (ADAS) Market

- Vehicle Electrification Market

- Autonomous Vehicle Market