Automotive Cable and Wire Market Definition & Overview

What is the automotive cable and wire market?

The Automotive Cable and Wire Market covers low-voltage wires, high-voltage battery cables, data cables, coaxial cables, charging cables, terminals, shielding materials, insulation compounds, connectors, cable assemblies, and wiring harness systems used to transmit power, signal, data inside passenger vehicles, commercial vehicles, electric vehicles, and off-highway mobility platforms. The market includes copper, aluminum, fiber optic, shielded, unshielded, single-core, multi-core, and application-specific cable solutions. Demand is tied to vehicle production, electrification, ADAS adoption, infotainment content, battery voltage architecture, thermal safety, electromagnetic compatibility, and OEM platform redesign cycles.

Automotive Cable and Wire Market Industry Background & Evolution

Parent market background: The parent automotive electrical architecture market has evolved from simple point-to-point wiring for lighting, ignition, comfort features into a dense power and data network that supports electrified propulsion, safety electronics, software defined vehicle functions, connected cockpit systems. Before 2015, vehicle wiring growth was mainly driven by comfort electronics and emission control sensors. From 2015 to 2020, ADAS, infotainment, body control modules expanded circuit count. From 2020 to 2025, EV high-voltage platforms, battery packs, zonal architecture shifted cable value toward shielded power cables and high speed data lines. From 2026 to 2035, the market roadmap moves toward lighter aluminum conductors, high-voltage 800V systems, automated harness production, recyclable insulation, modular zone based cable networks.

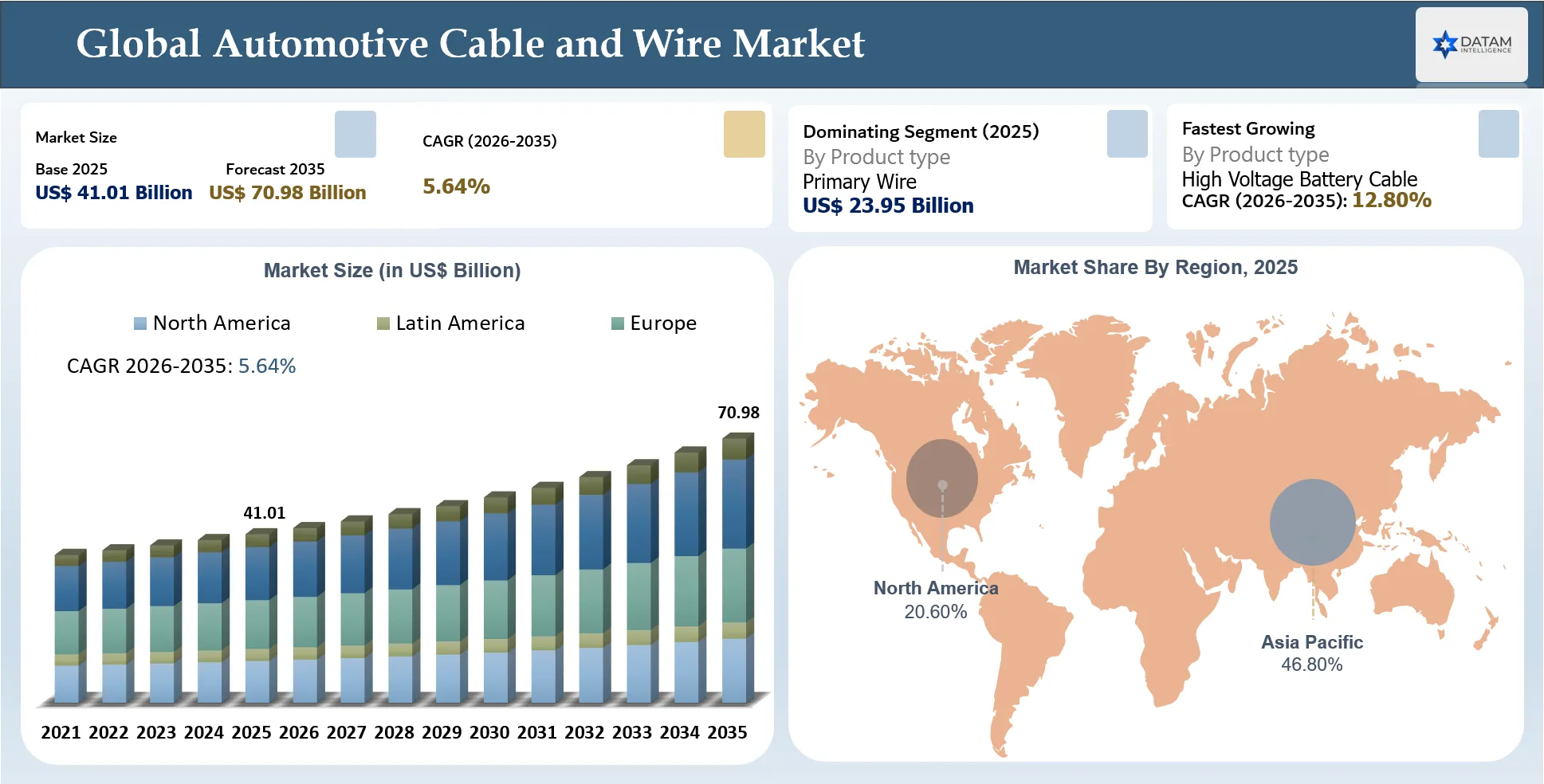

Global Automotive Cable and Wire Market Size & Forecast Analysis

The global automotive cable and wire market is entering a higher-value growth cycle as electrification increases cable content per vehicle while software-defined vehicle platforms expand demand for high-speed data transmission. The forecast reflects a blend of mature low-voltage replacement demand and faster expansion in EV high-voltage cable, shielded signal cable, and advanced harness assemblies.

Historical Automotive Cable and Wire Market Trend Analysis

Over the last 5 years, the Automotive Cable and Wire Market shifted from production volume recovery toward content growth per vehicle. The 2020 to 2021 period exposed harness supply fragility because cable assemblies rely on labor intensive production and regional supplier clusters. From 2022 onward, OEMs redesigned electrical architectures to support EV battery systems, ADAS sensors, connected infotainment, software update capability.

Cable demand moved toward high-voltage, shielded, flame retardant, lighter materials rather than commodity primary wire alone. Copper price volatility also pushed suppliers to qualify aluminum and optimized conductor geometries. The impact has been a market where value growth increasingly depends on voltage class, insulation performance, EMC reliability, automation readiness, regional localization rather than simple vehicle unit growth.

Automotive Cable and Wire Market Snapshot

| Metric | Value |

| Market Name | Automotive Cable and Wire Market |

| 2025 Market Size | USD $41.01 Billion |

| 2035 Projected Market Size | USD $70.98 Billion |

| CAGR 2026 to 2035 | 5.64% |

| Largest Segment Name and Share | Primary Wire - 58.40% |

| Fastest Growing Segment Name and Growth Rate | high-voltage Battery Cable - 12.80% |

| Largest Region Name and Share | Asia Pacific - 46.80% |

| Fastest Growing Region Name and Growth Rate | Asia Pacific - 6.40% |

| Geographic Market Share for the 5 Regions | Asia Pacific: 46.80%, Europe: 24.70%, North America: 20.60%, Latin America: 4.60%, Middle East and Africa: 3.30% |

| Top Companies | The market is concentrated among large Tier 1 electrical architecture suppliers and cable specialists that support OEMs across low-voltage, high-voltage, data, connector, harness programs. • Yazaki Corporation • Sumitomo Electric Industries • Aptiv PLC • Lear Corporation • Leoni AG • Furukawa Electric • Fujikura Ltd. • TE Connectivity • Nexans Autoelectric • Samvardhana Motherson International |

Automotive Cable and Wire Market Growth Outlook Summary

Short term growth is supported by vehicle production normalization, EV model launches, higher electronic content in mass market vehicles. Mid term growth will be shaped by 400V to 800V platform migration, ADAS sensor proliferation, regional wiring harness localization, the need for lighter materials to offset battery weight. Long term growth through 2035 will come from zonal architectures, integrated charging systems, autonomous driving data networks, circular material rules.

The market outlook remains structurally positive because every transition in mobility adds new cable value even when total vehicle production grows slowly. The most attractive areas are high-voltage cable assemblies, shielded data lines, battery pack wiring, charging inlet cables, recyclable insulation systems. Suppliers that combine material science, automation, local assembly, OEM co-development will capture stronger margins. Commodity wire producers face pricing pressure, while system level cable and harness suppliers gain strategic importance in platform design.

Automotive Cable and Wire Market Key Takeaways

- high-voltage EV cables are becoming the most important value growth pool as battery voltage rises and fast charging demand expands

- Asia Pacific is the largest region because China, Japan, South Korea, India combine vehicle production scale with deep component supply ecosystems

- The largest segment is low-voltage primary wire because every vehicle still uses extensive body, lighting, cabin, control wiring

- The fastest growing segment is high-voltage battery cable because EV platforms require specialized insulation, shielding, thermal safety

- The fastest growing region is Asia Pacific as EV production, battery localization, electronics integration expand quickly

- OEMs are reducing harness complexity through zonal architecture, but higher data and power content keeps cable value expanding

- Aluminum conductors, recyclable polymers, automated assembly are moving from optional cost levers to strategic sourcing requirements

Automotive Cable and Wire Market White Space & Investment Opportunities

Investment white spaces are opening where suppliers can combine high-voltage validation, lighter conductors, automation, and recyclable insulation to address OEM sourcing gaps.

- Regional automated harness plants close to EV assembly hubs remain under supplied and will attract investment in North America, India, Southeast Asia.

- Recyclable cable insulation and conductor recovery technologies are underdeveloped but increasingly important under circular vehicle rules.

- Integrated battery pack cable modules create white space for suppliers that can combine sensing, power transfer, thermal routing, safety interlocks.

Automotive Cable and Wire Market Procurement & Buyer Behavior Analysis

Procurement decisions are becoming more strategic because cable failures can affect vehicle safety, launch timing, warranty costs, regulatory compliance. Buyers increasingly evaluate suppliers on engineering support, validation depth, regional capacity, automation, cost transparency rather than price alone.

Automotive Cable and Wire Market Buyer Decision Making Criteria

- Automotive OEMs and Tier 1 buyers prioritize suppliers that can deliver validated electrical performance, consistent quality, local launch support. The procurement process weighs lifetime cost, safety risk, platform timing because wiring changes late in development are expensive

- high-voltage safety compliance and insulation reliability

- EMC shielding and signal integrity for data cables

- Regional capacity near vehicle assembly plants

- Copper and aluminum cost management capability

- Automated quality control and traceability

- OEM approved validation testing

- Lightweight material options

- Recyclable insulation and sustainability documentation

Automotive Cable and Wire Market Economic & Investment Analysis

Economic factors affecting the market include vehicle production cycles, copper pricing, EV capital spending, labor costs, automation investment, interest rates, regional trade policy. The market benefits when OEMs launch new platforms because wiring content is locked into multi year vehicle programs. Higher interest rates can slow vehicle demand, but EV incentives and electronics content still support cable value growth.

Copper and polymer costs are major margin variables, especially for suppliers locked into long-term contracts. Labor cost inflation is encouraging automation in harness production. Investment is flowing toward high-voltage cables, battery pack wiring, data cables, and regional assembly plants because these areas align with EV growth and supply chain resilience. Trade policy can shift production footprints, particularly between Mexico, Southeast Asia, India, and Eastern Europe.

Automotive Cable and Wire Market Macroeconomic Impact Factors

Macroeconomic conditions affect the automotive cable and wire market through vehicle production, raw material costs, capital spending, and consumer affordability. When interest rates remain high, vehicle purchases can slow, which reduces short-term OEM cable orders. However, the impact is partly offset by rising cable content per vehicle because EVs, ADAS, infotainment, and safety systems increase wiring value.

Copper and aluminum price movements have direct margin impact because conductor material is a large cost component. Wage inflation affects harness assembly because production remains labor-intensive in many countries. Currency shifts also matter because global suppliers source materials and ship components across regions. From 2026 to 2035, the strongest macro support will come from EV investment, battery plant localization, infrastructure spending.

The biggest risk is a prolonged downturn in vehicle production combined with high raw material prices.

Automotive Cable and Wire Market Investment Trends

- Investment is shifting from commodity wire capacity toward EV cable systems, automation, and regional supply resilience. Suppliers are prioritizing technologies that reduce labor dependence and improve platform level value

- Automated harness assembly and machine vision inspection

- high-voltage and 800V cable production capacity

- Recyclable insulation and low carbon conductor sourcing

Automotive Cable and Wire Market Funding & M&A Activity

- M&A focus is expected to center on wiring harness capacity, automation technology, high-voltage cable expertise, regional manufacturing footprints. Large Tier suppliers are likely to acquire specialized automation firms or regional harness businesses to secure EV platform readiness

- February 2025: Lear acquired StoneShield Engineering to strengthen automation capabilities within its E Systems business

- December 2025: Motherson agreed to acquire the Nexans Autoelectric wiring harness business for a reported EUR 207 million, expanding global capacity

- 2025 to 2026: Strategic funding is expected for EV cable automation, recyclable insulation, regional harness plants, with corporate investment more common than Series A or Series B funding

Automotive Cable and Wire Market Regulatory & Policy Analysis

- The regulatory framework is shaped by electric powertrain safety, vehicle type approval, flame resistance, electromagnetic compatibility, end of life vehicle rules, OEM material standards. high-voltage cables must meet safety requirements for isolation, orange identification, protection from electric shock, durability. UNECE R100 influences EV high-voltage systems and components, while regional vehicle safety standards define installation and validation expectations. Environmental rules are also becoming more important as Europe advances vehicle circularity and recycled content requirements. 2025/2026 regulatory changes impacting the industry include:

- December 2025: EU provisional agreement on end of life vehicle regulation, increasing pressure for recyclable cable materials

- 2025: Continued updates and application of EV high-voltage safety expectations under UNECE and regional frameworks

- 2026 onward: OEM sustainability requirements are expected to tighten supplier reporting for recycled content and material traceability

Automotive Cable and Wire Market Regulatory Framework Overview

The Automotive Cable and Wire Market is regulated through vehicle safety, electric powertrain protection, EMC, material safety, environmental rules. high-voltage EV cables are indirectly governed by electric powertrain standards such as UNECE R100, which addresses safety requirements for vehicles with high-voltage components. Cable materials must also satisfy flame resistance, insulation durability, OEM restricted substance requirements. In Europe, circular vehicle policy is pushing the market toward recyclable materials and greater end of life traceability. These regulations raise validation burden but also increase demand for higher quality cable systems and capable documentation suppliers.

Automotive Cable and Wire Market Trends & Innovation Landscape

Innovation is moving toward lighter conductors, higher voltage ratings, better shielding, automated assembly, greener materials. Cable suppliers are increasingly judged by platform engineering capability rather than material supply alone.

Automotive Cable and Wire Key Market Trends

- The key trend landscape is shaped by EV power requirements and software defined vehicle electronics. Suppliers are investing in higher voltage cable systems, data transmission capability, localized harness production, material circularity because OEMs need lighter, safer, more reliable wiring networks

- 800V EV platforms are moving high-voltage cables into premium value categories with stronger insulation and shielding requirements

- Zonal architecture is reducing wiring distance while increasing demand for modular cable assemblies and gateway connectors

Automotive Cable and Wire Market Technology Advancements

- Technology advancement is focused on reducing weight while improving power and data reliability. Cable design is moving toward aluminum conductors, miniaturized terminals, smart harness testing, automated assembly. These changes improve scalability and reduce warranty risk in EV and connected vehicle programs

- February 2025: Lear acquired StoneShield Engineering to strengthen automation capability for wire harness production

- 2025: high-voltage cable suppliers advanced shielded 800V ready products for fast charging and battery electric vehicle platforms

Automotive Cable and Wire Industry Transformation Trends

The market is transforming from component supply toward architecture participation. OEMs are involving cable suppliers earlier in EV platform design because harness routing, EMC, safety, assembly efficiency directly affect vehicle cost and launch risk. This gives system suppliers stronger bargaining power while commodity wire makers face margin pressure.

Automotive Cable and Wire Market Disruption Analysis

The primary disruption is the move from distributed wiring to zonal and centralized vehicle architecture. This reduces total wiring length in some platforms but raises value per cable through better shielding, connectors, data capability. A second disruption is automated harness assembly, which changes the cost model of a historically labor intensive market.

Automotive Cable and Wire Market Disruption & Structural Shift Analysis

The market is undergoing structural disruption as EVs and software defined vehicles change wiring value from basic power delivery to integrated electrical architecture. Automation, material substitution, circularity rules will alter supplier economics.

Automotive Cable and Wire Market Technology Disruption Impact

- Technology disruption is visible in automated harness manufacturing and zonal architecture. These changes reduce manual assembly dependence while forcing suppliers to become design partners with digital capability

- Zonal architecture disrupts conventional harness layouts by reducing long cable runs and increasing modular power or data nodes

- Automated crimping, routing, inspection disrupt labor intensive production by improving consistency and reducing launch risk

Automotive Cable and Wire Future Market Transformation

By 2035, the Automotive Cable and Wire Market will look less like a commodity material market and more like an electrical architecture ecosystem. Vehicle platforms will use zonal controllers, high-voltage battery systems, fast charging interfaces, high speed data backbones, connected safety functions. Suppliers will generate value through design integration, validation, automation, traceability, sustainability documentation. Business models will shift from selling meters of wire toward supplying validated cable modules, harness zones, lifecycle supported electrical systems. Circular material requirements will also create new services around conductor recovery, recycled polymer qualification, end of life traceability.

Automotive Cable and Wire Policy Impact on Market Growth

- Government policy is accelerating electrification, local sourcing, circularity. These policy shifts increase cable value per vehicle and reshape regional manufacturing decisions

- EV incentive and charging policies increase high-voltage cable demand by supporting battery electric vehicle adoption

- Local manufacturing policies encourage regional harness plants and reduce dependence on long distance supply chains

- Circular economy policies increase demand for recyclable insulation, copper recovery, supplier material traceability

Automotive Cable and Wire Market Growth Dynamics

The market is driven by electrification, vehicle electronics growth, wiring architecture redesign. It is constrained by copper price volatility, labor intensive harness assembly, and qualification complexity for safety critical EV cables.

Automotive Cable and Wire Market Drivers

- EV platform expansion increases high-voltage cable demand because battery packs, inverters, onboard chargers, DC fast charging, e axle systems require shielded power transmission.

- ADAS and connected cockpit growth raises demand for data cable, coaxial cable, sensor wire, EMC protected assemblies across premium and mass market vehicles.

- Vehicle safety and comfort electronics increase circuit density across seats, doors, lighting, HVAC, telematics, power distribution modules.

Automotive Cable and Wire Market Driver Impact Assessment

| Driver | Market Growth Impact (%) | Demand Concentration | Impacted Use Case | Strategic Impact |

EV and Hybrid Platform Expansion | 6.20% | China, Europe, North America, and South Korea EV production hubs | Battery pack wiring, charging cable assemblies, inverter connections, e-axle power transfer cables | Shifts market value from commodity primary wires toward certified high-voltage cable systems with enhanced thermal and safety performance. |

ADAS and Connected Vehicle Electronics | 5.10% | Premium vehicles, software-defined vehicle platforms, and autonomous mobility fleets | Sensor wiring, coaxial cables, automotive Ethernet cables, shielded high-speed data lines | Drives demand for cables with superior electromagnetic compatibility (EMC), signal integrity, and high-speed data transmission capabilities. |

Light weighting and Vehicle Efficiency Requirements | 3.80% | EV platforms and regions with stringent fuel economy and emission regulations | Aluminum conductors, optimized cable architectures, thin-wall insulation, lightweight wiring harnesses | Creates opportunities for material substitution, weight reduction, and improved vehicle energy efficiency while maintaining electrical performance. |

Automotive Cable and Wire Market Restraints

- Copper price volatility pressures cable margins because automotive wires depend heavily on copper conductors and long term contracts lag raw material changes.

- Harness manufacturing remains labor intensive, making scale up vulnerable to wage inflation, worker availability, regional disruption.

- high-voltage cable qualification cycles slow supplier entry because safety, thermal, EMC, durability validation can take years.

Automotive Cable and Wire Market Restraint Impact Assessment

| Restraint | Drag on Market Growth (%) | Primary Impact Area | Impacted Use Case | Strategic Impact |

Copper and Polymer Cost Volatility | 4.30% | Conductor procurement, raw material sourcing, and contract margin stability | Primary wires, battery cables, and high-voltage cables | Accelerates aluminum conductor qualification, recycled material adoption, and long-term sourcing strategies to mitigate cost fluctuations. |

Labor-Intensive Wiring Harness Production | 3.90% | Assembly capacity, labor availability, and localization costs | Wiring harnesses and customized cable assemblies | Encourages automation investments, digital manufacturing, and supplier footprint optimization to improve productivity and reduce dependence on manual labor. |

Long Validation Cycles for EV Cables | 3.40% | Safety testing, certification, and OEM approval processes | High-voltage power cables, charging cables, and EV cable systems | Strengthens the position of established suppliers with proven certifications while slowing market entry for new manufacturers and innovative products. |

Emerging Automotive Cable and Wire Growth Factors

Circular mobility, lightweighting targets, EV platform complexity, and material substitution are creating new growth factors that expand cable value beyond traditional vehicle production volume assumptions.

- Software defined vehicles require more high speed data pathways, creating demand for automotive Ethernet, coaxial, shielded cable systems.

- Battery safety monitoring increases sensor wire density inside packs and thermal management systems.

- Automated harness assembly improves scalability as suppliers adopt robotics, digital work instructions, machine vision quality checks.

Automotive Cable and Wire Market Segmentation Analysis

Segmentation shows a market split between high volume low-voltage wiring and fast growing high-voltage or data cable categories. The largest revenue pool remains primary wire and harness applications, while the strongest growth comes from EV battery cables, charging cables, high speed data lines.

Automotive Cable and Wire Market by Primary Wire Trends

The major segment is primary wire because all vehicle platforms require extensive low-voltage circuits for lighting, body controls, infotainment, HVAC, seats, doors, safety systems. The most important trend is material optimization as OEMs try to reduce vehicle weight and manage copper cost. Primary wire demand will remain resilient because electronics content grows even when vehicle production is cyclical. However, growth will be slower than EV specific cables because low-voltage systems are mature. The market is headed toward thinner wall insulation, optimized conductor sizing, improved recyclability, with suppliers competing on durability, cost stability, compliance with OEM electrical architecture standards.

Automotive Cable and Wire Market by Product Type Trends

Automotive Cable and Wire Market by Product Type Trends. The product type landscape is shifting from commodity wire toward engineered cable assemblies. Primary wire remains the largest segment due to broad usage in body, lighting, control functions. high-voltage cable is the fastest growing product group because battery electric vehicles require insulated, shielded, thermally stable power connections. Data cable is also gaining value as software defined vehicles need reliable bandwidth for cameras, sensors, infotainment. Through 2035, suppliers will differentiate through lighter materials, validated safety performance, automated assembly readiness, the ability to integrate cables with connectors and modules.

Automotive Cable and Wire Market by Vehicle Type Trends

Automotive Cable and Wire Market by Vehicle Type Trends. Passenger cars remain the largest demand base because global production volumes are high and electronic content continues to expand in mass market models. Electric vehicles represent the fastest growth because they add high-voltage power cables, charging cables, battery monitoring wires, shielded data lines. Commercial vehicles create specialized demand for rugged cables that withstand vibration, moisture, longer operating cycles. The market is headed toward platform specific cable kits where EV and hybrid architectures receive higher value cable content while internal combustion platforms continue supporting replacement and incremental electronics demand.

Automotive Cable and Wire Market by Application Trends

Automotive Cable and Wire Market by Application Trends. Body and lighting applications remain high volume because every vehicle requires distributed low-voltage wiring across doors, seats, cabin electronics, lighting, HVAC systems. Battery pack and charging applications are growing fastest as EV production scales and charging speeds increase. ADAS and infotainment applications are also raising data cable demand because cameras, radar, displays, telematics require low latency transmission. The market is headed toward mixed power and data architectures where suppliers must provide validated cable routing, electromagnetic protection, assembly integration rather than independent wire categories.

Automotive Cable and Wire Market Regional Market Analysis

Regional dynamics are led by Asia Pacific due to vehicle production scale and EV supply chain depth. Europe is shaped by premium EV platforms and circularity regulation, while North America is driven by local EV assembly, Mexico based wiring capacity, investment in regional supply resilience.

North America Automotive Cable and Wire Market

North America is moving from import dependent cable supply toward more localized EV cable and harness production. The United States, Mexico, Canada benefit from vehicle assembly concentration, EV battery plants, nearshore wiring harness capacity. Demand is shifting from conventional primary wire toward battery cable, charging cable, ADAS sensor wiring, software defined vehicle data lines. Mexico remains critical for labor intensive harness assembly because it offers proximity to U.S.

OEM plants and deep component manufacturing capability. The region also faces tariff, wage, copper cost pressure, which encourages automation and supplier footprint diversification. From 2026 to 2035, North America growth is expected to come from EV platform launches, charging infrastructure related vehicle content, commercial fleet electrification, higher electronic content in pickups and SUVs.

Suppliers with local testing, engineering support, rapid launch capability will gain advantage because OEMs are reducing supply chain risk after recent disruptions.

Europe Automotive Cable and Wire Market

Europe is a high value Automotive Cable and Wire Market because premium vehicles, EV penetration, strict safety rules create demand for advanced high-voltage and data cable solutions. Germany, France, Italy, Spain, Eastern Europe form a dense ecosystem of OEM assembly, Tier 1 harness production, cable material supply. Demand is influenced by battery electric platforms, 800V charging architectures, advanced driver assistance, lifecycle sustainability rules.

The proposed end of life vehicle framework is pushing OEMs to evaluate recyclable insulation, material traceability, component recoverability. Production capacity is increasingly balanced between Western European engineering centers and lower cost Eastern European assembly sites. Through 2035, Europe will remain a technology led market where suppliers compete on compliance, lightweighting, EMC performance, circular material readiness.

Asia Pacific Automotive Cable and Wire Market

Asia Pacific is the largest and fastest growing region because it combines the world’s largest vehicle production base with strong EV adoption and deep electronics supply chains. China leads demand through battery electric vehicle scale, 800V platform deployment, local cable supplier expansion. Japan and South Korea contribute advanced materials, connectors, high reliability cable systems for global OEM programs.

India and Southeast Asia are becoming important manufacturing bases for low-voltage wiring and export oriented harnesses. Demand is shifting from simple primary wire to battery cable, data cable, charging cable assemblies. Through 2035, the region will benefit from EV localization, lower cost assembly capacity, OEM pressure for regional sourcing. Competitive intensity will rise as Chinese cable and harness suppliers expand beyond domestic platforms.

Automotive Cable and Wire Country-Level Market Analysis

Country level performance is shaped by vehicle production scale, EV penetration, local supplier depth, OEM electrical architecture choices. China is the most important growth market, while the United States, Japan, India, Germany, South Korea, Mexico, France, Brazil are key demand centers.

United States Automotive Cable and Wire Market Size/Forecast

The United States market is driven by EV platform launches, commercial fleet electrification, ADAS adoption, high electronic content in trucks and SUVs. Demand is moving toward high-voltage battery cables, charging lines, data cables, advanced harness assemblies. U.S. OEMs are localizing supply because wiring systems are launch critical and difficult to reroute after design freeze. The market also benefits from battery plant investment and software defined vehicle programs. From 2026 to 2035, growth will be supported by domestic EV manufacturing, connected vehicle architectures, replacement demand for higher content vehicles. Suppliers with U.S. engineering and Mexico assembly footprints will be best positioned.

Japan Automotive Cable and Wire Market Size/Forecast

Japan remains a high quality engineering market for automotive cable and wire because local OEMs emphasize reliability, compact packaging, long product life. Demand is supported by hybrid vehicles, battery electric platforms, safety electronics, export oriented vehicle programs. Japanese suppliers are strong in wire harnesses, connectors, high reliability materials. Market growth is moderate because domestic vehicle production is mature, but value per vehicle is rising due to electrification and ADAS. From 2026 to 2035, Japan will influence global cable standards through advanced hybrid systems, compact EV platforms, supplier technology exported to Asia, North America, Europe.

China Automotive Cable and Wire Market Size/Forecast

China is the largest growth engine because it has massive EV production, fast model refresh cycles, aggressive adoption of 800V charging platforms. Local OEMs demand high-voltage cables, battery pack wiring, charging cables, data lines, integrated harness modules at scale. Domestic cable suppliers are improving quality and expanding into global programs, increasing competition for established multinational players. Production capacity is expanding around EV clusters in coastal and inland provinces. From 2026 to 2035, China will shape pricing, innovation speed, material substitution trends. The country specific market size and share outlook remains strong because EV penetration and local supplier depth are unmatched.

India Automotive Cable and Wire Market Size/Forecast

India is emerging as an important Automotive Cable and Wire Market due to rising passenger vehicle production, two wheeler electrification, commercial vehicle modernization, local component manufacturing. The market remains weighted toward low-voltage primary wire and harness assemblies, but EV buses, electric two wheelers, compact passenger EVs are expanding demand for battery cables and charging lines. OEM localization policies encourage domestic cable production and Tier supplier investment. From 2026 to 2035, India’s growth will be supported by vehicle exports, electronics content growth, supplier capacity expansion. Cost competitiveness will be critical, but quality and high-voltage validation capability will define premium opportunities.

Automotive Cable and Wire Market Other Key Countries

Germany Automotive Cable and Wire Market: Germany is central to premium EV platforms, 800V systems, ADAS electronics, high reliability wiring. Suppliers focus on engineering intensive cable systems and circular material compliance. South Korea Automotive Cable and Wire Market: South Korea benefits from battery, EV, electronics ecosystems, creating strong demand for high-voltage and data cables. Mexico Automotive Cable and Wire Market: Mexico is a strategic harness assembly hub for North America and benefits from nearshoring demand. France Automotive Cable and Wire Market: France supports EV and hybrid programs with demand for lightweight cable systems and compliance focused sourcing. Brazil Automotive Cable and Wire Market: Brazil remains important for regional vehicle production, aftermarket wiring, gradual electrification of fleets.

Automotive Cable and Wire Market Competitive Landscape

The competitive landscape is led by global harness and cable system suppliers with OEM platform relationships, regional assembly footprints, growing EV cable portfolios. Major companies include:

- Yazaki Corporation

- Sumitomo Electric Industries

- Aptiv PLC

- Lear Corporation

- Leoni AG

- Furukawa Electric

- Fujikura Ltd

- TE Connectivity

- Nexans Autoelectric

- Samvardhana Motherson International

Automotive Cable and Wire Market Competitive Benchmarking

Benchmarking shows that leaders compete on OEM integration depth, EV cable portfolios, high speed data capability, automation, regional manufacturing. The strongest players combine electrical architecture design with manufacturing scale, which allows them to support platform launches and engineering changes. Yazaki leads in global harness scale and OEM relationships, with strong conventional and electrified vehicle coverage. Sumitomo Electric is strong in high reliability wiring, connectors, Japanese OEM programs. Aptiv focuses on electrical distribution systems, high-voltage solutions, software defined vehicle architecture. Lear is strengthening automation and E Systems capability. TE Connectivity is strongest in connectors, terminals, data or high-voltage interface solutions.

Automotive Cable and Wire Market BCG Matrix List

Stars: Yazaki Corporation, Aptiv PLC. Question Marks: Leoni AG, Nexans Autoelectric. Cash Cows: Sumitomo Electric Industries, TE Connectivity. Niche Players: Furukawa Electric, Fujikura Ltd.

Automotive Cable and Wire Market BCG Matrix Analysis

Stars such as Yazaki and Aptiv have broad OEM relationships, global manufacturing footprints, direct exposure to EV high-voltage and software defined vehicle architectures. They are positioned in high share and high growth areas because they can support complete electrical distribution systems rather than isolated wire products. Cash Cows such as Sumitomo Electric and TE Connectivity have strong installed positions, proven component platforms, durable OEM relationships that generate stable revenue across conventional and electrified vehicles. Question Marks such as Leoni and Nexans Autoelectric have valuable capabilities but face restructuring, ownership transitions, or selective exposure to growth platforms. Niche Players such as Furukawa Electric and Fujikura are relevant in specialized cable, connector, high reliability applications, but their global share in complete automotive wiring systems is narrower than the largest Tier 1 groups.

Automotive Cable and Wire Market Company Profiles & Strategy Analysis

Company strategy is moving toward EV platform support, automation, regional capacity, architecture level collaboration. Suppliers with design engineering, validation, local assembly capacity are gaining stronger positions than commodity wire manufacturers.

Automotive Cable and Wire Market Expansion & Partnership Strategy

Expansion and partnership strategies are focused on automation, acquisitions, localized EV supply chains. Suppliers are using deals to gain technology, regional capacity, access to OEM programs. February 2025: Lear acquired StoneShield Engineering to strengthen automation within its E Systems business, improving harness manufacturing productivity and quality control. December 2025: Motherson agreed to acquire Nexans Autoelectric’s wiring harness business, expanding global wiring capacity and customer coverage. 2025: EV wiring and connector suppliers increased collaboration with OEMs on high-voltage and sustainable EV wiring strategies, supporting platform level sourcing and faster qualification cycles.

Automotive Cable and Wire Market Key Developments (2025,2026)

Market developments in 2025 and 2026 show the industry moving toward automation, consolidation, EV cable capability, circular vehicle compliance.

Automotive Cable and Wire Major Industry Developments

- The following developments highlight consolidation, automation, regulatory pressure that are reshaping the market. They also show how suppliers are preparing for EV and software defined vehicle programs

- February 2025: Lear acquired StoneShield Engineering to strengthen advanced automation in its E Systems business

- December 2025: Motherson agreed to acquire Nexans Autoelectric’s wiring harness business, expanding global harness capacity

- December 2025: EU institutions reached a provisional agreement on vehicle circularity and end of life vehicle rules, influencing cable material strategy

- 2025: EV wiring and connector suppliers accelerated 800V ready product development as fast charging platforms expanded

Automotive Cable and Wire Recent Market Announcements

December 2025: Motherson’s agreement to acquire Nexans Autoelectric’s wiring harness business is a major market announcement because it strengthens Motherson’s global wiring footprint and expands access to passenger and commercial vehicle programs. The deal reflects a broader trend toward consolidation in wiring systems as OEMs seek financially stable suppliers with regional capacity, engineering depth, EV platform readiness. It also signals that wiring harness assets remain strategically valuable despite automation challenges and labor intensity. The acquisition is expected to improve Motherson’s scale, customer diversification, ability to support complex electrified vehicle launches.

Automotive Cable and Wire Market Technology Launches & Partnerships

- Technology launches and partnerships are focused on automation, high-voltage performance, supplier OEM collaboration. These developments reduce production risk and support EV platform scale up

- February 2025: Lear and StoneShield integration strengthens automated harness manufacturing, improving repeatability and labor productivity

- 2025: Suppliers expanded high-voltage cable portfolios for 800V charging and battery electric vehicle architectures

- 2025: Connector and cable companies increased OEM collaboration on data cable solutions for ADAS, infotainment, central compute systems

Automotive Cable and Wire Market Strategic Insights & Analyst Perspective

Analyst perspective indicates the market is shifting from vehicle production linked growth toward content and architecture led growth. Cable value per vehicle is rising because EVs and software defined vehicles require higher voltage, faster data transmission, stronger safety validation, better routing design. This makes the market more resilient than traditional auto component categories.

However, suppliers face margin pressure from copper volatility, labor cost inflation, OEM cost reduction demands. DataM Intelligence perspective would view the strongest opportunities in high-voltage battery cables, 800V ready assemblies, automotive Ethernet, zonal harness modules, recyclable materials. The industry is headed toward deeper OEM supplier collaboration because electrical architecture decisions affect platform cost, range, safety, software capability.

Large suppliers with engineering and manufacturing scale will gain share, while commodity wire players must specialize or risk price pressure. The next decade will favor companies that can combine design simulation, validation, automated production, regional supply assurance. Market growth will be steady at the global level, but profit pools will shift faster toward EV and high speed data cable applications.

Analyst Insights of Automotive Cable and Wire Market

From an analyst perspective, the Automotive Cable and Wire Market is entering a phase where electrical architecture becomes a core vehicle differentiation factor. Historically, wiring was treated as a necessary cost center, but electrification and software defined vehicle development have changed its strategic role. high-voltage cables influence charging speed, vehicle safety, range efficiency, battery pack integration.

Data cables influence ADAS performance, infotainment quality, connected services, autonomous driving readiness. This means cable suppliers are moving closer to OEM platform strategy. The global market size is expected to grow steadily through 2035, but the most important shift is in the quality of revenue. low-voltage wire will remain a large share of the market, while high-voltage and data cable applications grow faster and carry higher engineering value.

DataM Intelligence analyst perspective would emphasize that suppliers must invest in automation, material science, local manufacturing, lifecycle traceability. Companies that cannot manage copper volatility or EV validation requirements will face margin pressure. Companies that can co design architectures, support regional EV launches, document sustainability performance will strengthen their forecast growth position.

Strategic Recommendations of Automotive Cable and Wire Market

Recommendation 1: Automotive cable suppliers should prioritize high-voltage and data cable platforms rather than relying on mature low-voltage wire. The most attractive growth will come from EV battery systems, charging interfaces, inverters, ADAS sensors, zonal controllers. Companies should invest in 800V validation, EMC testing, thermal aging capability, connector partnerships.

This strategy improves pricing power and protects margins because OEMs value safety, reliability, launch support in high-voltage systems. Recommendation 2: Suppliers should build regional automated harness capacity near EV manufacturing hubs. Harnesses are customized, bulky, launch critical, so OEMs prefer suppliers that can support local engineering changes and reduce logistics risk. Automation in cutting, crimping, routing, inspection can reduce labor exposure while improving quality.

This approach is especially relevant in North America, India, Eastern Europe, Southeast Asia, where OEMs are balancing cost, resilience, localization requirements.

Automotive Cable and Wire Future Market Outlook (2035 Vision)

In 2025, the automotive cable and wire market is still anchored by primary wire and conventional harness systems, with high-voltage and data cable categories growing quickly but sharing space with mature internal combustion vehicle applications. By 2035, the market will be shaped by electrified platforms, fast charging, software-defined vehicle architectures, and stricter circularity expectations. Cable systems will be lighter, more modular, more traceable, and more integrated with vehicle electronics.

high-voltage cable assemblies will be standard across a much larger share of production, while data cables will support centralized compute, sensors, and connected features. The business model will change from selling wire by specification toward supplying validated electrical modules and architecture services. Suppliers will need automated production, simulation tools, sustainability documentation, and regional capacity.

The market will be larger in size, more technical in product mix, more consolidated around strategic suppliers.

Automotive Cable and Wire Market Target Audience

- Automotive OEMs: To understand cable content growth, supplier capability, sourcing risk

- Tier 1 Electrical System Suppliers: To benchmark high-voltage, data cable, harness strategy

- Cable and Wire Manufacturers: To identify product growth areas and regional expansion opportunities

- Connector and Terminal Suppliers: To understand demand from EV power and data architectures

- Battery Pack Manufacturers: To assess high-voltage cable, sensing wire, safety interlock requirements

- Investors and Private Equity Firms: To identify consolidation, automation, EV cable investment themes

- Raw Material Suppliers: To track copper, aluminum, insulation, shielding material demand

- Automation Equipment Providers: To evaluate demand for harness production automation

Who Should Buy this Report?

- This report is designed for stakeholders that need a detailed view of market size, forecast growth, regional share, segment performance, supplier strategy. It helps buyers evaluate where cable value is shifting as EVs and software-defined vehicles reshape automotive architecture

- OEM sourcing and engineering teams

- Tier 1 electrical distribution suppliers

- Cable, wire, connector, terminal producers

- Battery system and charging component companies

- Material suppliers for copper, aluminum, polymers

- Automation technology providers

- Investors evaluating automotive component opportunities

- Strategy teams studying country specific market size and share

Why Choose DataM Intelligence?

- Business outcome focused market sizing that connects global forecast data with sourcing, capacity, investment decisions

- Detailed segmentation that identifies where growth is shifting across high-voltage cable, data cable, primary wire, harness systems

- Competitive intelligence that benchmarks suppliers by portfolio, target strategy, platform exposure

- Regional and country specific market analysis that supports go to market planning and localization choices

- Analyst perspective that converts raw market data into strategic recommendations for product development, partnerships, M&A

- Practical procurement insights that help buyers assess risk, quality, validation, long term supplier readiness