AI in Analytics Platforms Market Overview

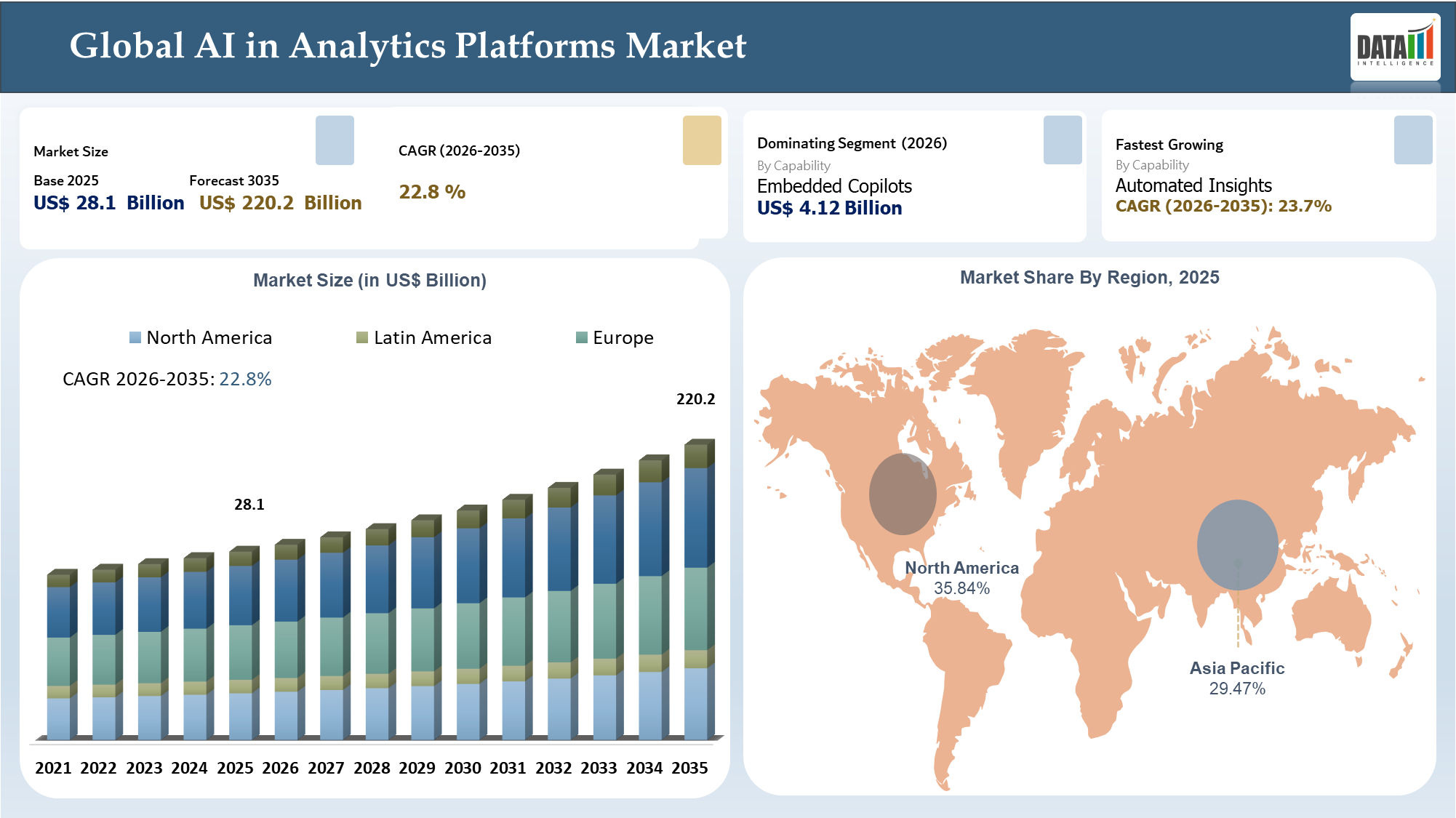

The global AI in Analytics Platforms market reached US$ 28.1 billion in 2025 and is expected to reach US$ 220.2 billion by 2035, growing with a CAGR of 22.8% during the forecast period 2026-2035. According to DataM insights, the AI in Analytics Platforms market is moving on to a new stage whereby value will not be generated simply through adding more AI-related functionality, but through enhanced decision-making capability within actual business processes. The market has moved on from differentiation that was largely surface level, such as general copilot and conversational functionalities, to more sophisticated solutions that include governed semantics, trust metrics, context-aware recommendations, and assisted analysis, all integrated directly into the enterprise decisioning context. This sets the bar higher for relevance of platform solutions, with customers increasingly favoring platforms that offer reliable outcomes, alignment with existing business operations, and scalable decision quality.

From DataM findings, competitive pressures are shifting from breadth of capabilities to depth of execution. Users are no longer judging the use of AI by analytics platforms based solely on ease-of-use or novelty; rather, they are determining whether the platform is able to detect anomalies, provide recommendations, and increase business responsiveness while maintaining appropriate governance and minimizing adoption hurdles. Consequently, providers with a proven ability to integrate workflows, monitor models, and implement outcomes-oriented solutions have gained a distinct competitive edge against vendors with more limited AI-based value propositions. While demand conditions remain positive, revenue achievement increasingly requires demonstrating the impact of AI within the very process area for which funds are being invested.

AI Impact Analysis

AI has become the driving force behind the success of the AI in Analytics Platforms Market. It has completely changed how platforms were developed, positioned, and used. The focus has shifted from showcasing the capabilities of the model in question to providing proof of its governance, auditability, and deployability within real-world work processes. Buyers now want to see if the AI-based analytics platform can provide reliable and controllable results without making the process unmanageable or unpredictable. This means that the observability of the AI, policy management, semantic governance, and integration with work processes take priority over the availability of models and additional features.

Secondly, we can see the growing role of orchestration and evaluation capabilities of platforms. Organizations understand that good model performance doesn't guarantee tangible results unless there is proper retrieval of models, validation of decisions, and analytics feedback loop. Those vendors who have managed to offer their solutions for building copilots and detecting anomalies have received disproportional attention.

Commercialization is another aspect impacted by AI in the AI in Analytics Platforms market. Sales departments can now offer simulation, configuration, and usage analysis services to clients, whereas post-sales departments rely on performance analytics to enhance their strategies for renewals, parts, and services.

There is a change in the way prices work as well, as customers start making their choice between various subscription plans, cost of building the necessary infrastructure, token economics, and anticipated labor efficiency. The winners, in fact, are the solutions that guarantee cost transparency, security, and tangible business results instead of being technically better or faster.

AI in Analytics Platforms Industry Trends and Strategic Insights

- Capabilities continue to be the most commercially relevant framework as they provide insight into buyer budgeting, supplier comparisons, and performance trade-offs within the AI in analytics offerings industry.

- The demand side is increasingly favoring offerings with the ability to demonstrate value propositions in Embedded Copilots and Automated Insights rather than platform-level value propositions.

- The USA and Canada are leading competition in North America through their influence in product design, sourcing, and marketing strategies.

- Successful suppliers are using product depth, application expertise, and ecosystem relationships to justify prices and accelerate buying cycles.

Market Scope

| Metrics | Details | |

| 2025 Market Size | US$ 28.1 Billion | |

| 2035 Projected Market Size | US$220.2 Billion | |

| CAGR (2026-2035) | 22.8% | |

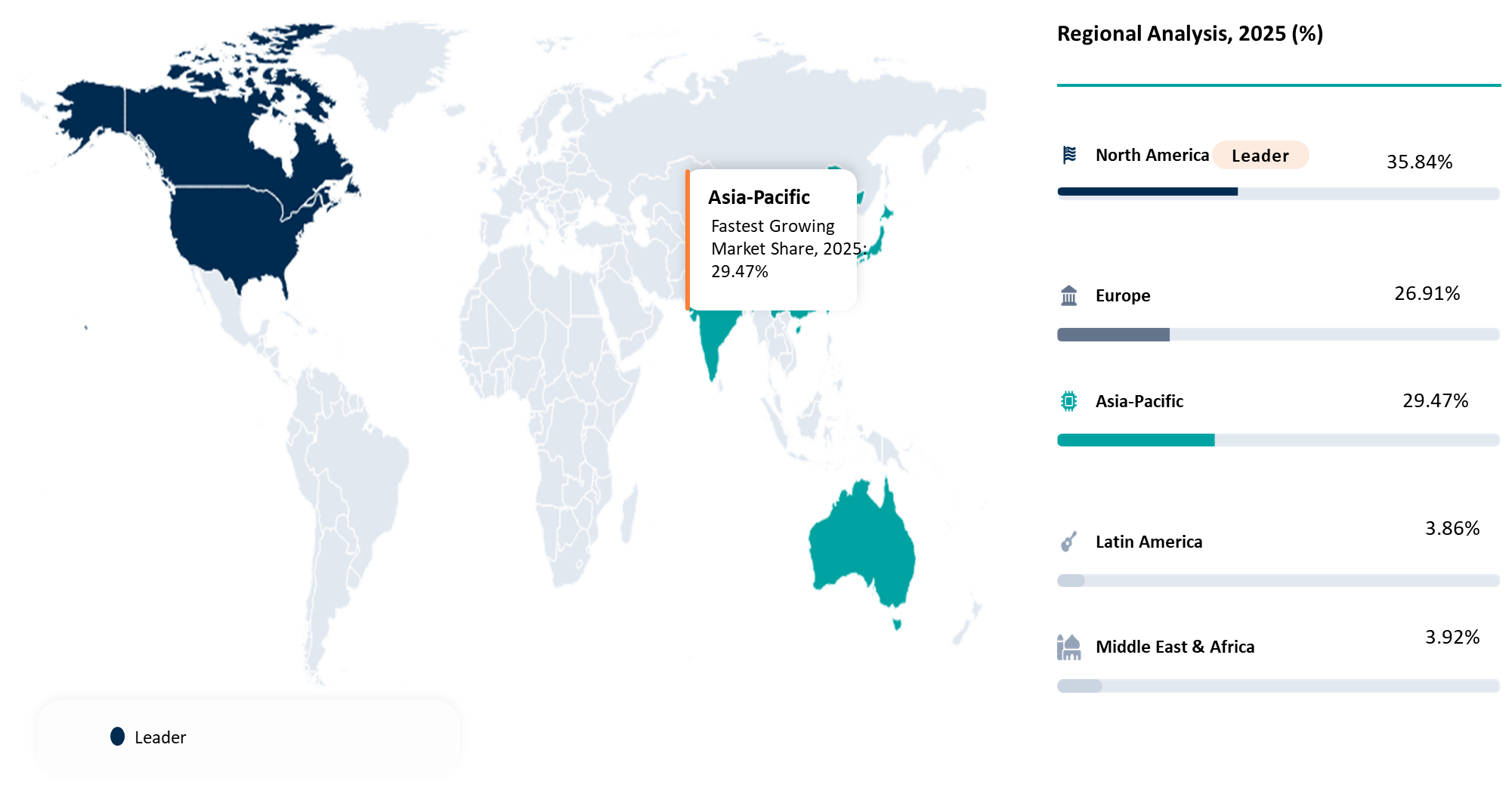

| Largest Market | North America | |

| Fastest Growing Market | Asia-Pacific | |

| By Capability | Natural Language Query, Predictive Analytics, Automated Insights, Embedded Copilots, Anomaly Detection | |

| By Deployment Model | Cloud, On Premises, Hybrid | |

| By Data Environment | Structured Data, Unstructured Data, Streaming Data, Semantic Layer Integrated Data | |

| By User Type | Business Users, Data Analysts, Data Scientists, Executives | |

| By End User | BFSI, Retail and E-commerce, Healthcare, Manufacturing, Telecom, Public Sector | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

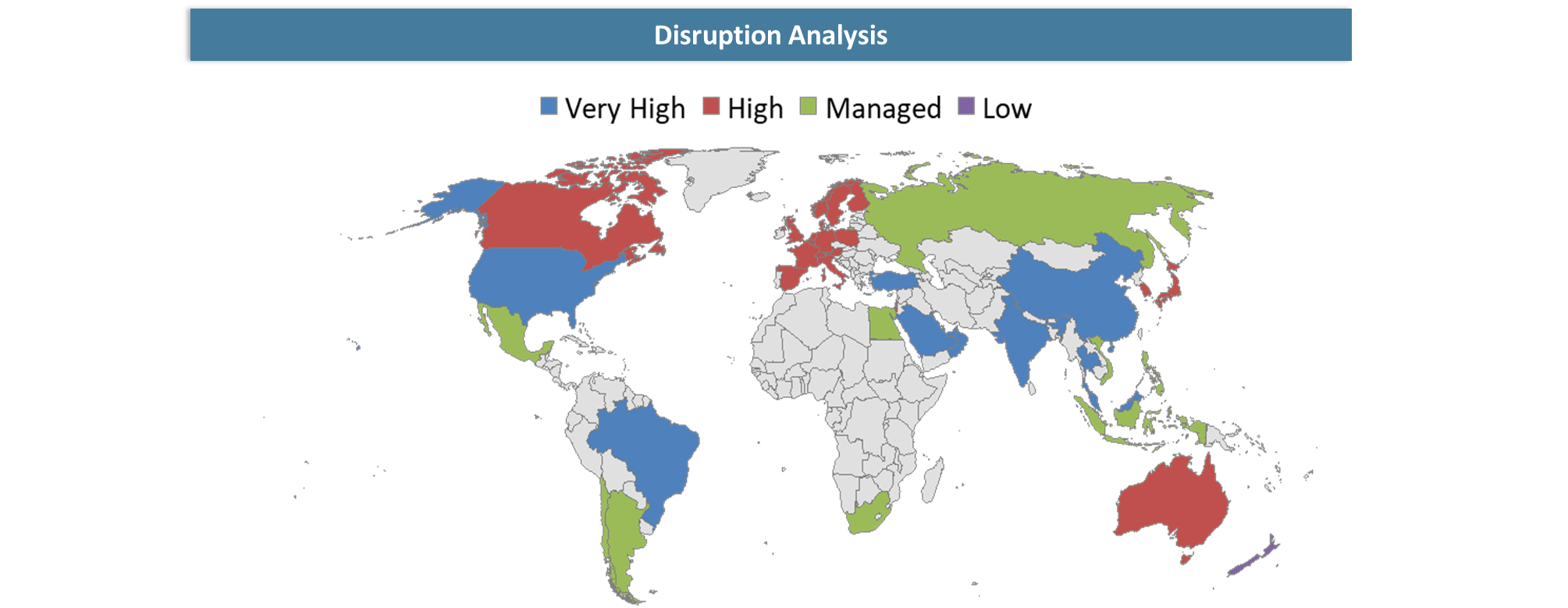

Disruption Analysis

Shift Toward Execution-Led Value, Platform Control, and Governance-Driven Economics in AI in Analytics Platforms Market

The primary market disruptor in the AI in Analytics Platforms Market is the move away from feature-driven competitive differentiation towards execution-based value creation. This adoption is quite mature at this point in time; indeed, a survey by McKinsey for 2025 shows that 78% of companies have adopted AI capabilities within one or more of their business functions while 71% use generative AI capabilities within at least one of these functions. This alters the nature of the business dialogue. Rather than merely praising suppliers who incorporate features such as co-pilots, natural language query, or automated insight generation, customers now demand whether these features will actually accelerate decision making, increase analyst productivity, or affect any business outcome positively in real-world situations.

The second disruption concerns architecture, with value becoming more focused on the vendors who own the data layer, semantic layer, and context in which AI runs. According to Microsoft’s Annual Report for 2025, Fabric had grown to 25,000 paying customers, and Power BI semantic models and OneLake were positioned as an architecture layer for enterprise AI applications. The significance lies in the fact that we are shifting from an age where the interface is innovating to an era where enterprise orchestration is the focus of the market. Architectures that are capable of integrating AI with data models, permissions, and business processes become more difficult to replace than those offering stand-alone conversational interfaces.

The third disruption is economic issues associated with governance. According to IBM's “Cost of a Data Breach 2025” study, the average data breach cost worldwide is $4.4 million, while 63 % of companies lack any AI governance policy, and 97 % of companies experiencing an AI-driven cybersecurity issue have inadequate AI access controls. From the perspective of the AI in analytics platforms market, this translates into increasing purchasing risk sensitivity. Customers increasingly opt for vendors who are able to deliver observability, access control, auditability, and accountability for the post-deployment of the offered solution. In other words, the winning proposal will no longer be the most extravagant one from the point of view of AI but rather the most cautious one that lowers business risks, regulatory risks, and price risks.

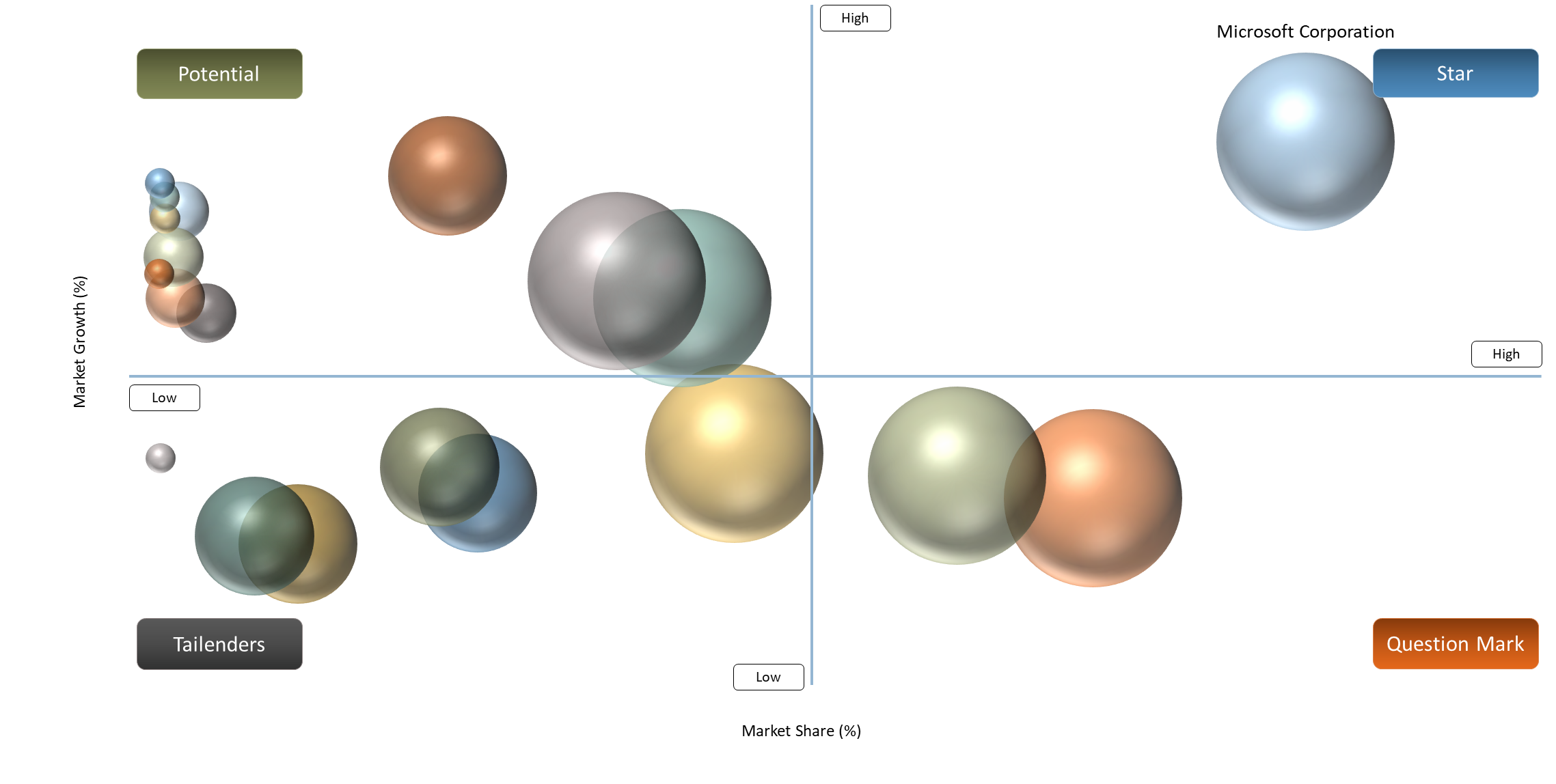

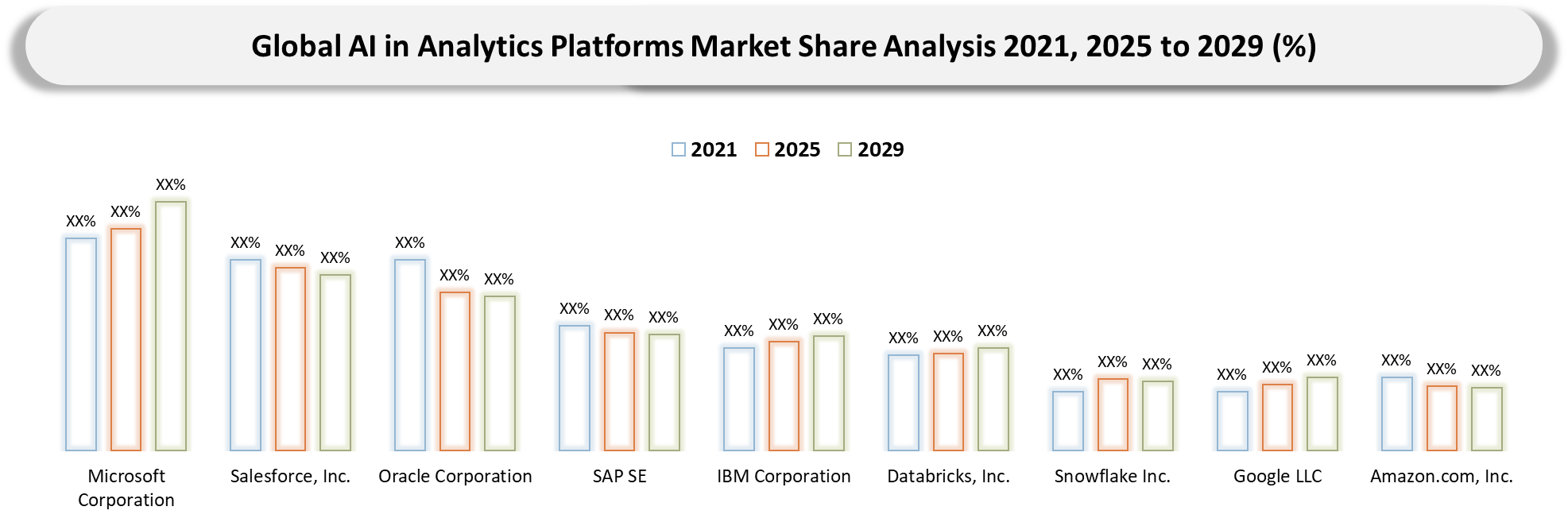

BCG Matrix: Company Evaluation

The market leaders for the AI in Analytics Platforms Market in BCG analysis include companies such as Microsoft Corporation, Salesforce, Inc., Oracle Corporation, SAP SE, Google LLC, and Amazon.com, Inc. These organizations are classified as such owing to their strong momentum, control over the ecosystem, cloud reach, and workflow integration. The success of such companies comes from setting high expectations in enterprise-level analytics and AI. On the other hand, those vendors that belong to the established value quadrant are characterized by large installed base, relationships within enterprises, and strong switching costs. Such organizations as IBM Corporation, SAS Institute Inc., Teradata Corporation, Informatica Inc., and MicroStrategy Incorporated are part of the established value quadrant. In addition, emerging opportunity quadrant involves Databricks, Inc., Snowflake Inc., ThoughtSpot Inc., Alteryx, Inc., Domo, Inc., and Hex Technologies, Inc. These vendors have gained prominence due to native analytics and automation, and more recently because of AI-native approaches. The selective pressure quadrant involves QlikTech International AB, Tableau Software, LLC, and TIBCO Software Inc.

Market Dynamics

Shift Toward Measurable Operating Value and Application-Specific Buying Criteria

Market growth in the AI in Analytics Platforms market space is now becoming driven more by vendor solutions that can deliver AI value through a defined decision workflow rather than those that merely overlay AI across a broader set of processes. This is clearly illustrated by where the commercial momentum is building: For example, Microsoft highlighted that the Fabric had achieved 25,000 paying customers, noting that the Power BI semantic model and OneLake platform formed the bedrock on which AI applications would be deployed at the enterprise level. Similarly, Salesforce announced that AI and Data Cloud had generated $900 million ARR in its FY25 period - representing a 120% YoY increase - alongside over 3,000 paying deals for its Agentforce platform and the Data Cloud reaching over 50 trillion records.

The growing maturity of the overall ecosystem represents another reason why the market can grow. As more organizations find ways to procure the supporting elements needed to take advantage of technology – including surrounding applications, integrators, connections, and manufacturing resources – they will be willing to make the purchase.

The other aspect related to the shift in demand is that consumers are seeking out platforms that offer more evidence of their capacity for deployment and data readiness. According to Qlik, there are 40,000 plus customers using the platform around the world. This indicates that market acceptance and credibility now go hand in hand with having a trustworthy foundation of data, experience with scale deployment, and the capability of turning artificial intelligence into tangible business results, not just features. The consequence of this trend is that demand is now being focused on embedded copilots, automated insights, and governed semantic layers where ROI can be justified more easily.

Integration Burden, Compliance Friction, and Longer Enterprise Decision Cycles

One of the main constraints in the market of artificial intelligence in analytics platforms is the growing mismatch between robust demand and limited enterprise-level adoption. The integration challenge persists as a major roadblock, especially when it comes to integrating AI into legacy data warehouses, governed semantic layers, and pre-existing BI stacks. As per Gartner, only 53% of AI projects transition successfully from pilot to production status, emphasizing the role of integration, data preparedness, and process optimization in hindering monetization. For analytics platforms, this becomes even more challenging since the AI results need to fit into established performance metrics, reporting frameworks, and business processes.

The compliance and governance demands are extending the deliberation time frame. According to IBM, only 63% of companies have AI governance policies, and in 97% of all security threats related to AI, there is an absence of access management, putting more pressure on the procurement process through legal, risk, and IT teams. This is especially true for analytics platforms integrated into financial planning, operational management, or customer decision journeys.

As a result, enterprise buying cycles are lengthening. Multi-stakeholder approvals, including data teams, compliance, and business owners, are becoming standard, slowing vendor onboarding. Suppliers that underestimate these constraints often overstate pilot-to-scale conversion timelines, while those with strong integration frameworks, governance capabilities, and implementation support are better positioned to capture revenue despite slower adoption cycles.

Segmentation Analysis

The global AI in Analytics Platforms market is segmented based on the capability, deployment model, data environment, user type, end user, and region/countries.

Capability-Centric Segmentation Shaping Commercial Outcomes in AI in Analytics Platforms Market

Economics start to diverge at the capability level since buyers are recognizing providers who have the capability to implement AI within an analytics governed environment, rather than simply providing a superficial AI assistant. Capability can be observed from vendor success. In February 2026, Databricks announced that it surpassed a $5.4 billion annual revenue run rate with more than 65% year-on-year growth, illustrating the significant investment that enterprises are making towards capabilities that offer data, analytics, and AI execution together within the same architecture. Investor materials from Snowflake list 733 customers driving revenues over $1 million on a trailing twelve month basis, 790 Forbes Global 2000 companies, and a net revenue retention rate of 125%, as of January 31, 2026, suggesting that capability-driven platforms can penetrate significantly after gaining access into the enterprise process flow. Lastly, Qlik claims that over 40,000 customers use its platform.

Under capability, the differentiation between embedded copilot and automated insights is driven by various commercial considerations. In cases where quick adoption, ease of use, and little disruption to the workflow process are the top priorities, embedded copilots are more likely to triumph. Conversely, automated insights become more relevant in scenarios where companies desire proactive decision-making, pattern recognition, and action generation using AI, with more control over the corporate environment. The current strategy of ThoughtSpot, which emphasizes its agentic analytics solution that offers insights “inside the agents, apps, and platforms” that people already use, demonstrates a move towards action-driven analytics rather than just dashboard-based analytics.

Geographical Penetration

North America Dominates as the Largest Region Driven by Enterprise-Scale Adoption and Governed Analytics Integration

North America continues to lead other regions on a commercial basis for the AI in Analytics Platforms Market since the region combines having many analytics users among enterprises alongside more rapid adoption of AI solutions in a live environment. According to a report from the Census Bureau in the United States, business use of AI has grown from 3.7% in September 2023 to 5.4% in February 2024 with projected adoption set to grow to 6.6% in early fall 2024, indicating growth in AI enterprise use in actual operational environments and not just pilot interest.

This is also significant since platform providers are growing through the provision of governed analytics architectures, not just through front-end AI capabilities. As mentioned in the 2025 Annual Report from Microsoft, Fabric has been adopted by 25,000 paying customers, with OneLake and Power BI semantic models seen as the basis for enterprise AI solutions. This is also significant since the region is where analytics platform buyers invest heavily in analytics platforms that include AI and trusted data layer governance.

While the U.S. is largely responsible for the revenue concentration in the region, Canada brings governance-based strategic significance to the picture by adopting AI through governance. Through its “AI Strategy for the Federal Public Service 2025-2027,” Canada has created an organized framework for responsible use of AI, thus strengthening demand conditions for sectors which require transparency and accountability from AI applications. Overall, the two North American countries demonstrate that the demand for AI analytics in North America comes from areas with governance significance.

U.S. AI in Analytics Platforms Market Trends

The United States is still the leading nation in the AI in Analytics Platforms Market since the U.S. not only spends heavily in terms of enterprise analytics but is also more inclined towards faster transition from experimentation to production adoption. As per the findings of the 2025 U.S. Census Bureau Center for Economic Studies Research Report, existing AI adoption amongst US businesses had increased from an estimated 3.5% in September 2023 to 9.5% in May 2025, and future AI adoption in the following six months was projected to be around 11%.

This is a clear indication that enterprise AI adoption is growing steadily and consistently through live business applications as opposed to being contained to pilot projects. Enterprises in the U.S. are also becoming more inclined to implement AI in governed data and analytics stacks. According to Databricks' 'State of Data + AI', this analysis is based on 10,000 customers, including over 300 Fortune 500 companies, and it was discovered that year-over-year growth in models registered for production had grown by 1,018%.

Canada AI in Analytics Platforms market Outlook

The strategic importance of Canada in the AI in Analytics Platforms Market is increasing because of the growing adoption rate and focus on AI governance. According to Statistics Canada, 12.2% of organizations implemented AI solutions to produce products or provide services in Q2 of 2025, which increased from 6.1% in Q2 of 2024. In terms of AI usage scenarios, data analytics occupied 26.4% of such use cases, which indicates that applications in analytics have become the leading segments in implementing AI applications for enterprises in Canada.

Another feature that distinguishes Canada is that there are governance and explainability criteria affecting AI growth. For example, as per the AI Strategy for the Federal Public Service 2025-2027 of the Government of Canada, it is noted that the strategy establishes an adequate AI governance framework to facilitate the ethical and transparent use of AI. This implies the demand for analytics platforms capable of providing traceability, policies and control, among others. Thus, Canada has become a strategic market for AI analytics platforms, where apart from automated insight generation and creation, accountability and explainability have become increasingly important.

Competitive Landscape

- The competition in the market of AI in Analytics Platforms is becoming increasingly clear in terms of the distinction between providers of comprehensive platforms and providers specializing in innovative analytics solutions. Competing in this category include large players such as Microsoft Corporation, Salesforce, Inc., Oracle Corporation, SAP SE, IBM Corporation, Google LLC, and Amazon.com, Inc. Meanwhile, competing in the second category include providers such as Databricks, Inc., Snowflake Inc., ThoughtSpot Inc., Alteryx, Inc., Domo, Inc., Hex Technologies, Inc., QlikTech International AB, Tableau Software, LLC, MicroStrategy Incorporated, SAS Institute Inc., TIBCO Software Inc., Teradata Corporation, and Informatica Inc. As the market evolves, competitive advantage comes to companies capable of combining advanced capabilities with strong support and customer relationships.

- Market positioning is now heavily dependent on how effectively the suppliers can protect the entire customer experience journey instead of the core product itself. The platform quality will be crucial, but the competitive edge will be determined by the ability to onboard customers easily, integrate effectively, maintain control of semantics and data, match workflows, manage models, and sustain the lifecycle. The vendors who can build trust in the highly lucrative segments like Embedded Copilots and Automated Insights stand a much better chance of defending their prices and growing their market share.

Key Developments

- March 2025: Microsoft Corporation expanded its AI in analytics strategy through deeper integration of embedded copilots within Fabric and Power BI, strengthening ecosystem partnerships to support enterprise-scale, workflow-driven analytics adoption.

- February 2025: Salesforce, Inc. accelerated commercialization of automated insights through Data Cloud and Agentforce, enhancing product-market fit, partner enablement, and enterprise support capabilities for AI-driven decision workflows.

- January 2025: Oracle Corporation advanced its analytics cloud positioning by embedding AI-driven insights and automation across Oracle Analytics Cloud, focusing on governed data environments and enterprise application integration.

- April 2025: SAP SE strengthened its Business Data Cloud and analytics portfolio by integrating AI capabilities into SAP Analytics Cloud, emphasizing semantic layers, enterprise data context, and business workflow alignment.

- May 2025: IBM Corporation enhanced its watsonx analytics ecosystem with a focus on governance, model monitoring, and explainability, addressing enterprise demand for controlled and auditable AI-driven analytics.

- June 2025: Databricks, Inc. expanded its Data Intelligence Platform capabilities by integrating AI models with unified data architectures, reinforcing its position in automated insights and large-scale analytics deployment.

- July 2025: Snowflake Inc. strengthened its Cortex AI capabilities within its data cloud, enabling embedded analytics, automated insights, and scalable AI model deployment across enterprise datasets.

- August 2025: Google LLC expanded Vertex AI and Looker integration, focusing on embedding AI-driven analytics and natural language insights into enterprise data workflows and applications.

- September 2025: Amazon.com, Inc. enhanced AWS analytics services by integrating generative AI capabilities into tools such as QuickSight, improving automated insights and enterprise reporting efficiency.

- October 2025: ThoughtSpot Inc. advanced its agentic analytics platform strategy, emphasizing AI-driven insights delivered directly within enterprise applications, workflows, and decision environments.

White Space Opportunities

As pointed out by DataM, one of the most evident white spaces in the AI in Analytics Platforms Market is beyond the enterprise purchasing programs that are most prominent. Though many vendors are still aggressively pursuing platform mandates, there is a need for their products in narrower, higher friction decision environments where the buyer seeks certainty, governance, and deliverable results over broader product sets. In other words, vendors that are able to bundle their offerings based on certain functionalities like Embedded Copilots or Automated Insights along with implementation and change management capabilities can generate more profitable sales.

From our perspective, another whitespace for suppliers is in the commercialization process rather than product capability itself. Customers are showing an increasing preference towards those providers that can lower adoption barriers through onboarding, validation, governance preparation, performance demonstration, and optimization services after the deployment process. Another deficiency occurs at the midmarket and vertical-specific account level, where customer demand may be genuine but is being overlooked because of a larger emphasis on enterprise deals. Our estimation suggests that the winners in the future will be companies with repeatable outcome-based solutions targeting these more elusive profit centers.

DMI Opinion

According to DataM, rather than asking if enterprise demand for AI-based analytics platforms even exists, the key question is rather about what suppliers can turn AI interest into commercially scalable implementations that are operational and governance-friendly. Increasingly, the market rewards companies that help customers to adopt AI in a way that makes its application credible in practical analytical operations. In our opinion, success is a result of trustworthy data foundations, integrations, semantic governance, and the creation of tangible business value without growing complexity.

In accordance with DataM’s observations, many industry players overrate the value of wide AI positioning and underrate deployment-related aspects. Indeed, the buyer decision process is more and more based on factors such as implementation cost, readiness to govern models, traceability of models, and the reality of claimed productivity/decision advantages. This is precisely why the vendors that concentrate efforts on deployment-related activities have better prospects than other suppliers.

Why Choose DataM?

- Technological Innovations: Encompasses recent innovations in AI within Analytics Platforms, such as embedded copilot capabilities, natural language query, automated insights, semantic layer, predictive analytics, and integration with cloud, data fabric, and enterprise workflow systems.

- Positioning of Major Providers: Analyzes top vendors on factors like platform scalability, integration, governance, analytics effectiveness, enterprise penetration, user experience, and workflow suitability.

- Use Cases for AI in Analytics Platforms: Illustrates practical applications like automated reporting, anomaly detection, decision-making support, forecasting, customer analytics, financial analytics, and operational performance monitoring.

- Market Trends and Dynamics: Investigates prevailing trends, such as the need for reliable measurement metrics, emergence of automated insights, increased use of embedded AI, hybrid deployment strategies, and the emphasis on decision-making value within enterprises.

- Competitive Strategies: Details strategies employed by competitors to increase market share, including improving their platforms, partnering with ecosystems, integrating workflows, incorporating governance, and differentiating through capabilities.

- Pricing Models and Market Access: Discusses pricing structures such as subscription, pay-per-use, enterprise licensing, and implementation-based pricing, as well as integration, support, and governance costs.

- Market Expansion and Growth: Identifies avenues for growth in terms of industries, functional areas, and mid-market organizations.

Target Audience

- Product strategy teams

- Corporate strategy and market intelligence teams

- Business development leaders

- Sales and channel leaders

- Investors and private equity firms

- Procurement and sourcing teams

- Technology and operations leaders

- Consulting and advisory teams.