AI Agents for IT Operations Market Size & Growth

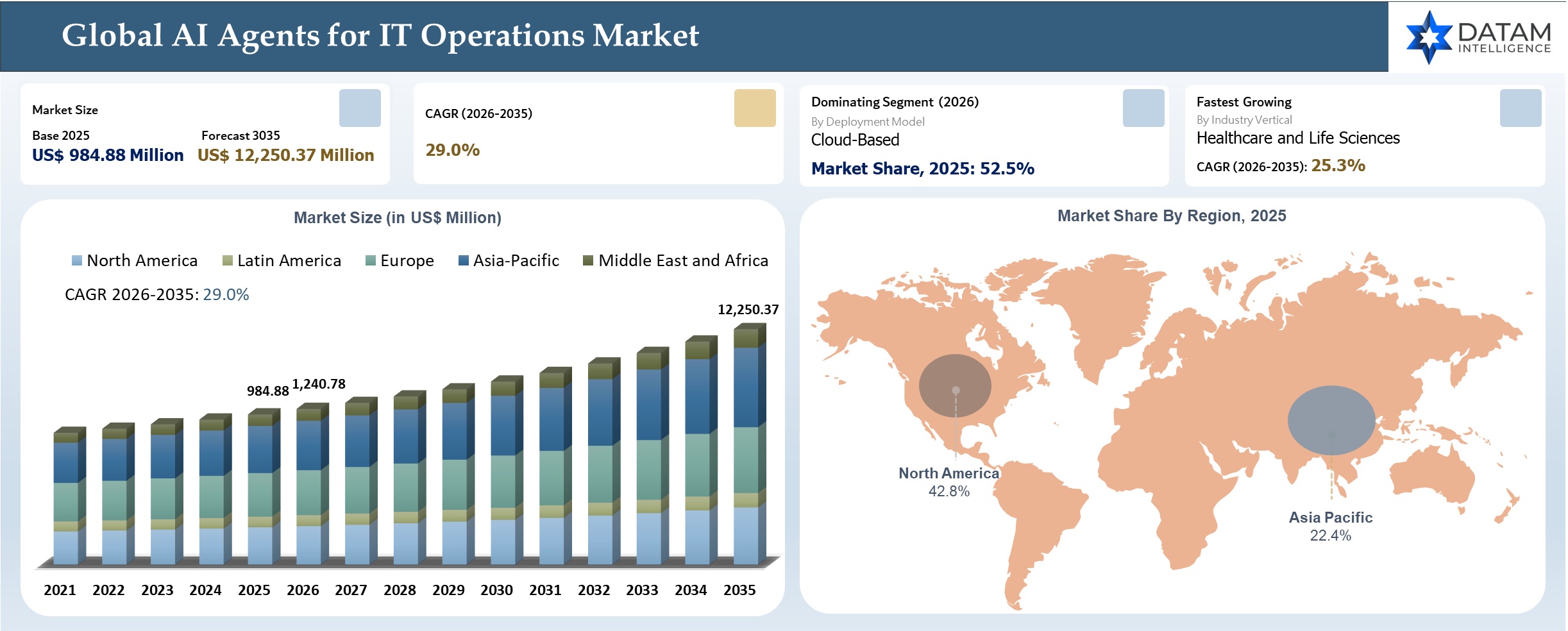

The global AI Agents for IT Operations market reached US$ 984.88 million in 2025 and is expected to reach US$ 12,250.37 million by 2035, growing with a CAGR of 29.0% during the forecast period 2026-2035. AI agents are helping transform IT operations through the potential of moving from traditional and manual IT processes to intelligent and autonomous actions. The complexities of modern systems and the deployment cycle have revealed that existing solutions based on monitoring and automation of processes are unable to ensure effective operation due to increased downtimes and costs associated with the management of processes. The incorporation of AI agents within AIOps platforms offers an advantage as they can correlate all information collected from the IT stack and conduct root cause analysis as well as automatic resolution of issues.

AI Agents for IT Operations Industry Trends and Strategic Insights

- AI-driven automation of IT processes is shifting IT operations from incident response to fully automated actions. The real-time correlation of data from logs, metrics, and traces facilitates real-time root cause analysis and automation of remediation processes. It decreases MTTR to minutes and eliminates human intervention.

- AI is being incorporated into observability systems, CI/CD workflows, infrastructure, networking, and security. This results in an overall operating paradigm where the verification of deployments, resolution of incidents, and optimization of resources are all handled in a coordinated manner, providing both agility and reliability.

- Adoption takes place in high impact scenarios like incident management, capacity planning, and infrastructure automation. Companies are focusing on building interoperable AI environments, observability, and strong governance systems to guarantee regulatory compliance, security, and operational savings that increase with automation scale.

AI Agents for IT Operations Market Scope

| Metrics | Details | |

| 2025 Market Size | US$ 984.88 Million | |

| 2035 Projected Market Size | US$ 12,250.37 Million | |

| CAGR (2026-2035) | 29.0% | |

| Largest Market | North America | |

| Fastest Growing Market | Asia-Pacific | |

| By Component | Platform/Software and Services | |

| By Agent Function | Detection, Diagnosis, Remediation, Prediction and Optimization | |

| By Technology Architecture | Deterministic AI Agents, Learning-Based Agents, Generative AI Agents, Reinforcement Learning and Multi-Agent Systems | |

| By Deployment Model | On-Premises and Cloud-Based | |

| By Operational Environment | Infrastructure Operations, Network Operations, Cloud Operations, Application Operations and Others | |

| By Enterprise Size | Large Enterprises and Small and Medium Enterprises (SMEs) | |

| By Industry Vertical | Banking, Financial Services, and Insurance (BFSI), IT and Telecom, Healthcare and Life Sciences, Retail and E-commerce, Manufacturing, Government and Public Sector, Energy and Utilities and Others | |

| By Integration Type | Native AIOps Platforms, ITSM-Integrated Agents, Observability-Integrated Agents and Standalone Agents | |

| By Use Case | Anomaly Detection and Alert Management, Automated Incident Resolution, Capacity Planning and Forecasting, Service Performance Optimization, Change and Configuration Management Automation and Cost and Resource Optimization | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

Disruption Analysis

Shift from Human-Led Incident Management to Autonomous Resolution

The use of AI agents is changing incident management from a process that relies on manual ticketing systems to an autonomous one with a closed-loop process. With the traditional method, engineers would have to find the correlation between the alerts and determine the root cause before solving the problem within various systems, making the process take longer and increasing costs due to downtime.

It also has implications beyond efficiencies to a paradigm shift in how systems operate and costs are incurred. The need for a huge operations staff is reduced as troubleshooting activities become automated, enabling engineers to spend time designing, optimizing, and overseeing systems. Value generation shifts from effort-based service delivery to outcome-based performance metrics such as uptime, reliability, and operational efficiency, creating a competitive advantage for organizations that adopt autonomous IT operations.

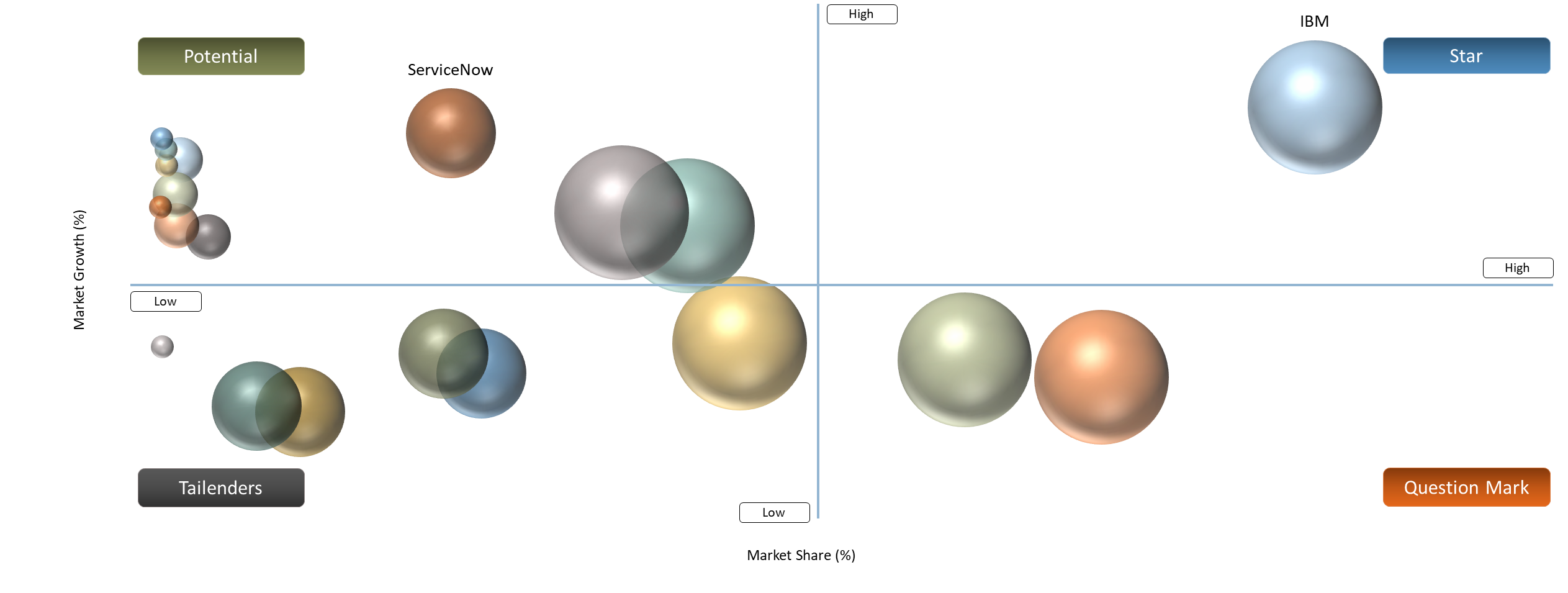

BCG Matrix: Company Evaluation

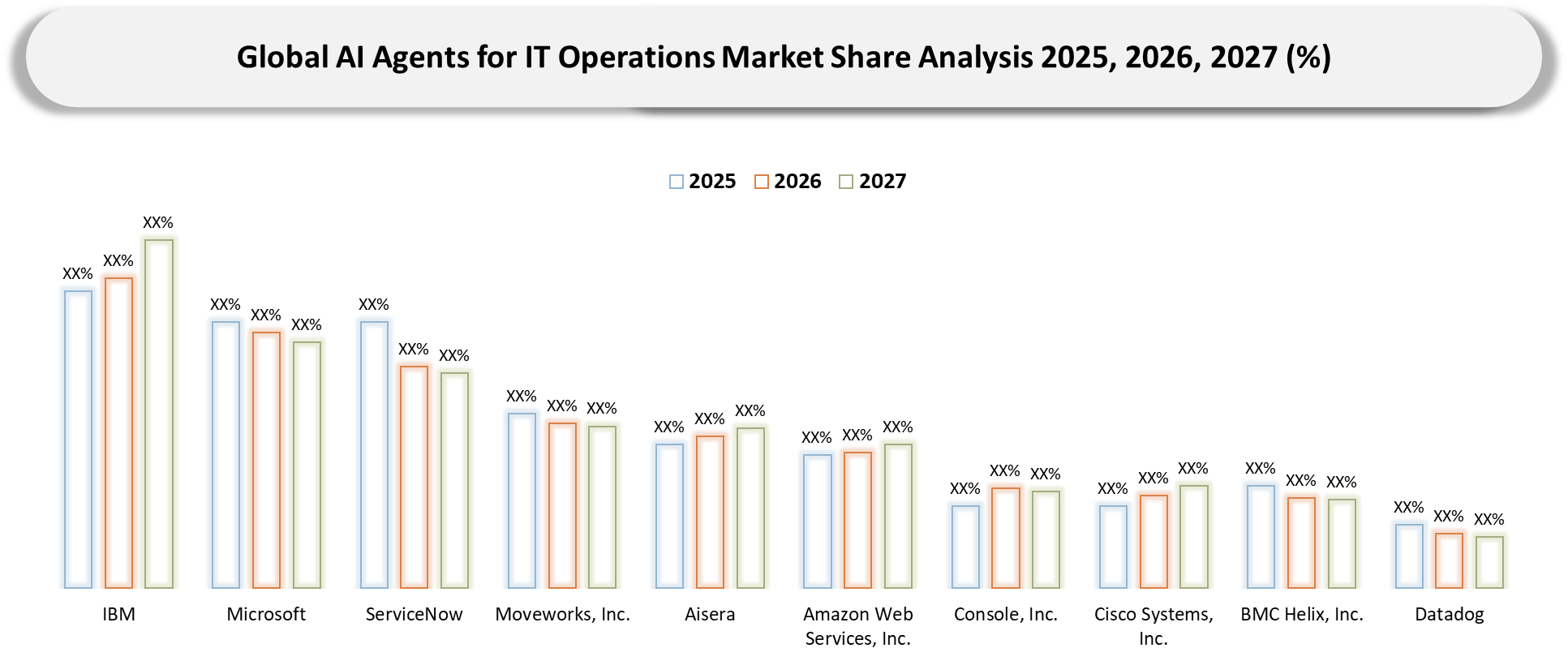

BCG Matrix analysis for AI agents in IT Operations reveals a market dominated by platform-driven market leaders and fast-moving innovators. The company that lies in the Stars category is Microsoft, with its dominance in the market and extensive use of AI technology. Amazon Web Services, IBM, and ServiceNow lie in the Potential category, where there is potential for development with their significant capabilities and enterprise reach, yet they are developing AI agents.

Emerging players such as Moveworks, Inc. and Aisera are categorized in the Question Mark quadrant because of the significant level of innovation but the low degree of market presence, and, therefore, they should achieve growth by expanding into new ecosystems. The following vendors are classified as Tailenders: Cisco Systems, Inc., BMC Helix, Inc., ScienceLogic, Datadog, and Console, Inc. because of their less differentiating AI agents' capabilities in comparison to those of competitors.

AI Agents for IT Operations Market Dynamics

Increasing Cost of Downtime Accelerating Autonomous IT Operations Adoption

Increasing financial consequences of unscheduled downtimes are one of the key drivers of the size of the AI for IT ops market and the growth of the AIOps market. According to Uptime Institute, a growing percentage of business disruptions is now exceeding USD 100,000 for each outage, with major disruptions costing more than USD 1 million. The situation is making companies switch from legacy monitoring to IT automation using artificial intelligence and incident response AI, enabling automatic detection, correlation, and troubleshooting actions. Due to this, the companies are focusing on acquiring IT monitoring software with AI.

The adoption will be driven by the imperative to minimize Mean Time to Resolution (MTTR) within hybrid environments. Companies are implementing advanced IT operations functionalities that employ machine learning techniques to detect fault trends prior to disruption, thus contributing to the IT automation AI market research trends in terms of operational efficiency. Top players are incorporating AI agents into observation and automation solutions for IT operations, thereby facilitating faster triage, root cause analysis, and implementation of remediation measures. It will significantly impact the development of the IT operations market forecast, as well as the importance of AI agents in the field of enterprise IT operations.

Operational Risk and Control Limitations Restraining Autonomous AI Agent Adoption

Operational risk continues to be a fundamental limitation in expanding the implementation of AI-powered IT automation, especially where AI-driven bots are enabled to perform actions on live production systems. Large organizations have IT systems that are highly integrated, covering applications, infrastructures, and cloud services, which means that one wrong automated action will cause major disruptions to services. According to guidelines provided by firms like Google’s SRE, it is essential to implement stringent change control procedures, error budgeting, and rollout control to avoid any unintended problems. It introduces an element of unpredictability in the actions performed by autonomous bots, making organizations hesitant to leverage AI-based incident response tools.

Control constraints also hinder the use of AI and IT tools that employ automation in monitoring because corporations need determinism and rollback assurances prior to allowing AI programs full control over the IT operation. Many companies use human approval procedures for automation and put policies in place to reduce risks, delaying their adoption of autonomous prediction-driven IT operation.

AI Agents for IT Operations Market Segmentation Analysis

The global AI Agents for IT Operations market is segmented based on component, agent function, technology architecture, deployment model, operational environment, enterprise size, industry vertical, integration type, use case and region.

Scale Generative AI Agents for Intelligent, Self-Healing IT Operations

Generative AI agents are evolving into a high-impact category, as they allow for autonomous execution of complicated IT workflows involving real-time reasoning, planning, and action. In contrast to traditional approaches, the generative AI agents leverage both LLMs and agency to perform reasoning over structured/unstructured data such as logs, tickets, and events and create contextual actions to address the problem. This technology empowers companies to progress from rule-based decision-making to intelligent, adaptive operations where incidents can be detected, analyzed, and resolved in one single loop.

Specifically, in the field of IT management, the use of generative AI agents provides definite business benefits in the form of predictive maintenance, ticketing automation, and proactive problem-solving, thus avoiding downtime and minimizing operational costs. Technology is able to apply its analytics in order to recognize patterns of failure, recommend appropriate fixes, and increase the efficiency of the infrastructure used while eliminating human effort throughout the process. Companies embracing this area have seen increased system uptime and increased efficiency, making it an essential feature of future AIOps tools.

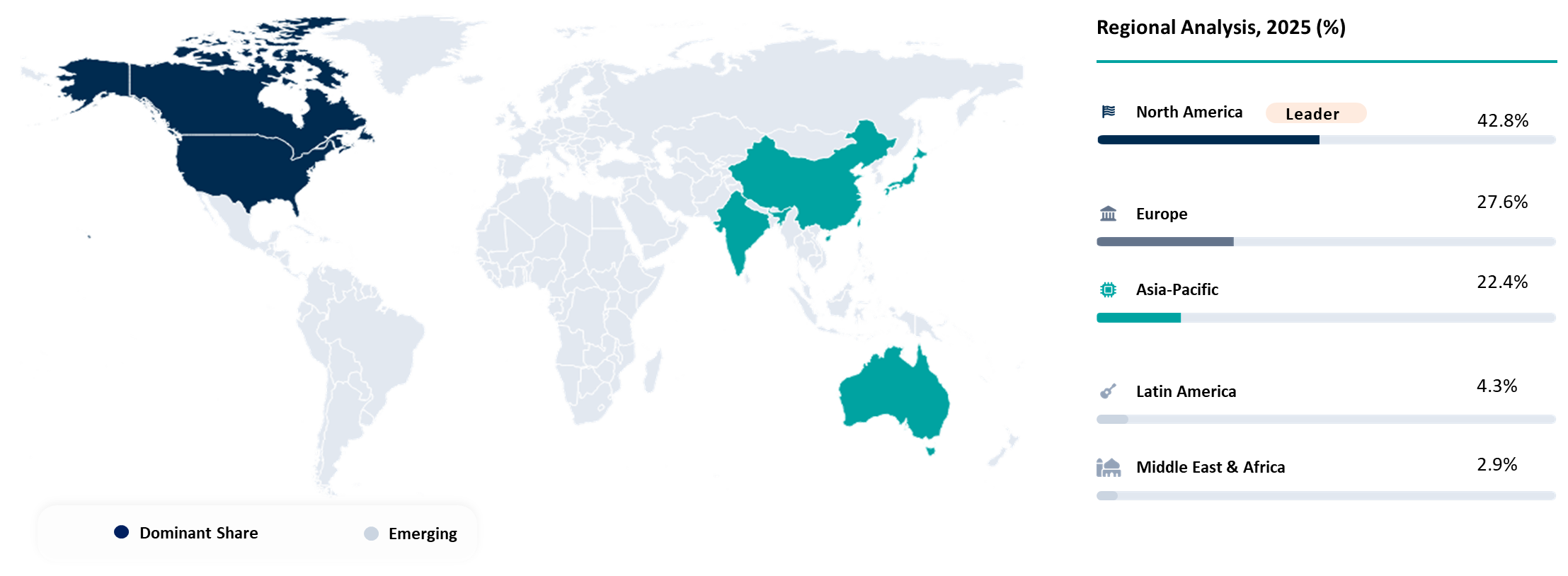

AI Agents for IT Operations Market Geographical Penetration

North America Led by Hyperscale Cloud Ecosystems and Enterprise Automation Maturity

North America leads the market owing to its superior cloud infrastructure, digital maturity, and early adoption of AI-based IT operations in enterprises. Organizations throughout the region are running highly distributed and multi-cloud deployments, resulting in the need for smart monitoring, predictive analytics, and automation of incident management. The continuous investment in cloud-native solutions and observability technologies is propelling the adoption of autonomous IT operations.

The presence of a robust vendor ecosystem, backed by the power of hyperscalers and enterprise software vendors, is crucial for the quick implementation and scaling of AI-powered operational tools. The emphasis on resilience, availability, and cost-effectiveness at enterprises is driving the adoption of automation-based IT management solutions.

United States Driven by Hyperscaler Innovation and Enterprise-Scale IT Complexity

US dominates regional growth due to the deep integration of AI into key cloud services like AWS, Microsoft, and Google. Organizations manage highly sophisticated IT infrastructure that requires sophisticated monitoring and prediction systems, as well as automated remediation measures to ensure consistent service availability.

Adoption is reinforced by mature engineering practices and significant investments in innovation. National initiatives like the National AI Initiative are improving research efforts and the enterprise’s preparedness for AI. The high level of investment in IT and the fast adoption of cutting-edge technology reinforce the leadership position of the US when it comes to innovation and implementation.

Canada Supported by Policy-Led AI Development and Regulated Industry Demand

Canada represents a stable and growing economy due to its government’s active participation and developed AI research framework. Programs like Pan-Canadian Artificial Intelligence Strategy are encouraging innovative approaches that are helping companies integrate AI into their operations. The rise in cloud use cases will increase demands for intelligent monitoring and automation in hybrid infrastructures.

Sectors like banking, telecommunications, and public services are at the forefront of adopting the technology, where reliability, compliance, and continuous service delivery are essential. Companies are emphasizing the need for systematic and managed implementation of AI-powered operations through partnership among academia, small and new firms, and international technology firms. It has been instrumental in driving consistent growth of the market.

AI Agents for IT Operations Market Competitive Landscape

- AI agents for IT Operations exhibit a competitive environment dominated by leading platform vendors operating through well-built cloud ecosystems and a deep enterprise footprint. Microsoft, AWS, IBM, and ServiceNow dominate this domain by deploying their AI agents in observability, IT service management, and DevOps landscapes, which results in seamless automation and closed-loop operations. Such entities have the advantage of being integrated platforms with significant customer footprints and constant investments in AI technologies.

- Additionally, there are a variety of innovators and IT operations vendors, including Moveworks, Inc. and Aisera, which provide unique solutions to help businesses implement automation and conversational agents based on AI technology. These companies contribute to innovations in autonomous workflows while continuing to broaden their presence in the market. At the same time, other companies such as Datadog, Cisco Systems, Inc., ScienceLogic, BMC Helix, Inc., and Console, Inc. benefit from their strong observability, network management, and ITSM services but struggle to enhance their AI agents' integration and platform unification capabilities.

- Key players include IBM, Microsoft, ServiceNow, Moveworks, Inc., Aisera, Amazon Web Services, Inc., Console, Inc., Cisco Systems, Inc., BMC Helix, Inc., Datadog and ScienceLogic

Key Developments in AI Agents for IT Operations Market

- October 2025 - Digitate introduced a new version of their Ignio software, which comes with a collection of AI agents that can be used for autonomous IT Operations. The new platform helps to implement ticketless IT using an agentic approach based on deterministic, predictive, and generative AI.

- November 2025 - Cognizant announced its new solution called Cognizant Resilient IT Operations that uses a platform-based approach with AI-powered agents and automation to revolutionize IT operations within enterprises. The solution allows for the process of agentification of IT processes via self-healing automation, proactive management of incidents, and minimizing operational debt, helping businesses increase their resiliency and move towards innovation.

- October 2025 - The SolarWinds AI Agent was released for IT operations, with the introduction of a context-aware platform that would improve the autonomous capabilities of operational resilience. It allows for predicting issues, executing responses automatically, and identifying the root cause of incidents, all the while acting as an intelligent team member in the process of observability and incident management.

- May 2025 - ServiceNow launched AI agents for IT ops, making it possible to have autonomous detection and solving of issues in ITSM, ITOM, and ITAM landscapes. The move is geared towards facilitating the transition from reactive assistance to proactive management through automation of alert triaging, root cause determination, and service process optimization.

Why Choose DataM?

- Technological Innovations: Explores advancements in AI agents and AIOps platforms, including generative AI-driven agents, reinforcement learning models, multi-agent architectures, and edge AI integration. Focus includes how these technologies enhance real-time data correlation, enable autonomous incident resolution, improve predictive maintenance accuracy, and support self-healing IT environments across hybrid and multi-cloud infrastructures.

- Product Performance & Market Positioning: Evaluates how leading AI agent platforms perform across key IT operations functions such as incident management, observability, infrastructure automation, and DevOps optimization. Analysis compares capabilities in root-cause analysis, scalability, integration with existing IT ecosystems, and deployment flexibility, highlighting differentiation among major vendors and emerging players.

- Real-World Evidence: Highlights enterprise adoption of AI agents in IT operations, including use cases in automated incident resolution, anomaly detection, capacity forecasting, and network optimization. Demonstrates measurable outcomes such as reduced MTTR, lower downtime, improved system reliability, and increased operational efficiency across large-scale IT environments.

- Market Updates & Industry Changes: Tracks key developments such as new AIOps platform launches, advancements in generative AI capabilities, strategic partnerships between cloud providers and enterprise software vendors, and increased investment in AI-driven automation. Coverage includes expansion of AI-enabled observability solutions and growing adoption across North America, Europe, and Asia-Pacific.

- Competitive Strategies: Analyzes how leading players strengthen market position through AI integration across product portfolios, partnerships with cloud and enterprise platforms, development of proprietary AI models, and expansion of end-to-end automation capabilities. Focus includes ecosystem building and platform consolidation to deliver unified, intelligent IT operations solutions.

- Pricing & Market Access: Explains pricing models including subscription-based SaaS platforms, usage-based pricing for cloud-integrated AIOps solutions, and enterprise licensing for advanced AI capabilities. Reviews accessibility through cloud marketplaces, API-based integrations, and partnerships that enable scalable deployment across diverse IT environments.

- Market Entry & Expansion: Identifies growth opportunities driven by increasing IT complexity, rising demand for automation, and expansion of hybrid and multi-cloud environments. Outlines strategies for market entry and scaling, including targeting high-impact use cases, building interoperable platforms, forming strategic alliances, and expanding into regions with strong digital transformation initiatives.

Target Audience

- Enterprises & IT Operations Teams: Large enterprises across BFSI, telecom, healthcare, retail, and manufacturing deploying AI agents to automate incident management, improve system reliability, and optimize hybrid and multi-cloud environments. Focus includes reducing downtime, enhancing service performance, and scaling IT operations efficiently.

- Managed Service Providers (MSPs) & IT Service Firms: Service providers integrating AI-driven AIOps capabilities to deliver proactive monitoring, automated remediation, and outcome-based service models. Emphasis is on improving service-level agreements (SLAs), reducing operational costs, and enhancing client value propositions.

- Cloud Service Providers & Hyperscalers: Organizations such as Amazon Web Services, Inc., Microsoft, and Google Cloud embedding AI agents within cloud platforms to enhance observability, automation, and infrastructure management capabilities for enterprise customers.

- AIOps & Enterprise Software Vendors: Companies including ServiceNow, IBM, and BMC Helix, Inc. developing AI-native platforms that integrate ITSM, observability, and automation to deliver end-to-end intelligent IT operations solutions.

- Investors & Private Equity Firms: Investment groups targeting high-growth opportunities in AI-driven automation, AIOps platforms, and agent-based architectures, with focus on startups and scale-ups delivering autonomous IT operations capabilities.

- Government & Regulatory Bodies: Public sector organizations supporting digital infrastructure modernization, cybersecurity resilience, and AI adoption through policy frameworks, funding programs, and compliance standards for autonomous IT systems.

Related Reports

The Artificial Intelligence for IT Operations (AIOps) Platform Market is the closest adjacent market to AI agents for IT operations, providing the underlying analytics, automation, and observability capabilities that enable autonomous IT management. Organizations are increasingly adopting AI-driven platforms to reduce downtime, automate incident resolution, and improve infrastructure reliability. The growing complexity of hybrid IT environments is accelerating investments in intelligent AIOps solutions.

Server less computing enables AI agents to execute event-driven automation without managing underlying infrastructure, making it an ideal deployment model for modern IT operations. Organizations are adopting serverless architectures to improve scalability, accelerate application deployment, and reduce operational overhead. The convergence of serverless computing and AI-driven automation is transforming enterprise IT operations.

Cloud infrastructure provides the compute, networking, and storage foundation required for AI agents to monitor, analyze, and automate enterprise IT environments. As businesses expand hybrid and multi-cloud deployments, AI-powered operations platforms rely on scalable cloud infrastructure to deliver real-time intelligence. Growing cloud adoption continues to drive demand for autonomous IT management solutions.

Artificial intelligence powers autonomous IT agents through machine learning, natural language processing, and generative AI technologies. AI agents help organizations automate incident management, optimize infrastructure performance, and improve operational resilience. Rapid enterprise AI adoption is accelerating the evolution of intelligent IT operations.

AI agents process massive volumes of operational logs, telemetry, and enterprise data, making data security a critical requirement. Big data security solutions protect AI-driven IT operations through encryption, threat detection, and access governance. As organizations automate more operational tasks, securing AI workflows has become a strategic priority.

Application security ensures AI agents can safely automate software deployments, vulnerability detection, and remediation across enterprise environments. Modern DevSecOps practices increasingly integrate AI-powered agents to identify security risks before production deployment. The demand for secure autonomous software operations continues to expand.

AI data centers provide the high-performance infrastructure necessary for training, deploying, and managing enterprise AI agents. Increasing adoption of generative AI, autonomous operations, and intelligent observability platforms is driving investment in AI-optimized data center infrastructure. High-performance computing remains essential for large-scale AI operations.

Edge AI enables IT operations agents to analyze infrastructure data closer to where it is generated, reducing latency and enabling faster incident response. Intelligent edge deployments improve operational resilience across distributed enterprise environments. The combination of edge computing and AI agents is accelerating autonomous IT management.

Data Center Infrastructure Management (DCIM) solutions complement AI agents by providing visibility into servers, storage, networking, power, and cooling systems. AI agents leverage DCIM data to automate capacity planning, predictive maintenance, and resource optimization. As enterprises modernize their IT infrastructure, AI-driven DCIM is becoming a key component of autonomous operations.