AI Infrastructure Enters a Critical Expansion Phase

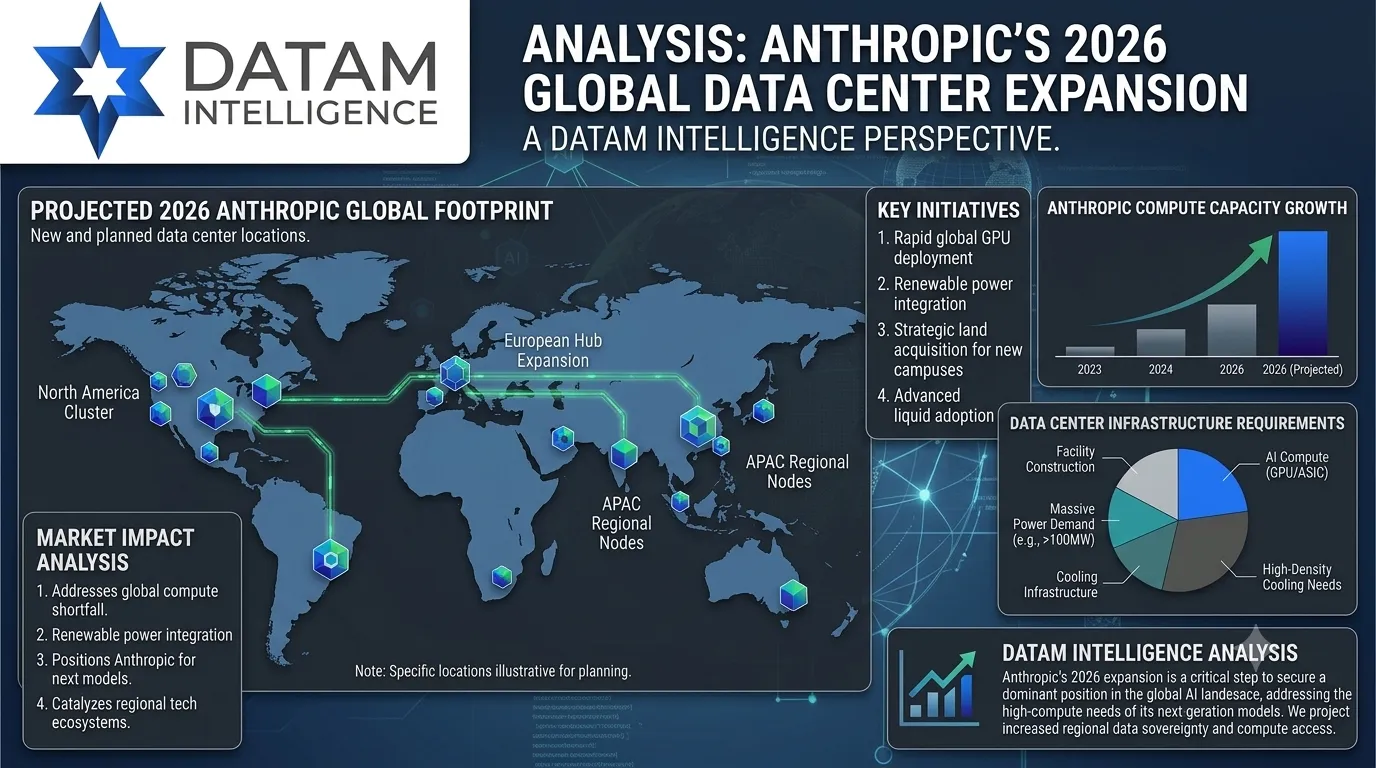

The artificial intelligence sector is undergoing a major transformation as demand for high-performance compute infrastructure accelerates at an unprecedented pace. According to recent industry developments and reporting from CNBC (June 2026), Anthropic is significantly expanding its global AI infrastructure footprint to support next-generation AI systems, including increasingly complex reasoning and multimodal models.

This move underscores a broader industry reality: AI progress is now fundamentally constrained by compute availability rather than algorithmic innovation alone.

As model sizes grow and enterprise adoption of generative AI accelerates, the demand for hyperscale data center capacity is reshaping global cloud and infrastructure markets.

The Rise of AI Data Centers as Strategic Infrastructure

AI data centers are evolving from traditional cloud computing facilities into highly specialized compute environments designed for:

- GPU-intensive model training

- Real-time AI inference at scale

- High-bandwidth distributed computing workloads

- Low-latency enterprise AI applications

The global shift is being driven by exponential growth in generative AI applications across industries such as finance, healthcare, logistics, manufacturing, and software development.

Industry analysis from the AI Data Centers Market Report indicates that this sector is entering a sustained high-growth cycle, supported by hyper scaler capital expenditure and long-term enterprise AI adoption strategies.

Anthropic’s Strategic Compute Expansion

Anthropic’s infrastructure strategy reflects a new competitive paradigm in artificial intelligence: compute-first scaling.

Rather than relying solely on software optimization, frontier AI companies are now prioritizing:

- Long-term cloud and colocation partnerships

- Dedicated GPU cluster access agreements

- Multi-region infrastructure diversification

- Energy-efficient compute scaling strategies

This approach ensures stable access to the massive computational resources required to train and deploy frontier models such as Claude and future multimodal AI systems.

The company’s expansion also reflects increasing competition among leading AI labs to secure limited GPU supply and high-density compute infrastructure.

Global AI Compute Demand Reshaping Market Dynamics

The rapid expansion of AI workloads has triggered a structural shift in global infrastructure economics. Key market drivers include:

1. Explosive Growth in Generative AI Usage

Enterprise adoption of AI copilots, automation systems, and agent-based workflows is driving sustained compute consumption.

2. GPU Supply Chain Constraints

Demand for high-performance accelerators continues to outpace manufacturing capacity, particularly for advanced AI chips.

3. Hyperscaler Capital Investment Surge

Major cloud providers are investing hundreds of billions into AI-optimized infrastructure expansion.

4. Energy and Cooling Limitations

Power availability and thermal management have become critical bottlenecks for next-generation data center design.

AI Data Center Market Outlook (2026–2032)

The AI data center ecosystem is expected to experience sustained expansion over the next decade, driven by:

- Large-scale AI model training clusters

- Enterprise AI deployment at global scale

- Expansion of edge AI infrastructure networks

- Growth in sovereign AI infrastructure programs

Emerging infrastructure trends include:

- Liquid-cooled GPU server farms

- AI-optimized semiconductor architectures

- Hybrid cloud-edge compute models

- Modular hyperscale data center design

These developments are redefining how digital infrastructure is designed, financed, and operated.

Industry Implications

Cloud Providers: The Acceleration of AI-Native Infrastructure

The rapid expansion of artificial intelligence workloads is fundamentally reshaping the competitive dynamics among hyperscale cloud providers. Major platforms such as Amazon Web Services, Google Cloud, and Microsoft Azure are entering a new phase of infrastructure evolution moving beyond traditional cloud computing into AI-native infrastructure ecosystems.

Rather than treating AI workloads as an extension of existing services, hyperscalers are now building dedicated AI supercomputing layers optimized for:

- Large-scale training of foundation models

- High-throughput inference serving

- GPU cluster orchestration at global scale

- Low-latency distributed AI applications

This shift is driving unprecedented capital expenditure cycles, with cloud providers investing heavily in:

- Custom AI data center architecture

- Advanced GPU fleet expansion

- High-bandwidth networking fabrics

- AI-optimized storage systems

As a result, cloud competition is no longer defined by storage or compute alone, but by who can deliver the most scalable and cost-efficient AI compute ecosystem.

Semiconductor Industry: The AI Hardware Supercycle

The semiconductor industry is experiencing a structural demand surge driven by the exponential growth of AI workloads. The increasing complexity of models requires significantly more compute density, fueling demand for:

- Next-generation GPUs (graphics processing units)

- High-Bandwidth Memory (HBM3 and beyond)

- Custom AI accelerators and inference chips

- Advanced packaging technologies such as chiplets and 3D stacking

Leading chip manufacturers, particularly NVIDIA, have become central to the AI ecosystem due to their dominance in GPU architecture and AI compute acceleration.

At the same time, cloud providers and AI companies are increasingly developing in-house silicon solutions to reduce dependency on external supply chains. This includes:

- Custom AI chips for inference optimization

- Proprietary training accelerators

- Energy-efficient edge AI processors

This dual-track evolution GPU dominance combined with custom silicon development is creating a long-term AI hardware supercycle, where demand consistently outpaces supply across multiple semiconductor layers.

Energy Sector: AI as a New Structural Power Demand Driver

AI data centers are rapidly emerging as one of the most significant new sources of global electricity demand. Unlike traditional cloud workloads, AI training and inference operations require:

- Continuous high-density power consumption

- Advanced cooling infrastructure (liquid cooling, immersion systems)

- Stable low-latency power delivery systems

- Large-scale grid interconnection capacity

This has transformed AI infrastructure into a critical energy planning variable for utilities and governments worldwide.

Key implications include:

Grid Expansion Pressure

Electric utilities are accelerating investments in transmission infrastructure to support hyperscale AI campuses.

Renewable Energy Integration

Many data center operators are securing long-term renewable energy contracts (solar, wind, hydro) to stabilize energy costs and meet sustainability targets.

Thermal Efficiency Innovation

Next-generation AI facilities are adopting advanced cooling technologies to reduce energy waste and improve compute efficiency per watt.

As AI workloads scale, electricity demand from data centers is expected to become a structural driver of global energy markets, comparable to industrial manufacturing sectors.

Investment Landscape: AI Infrastructure as a Core Institutional Asset Class

AI infrastructure is increasingly being recognized as a strategic, long-duration investment class with strong secular growth characteristics. Institutional investors are expanding exposure across multiple segments of the AI ecosystem, including:

Data Center Real Estate Investment Trusts (REITs)

Investors are allocating capital to large-scale data center operators due to stable long-term lease structures and growing demand from hyperscalers and AI companies.

GPU and Compute Infrastructure Firms

Companies specializing in GPU cloud services, AI hosting, and compute marketplaces are attracting significant venture capital and private equity investment.

Cloud Ecosystem Expansion

Strategic investments in hyperscaler ecosystems are viewed as indirect exposure to AI compute demand growth.

Energy-Linked Infrastructure Assets

Energy producers, grid operators, and power infrastructure companies are increasingly tied to AI data center expansion cycles.

This convergence of technology, energy, and real estate is creating a multi-layered AI infrastructure investment ecosystem, where returns are driven by long-term compute demand rather than short-term software cycles.

Strategic Outlook: Compute as the New Competitive Moat

The AI industry is entering a phase where compute access is becoming a primary competitive differentiator. Companies capable of securing scalable, reliable, and energy-efficient infrastructure are positioned to lead the next wave of AI innovation.

Anthropic’s expansion strategy reflects this shift, highlighting the growing importance of infrastructure control in determining model capability, deployment speed, and market reach.

This evolution marks a transition from software-centric competition to infrastructure-driven AI economics.

Why are AI data centers expanding rapidly in 2026?

AI data centers are expanding rapidly due to increasing demand for generative AI models, rising GPU consumption, hyperscaler infrastructure investments, and enterprise adoption of AI-powered applications. Companies like Anthropic are scaling compute infrastructure globally to support advanced model training and deployment requirements.

Conclusion

The expansion of AI data center infrastructure marks a defining moment in the evolution of artificial intelligence. As Anthropic and other leading AI organizations scale their global compute footprint, the industry is transitioning into a new era where infrastructure capability not just algorithmic innovation determines competitive advantage.

The next decade of AI growth will be shaped by those who control the most scalable, efficient, and resilient compute ecosystems.

News source: https://www.cnbc.com/2026/06/25/anthropic-global-ai-data-center-push.html