LoRa and LoRaWAN IoT Market Overview

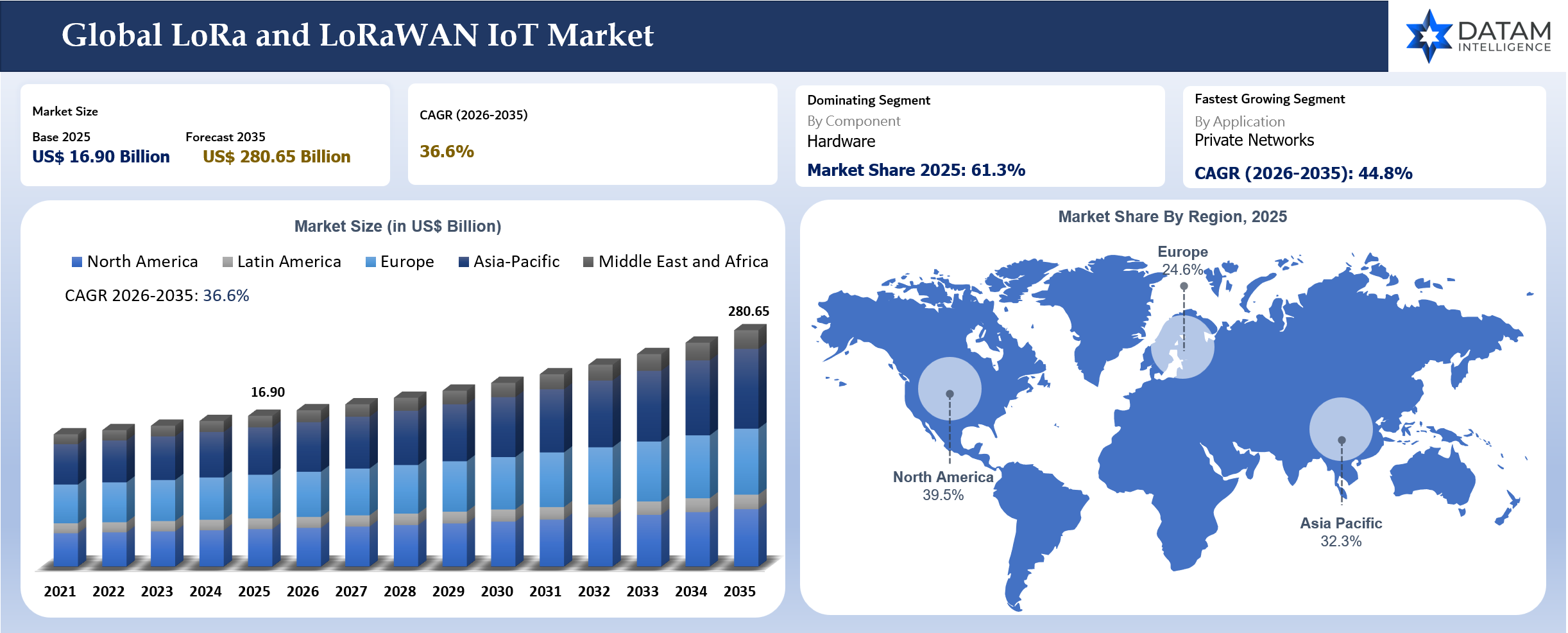

The global LoRa and LoRaWAN IoT market reached US$ 16.90 billion in 2025 and is expected to reach US$ 280.65 billion by 2035, growing at a CAGR of 36.6% during 2026 to 2035.Commercial demand is strongest where cellular connectivity is too expensive, Wi-Fi coverage is impractical and manual field inspection is costly. Smart water meters, gas meters, leak sensors, soil monitors, temperature sensors, asset trackers, waste-bin sensors, indoor air quality devices and industrial monitors have strong demand because they need long battery life rather than high bandwidth. LoRaWAN is therefore gaining demand in utility-scale and private-network deployments where thousands of devices must operate reliably for years.

Customers are moving from trials toward operational rollouts. Earlier adoption focused on proof-of-concept projects in smart cities, campuses and buildings. Current procurement is more disciplined and focuses on gateway density, indoor penetration, certification, battery life, cloud integration, device provisioning, security and field maintenance cost. The strongest market opportunities are now tied to measurable operational savings such as fewer truck rolls, lower water losses, reduced manual meter reading, better facility monitoring and more reliable asset visibility.

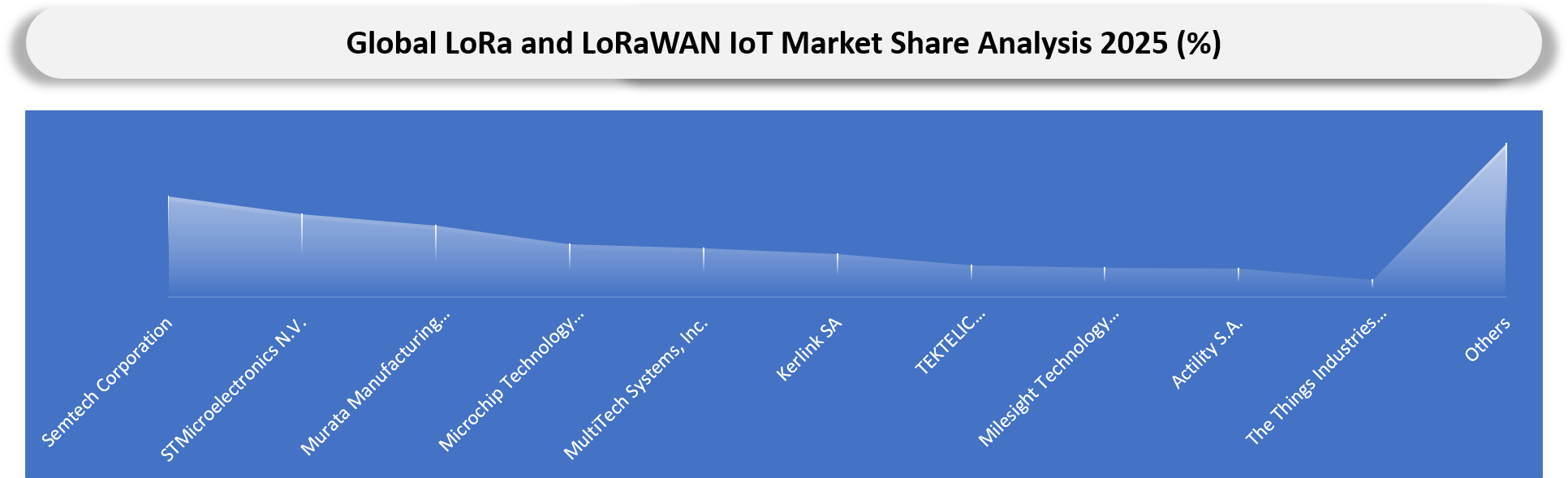

Supplier competition is spread across chipsets, modules, gateways, sensors, trackers, network servers, network operators and system integrators. Semtech remains central because LoRa technology underpins the ecosystem, while STMicroelectronics, Murata, Microchip, Kerlink, MultiTech, TEKTELIC, Milesight, Actility, The Things Industries, Senet, Everynet and UnaBiz compete across different layers. The market is no longer only about connectivity hardware. Value is shifting toward certified devices, private network design, application integration, data analytics and lifecycle device management.

Key Takeaways

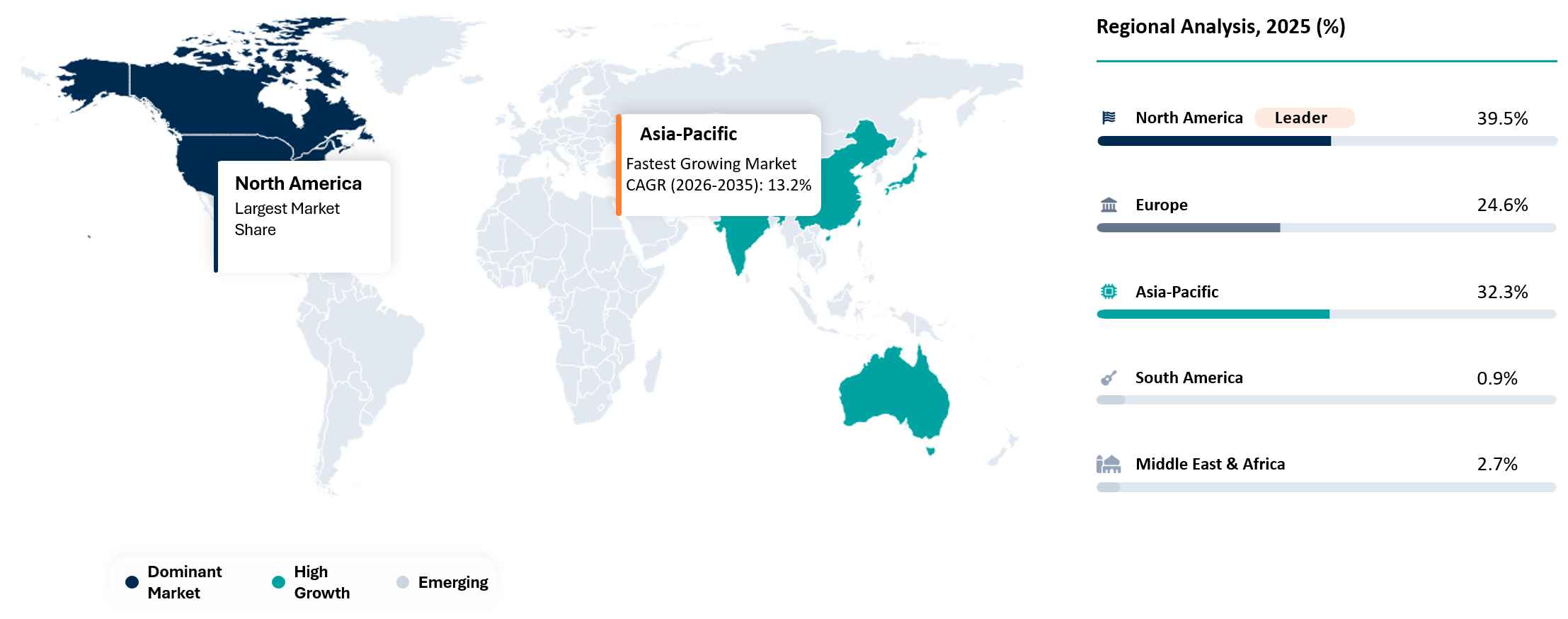

- North America dominated the market with 39.5% share in 2025, supported by private LoRaWAN networks, water utility monitoring, smart buildings, logistics tracking and industrial IoT deployments.

- Asia-Pacific is the fastest-growing region with a CAGR of 42.4% and is expected to become the largest regional market by 2035 with 46.8% share, supported by smart metering, smart city infrastructure, agriculture digitization and utility modernization.

- Europe represented 24.6% share in 2025, supported by smart metering, energy efficiency programs, city infrastructure monitoring and a mature LoRaWAN ecosystem.

- Hardware remains the leading component because large deployments require end nodes, sensors, gateways, modules, chipsets, trackers and meters before recurring software and services scale.

- Private LoRaWAN networks are expected to grow fastest as utilities, factories, campuses, ports and municipalities seek stronger control over coverage, device data and lifecycle cost.

- Smart metering remains the leading application because water, gas and electricity utilities need low-power devices that reduce manual reading, improve billing accuracy and detect leaks or abnormal usage.

- Supplier differentiation is moving toward certified devices, battery-life evidence, gateway planning, private network expertise, network server reliability and application integration.

Market Scope

| Metrics | Details | |

| Market Size In 2025 | US$ 16.90 Billion | |

| Market Size By 2035 | US$ 280.65 Billion | |

| CAGR During 2026 To 2035 | 36.6% | |

| Largest Region In 2025 | North America, 39.5% market share in 2025 | |

| Fastest Growing Region | Asia-Pacific, 42.2% CAGR between 2026 and 2035 | |

| Key Regional Shift | Asia-Pacific is expected to increase from 32.3% market share in 2025 to 46.8% market share by 2035 | |

| Leading Component | Hardware | |

| Fastest Growing Network Type | Private LoRaWAN Network | |

| Leading Application | Smart Metering | |

| Fastest Growing Application | Smart Water Network Monitoring | |

| Market Maturity | High-Growth Stage | |

| Key Buying Question | Which deployment model can reduce battery replacement, field visits and connectivity cost across large sensor fleets? | |

| By Component | Hardware, Software, Services | |

| By Network Type | Public Network, Private Network, Hybrid Network, Community Network, Satellite-Enabled Network | |

| By Deployment Model | Indoor Deployment, Outdoor Deployment, Industrial Deployment, Utility-Scale Deployment, Agricultural Deployment | |

| By Application | Smart Metering, Smart Buildings, Smart Cities, Asset Tracking, Smart Agriculture, Industrial Monitoring, Environmental Monitoring, Logistics and Fleet Tracking, Smart Lighting, Waste Management, Water Network Monitoring, Others | |

| By End-User | Utilities, Agriculture, Logistics and Transportation, Industrial Manufacturing, Smart Cities and Municipalities, Commercial Buildings, Oil and Gas, Retail and Warehousing, Healthcare Facilities, Others | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

Why Does This Report Matter In 2026?

LoRa and LoRaWAN IoT matter in 2026 because organizations are no longer asking whether low-power wide-area IoT works. They are asking how to scale it economically across thousands or millions of field devices. Utilities need battery-powered meters and leak sensors that can operate in basements, meter pits and dense urban blocks. Cities need environmental, lighting, parking and waste sensors without heavy network infrastructure. Industrial sites need low-cost monitoring in locations where cabling is expensive and cellular subscriptions are not justified.

The most important 2026 shift is the move from pilot projects to network planning. A successful LoRaWAN deployment depends on gateway placement, device certification, indoor penetration, battery profile, antenna design, network server reliability and integration with utility or enterprise systems. Buyers are also reviewing whether public, private, hybrid or satellite-enabled networks provide the best lifecycle economics. A low-cost sensor can become expensive if it fails early, drains batteries quickly or cannot be integrated into the customer’s operational platform.

The report helps client’s separate hardware opportunity from software and services opportunity. Device makers compete on price, battery life and certification. Gateway suppliers compete on coverage, capacity and ruggedness. Network server providers compete on device management, security and integration. System integrators compete on deployment planning and lifecycle support. Strong market analysis must therefore assess the full ecosystem rather than only the radio technology.

Evidence Base Used For This Report

- LoRa Alliance technical and market information on LoRaWAN standard, network options, certification and vertical applications.

- Official product documentation from chipset, module, gateway, sensor and network server companies.

- Company product pages and official solution pages covering LoRa chipsets, STM32WL wireless MCUs, gateways, sensors, trackers and IoT platforms.

- Trade data indicators using HS 851762, HS 854231, HS 854239, HS 902610 and HS 902580.

- Utility, smart city, building, agriculture and industrial IoT deployment references from official organizations and ecosystem participants.

- DataM internal market model using device demand, gateway deployment, network software spending, integration services and regional adoption.

Strategic Indicators For LoRa and LoRaWAN IoT

High Regulation Impact

Regulation affects LoRa and LoRaWAN IoT through unlicensed spectrum rules, frequency bands, duty-cycle limits, device certification, utility metering rules, data protection and critical infrastructure requirements. Each region has its own radio frequency conditions, so device makers must align hardware design with local regulatory requirements. Metering and utility applications also require secure data handling and dependable device identity because billing, consumption tracking and public infrastructure monitoring are involved.

Smart metering creates the highest compliance exposure because utilities need reliable data for billing, network planning and customer service. Water and gas utilities require devices that can operate safely in field environments and transmit accurate readings without frequent visits. Electricity, gas and water metering systems also need secure provisioning, tamper protection and integration with head-end systems. Certification and interoperability reduce procurement risk when large utilities buy from multiple vendors.

Public-sector deployments face additional requirements around data ownership, privacy and system resilience. Smart city projects may capture occupancy, asset movement, environmental readings or building data that must be managed responsibly. Procurement teams increasingly ask for encryption, device authentication, secure firmware update capability and long-term vendor support. LoRaWAN suppliers that combine compliance support with certified devices can move faster through public tenders.

High Investment Activity

Investment is concentrated in smart water metering, gas metering, building sensors, asset tracking, private networks, satellite-enabled LoRaWAN, energy harvesting and industrial monitoring. Utilities are investing because manual meter reading, non-revenue water, leak response and field visits create recurring cost. Commercial building owners are deploying sensors to monitor occupancy, indoor air quality, leak detection and energy use. Industrial customers are using LoRaWAN where equipment conditions must be monitored without wiring every machine or asset.

Private network investment is rising because enterprises want stronger control over coverage and data. A factory, campus, port, utility or municipality can deploy its own gateways and manage traffic without relying fully on public network availability. This model is attractive where coverage requirements are site-specific and device density is predictable. Gateway suppliers, network server providers and system integrators benefit because private networks require planning, installation, configuration and maintenance.

Energy harvesting and battery-free IoT are becoming a new investment area. Large sensor fleets create battery replacement and disposal problems. Indoor light harvesting, vibration energy harvesting and ultra-low-power devices can reduce maintenance cost in buildings and industrial locations. The combination of energy harvesting, edge AI and LoRaWAN is expanding the addressable market for maintenance-light IoT applications.

Supply Chain Disruption

Supply-chain risk is concentrated around chipsets, wireless MCUs, modules, gateways, sensors, batteries, antennas, enclosures and certified devices. A large utility rollout can be delayed if an approved module or gateway is unavailable. Device designs are often certified around specific components, so changing suppliers during deployment can trigger testing, integration and procurement delays. Hardware availability therefore remains important even though software and services are gaining value.

Battery supply and quality create a practical field risk. Many LoRaWAN devices are sold on long-life claims, but actual life depends on battery chemistry, temperature, transmission frequency, signal quality and firmware behavior. Poor battery selection can increase replacement cost and damage project economics. Buyers are increasingly requesting field evidence rather than relying only on datasheet claims.

Gateway supply and installation planning also affect deployment speed. Utility-scale and smart city networks require rugged gateways, antennas, mounting hardware, backhaul, power and site permissions. Delays in gateway installation can slow device activation. Suppliers with local inventory, deployment partners and installation support can reduce rollout risk.

Pricing Volatility

Pricing is shaped by chipset cost, sensor type, battery specification, enclosure rating, certification, gateway capacity, antenna design, network server subscription and integration work. A simple temperature sensor may cost far less than a smart water meter or industrial pressure monitor. A rugged outdoor gateway can cost more than several hundred end devices, but poor gateway planning can create higher lifecycle cost through coverage gaps and repeat visits.

Private network projects often carry higher upfront cost because gateways, installation and network configuration must be funded by the buyer. Lifecycle cost can still be attractive when device volumes are high and public connectivity fees would become expensive. Public networks reduce upfront effort where coverage exists, but coverage and subscription cost vary by market.

Enterprise buyers are shifting from device price toward cost per connected sensor over the full device life. The real economics include battery replacement, truck rolls, device failure, data platform fees, gateway maintenance, firmware updates and integration support. Vendors that can demonstrate lower lifecycle cost will have a stronger position even when device price is not the lowest.

Procurement Pressure

Procurement teams are under pressure to move beyond pilots and prove operational payback. Utilities need lower meter-reading cost, faster leak detection and better asset visibility. Building owners need energy savings and maintenance efficiency. Industrial sites need monitoring without wiring cost. Logistics companies need asset visibility at lower cost than cellular tracking for non-powered assets.

Large buyers increasingly require certified devices, field references, battery-life evidence, security documentation and integration support. Device certification is becoming a central procurement filter because multi-vendor projects can fail when interoperability is weak. Buyers also need clear service-level responsibilities across device makers, gateway providers, network server companies and system integrators.

Procurement is also affected by internal ownership. IT, operations, facilities, utilities, sustainability and finance teams may all influence LoRaWAN buying decisions. A strong business case must translate sensor data into reduced field visits, avoided losses, better compliance, higher uptime or lower energy use. Suppliers that help build this business case can shorten sales cycles.

New Technology Adoption

Technology adoption is strongest in private LoRaWAN networks, satellite LoRaWAN, hybrid positioning, energy harvesting devices, edge AI sensors and certified device ecosystems. Private networks are expanding because enterprises want dedicated coverage and more control over device data. Satellite-enabled LoRaWAN expands the addressable market into farms, forests, pipelines, mines, remote logistics routes and environmental monitoring zones where terrestrial networks are limited.

Hybrid positioning is gaining attention in asset tracking. LoRaWAN can be combined with GNSS scanning, Wi-Fi scanning, Bluetooth Low Energy and cellular backhaul depending on accuracy and battery needs. Semtech’s LoRa Edge positioning reflects this shift because asset tracking customers often need location intelligence without the energy cost of continuous GPS.

Energy harvesting and battery-free devices are emerging as a differentiated technology layer. Battery replacement becomes expensive at scale, especially for hard-to-reach sensors. Devices powered by indoor light, vibration or other ambient energy sources can expand adoption in buildings, warehouses and industrial sites when data transmission remains low power.

Regional Expansion Opportunity

Asia-Pacific offers the largest and fastest growth opportunity because China, India, Japan, South Korea and Southeast Asia are deploying smart meters, smart cities, industrial monitoring and agriculture digitization. India is especially relevant for water metering, city infrastructure and agriculture monitoring because large field networks need low-cost connectivity. Japan is attractive for utility monitoring, building automation, disaster prevention and industrial quality systems.

Europe remains a mature and innovation-led region. Smart utility programs, building energy efficiency, environmental monitoring and city infrastructure support LoRaWAN adoption. European demand is also supported by strong ecosystem players across gateways, network servers and metering. Regulatory pressure around remote meter reading and energy efficiency strengthens smart utility use cases.

North America offers strong demand in private networks, smart buildings, water utilities, campuses, logistics and industrial IoT. Public network availability varies, so private and hybrid networks are important. Buyers focus heavily on integration, security and operational return. Suppliers with system integrator partnerships can scale more effectively.

Government Policy Support

Government policy supports LoRaWAN demand through smart city programs, water-loss reduction initiatives, utility modernization, agriculture digitization, environmental monitoring and public infrastructure upgrades. Municipalities need affordable sensors for water networks, streetlights, parking, waste bins, public buildings and air quality. Low-power wide-area networks reduce the cost of connecting these distributed assets.

Utility modernization policies are especially important. Remote meter reading, leak detection and pressure monitoring can reduce losses and improve service quality. Water scarcity and aging infrastructure are pushing cities to monitor distribution networks more closely. LoRaWAN is attractive where devices must operate for many years with limited maintenance.

Agriculture and environmental programs also create opportunity. Soil moisture, weather, irrigation, flood monitoring and livestock tracking can support better resource use. Government-backed rural digitization programs can help accelerate adoption where private buyers alone may not justify early network investment.

Company Coverage Preview

Semtech Corporation is the most influential technology owner in the LoRa ecosystem because LoRa chipsets and radio technology form the foundation for many LoRaWAN devices. The company’s LoRa Connect portfolio supports long-range and low-power communication between IoT devices and gateways, while LoRa Edge extends the value proposition into asset tracking and geolocation. Semtech’s role is strategic because chipset availability, reference designs and ecosystem partnerships influence the pace of device development across metering, logistics, industrial monitoring and smart buildings.

STMicroelectronics is important because its STM32WL series combines a low-power microcontroller and sub-GHz radio in one product family. The series supports LoRaWAN and other low-power wireless protocols, which helps device makers simplify design and reduce PCB footprint. STM32WL modules and reference designs are relevant for metering, smart logistics, building sensors and industrial IoT products where embedded security, low power and regional regulatory compliance matter.

Actility, The Things Industries, OrbiWise, Senet, Everynet and UnaBiz are central to the software and network layer. Their platforms support device provisioning, network servers, public or private network management, routing and integration into customer applications. These companies are important because large IoT deployments fail when device data cannot be managed reliably. Network software and operating services create recurring value after hardware is installed.

Gateway and device companies such as Kerlink, TEKTELIC, MultiTech, Milesight, Seeed, MOKO, Dragino, Murata, Microchip, Advantech and Laird Connectivity compete by serving specific deployment needs. Gateways must handle outdoor conditions, backhaul and dense traffic. Sensors and trackers must balance cost, battery life, enclosure design and certification. The winning suppliers will be those that combine hardware reliability with easy integration and field support.

AI Impact Analysis

AI impact in LoRa and LoRaWAN IoT is strongest after field data is collected. LoRaWAN devices typically send small data packets such as meter readings, leak alerts, temperature readings, soil moisture, vibration signals and asset movement events. AI can turn these signals into operational decisions such as leak prioritization, preventive maintenance, energy optimization and route planning. The technology does not need high bandwidth to create value when the right data is captured consistently.

Smart utilities can use AI to detect abnormal consumption, identify likely leaks, prioritize field repair and improve demand forecasting. Water utilities benefit when sensor signals from meters, pressure monitors and leak detectors are combined with operational history. The economic value comes from reduced water loss, fewer emergency repairs and better asset planning. LoRaWAN provides the low-power data collection layer, while AI improves interpretation.

Smart buildings can use AI to analyze occupancy, indoor air quality, temperature, humidity and energy patterns from LoRaWAN sensors. Facility teams can adjust HVAC, cleaning and space planning based on actual use. Battery-powered sensors make retrofits easier in older buildings because wiring is often expensive or disruptive. AI improves payback when sensor data is tied to energy savings or maintenance actions.

Industrial users can apply AI to vibration, temperature, level and environmental data collected from remote assets. Predictive alerts can reduce downtime when monitoring equipment that previously had no connectivity. LoRaWAN is not suitable for high-frequency machine vision or real-time control, but it is valuable for periodic asset condition signals. The strongest AI value will come from combining low-power sensors with analytics that reduce maintenance cost.

Disruption Analysis

Market disruption is coming from private LoRaWAN networks, utility-scale sensor rollouts, energy harvesting and satellite-enabled low-power IoT. Enterprises no longer need to wait for national public network coverage when a private network can be planned around a campus, factory, city or utility service territory. Private networks change the economics because the customer can control gateway placement, data routing and coverage expansion.

Battery-free and energy harvesting devices are also changing the deployment model. Large sensor networks can become expensive when battery replacement is required every few years. Energy harvesting reduces maintenance burden and supports devices in hard-to-reach spaces such as ceilings, walls, storage zones, equipment rooms and industrial sites. The combination of LoRaWAN, energy harvesting and edge AI can open new categories of maintenance-light IoT.

Satellite-enabled LoRaWAN extends the technology into remote environments. Agriculture, mining, forestry, pipelines, disaster monitoring and logistics routes often lack reliable terrestrial coverage. Satellite connectivity can make low-power devices practical in regions where cellular networks are unavailable or too expensive. Adoption will depend on subscription cost, message frequency and device power budget.

Competition from NB-IoT, LTE-M, Wi-Fi HaLow, Bluetooth Low Energy and proprietary RF systems remains important. LoRaWAN will not replace every IoT connectivity option. It will remain strongest where devices send small messages, need long battery life and operate over wide areas. Technology selection will depend on data rate, latency, mobility, coverage, ownership model and lifecycle cost.

BCG Matrix: Company Evaluation

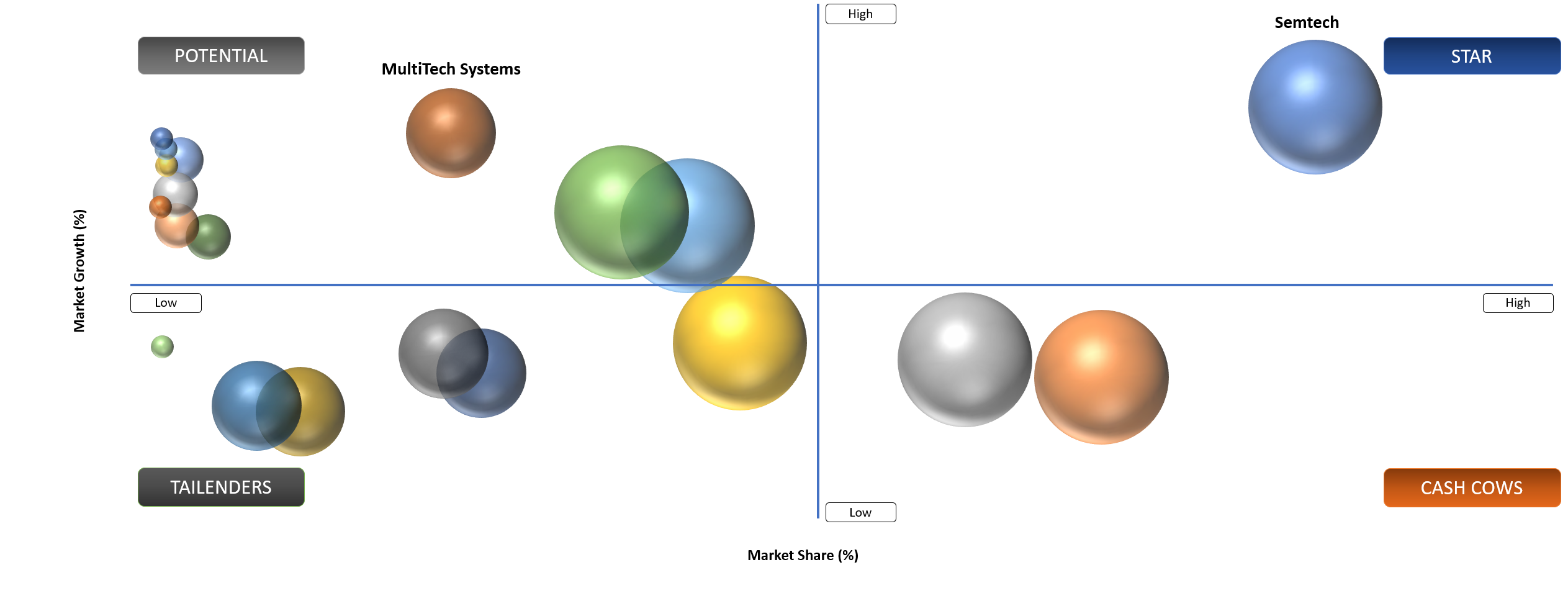

Star

Star players include Semtech, STMicroelectronics, Murata, Microchip, MultiTech, Kerlink, TEKTELIC, Actility, The Things Industries, Senet and Everynet. These companies support core ecosystem layers such as chipsets, wireless MCUs, modules, gateways, network servers and network operations. Strong players benefit from certification, technical depth, proven deployments and multi-industry customer access.

Potential

Potential players include private network integrators, energy harvesting device developers, satellite LoRaWAN providers, smart water solution companies and hybrid asset tracking specialists. These companies can grow quickly by solving specific operational problems rather than selling connectivity alone. Growth depends on field validation, integration capability, channel partnerships, and ability to prove savings from reduced manual work or lower battery maintenance.

Market Dynamics

Driver Impact Analysis

| Driver | Market Growth Impact | Demand Concentration | Impacted Use Case | Strategic Impact |

Utilities need low-power smart metering and leak monitoring | 4.2% | Europe, China, India, Japan and North America | Smart water, gas and electricity metering | Supports large device rollouts and recurring platform revenue |

Private networks reduce dependency on public coverage | 3.6% | Industrial campuses, utilities, ports and smart cities | Dedicated LoRaWAN networks | Increases gateway, network server and integration demand |

Battery replacement cost drives long-life sensor adoption | 3.1% | Smart buildings, utilities and agriculture | Low-maintenance sensors | Strengthens lifecycle cost argument |

Asset tracking requires lower-cost location visibility | 2.7% | Logistics, warehouses and industrial yards | Trackers and hybrid location devices | Expands demand beyond static sensors |

Smart Metering and Water Network Monitoring Need Low-Power Coverage

Smart metering is the most powerful commercial driver because meter readings are low-data, periodic and widely distributed. Water and gas meters are often installed in basements, pits and dense urban areas where conventional connectivity can struggle. LoRaWAN’s long-range and low-power profile fits this requirement because devices can transmit small packets without frequent battery replacement.

Water utilities create especially strong demand. Non-revenue water, leak detection and pressure monitoring are operational pain points in many cities. Manual meter reading is costly and often delayed, while leaks can remain hidden for long periods. LoRaWAN-enabled meters and leak sensors can improve visibility without requiring dense powered infrastructure. Utility buyers value the ability to reduce field visits and prioritize repairs.

Smart metering also benefits from network reuse. A LoRaWAN network built for water meters can support additional applications such as pressure sensors, street lighting, waste monitoring, environmental sensors and building sensors. Cities and utilities can therefore build a broader digital infrastructure layer from one network investment. This improves the business case for gateways and network servers.

Procurement will increasingly favor certified and field-tested devices. A meter expected to operate for many years cannot rely on unproven battery claims or weak integration. Utilities need device certification, rugged enclosures, secure provisioning, firmware update support and clear installation guidance. Suppliers that understand utility operations will capture more value than low-cost device sellers.

Restraint Impact Analysis

| Restraint | Drag On Market Growth | Primary Impact Area | Impacted Use Case | Strategic Impact |

| Fragmented network coverage limits national rollouts | 3.4% | Public network projects | Smart cities, logistics and utilities | Pushes buyers toward private or hybrid networks |

| Battery life claims vary from field performance | 2.8% | End devices and sensors | Utility meters, trackers and building sensors | Raises demand for field validation |

| Integration complexity slows enterprise adoption | 2.6% | Software and services | Smart buildings, industrial sites and utilities | Strengthens role of system integrators |

| Low data rate limits high-bandwidth applications | 2.2% | Application scope | Video, voice and real-time control | Keeps LoRaWAN focused on low-data use cases |

Fragmented Coverage and Integration Complexity Slow Scaling

Fragmented network coverage is the most visible restraint because public LoRaWAN availability varies by country, city and operator. A device that works well in one location may need private gateways in another. This creates complexity for logistics companies, utilities and multinational enterprises that want consistent coverage across multiple sites or regions.

Private networks solve coverage issues but add design and ownership responsibility. Buyers must plan gateway locations, backhaul, mounting, security, device onboarding and maintenance. Smaller organizations may lack the technical resources to manage this transition. System integrators and managed network providers can reduce the burden but add cost.

Integration is often harder than sensor installation. A utility does not only need a meter reading. It needs data inside billing, asset management and maintenance systems. A building owner needs sensor data inside energy and facility platforms. An industrial user needs alerts inside maintenance workflows. Weak integration can turn a successful device pilot into a stalled enterprise rollout.

Low data rate also limits the market. LoRaWAN is not designed for continuous video, voice or high-frequency telemetry. Buyers must match the technology to the right use case. The market grows best when suppliers clearly position LoRaWAN for periodic sensing, alerts, monitoring and asset events rather than trying to present it as a universal IoT connectivity layer.

Segmentation Analysis

Hardware Will Continue To Dominate Initial Deployment Spend

Hardware will continue to dominate market spending because every LoRaWAN rollout requires end devices, sensors, modules, gateways, antennas and installation materials before recurring software revenue can scale. Large utility and smart city deployments can involve thousands or millions of field devices. Even when platform software becomes more strategic, hardware remains the largest first-phase spending layer.

End devices represent the most visible hardware opportunity. Smart meters, leak sensors, environmental sensors, asset trackers and industrial monitors are purchased based on use case, enclosure design, battery profile, certification and price. A device installed in a meter pit must survive different conditions than a sensor installed in an office building. Application-specific hardware design is therefore essential.

Gateways are smaller in volume but critical in value. One gateway can serve many devices, but poor placement can create weak coverage and higher maintenance cost. Outdoor gateways need rugged design, backhaul options and power planning. Industrial gateways may need higher reliability and security. Gateway suppliers that support site planning and installation partners can defend stronger pricing.

Modules and chipsets create the enabling layer. Device makers use LoRa chipsets, wireless MCUs and certified modules to reduce development time. Integrated modules and reference designs can accelerate market entry because RF design and certification are complex. Semiconductor suppliers influence the pace of innovation because device cost, power consumption and regional band support begin at the component level.

Smart Metering Will Continue To Lead Application Demand

Smart metering will continue to lead because utility meter data fits LoRaWAN’s strengths. Water, gas and electricity meters usually send small messages at defined intervals. Long battery life, deep indoor coverage and low data cost are more important than high throughput. This makes smart metering one of the most scalable LoRaWAN opportunities.

Water metering is especially attractive. Many water utilities face aging infrastructure, leakage, inaccurate billing and high manual reading cost. Smart meters and pressure sensors help identify abnormal consumption and network losses. The commercial value becomes clear when fewer truck rolls and faster leak detection reduce operating cost.

Gas metering also supports LoRaWAN adoption where safety, battery life and remote reading matter. Gas meters are distributed across homes, businesses and industrial sites and may be difficult to access manually. Utility buyers require secure communication and reliable long-term operation because meter replacement cycles are lengthy.

Electricity metering can use multiple communication technologies depending on country and grid architecture. LoRaWAN is more likely to be used in selected submetering, building, rural or utility monitoring use cases rather than every national electricity meter rollout. The strongest opportunities appear where low-power wireless connectivity and private network control are more valuable than high-bandwidth grid communication.

Smart Buildings Are Expanding Through Energy and Occupancy Use Cases

Smart buildings represent a strong growth segment because LoRaWAN sensors can be deployed without wiring across offices, hospitals, campuses, hotels and public buildings. Occupancy, temperature, humidity, air quality, leak detection and space utilization sensors can improve facility operations. Retrofit projects are especially attractive because existing buildings often cannot justify wired sensor installation.

Energy optimization is a practical driver. Building owners need better data to reduce heating, cooling and lighting waste. Battery-powered sensors can identify unused spaces, abnormal temperature zones, water leaks or poor air quality. When connected to facility management platforms, sensor data can support measurable savings.

Facility teams also value low maintenance. A sensor network becomes expensive if batteries fail often or devices lose connectivity. LoRaWAN’s long battery life and wide coverage help reduce operating burden. Procurement teams still need field proof because indoor walls, basements and equipment rooms can affect actual performance.

Smart buildings also benefit from private networks. A campus or commercial property owner can install gateways to cover multiple buildings and support additional use cases over time. Water leak detection, indoor air quality, asset tracking and occupancy analytics can share the same network infrastructure. This improves return on gateway investment.

Asset Tracking Is Moving Toward Hybrid Location Models

Asset tracking is gaining demand in logistics, warehousing, ports, industrial yards and equipment rental. Many assets do not need real-time cellular tracking every second. They need periodic location, movement or condition updates at lower cost and longer battery life. LoRaWAN fits non-powered assets that move within defined locations or across supported network zones.

Hybrid positioning is becoming more important because LoRaWAN alone may not provide the location precision required for every use case. Trackers can combine LoRaWAN with GNSS scanning, Wi-Fi scanning, Bluetooth Low Energy or QR-based processes. Semtech’s LoRa Edge positioning reflects this market need by combining connectivity with geolocation capability.

Industrial sites can use asset tracking to locate tools, containers, pallets, vehicles and safety equipment. Ports and warehouses can reduce search time and improve utilization. Logistics companies can monitor conditions such as temperature, shock or door opening where full cellular tracking is not necessary.

The commercial opportunity depends on platform integration. Buyers need dashboards, alerts and workflow triggers, not just location pings. Suppliers that combine trackers, gateways, network software and analytics will capture more value than device-only vendors.

Market Segmentation

- By Component

- Hardware

- End Nodes

- Sensors

- Gateways

- Modules

- Chipsets

- Antennas

- Trackers

- Meters

- Others

- Software

- Network Server

- Device Management Platform

- Application Enablement Platform

- Analytics Software

- Security Software

- Others

- Services

- Consulting

- Network Planning

- Installation and Integration

- Managed Network Services

- Device Certification Support

- Maintenance and Support

- Others

- Hardware

- By Network Type

- Public Network

- Private Network

- Hybrid Network

- Community Network

- Satellite-Enabled Network

- By Deployment Model

- Indoor Deployment

- Outdoor Deployment

- Industrial Deployment

- Utility-Scale Deployment

- Agricultural Deployment

- By Application

- Smart Metering

- Smart Buildings

- Smart Cities

- Asset Tracking

- Smart Agriculture

- Industrial Monitoring

- Environmental Monitoring

- Logistics and Fleet Tracking

- Smart Lighting

- Waste Management

- Water Network Monitoring

- Others

- By End-User

- Utilities

- Agriculture

- Logistics and Transportation

- Industrial Manufacturing

- Smart Cities and Municipalities

- Commercial Buildings

- Oil and Gas

- Retail and Warehousing

- Healthcare Facilities

- Others

Geographical Penetration

Asia-Pacific LoRa and LoRaWAN IoT Market Trends

Asia-Pacific led the market in 2025 because the region combines high device manufacturing capacity, large utility needs, smart city investment and industrial digitization. China has strong electronics and IoT manufacturing scale, while India offers large future demand in water metering, city infrastructure and agriculture monitoring. Japan and South Korea add high-value opportunities in smart buildings, industrial monitoring and utility reliability.

China’s opportunity is broad because smart city and industrial IoT adoption are supported by manufacturing capacity and dense urban infrastructure needs. Local device makers can produce sensors, gateways, meters and modules at scale. Competitive intensity is high, but deployment volume is attractive. LoRaWAN competes with NB-IoT and other domestic connectivity options, so use-case selection matters.

Southeast Asia offers strong potential in water utilities, logistics, agriculture and urban infrastructure. Many countries need cost-effective monitoring for assets spread across wide areas. LoRaWAN can support use cases where manual inspection is costly and cellular subscriptions are difficult to justify. Market growth will depend on local system integrators and network availability.

Asia-Pacific buyers are likely to favor practical economics over technology branding. Projects will scale when device cost, battery life, network coverage and integration produce measurable savings. Suppliers that offer local support, certified devices and deployment planning will outperform vendors selling generic sensors.

U.S. LoRa and LoRaWAN IoT Market Landscape

The U.S. market is shaped by private networks, smart buildings, water utilities, industrial campuses, logistics and environmental monitoring. Public network coverage varies by area, so many enterprise buyers evaluate private or hybrid deployments. This creates demand for gateways, network servers, integrators and managed network services.

Water utilities represent one of the most practical U.S. opportunities. Aging water infrastructure and non-revenue water create pressure to improve monitoring. LoRaWAN can support meters, leak sensors and pressure monitors where long battery life and deep coverage matter. Procurement decisions depend on field trials, meter integration and system reliability.

Smart buildings and campuses are another strong use case. Commercial properties, universities, hospitals and industrial campuses can deploy private networks to support occupancy, leak detection, air quality and asset tracking. Wireless retrofits are attractive because wiring costs can be high in existing buildings.

Logistics and industrial asset tracking are gaining traction where companies need visibility without the recurring cost of cellular for every asset. LoRaWAN is best suited to periodic updates, site-level visibility and condition monitoring. Suppliers need to connect device data into warehouse, yard management and maintenance systems to create value.

India LoRa and LoRaWAN IoT Market Landscape

India is one of the most attractive future markets because smart city needs, water losses, agriculture digitization and utility modernization create large-scale monitoring requirements. LoRaWAN can support low-cost connectivity for meters, soil sensors, weather stations, waste bins, lighting and industrial assets. The strongest opportunity lies in use cases where field visits are costly and data frequency is modest.

Water utilities and municipal bodies are key buyers. Urban water networks need leak detection, pressure monitoring and better consumption data. A LoRaWAN network can be deployed across city zones and reused for additional municipal services. Procurement will depend on device affordability, gateway planning and integration with municipal platforms.

Agriculture offers long-term demand. Soil moisture, irrigation control, weather monitoring and livestock tracking require low-cost field sensors with long battery life. Connectivity must work across rural areas where cellular may be expensive or inconsistent. LoRaWAN can be a strong fit when cooperatives, agritech companies or government-backed programs support deployment.

India also has a growing base of IoT solution providers and electronics manufacturers. Local assembly and system integration can lower cost and improve support. However, large projects need stronger standards, certification discipline and service models. Successful suppliers will combine technology with deployment execution.

Japan LoRa and LoRaWAN IoT Market Outlook

Japan is a high-value market because customers prioritize reliability, quality, documentation and long-term performance. Smart buildings, utilities, industrial monitoring, disaster prevention and asset tracking are relevant use cases. Japanese buyers are cautious but can become loyal once a solution proves reliable.

Disaster monitoring and environmental sensing are practical opportunities. Flood, landslide, water-level and infrastructure monitoring require sensors in distributed and sometimes difficult locations. LoRaWAN can support these use cases where low power and long range are more important than high bandwidth.

Industrial and building applications are also attractive. Japanese factories and commercial facilities often value predictive maintenance, energy efficiency and compact deployment. LoRaWAN sensors can support equipment rooms, storage areas, clean spaces and older buildings where wiring is difficult.

Supplier selection in Japan depends heavily on product quality, local support and compliance. Device makers with certified modules, low-power performance and strong documentation will be better positioned. Partnerships with Japanese electronics companies, utility integrators and facility management firms can accelerate adoption.

Competitive Landscape

- Competition is split across chipset suppliers, wireless MCU and module makers, gateway manufacturers, device companies, network server providers, public network operators, private network integrators and analytics platforms. No single company controls the full market because LoRaWAN deployments require a multi-layer ecosystem.

- Semtech remains the central technology anchor because LoRa chipsets and related platforms support many end devices. STMicroelectronics, Murata, Microchip and module suppliers compete by helping device makers reduce design complexity and speed time to market. Gateway companies such as Kerlink, MultiTech, TEKTELIC and Milesight compete on ruggedness, capacity, coverage and deployment support.

- Software and network companies compete on device management, network server reliability, integration, security and operating tools. Actility, The Things Industries, OrbiWise, Senet, Everynet and UnaBiz are important because large deployments require scalable provisioning, routing and lifecycle management. Software differentiation grows as device fleets expand.

- System integrators and solution providers increasingly influence vendor choice. Buyers do not want separate device, gateway and software problems. They want a working application. Competitive benchmarking should track certification, battery performance, gateway planning, integration quality, security, service support, ecosystem partnerships and proven field deployments.

Top Companies Compared By Capability

| Company | Strongest Capability | Best-Fit Customer Need |

| Semtech Corporation | LoRa chipsets, LoRa Connect and LoRa Edge platforms | Device makers and asset tracking solutions needing long-range low-power connectivity |

| STMicroelectronics N.V. | STM32WL wireless MCUs and certified modules | Embedded device developers needing integrated MCU and radio capability |

| Murata Manufacturing Co., Ltd. | Compact LoRaWAN modules | Device makers needing certified small-form-factor wireless modules |

| Microchip Technology Inc. | LoRa modules and embedded control | Industrial and embedded developers needing stable component supply |

| MultiTech Systems, Inc. | Gateways and industrial IoT connectivity | Enterprises needing gateway hardware and connectivity integration |

| Kerlink SA | Carrier-grade and industrial LoRaWAN gateways | Utilities and smart cities needing outdoor network infrastructure |

| TEKTELIC Communications Inc. | Gateways, sensors and enterprise IoT devices | Utilities, buildings and industrial customers needing complete hardware options |

| Milesight Technology Co., Ltd. | Sensors, gateways and smart building devices | Building and smart city projects needing ready-to-deploy devices |

| Actility S.A. | ThingPark network server and IoT platform | Operators and enterprises needing large-scale network management |

| The Things Industries B.V. | LoRaWAN network server and developer ecosystem | Private networks and developers needing scalable cloud network management |

Major Pain Points

- Public LoRaWAN coverage varies across countries and cities, making national rollouts difficult without private or hybrid network planning.

- Battery-life claims can differ from field performance when devices operate in poor signal areas, extreme temperatures or high-message-frequency conditions.

- Device certification gaps create interoperability risk when buyers combine sensors, gateways and network servers from multiple vendors.

- Smart utility deployments require long procurement cycles because devices must meet metering, cybersecurity and field-life requirements.

- Gateway placement directly affects coverage, indoor penetration and device battery life, making poor site planning expensive.

- LoRaWAN’s low data rate limits use in video, voice, high-frequency telemetry and real-time control applications.

- Device management becomes complex when deployments scale from hundreds of sensors to tens of thousands of devices.

- Integration with billing, maintenance, energy management and city platforms can take longer than physical device installation.

- Asset tracking requires hybrid location methods in many real-world environments because LoRaWAN connectivity alone may not provide required precision.

- Security configuration, key management and firmware update discipline become more important as LoRaWAN networks support public infrastructure.

Recent Developments

- March 2026: Browan Communications highlighted AI-powered zone-level tracking at MWC through a LoRa Alliance update, reinforcing demand for low-power location and indoor tracking solutions in enterprise IoT deployments.

- February 2026: Dracula Technologies, ASYGN and Semtech demonstrated a battery-free AI vision device connected through LoRaWAN at CES 2026, showing how energy harvesting, edge AI and low-power wide-area connectivity can reduce battery maintenance in future IoT deployments.

- December 2025: LoRaWAN was showcased at Salon des Maires 2025 in France through LoRa Alliance ecosystem activity, strengthening visibility for connected territories, smart cities and municipal infrastructure applications.

- November 2025: LoRa Alliance’s Smart Water and Energies Work Group highlighted LoRaWAN’s role in smart utilities, including large-scale water and gas metering rollouts, remote readability and utility network efficiency.

- September 2025: ZENNER reached a 10 million sensor milestone across its LoRaWAN network, supporting the commercial case for large-scale metering and smart city infrastructure deployments.

- August 2025: MClimate highlighted customer benefits of energy harvesting LoRaWAN devices through LoRa Alliance ecosystem communication, strengthening the business case for battery-light and lower-maintenance building sensor networks.

Key Procurement Priorities and Buyer Evaluation Criteria

- Utilities evaluate suppliers on meter integration, field battery life, signal penetration, device certification, cybersecurity, head-end integration and long-term service support.

- Smart city buyers prioritize gateway coverage, multi-use network potential, environmental sensor reliability, public procurement compliance and municipal platform integration.

- Building owners prioritize retrofit ease, battery life, sensor accuracy, building management system integration and lower maintenance cost.

- Industrial users prioritize rugged devices, private network reliability, asset visibility, security and integration with maintenance workflows.

- Logistics buyers prioritize tracker battery life, location accuracy, hybrid positioning capability, platform analytics and total subscription cost.

- Preferred suppliers provide certified devices, network planning, installation support, security guidance, integration services and post-deployment device management.

Analyst View and Opinion

- LoRaWAN will remain strongest in low-data, long-battery and hard-to-reach IoT use cases rather than high-bandwidth industrial automation.

- Smart metering will remain the most defensible large-scale application because meter data is periodic, distributed and expensive to collect manually.

- Private LoRaWAN networks will gain share as enterprises and utilities seek stronger control over coverage, device data and lifecycle cost.

- Public LoRaWAN networks will remain important for smart cities and shared infrastructure, but coverage fragmentation will keep private deployments relevant.

- Energy harvesting will become a stronger differentiator as large sensor fleets expose the hidden cost of battery replacement.

- Satellite-enabled LoRaWAN will expand remote monitoring in agriculture, mining, forestry, pipelines and environmental applications.

- LoRaWAN will coexist with NB-IoT, LTE-M, Wi-Fi HaLow and Bluetooth Low Energy because each technology serves different data, latency, mobility and ownership needs.

- Device certification and interoperability will become stronger procurement filters as buyers move from pilots to large operational networks.

- India can become a major growth market if smart water, municipal infrastructure and agriculture monitoring programs adopt low-cost long-life sensors.

- Supplier advantage will shift from selling hardware to delivering measurable operational outcomes such as fewer truck rolls, lower water losses and better asset utilization.

Target Audience

| Industry | Who Should Buy This Report? | Reason To Buy This Report |

| Utilities | Smart Metering Teams, Water Network Teams, Digital Grid Teams | Evaluate LoRaWAN demand for water, gas, electricity, leak monitoring and pressure sensing |

| Smart Cities | Municipal Leaders, Digital Infrastructure Teams | Identify use cases across waste, lighting, parking, environmental monitoring and public buildings |

| Agriculture | Agritech Firms, Irrigation Companies, Farm Cooperatives | Assess soil, weather, irrigation and livestock monitoring opportunities |

| Industrial Manufacturing | Plant Managers, Maintenance Leaders, Industrial IoT Teams | Understand private network and low-power monitoring use cases |

| Logistics and Warehousing | Asset Managers, Supply Chain Teams | Evaluate low-cost tracking and condition monitoring for non-powered assets |

| Building Owners | Facility Managers, Energy Teams | Assess occupancy, leak detection, air quality and energy sensor deployments |

| IoT Device Makers | Product Managers, Hardware Teams | Benchmark chipset, module, certification and application demand |

| Network Operators | IoT Business Teams | Evaluate public, private and hybrid LoRaWAN service opportunities |

| Investors | Technology Investors, Infrastructure Investors | Identify high-growth IoT hardware, software and service layers |

| Consulting Firms | ICT Strategy Teams, Utility Advisors | Support market entry, partner screening and deployment strategy |

What DataM Uniquely Provides

- DataM connects LoRa and LoRaWAN market sizing with hardware, software and services instead of treating the market as only a connectivity protocol.

- DataM maps demand by actual use case, including smart metering, water network monitoring, smart buildings, smart cities, asset tracking, agriculture and industrial monitoring.

- DataM benchmarks ecosystem players across chipsets, modules, gateways, sensors, trackers, network servers, public networks and private network integrators.

- DataM evaluates procurement risk through gateway planning, certification, battery life, device failure, platform fees and field maintenance cost.

- DataM provides import-export intelligence using HS 851762, HS 854231, HS 854239, HS 902610 and HS 902580 to support hardware trade validation.

- DataM separates public, private, hybrid, community and satellite-enabled networks so clients can evaluate deployment economics by ownership model.

- DataM identifies application-level payback drivers such as water loss reduction, truck-roll reduction, manual meter reading avoidance and asset utilization.

- DataM supports buyers with a decision framework comparing LoRaWAN against NB-IoT, LTE-M, Wi-Fi HaLow, Bluetooth Low Energy and proprietary RF options.