HDPE Nonwoven Market Overview

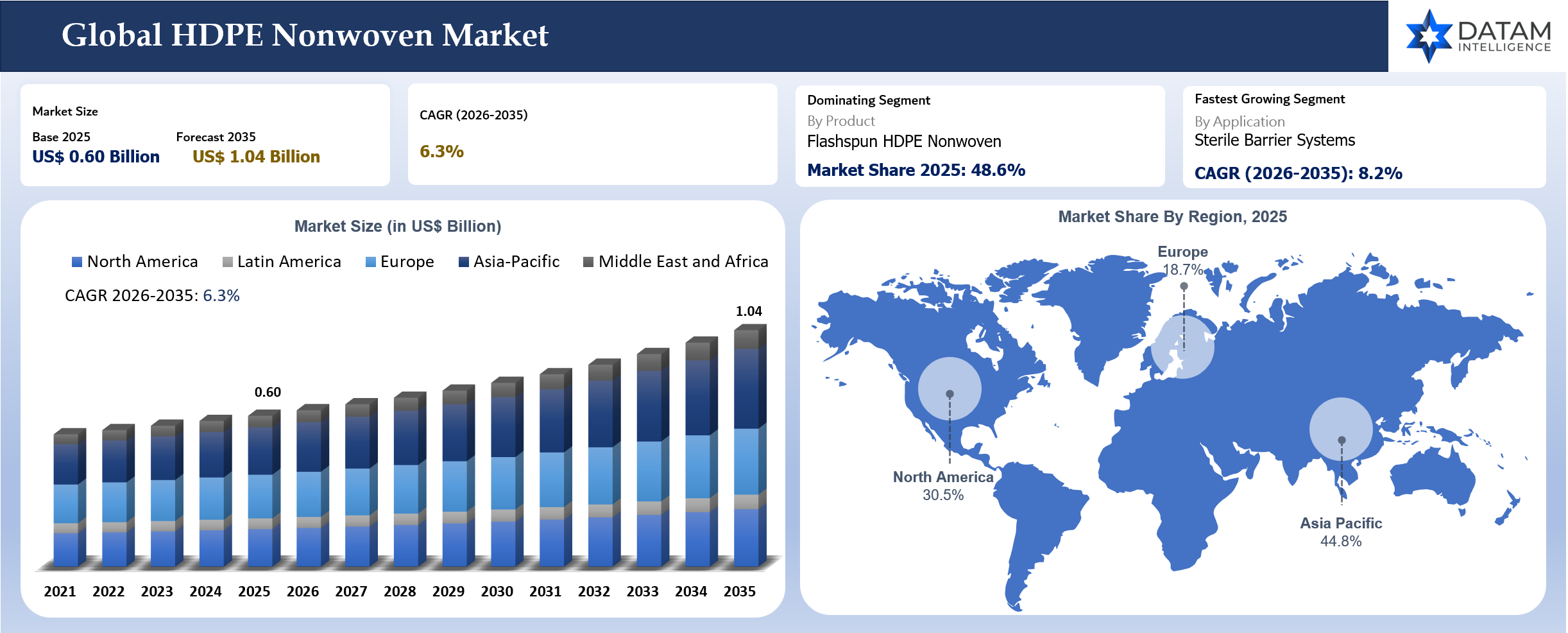

The global HDPE nonwoven market reached US$ 0.60 billion in 2025 and is expected to reach US$ 1.04 billion by 2035, growing at a CAGR of 6.3% during 2026 to 2035. Demand is concentrated in applications where material failure creates high commercial or compliance risk. Medical packaging buyers need sterile barrier materials that can support seal consistency, clean peel, microbial barrier performance and sterilization compatibility. Building envelope buyers need breathable weather barriers that can resist bulk water while supporting moisture movement through wall assemblies. Protective apparel, cleanroom supplies and industrial packaging applications also support demand where durability, low linting and barrier reliability matter more than basic roll price.

Asia-Pacific will remain the main growth engine as medical device manufacturing, pharmaceutical packaging, electronics cleanrooms, protective apparel and construction quality standards expand across China, India, Japan and South Korea. North America will continue to hold a high-value position because medical packaging qualification, building wrap brand trust and protective material performance are mature buying factors. Supplier differentiation will depend on substrate consistency, converter relationships, documentation quality, validation support and supply reliability.

Key Takeaways

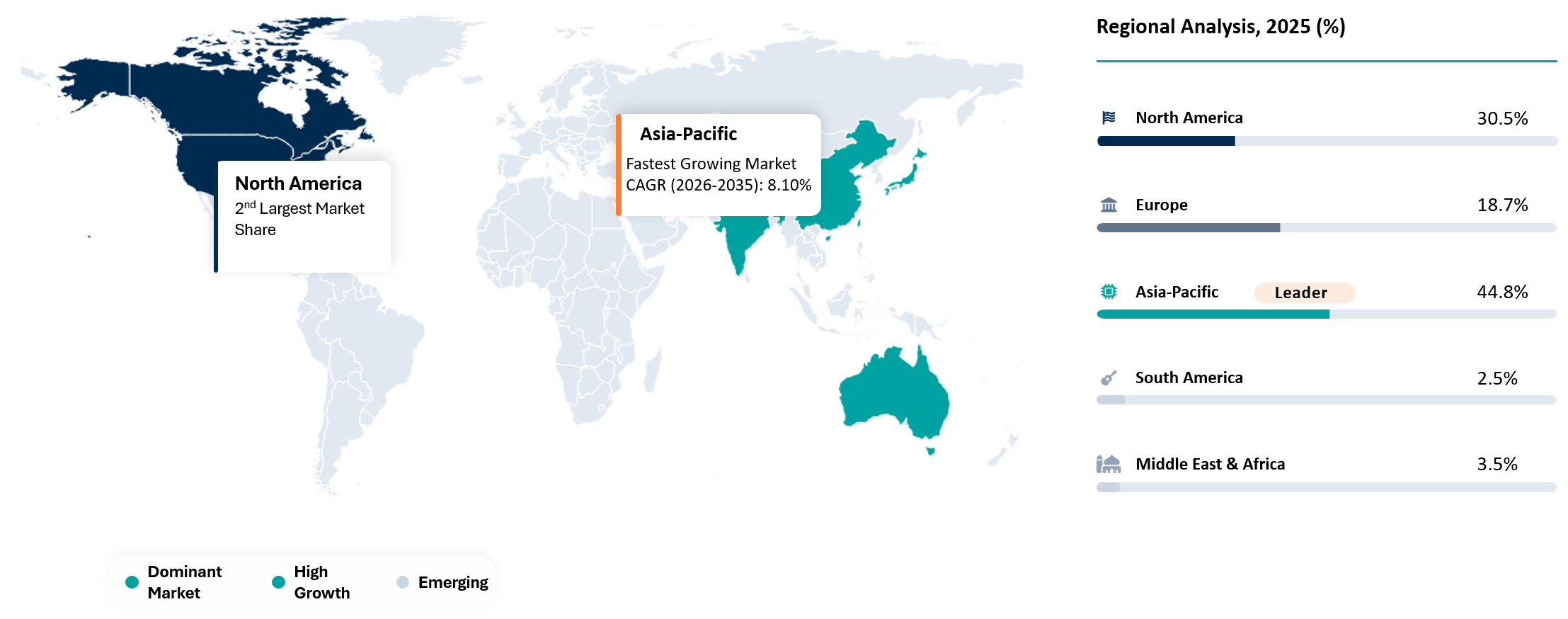

- Asia-Pacific dominated the market with 44.8% market share in 2025 and is expected to reach 52.0% market share by 2035, supported by medical device manufacturing, pharmaceutical packaging, cleanroom supply demand, electronics production and construction material upgrades.

- Asia-Pacific is also the fastest-growing region with an 8.1% CAGR between 2026 and 2035, making the region the main growth engine for HDPE nonwoven demand.

- North America represented 30.5% market share in 2025, supported by mature sterile medical packaging, Flashspun HDPE materials, protective apparel and building envelope applications.

- Flashspun HDPE nonwoven remains the leading Type because it offers a premium balance of breathability, tear resistance, water resistance, durability and barrier performance.

- Medical packaging remains the leading application because sterile barrier systems require validated substrates, seal consistency, clean peel, microbial barrier performance and sterilization compatibility.

- Sterile barrier systems are expected to be the fastest-growing application as medical device companies expand single-use devices, diagnostic consumables and home-use healthcare products.

- Supplier differentiation is moving toward medical validation support, converter relationships, substrate consistency, lot-to-lot quality, technical documentation and supply reliability.

Market Scope

| Metrics | Details | |

| Market Size In 2025 | US$ 0.60 Billion | |

| Market Size By 2035 | US$ 1.04 Billion | |

| CAGR During 2026 To 2035 | 6.3% | |

| Largest Region In 2025 | Asia-Pacific, 44.8% market share in 2025 | |

| Fastest Growing Region | Asia-Pacific, 8.1% CAGR between 2026 and 2035 | |

| Key Regional Shift | Asia-Pacific is expected to increase from 44.8% market share in 2025 to 52.0% market share by 2035 | |

| Leading Type | Flashspun HDPE Nonwoven | |

| Leading Application | Medical Packaging | |

| Fastest Growing Application | Sterile Barrier Systems | |

| Market Maturity | Growth Stage | |

| Key Buying Question | Which substrate can provide barrier performance, tear strength and qualification reliability? | |

| By Type | Flashspun HDPE Nonwoven, Spunbond HDPE Nonwoven, Composite HDPE Nonwoven, Coated HDPE Nonwoven, Laminated HDPE Nonwoven, Others | |

| By Basis Weight | Up To 40 GSM, 41 To 80 GSM, 81 To 120 GSM, Above 120 GSM | |

| By Form | Rolls, Sheets, Pouches, Envelopes, Coveralls, Tapes, Laminates, Others | |

| By Application | Medical Packaging, Protective Apparel, Building Wrap, Industrial Packaging, Graphic Media, Tags and Labels, Sterile Barrier Systems, Cleanroom Supplies, Filtration, Others | |

| By End-User | Healthcare and Medical Device Companies, Pharmaceutical Packaging Companies, Construction and Building Envelope Companies, Personal Protective Equipment Manufacturers, Industrial Packaging Companies, Printing and Graphics Companies, Cleanroom Operators, Logistics and Mailing Companies, Others | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| South America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

Why Does This Report Matter In 2026?

HDPE nonwoven demand matters in 2026 because healthcare packaging, building envelopes, cleanroom supplies and protective apparel buyers are becoming more selective about material performance. Medical device packaging cannot rely on low-cost substrates when sterile barrier performance, clean peel, seal strength and sterilization compatibility affect product release. Building wrap buyers also need materials that resist bulk water while allowing vapor movement, especially in energy-efficient wall assemblies where moisture failure can create costly claims.

The most important market shift is the move from basic nonwoven selection to validated substrate selection. Medical device companies, pharmaceutical packaging converters and sterile barrier system suppliers need materials supported by long qualification history and strong documentation. Construction buyers need a material that can survive job-site handling, wind exposure and fastening without compromising moisture control. Cleanroom buyers need low-linting and contamination-control performance that supports regulated production environments.

HDPE nonwoven suppliers are competing in a market where switching is slow. A medical packaging converter cannot easily replace an approved substrate because new validation may require seal studies, sterilization testing, aging tests and customer approvals. A building product supplier also faces brand and warranty risk if a material fails after installation. Buyers therefore evaluate more than price. Material consistency, technical support, documentation quality, converter performance and supply security are now central to procurement.

Strategic Indicators For HDPE Nonwoven

High Regulation Impact

Regulation has strong influence on HDPE nonwoven demand because the material is used in healthcare packaging, sterile barrier systems, protective apparel, cleanroom applications and building envelope products. Medical packaging requires documentation around sterile barrier integrity, seal behavior, compatibility with sterilization methods and product protection through distribution and storage. Packaging failure can delay product release, increase complaint risk and create audit exposure for medical device companies.

Building envelope products are also shaped by codes, testing standards and performance expectations. Weather-resistive barriers need to protect wall assemblies from water intrusion while allowing moisture vapor to escape. Builders and architects increasingly evaluate products through installation durability, permeability, water holdout and compatibility with tapes and flashing systems. A low-cost barrier material can create high downstream cost if moisture damage appears after occupancy.

Protective apparel and cleanroom applications face workplace safety and contamination-control expectations. Cleanroom operators need materials that reduce linting, particulate release and contamination risk. Personal protection buyers evaluate barrier performance, comfort and suitability for the exposure environment. Regulation therefore supports premium demand where validated performance is more important than lowest material cost.

High Investment Activity

Investment activity is concentrated around healthcare packaging substrates, sterile barrier systems, converter-led laminates, protective apparel, cleanroom materials and building envelope products. Medical packaging converters are improving pouching, coating, lamination and printing capabilities to serve device manufacturers that need reliable sterile barrier formats. Investment is also moving toward better quality control because seal variation, surface defects and roll inconsistency can create downstream rejection.

Packaging consolidation is an important signal. Amcor completed its combination with Berry Global in April 2025, creating a broader packaging platform with stronger scale and material science capability. This type of consolidation matters because healthcare packaging customers want suppliers that can support global production, technical development and consistent service. Larger packaging platforms can also influence converter relationships and material selection.

Asia-Pacific investment is expected to be strongest because medical device manufacturing, pharmaceutical packaging, electronics cleanrooms and construction activity are expanding across China, India, Japan and South Korea. Local converters are moving up the quality curve as export-oriented healthcare and electronics customers require better documentation and material reliability. HDPE nonwoven demand will benefit where these investments create demand for sterile packaging, cleanroom supplies and technical barriers.

Supply Chain Disruption

HDPE nonwoven supply-chain risk is linked to HDPE resin availability, flashspun capacity, nonwoven roll supply, converter capacity, sterile packaging validation and logistics. Flashspun HDPE is more concentrated than many standard spunbond and meltblown nonwoven categories, which increases buyer dependence on qualified supply. A medical device company using an approved substrate cannot switch quickly during shortage without regulatory and customer approval risk.

Resin price and availability also influence supply stability. HDPE resin is tied to petrochemical feedstock economics, energy costs, regional production outages and logistics. Roll-goods suppliers may face margin pressure when resin prices rise faster than contract pass-through mechanisms. Construction, protective apparel and industrial packaging buyers are more price sensitive than healthcare packaging customers, making resin volatility more visible in those applications.

Converter capacity can create another bottleneck. Medical packaging requires pouching, coating, sealing, clean handling, printing and quality control. A strong substrate alone does not guarantee reliable supply if converters lack capacity or process control. Buyers increasingly assess the whole supply chain, including substrate supplier, converter, sterilization route and packaging validation status.

Pricing Volatility

Pricing depends on HDPE resin cost, basis weight, process route, product form, coating, lamination, sterilization compatibility, cleanroom quality and documentation requirements. Flashspun HDPE products usually command premium pricing because performance characteristics are difficult to replicate through standard nonwoven processes. Medical packaging carries the strongest qualification premium because buyers pay for risk reduction, consistency and validation support.

Building wrap and industrial packaging behave differently. Buyers in these applications compare durability, printability, breathability, water resistance and installation performance against cost. A premium material can justify higher pricing when it prevents failures, reduces job-site damage or improves brand trust. However, construction-cycle weakness or aggressive contractor purchasing can increase pressure on suppliers.

Protective apparel pricing can be volatile because demand can rise sharply during public health events and then normalize. Cleanroom and industrial safety demand is more stable but still depends on semiconductor, pharmaceutical and laboratory activity. Suppliers with diversified exposure across healthcare packaging, construction, apparel and industrial uses are better positioned to manage pricing cycles.

Procurement Pressure

Procurement teams are under pressure to balance material cost with failure risk. Medical packaging buyers cannot evaluate HDPE nonwoven only by basis weight or roll price. They need seal behavior, peel performance, microbial barrier data, sterilization compatibility, linting behavior, aging performance, and supplier documentation. A cheaper substrate can become costly if it creates package failures or validation delays.

Construction buyers evaluate material through job-site durability, vapor permeability, water resistance, fastening performance, and installer familiarity. Building envelope failures can create warranty exposure, mold concerns, and brand damage. Procurement decisions therefore include contractor trust and technical support, not only material price.

Cleanroom and protective apparel buyers focus on contamination control, comfort and supply reliability. A material that sheds particles, tears easily or creates discomfort can reduce user acceptance. Buyers are increasingly asking suppliers for application-specific guidance, technical data and conversion support. The strongest suppliers will win where procurement teams connect material selection with total risk reduction.

New Technology Adoption

Technology adoption is strongest in converter-led laminates, coated HDPE nonwovens, sterile barrier pouch structures, cleanroom-compatible materials, printable nonwoven media and breathable building wraps. Medical packaging converters are developing structures that improve seal consistency, opening behavior, print clarity and sterilization performance. Coatings and laminates can extend HDPE nonwoven use into applications that require added barrier, sealing or handling properties.

Quality inspection technology is also becoming more important. Vision inspection, roll defect detection and process analytics can reduce scrap and improve converter yield. Medical packaging customers need consistent roll quality because small defects can affect package integrity. Suppliers that invest in better quality systems can strengthen their position with regulated buyers.

Sustainability technology is still emerging. Recycling of coated, laminated or contaminated nonwoven structures remains difficult. Material suppliers are therefore exploring waste reduction, take-back programs, downgauging, improved converter yield and lower-emission manufacturing. Buyers want credible sustainability paths but will not compromise sterile barrier or building protection performance.

Regional Expansion Opportunity

Asia-Pacific offers the strongest regional expansion opportunity because it already held the largest share in 2025 and is expected to increase its share by 2035. China, India, Japan and South Korea support demand through medical device manufacturing, pharmaceutical packaging, electronics cleanrooms, protective apparel and construction materials. Export-oriented healthcare manufacturing is especially important because global customers require validated materials and documentation.

North America remains a high-value market because U.S. healthcare packaging, medical devices, protective apparel and building envelope products are mature. Buyers in the region value supplier qualification, brand trust and technical support. Premium demand is strong where failure risk is costly, especially in sterile medical packaging and building wrap.

Europe offers stable premium demand in medical packaging, cleanrooms, technical textiles and building performance applications. Regulatory discipline and sustainability scrutiny influence material selection. European buyers often require strong documentation, environmental positioning and consistent supplier support. Growth may be slower than Asia-Pacific, but value per application remains attractive.

Government Policy Support

Government policy supports demand indirectly through healthcare infrastructure, medical device regulation, worker safety standards, building performance rules and cleanroom-linked advanced manufacturing programs. Healthcare policies that support domestic device production and safer packaging systems can increase demand for validated sterile barrier materials. Public healthcare procurement also influences packaging quality expectations for medical consumables.

Building energy policies support better envelope systems. Weather-resistive barriers and breathable wraps can help protect wall assemblies and support moisture management in energy-efficient buildings. As construction practices improve, builders may adopt higher-performance barrier materials to reduce warranty exposure and improve durability.

Advanced manufacturing policies can also support cleanroom material demand. Semiconductor, pharmaceutical and biotechnology investments require contamination-control materials, protective apparel and specialized packaging. HDPE nonwoven suppliers can benefit when cleanroom construction and regulated manufacturing expand.

Import-Export and Pricing Intelligence

HDPE nonwoven trade is driven by roll goods, medical packaging substrates, protective apparel, building wrap, industrial packaging and converter-ready materials. Demand is strongest where buyers need tear resistance, moisture resistance, microbial barrier performance, breathable protection or cleanroom suitability. Trade data should be interpreted with product mix in mind because lightweight nonwovens, coated structures, apparel and PE films may move under different product codes.

Pricing depends on HDPE resin cost, basis weight, product route, coating, lamination, sterilization compatibility, cleanroom quality and qualification status. Flashspun HDPE carries premium pricing where healthcare packaging, building envelope and protective apparel applications require validated performance. Standard spunbond or composite structures may compete more aggressively on cost in industrial packaging and selected apparel applications.

Medical packaging has the strongest pricing discipline because approved materials cannot be replaced easily. Buyers pay for consistency, documentation and reduced validation risk. Construction and industrial packaging buyers are more exposed to resin and roll-goods pricing, although premium building wrap brands can protect margins through performance and installer trust.

AI Impact Analysis

AI can improve HDPE nonwoven production through defect detection, roll inspection, process control, coating uniformity and demand forecasting. Medical packaging substrates require consistent surface behavior, seal performance and low defect rates. Vision inspection can detect holes, wrinkles, contamination, thickness variation and surface irregularities before material reaches converters. This reduces waste and supports stronger quality assurance.

Converters can use analytics to improve pouching, sealing, coating, laminating and printing operations. Sterile barrier packaging needs stable seal windows and predictable opening behavior. Process data can identify when heat, pressure, dwell time or substrate variation is moving outside the ideal range. Better process control reduces scrap and lowers customer complaint risk.

Building wrap and industrial packaging suppliers can also use AI to forecast demand. Construction cycles, healthcare packaging demand and protective apparel demand follow different patterns. A better forecasting model can reduce inventory imbalance and improve service levels. Protective apparel demand is especially sensitive to health events, industrial safety programs and distributor stocking behavior.

AI can also support material development. Models can compare coating recipes, laminate structures, basis weight changes and mechanical performance data. Material suppliers can shorten development cycles for products that need better barrier, tear resistance, breathability or printability. The strongest AI impact will come from linking production data with converter performance and end-user complaint history.

Disruption Analysis

Disruption is coming from healthcare packaging validation, building envelope modernization, converter-led laminates and sustainability pressure. Medical device growth creates more need for sterile barrier materials, but suppliers must meet strict qualification expectations. A validated substrate can defend share for many years because switching is difficult once a device packaging system is approved.

Building envelope modernization is changing demand because moisture control and energy efficiency are becoming more important. Builders need materials that protect wall assemblies from water intrusion while allowing vapor movement. HDPE nonwoven building wraps can benefit where contractors value durability and installation reliability. Growth depends on code awareness, builder education and product availability.

Converter-led laminates are creating new value. HDPE nonwoven can be combined with films, coatings and adhesives to serve medical pouches, industrial covers, cleanroom packaging and specialty mailing formats. Converters that develop application-specific structures can capture more value than suppliers selling commodity roll goods.

Sustainability pressure can disrupt material selection, especially in packaging and protective apparel. Buyers want lower waste and better end-of-life solutions. However, sterile barrier performance and worker protection cannot be sacrificed for recyclability alone. Suppliers that reduce waste while maintaining performance will gain stronger customer trust.

BCG Matrix: Company Evaluation

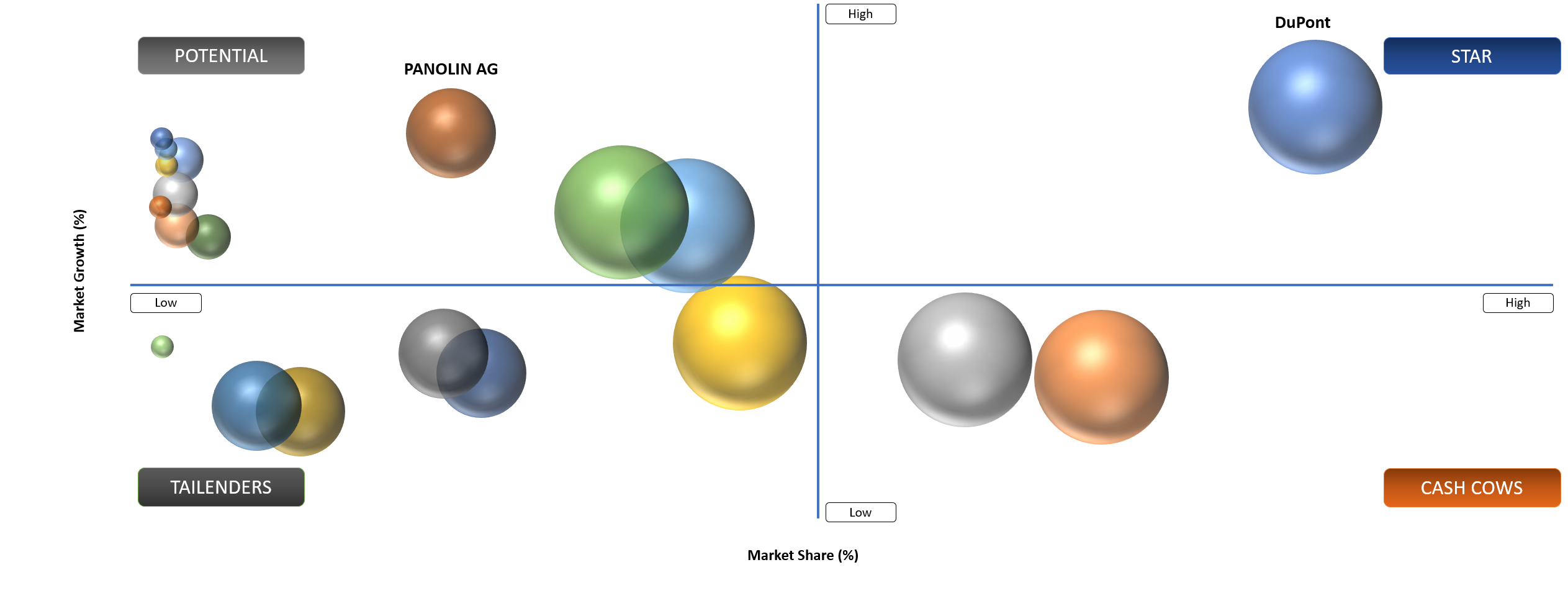

Star

Star players include DuPont de Nemours, Inc., Magnera Corporation, Freudenberg SE, Ahlstrom Oyj, Fitesa S.A., PFNonwovens Holding s.r.o., Toray Industries, Inc., Mitsui Chemicals, Inc. and Asahi Kasei Corporation. These companies have strong technical material capability, broad customer access and relevant exposure across healthcare packaging, construction, technical textiles, protective apparel and industrial uses. DuPont remains the strongest benchmark in flashspun HDPE nonwoven because Tyvek is closely associated with premium performance in sterile packaging, building envelope and protective material applications.

Potential

Potential companies include Fibertex Nonwovens A S, Mogul Co., Ltd. and Zhejiang Kingsafe Nonwovens Co., Ltd. These companies can gain share through regional technical nonwoven supply, converter partnerships, cost-competitive production and application expansion across hygiene, construction, industrial packaging and protective material uses. Growth potential will depend on whether they can move beyond standard roll goods into higher-value structures that require stronger quality control, documentation support and application-specific performance.

Market Dynamics

Driver Impact Analysis

| Driver | Market Growth Impact | Demand Concentration | Impacted Use Case | Strategic Impact |

Sterile Medical Packaging Needs Validated Barrier Materials | High | U.S., Europe, Japan, China and India | Medical Packaging and Sterile Barrier Systems | Supports premium qualified substrates |

Building Envelope Upgrades Increase Breathable Weather Barrier Demand | Medium To High | North America, Europe and Asia-Pacific | Building Wrap | Drives construction material demand |

Cleanroom and Protective Apparel Demand Supports Technical Nonwovens | Medium | Healthcare, Electronics and Pharmaceuticals | Coveralls and Cleanroom Supplies | Expands safety and contamination-control use |

Industrial Packaging Requires Lightweight Tear-Resistant Substrates | Medium | Global Industrial Buyers | Pouches, Covers and Envelopes | Supports durable packaging formats |

Sterile Medical Packaging Needs Validated Barrier Materials

Sterile medical packaging is the strongest driver because medical devices, surgical kits, diagnostic consumables and pharmaceutical delivery products require packaging that maintains sterility from manufacturing through clinical use. HDPE nonwoven materials are selected where buyers need breathability for sterilization, tear resistance during handling and a reliable microbial barrier. Medical packaging decisions are made slowly because packaging failure can affect patient safety, product release and regulatory confidence.

Medical device companies increasingly need packaging that supports multiple sterilization routes and clean opening behavior. Pouches, lids and sterile barrier systems must maintain seal integrity during transportation, storage and hospital handling. A substrate that tears unpredictably, creates lint or produces inconsistent seals can create operational risk. HDPE nonwoven materials gain value when they reduce this risk through predictable performance.

Single-use medical devices and diagnostic consumables are expanding the opportunity. More procedures use packaged components that must remain sterile until point of use. Home healthcare and self-administered therapies also increase demand for packaging that protects devices outside traditional clinical environments. Packaging needs to be durable enough for distribution but easy enough for End-Users to open safely.

Supplier differentiation depends on documentation, converter support and qualification history. Medical packaging buyers need technical data, roll consistency and compatibility with sealing equipment. A supplier that supports converters during validation can secure long-term demand because approved packaging structures are difficult to replace.

Restraint Impact Analysis

| Restraint | Drag On Market Growth | Primary Impact Area | Impacted Use Case | Strategic Impact |

Resin Cost and Qualification Barriers Limit Supplier Switching | High | Medical Packaging and Roll Goods | Sterile Pouches and Roll Stock | Keeps customers tied to approved materials |

Flashspun HDPE Capacity Concentration Raises Supply Risk | Medium To High | Premium HDPE Nonwoven | Healthcare and Building Envelope Applications | Supports dual sourcing discussions |

Recycling Complexity Limits Circularity Claims | Medium | Laminates and Coated Materials | Packaging and Apparel | Raises sustainability pressure |

Construction Cycles Create Weather Barrier Demand Volatility | Medium | Building Wrap | Residential and Commercial Construction | Links demand to building activity |

Resin Cost and Qualification Barriers Limit Supplier Switching

HDPE resin cost affects roll-goods pricing, converter margins and buyer negotiation. Resin price movement can be difficult to pass through quickly in construction, protective apparel and industrial packaging channels. Buyers in these applications may compare HDPE nonwoven with other nonwoven or film-based alternatives when price rises. This creates pressure on suppliers serving cost-sensitive formats.

Medical packaging behaves differently because qualification barriers make switching difficult. A new substrate may require seal testing, sterilization validation, aging studies, transport simulation, packaging line adjustments and customer approval. Even if a competing material is cheaper, switching can take months or longer. This protects approved suppliers but also slows new entrant penetration.

Flashspun HDPE supply concentration creates another restraint. Premium applications often depend on established materials with long performance history. Customers may want dual sourcing but struggle to find equivalent materials that can pass validation. This can create supply security concerns for large medical device companies and global converters.

Sustainability and recycling challenges also limit expansion in some applications. Coated, laminated, contaminated or sterile-contact materials can be difficult to recycle through standard systems. Buyers want improved circularity but must prioritize sterility, protection and durability. Suppliers face pressure to reduce waste without weakening performance.

Segmentation Analysis

Flashspun HDPE Nonwoven Will Continue To Lead Premium Demand

Flashspun HDPE nonwoven will continue to lead premium demand because it offers a strong balance of breathability, durability, water resistance, microbial barrier performance and tear resistance. The material is difficult to position as a simple commodity because its value is tied to performance in demanding applications. Medical packaging, building envelopes, protective apparel and industrial packaging all require material behavior that standard roll goods may not consistently provide.

Medical packaging gives flashspun HDPE its strongest value base. Sterile barrier systems need a substrate that allows sterilization while protecting against contamination. Package integrity must remain stable during handling, transport and storage. A proven flashspun HDPE substrate can reduce qualification risk and support long-term customer retention. Buyers are therefore more willing to pay for consistency and documentation.

Building envelope applications value a different performance balance. Weather barriers need to resist bulk water while allowing moisture vapor to escape from wall assemblies. Job-site durability matters because materials are exposed to wind, fastening, cutting and handling during construction. A breathable and tear-resistant HDPE nonwoven can reduce installation failures and support better building durability.

Protective apparel and controlled environment use also support premium demand. Coveralls and cleanroom garments need barrier performance, comfort and resistance to tearing. Materials that are too stiff or fragile can reduce worker acceptance. Flashspun HDPE remains attractive where protection, breathability and durability need to work together.

Medical Packaging Creates The Strongest Qualification Barrier

Medical packaging is the most defensible application because approved sterile barrier materials are difficult to replace. Medical device companies must validate packaging as part of product safety and regulatory compliance. A substrate change can affect sealing, sterilization, aging performance, transport durability and user opening behavior. This makes medical packaging a high-retention market for qualified HDPE nonwoven suppliers.

Sterile pouches, lids and form-fill-seal structures need consistent roll quality. Surface irregularities, linting, holes or inconsistent thickness can create defects during conversion. Converters also need predictable sealing windows because heat, pressure and dwell time must produce reliable seals without damaging the material. HDPE nonwoven suppliers that deliver lot-to-lot consistency and strong technical support can earn preferred status.

Growth is supported by medical device expansion, diagnostic testing and home healthcare. Single-use surgical tools, implant accessories, diagnostic cartridges, monitoring devices and self-care products all require packaging that protects function and sterility. As medical care moves outside hospitals, packaging must remain durable across longer and more varied distribution channels.

Medical packaging also benefits from global manufacturing shifts. Asia-Pacific manufacturers serving export markets need substrates that satisfy international buyer expectations. India, China, Japan and South Korea are expanding medical device and diagnostic manufacturing. Demand will grow where local converters can deliver packaging quality that meets global healthcare standards.

Building Wrap Demand Depends On Moisture Control and Job-Site Durability

Building wrap demand is linked to moisture management, air infiltration control and energy-efficient construction. Wall assemblies need protection from bulk water while allowing vapor to escape. Breathable HDPE nonwoven barriers are used where builders want to reduce moisture-related risk. Material failure can create mold, rot, insulation damage and warranty claims, so product selection matters.

Contractor handling is a practical buying factor. Building wraps are exposed to wind, fasteners, cutting, rough handling and weather before cladding is installed. A product that tears easily can delay installation and increase waste. Tear resistance and fastening strength therefore influence purchase decisions alongside price.

Energy-efficient construction increases the importance of building envelope quality. Tighter buildings require better moisture management because trapped moisture can become more damaging. Builders, architects and inspectors are paying closer attention to weather-resistive barriers, flashing details and wall system compatibility. HDPE nonwoven suppliers can benefit when building practices move beyond minimum-cost materials.

Regional demand depends on construction activity, building codes, climate and installer education. North America remains a mature market for house wrap and commercial building wrap. Europe emphasizes energy performance and moisture control. Asia-Pacific offers growth as construction quality standards rise in urban projects, healthcare facilities, data centers and premium residential construction.

Protective Apparel and Cleanroom Supplies Support Technical Nonwoven Demand

Protective apparel and cleanroom supplies create demand for HDPE nonwoven materials where barrier protection, low linting, comfort and tear resistance matter. Controlled environments such as pharmaceutical manufacturing, electronics production, biotechnology labs and cleanrooms require garments and covers that reduce contamination risk. A material that sheds particles or tears easily can compromise operations.

Protective apparel demand is more cyclical than medical packaging because purchasing can rise during health events, industrial safety campaigns or emergency response needs. After demand spikes, inventories may normalize. Suppliers need flexibility because sudden changes in distributor orders can create production and inventory stress.

Cleanroom demand is more stable and higher value. Semiconductor, pharmaceutical and medical device production requires contamination control and strict operating discipline. Materials used in these settings need consistent quality and documentation. Asia-Pacific cleanroom growth is especially important because electronics, batteries, pharmaceuticals and medical devices are expanding across Japan, South Korea, China and India.

Comfort and user acceptance are important. Workers wearing protective apparel for long shifts need breathable and durable materials. A garment that traps heat or tears easily can reduce compliance. HDPE nonwoven suppliers that balance protection with comfort can defend share in controlled environments and industrial safety applications.

Market Segmentation

- By Type

- Flashspun HDPE Nonwoven

- Spunbond HDPE Nonwoven

- Composite HDPE Nonwoven

- Coated HDPE Nonwoven

- Laminated HDPE Nonwoven

- Others

- By Basis Weight

- Up To 40 GSM

- 41 To 80 GSM

- 81 To 120 GSM

- Above 120 GSM

- By Form

- Rolls

- Sheets

- Pouches

- Envelopes

- Coveralls

- Tapes

- Laminates

- Others

- By Application

- Medical Packaging

- Protective Apparel

- Building Wrap

- Industrial Packaging

- Graphic Media

- Tags and Labels

- Sterile Barrier Systems

- Cleanroom Supplies

- Filtration

- Others

- By End-User

- Healthcare and Medical Device Companies

- Pharmaceutical Packaging Companies

- Construction and Building Envelope Companies

- Personal Protective Equipment Manufacturers

- Industrial Packaging Companies

- Printing and Graphics Companies

- Cleanroom Operators

- Logistics and Mailing Companies

- Others

Geographical Penetration

Asia-Pacific HDPE Nonwoven Market Trends

Asia-Pacific dominated the global HDPE nonwoven market with 44.8% market share in 2025 and is expected to reach 52.0% market share by 2035. The region is also the fastest-growing with an 8.1% CAGR between 2026 and 2035. Growth is supported by medical device manufacturing, pharmaceutical packaging, electronics cleanrooms, protective apparel, construction activity and industrial packaging conversion.

China remains the largest manufacturing base in the region. Demand is supported by healthcare packaging, protective apparel, technical nonwovens, construction materials and export-oriented conversion. Chinese producers also compete strongly in standard nonwoven roll goods, although premium sterile packaging and high-performance flashspun applications remain more dependent on validated suppliers and customer qualification.

India is becoming an important growth market because healthcare manufacturing, pharmaceutical packaging, diagnostics, building materials and cleanroom infrastructure are expanding. Export-oriented medical device producers need packaging materials that satisfy global customer requirements. Construction materials are also moving toward better moisture management in premium residential, hospital, commercial and industrial projects.

Japan and South Korea support high-value demand through quality-driven manufacturing. Medical packaging, electronics cleanrooms and industrial protection applications require materials with strong consistency and technical documentation. Buyers in these countries prioritize reliability and supplier trust, which supports premium materials rather than purely cost-led sourcing.

U.S. HDPE Nonwoven Market Landscape

The U.S. remains one of the most important value markets for HDPE nonwoven because healthcare packaging, medical device production, building wrap and protective apparel demand are mature. Medical packaging customers require validated substrates supported by documentation and converter expertise. Material qualification barriers protect established suppliers and make the U.S. a high-retention market.

Building envelope demand is also important. U.S. residential and commercial construction uses weather-resistive barriers to protect wall assemblies from water intrusion. Contractors value product familiarity, installation guidance and brand trust. Premium building wraps can defend share where builders want durability and moisture-control performance.

Protective apparel and cleanroom applications support additional demand. Healthcare, pharmaceuticals, biotechnology, laboratories and electronics production use disposable or limited-use protective materials. Demand can fluctuate during health emergencies, but controlled environment applications provide a more stable base.

The U.S. also influences global supplier standards. Medical device companies and global converters often set strict expectations for packaging quality, technical files and supplier performance. Materials accepted in U.S. healthcare packaging can influence procurement decisions in other regions.

India HDPE Nonwoven Market Landscape

India is one of the most attractive growth markets for HDPE nonwoven because the country is expanding healthcare manufacturing, pharmaceutical packaging, diagnostics, medical devices and construction quality. The market remains price-sensitive, but export-focused manufacturers and premium healthcare suppliers increasingly need validated packaging materials. This creates a two-layer market: commodity nonwovens for cost-led uses and technical nonwovens for regulated or export-oriented applications.

Medical packaging is a key growth route. India’s pharmaceutical and medical device industries require packaging that can support sterilization, transport and compliance expectations. Local converters serving global customers must improve seal quality, material consistency and documentation. HDPE nonwoven adoption will grow where device makers require sterile barrier formats with stronger performance evidence.

Construction applications are developing gradually. Premium builders, hospitals, cleanrooms, warehouses and institutional projects are more likely to adopt advanced building envelope materials before mass residential construction. Better awareness of moisture control and energy efficiency can support weather barrier demand over the forecast period.

Cleanroom and protective apparel demand will also expand. Pharmaceutical manufacturing, biotechnology, electronics assembly and laboratory infrastructure require contamination-control materials. As these industries scale, demand for technical nonwovens with better quality and consistency will increase.

Japan HDPE Nonwoven Market Outlook

Japan is a high-value HDPE nonwoven market because buyers prioritize quality, reliability, documentation and supplier consistency. Medical packaging, cleanroom supplies, industrial protection and electronics-related uses are more important than commodity volume. Japanese customers are cautious when qualifying new materials, but approved suppliers often retain business for long periods.

Medical packaging demand is supported by advanced healthcare, diagnostic and device manufacturing. Sterile barrier systems need predictable material behavior, seal reliability and clean opening performance. Japanese buyers place strong emphasis on testing and documentation, which supports premium HDPE nonwoven products.

Cleanroom demand is also important because Japan has strong electronics, precision manufacturing, life sciences and materials industries. Low-linting and controlled contamination materials are important in production environments where small defects can create high losses. HDPE nonwoven suppliers that can provide consistent quality and strong technical data are well positioned.

Building envelope demand is more selective but valuable. Durable weather barriers can support high-quality building practices where moisture control and long service life matter. Adoption depends on building system design, local construction practices and contractor familiarity with premium materials.

Competitive Landscape

- Competition is concentrated around flashspun HDPE leaders, technical nonwoven producers, medical packaging substrate suppliers, protective apparel converters and building envelope material providers. Flashspun HDPE is not easy to replicate because performance depends on process technology, fiber structure, bonding, consistency and application history. DuPont remains the key benchmark through Tyvek.

- Technical nonwoven producers such as Magnera, Freudenberg, Ahlstrom, Fitesa, PFNonwovens, Toray, Mitsui Chemicals and Asahi Kasei influence the broader competitive field. Some compete directly in selected technical nonwoven applications, while others compete through alternative materials, coated structures, composite nonwovens or converter partnerships. The market is therefore broader than one material format, especially in packaging, apparel and industrial uses.

- Healthcare packaging competition is more qualification-led than price-led. Medical device companies and converters value suppliers with strong documentation, stable roll quality, sterilization compatibility and technical support. New entrants face long approval cycles, even when materials appear cost-competitive. Established suppliers benefit from installed qualification history and customer trust.

- Building wrap competition is more brand-led and contractor-led. Builders evaluate water resistance, vapor permeability, tear strength, installation ease, tape compatibility and warranty support. Contractors often prefer materials with known field performance. Premium suppliers can defend share through training, technical guidance and long-term building envelope credibility.

- Protective apparel and cleanroom competition is more volume-flexible. Demand can shift quickly, especially after health events. Suppliers with broad converting capability, reliable material supply and regional distribution can respond faster. Cleanroom buyers remain more selective because contamination-control performance and documentation matter.

- Competitive benchmarking should track material performance, medical packaging qualification, basis weight range, converter support, sterilization compatibility, building code acceptance, cleanroom suitability, global supply reliability, resin exposure and customer switching risk.

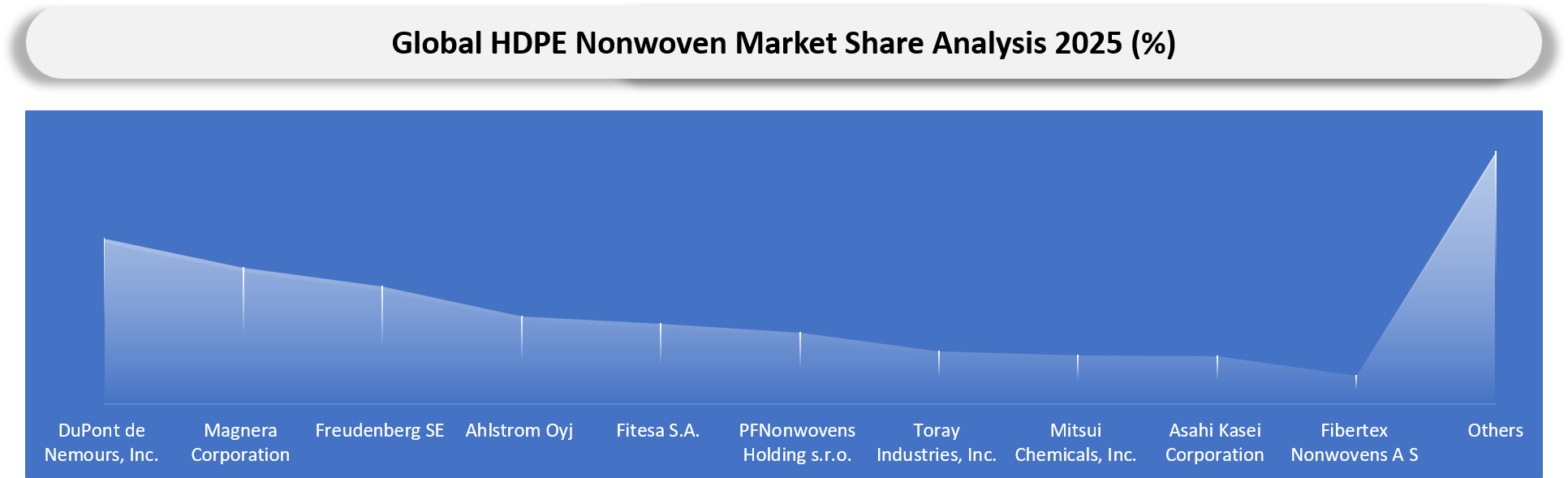

Key Players

- DuPont de Nemours, Inc.

- Magnera Corporation

- Freudenberg SE

- Ahlstrom Oyj

- Fitesa S.A.

- PFNonwovens Holding s.r.o.

- Toray Industries, Inc.

- Mitsui Chemicals, Inc.

- Asahi Kasei Corporation

- Fibertex Nonwovens A S

- Johns Manville Corporation

- Avgol Industries 1953 Ltd.

- TWE Group GmbH

- Sandler AG

- Mogul Co., Ltd.

- Suominen Corporation

- Don and Low Ltd.

- Tex Tech Industries, Inc.

- Zhejiang Kingsafe Nonwovens Co., Ltd.

- Xinlong Holding Group Company Ltd.

Company Coverage Preview

DuPont de Nemours, Inc. remains the benchmark company in HDPE nonwoven through Tyvek. Tyvek is positioned across healthcare packaging, building envelopes, protective apparel, controlled environments, graphics, industrial packaging, envelopes and cargo covers. Its advantage comes from a strong brand, deep application history, technical documentation and a material profile that combines breathability, durability, water resistance and barrier performance. Medical packaging buyers value Tyvek because sterile barrier applications require proven performance and long qualification history.

Magnera Corporation is an important company to watch because it brings together a broad nonwovens and specialty materials platform. The company’s official market coverage includes healthcare, building and construction, filtration, hygiene, technical nonwovens and specialties. Magnera’s relevance comes from scale, customer access and exposure to multiple nonwoven end markets. Its role is broader than pure HDPE nonwoven, but its platform can influence converter relationships and adjacent material substitution.

Amcor’s combination with Berry Global matters for the HDPE nonwoven value chain because healthcare packaging and material science capabilities are becoming more consolidated. The combined company brings wider packaging reach, technical capability and customer access. Medical device and pharmaceutical customers increasingly prefer packaging partners with global scale, documentation discipline and material innovation capacity. This creates indirect pressure on substrate suppliers to support global converter networks.

Freudenberg SE, Ahlstrom Oyj, Fitesa S.A., PFNonwovens Holding s.r.o., Toray Industries, Inc., Mitsui Chemicals, Inc., Asahi Kasei Corporation and Fibertex Nonwovens A S compete across technical nonwovens and adjacent high-performance material categories. Many of these players are not direct equivalents to flashspun HDPE leaders in every application, but they influence customer choice were alternative substrates, composite structures or coated nonwovens can meet application needs.

Major Pain Points

- Medical packaging qualification cycles make supplier switching slow and costly.

- HDPE resin price movement affects roll-goods, protective apparel, building wrap and industrial packaging margins.

- Flashspun HDPE capacity concentration creates supply security concerns for premium applications.

- Sterile packaging buyers require strong documentation, lot consistency and validated seal performance.

- Converter scrap can rise when roll quality, coating consistency or sealing behavior varies.

- Building wrap failures can create moisture damage, warranty exposure and contractor complaints.

- Protective apparel demand can spike and normalize quickly, creating inventory planning risk.

- Recycling remains difficult when HDPE nonwoven is coated, laminated, contaminated or used in medical and protective applications.

- Cleanroom users require low-linting and contamination-control performance that standard nonwovens may not provide.

- Asia-Pacific growth requires local converter quality, regulatory readiness and stronger technical support.

Recent Developments

- April 2025: Amcor completed its combination with Berry Global, creating a broader consumer and healthcare packaging platform with expanded material science and innovation capabilities.

- January 2025: DuPont revised its corporate separation plan and continued retaining industrial material businesses that include Tyvek-related applications, supporting continuity for customers using HDPE nonwoven materials in healthcare, construction and protection-related uses.

- January 2025: DuPont advanced its portfolio separation plan toward an electronics spin-off while keeping core industrial material businesses under the remaining company, supporting ongoing focus on specialty materials used in healthcare, building and safety applications.

- 2025: Healthcare packaging converters increased focus on sterile barrier substrates that provide clean peel, microbial barrier performance, seal consistency and sterilization compatibility.

- 2025: Building envelope suppliers increased emphasis on breathable weather barriers that combine water resistance, vapor permeability and job-site durability for energy-efficient construction.

Analyst View and Opinion

- HDPE nonwoven demand will remain more value-driven than volume-driven because the best applications depend on validated performance rather than commodity fabric supply.

- Medical packaging will remain the most attractive application because sterile barrier qualification creates high customer retention and premium pricing potential.

- Flashspun HDPE will continue to dominate premium demand where breathability, water resistance, microbial barrier performance and tear strength must be combined in one substrate.

- Asia-Pacific will become increasingly important because medical device manufacturing, pharmaceutical packaging, electronics cleanrooms and construction quality standards are expanding together.

- North America will remain a high-value market because healthcare packaging and building wrap demand are mature, specification-led and supported by strong supplier relationships.

- Europe will maintain premium demand through regulatory discipline, building performance requirements, cleanroom materials and technical textile standards.

- Supplier switching will remain slow in medical packaging because validation, sterilization and aging studies protect approved materials.

- Converter partnerships will become more important as customers buy finished sterile pouches, laminates, covers, garments and packaging formats rather than raw roll goods alone.

- Sustainability pressure will rise, but performance will remain the first filter in healthcare and protective applications.

- Competitive advantage will move toward suppliers that combine material science, technical documentation, application support, converter relationships and reliable regional supply.

Target Audience

| Industry | Who Should Buy This Report? | Reason To Buy This Report |

| Medical Device Companies | Packaging Development Teams, Regulatory Teams, Procurement Teams | Evaluate validated sterile barrier materials and supplier risks |

| Pharmaceutical Packaging Companies | Packaging Engineers, Converter Teams, Strategy Teams | Track demand for breathable, sealable and sterilization-compatible substrates |

| Building Envelope Companies | Product Managers, Commercial Teams, Specification Teams | Understand weather barrier demand, material positioning and regional growth |

| Protective Apparel Manufacturers | Product Development Teams, Sourcing Teams | Evaluate material demand for coveralls, controlled environments and safety apparel |

| Cleanroom Operators | Facility Managers, Quality Teams | Assess low-linting and contamination-control material needs |

| Technical Nonwoven Producers | Strategy Teams, Sales Leaders, Product Managers | Identify premium application opportunities and competitive pressure |

| Packaging Converters | Operations Teams, Commercial Teams | Understand medical pouch, laminate and specialty packaging demand |

| Investors | Specialty Materials Investors, Packaging Investors | Evaluate premium nonwoven growth pockets and consolidation signals |

| Consulting Firms | Materials Practice Teams, Healthcare Packaging Advisors | Support market entry, supplier benchmarking and opportunity mapping |

What DataM Uniquely Provides

- DataM separates HDPE nonwoven demand by Type, basis weight, form, application, End-User and region, helping clients avoid treating all nonwovens as one broad material category.

- DataM maps application value across medical packaging, sterile barrier systems, building wrap, protective apparel, industrial packaging, cleanroom supplies, graphics and envelopes.

- DataM benchmarks suppliers across flashspun HDPE, technical nonwovens, medical packaging substrates, protective apparel materials and converter relationships.

- DataM evaluates pricing pressure from HDPE resin, basis weight, coating, lamination, sterilization compatibility, cleanroom quality and qualification premiums.

- DataM provides procurement-risk mapping for medical validation, supply concentration, resin exposure, converter quality and regional availability.

- DataM assesses Asia-Pacific opportunity through medical device manufacturing, pharmaceutical packaging, electronics cleanrooms, protective apparel and construction material upgrades.

- DataM supports buyer decision-making by comparing performance-led demand against cost-led substitution pressure across healthcare, construction and industrial applications.

- DataM includes trade intelligence through HS 560312, HS 560313, HS 560314, HS 621010 and HS 392010 for nonwoven roll goods, protective apparel and PE material flows.