Digital Inks Market Overview

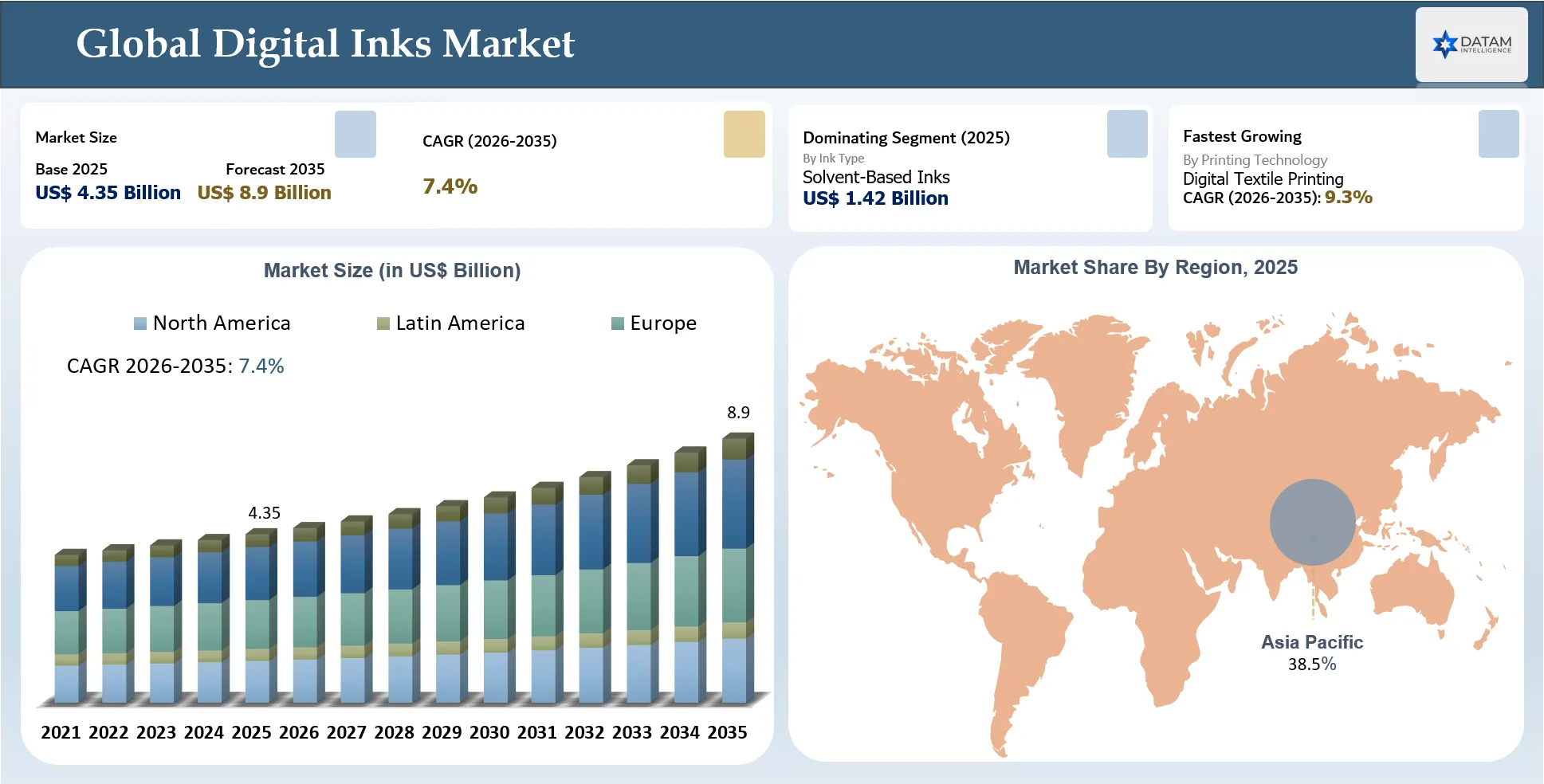

The Global Digital Inks Market stood at US$ 4.35 billion in 2025 and is expected to reach US$ 8.9 billion by 2035, growing with a CAGR of 7.4% during the forecast period 2026-2035.

Global Digital Inks Market is undergoing a noticeable trend of technology and compliance evolution with the increasing move from solvent-rich inks towards water-based, low-VOC, UV, LED-UV curable, bio-based, and food-safe digital ink products. This technology change is not only about sustainability, but also about the procurement needs of converters, packagers, and brand owners of short runs, fast curing, minimal odors, migration control, substrate versatility, and regulatory approval. In April 2026, Sun Chemical Corporation, which is part of DIC Group introduced the innovative AquaHeat technology, which delivers food-safe, bio-based printing inks for high-temperature applications.

These developments illustrate the growing trend in the digital ink market, where suppliers compete in performance engineering, rather than commodity ink manufacturing. It indicates that there is a move to ink products that can be used in combination with compatible printheads, guaranteeing color accuracy and food contact safety, rapid drying and curing processes, and a sustainable approach. Packaging and labelling, textile, and industrial printing customers will have an advantage with ink suppliers, who can provide strong formulation expertise and a comprehensive product portfolio.

Key Takeaways

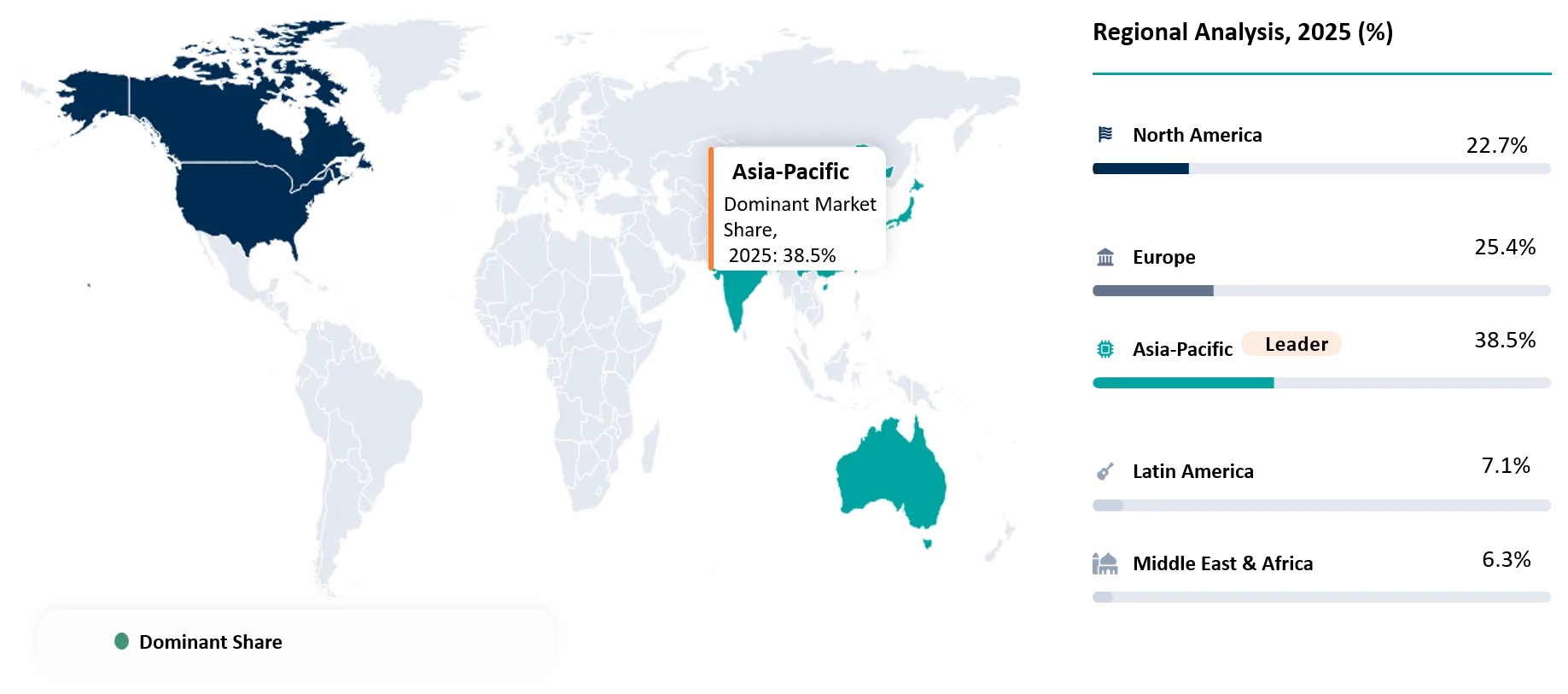

- Asia-Pacific held the highest market share at 38.5% in 2025, supported by large-scale packaging conversion, textile printing capacity, consumer goods production and expanding digital print adoption.

- Asia-Pacific is expected to remain the fastest-growing region, driven by growth in flexible packaging, labels, apparel printing, signage, electronics marking and low-VOC digital ink adoption.

- Solvent-Based Inks dominated the market in 2025, valued at approximately US$ 1.42 billion, supported by strong use in wide-format graphics, outdoor signage, plastic films and durable substrate printing.

- Digital Textile Printing is projected to be the fastest-growing printing technology segment, expanding at an estimated 9.3% CAGR during 2026-2035, driven by on-demand apparel production, customization and pigment-based textile ink adoption.

- Sustainability is becoming a key procurement factor, with buyers shifting toward water-based, low-VOC, latex, UV-curable, LED UV-curable and low-migration digital ink systems.

- Procurement decisions are increasingly based on printhead compatibility, color consistency, substrate adhesion, drying or curing speed, food-contact safety, VOC profile, technical support and supply reliability.

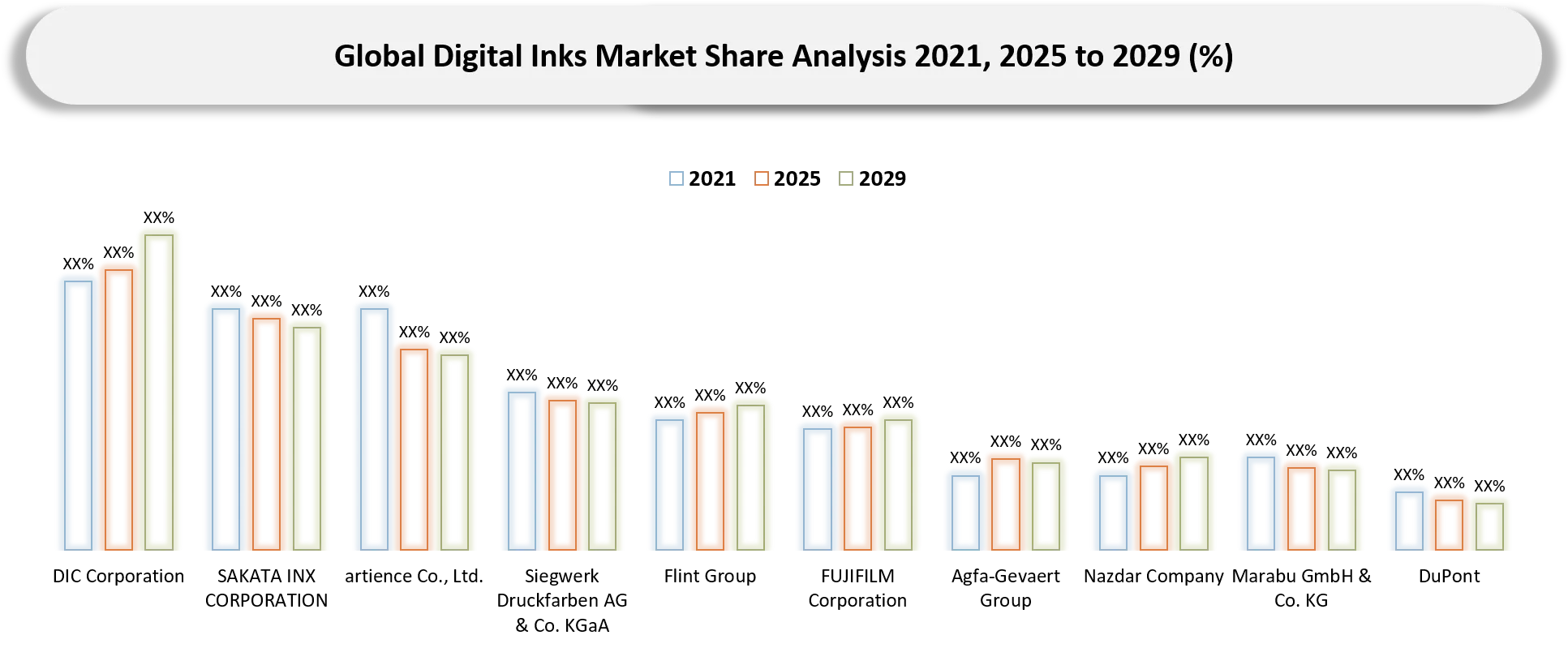

- The market is competitive, with top players including DIC Corporation, SAKATA INX CORPORATION, artience Co., Ltd., Siegwerk Druckfarben AG & Co. KGaA and Flint Group.

Digital ink Market Scope

| Metrics | Details | |

| 2025 Market Size | US$ 4.35 Billion | |

| 2035 Projected Market Size | US$ 8.9 Billion | |

| CAGR (2026-2035) | 7.4% | |

| Largest Market | Asia-Pacific | |

| Fastest Growing Market | Asia-Pacific | |

| By Ink Type | Solvent-Based Inks, Water-Based Inks, Oil-Based Inks, Latex Inks, and Others | |

| By Curing Type | Conventional Drying Inks, UV-Curable Inks, LED UV-Curable Inks, Electron Beam-Curable Inks, Oxidative Drying Inks, and Others | |

| By VOC Level | Zero VOC Inks, Low VOC Inks, and High VOC Inks | |

| By Bio-Based Content | Bio-Based Inks, and Non-Bio-Based Inks | |

| By Printing Technology | Inkjet Printing, Electrophotography Printing, Digital Textile Printing, Digital Label Printing, Digital Packaging Printing, and Others | |

| By Resin Type | Acrylic, Polyurethane, Polyamide, Nitrocellulose, Epoxy, Polyester, and Others | |

| By Application / Use Case | Packaging, Labels and Tags, Commercial Printing, Publications, Decorative Printing, Textile Printing, Security Printing, Industrial Printing, and Others | |

| By Substrate | Paper and Paperboard, Plastic and Films, Textile, Glass and Ceramics, Metal, Wood, and Others | |

| By End-Use Industry | Food and Beverages, Pharmaceuticals, Personal Care and Cosmetics, Consumer Goods, Publishing and Commercial Printing, Textiles and Apparel, Electronics, Automotive, Industrial Goods, and Others | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

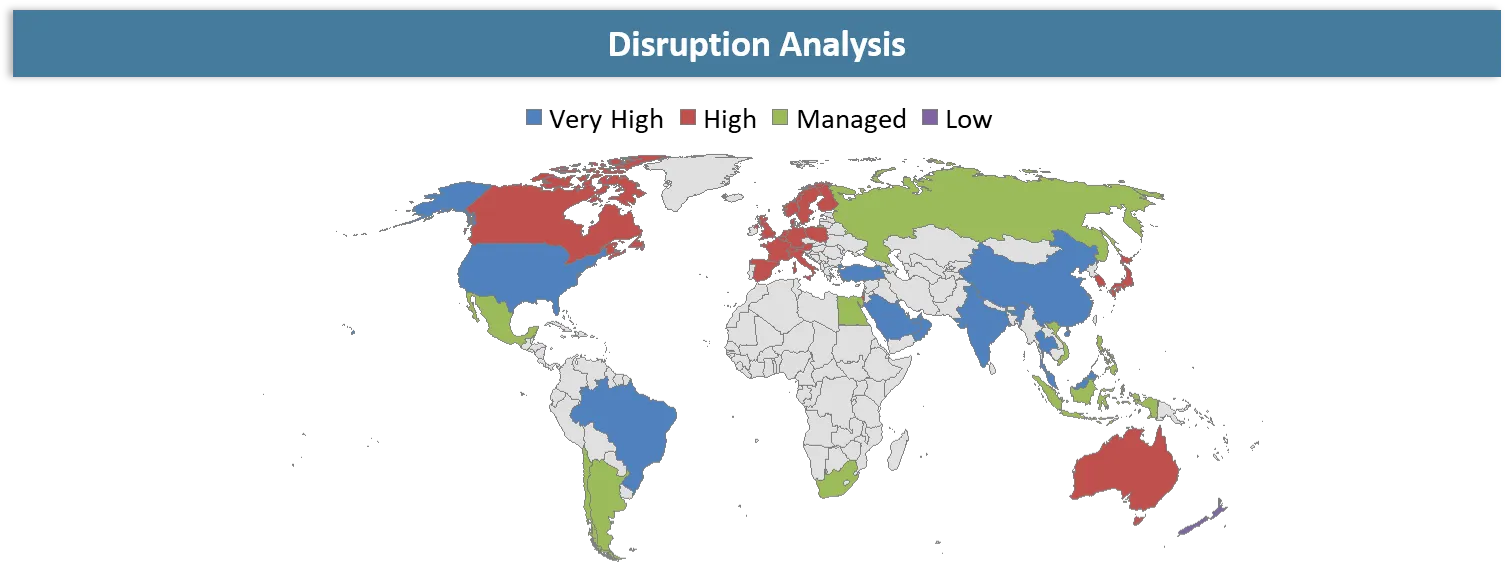

Disruption Analysis

Shift Toward Application-Specific, Sustainable and OEM-Compatible Digital Ink Systems

The Global Digital Inks Market is undergoing a structural change in view of the demand for digital manufacturing among print buyers that entails a move from standardization and long runs to agile processes and manufacturing approaches that are based on digital technology. Packaging converters, label manufacturers, textile printers and other industrial users face the challenge of delivering fast delivery schedules, reduced order quantities, easy adjustments in artwork and customized SKUs. This creates an unprecedented change in terms of ink purchasing, since buyers need ink products that operate successfully at high speeds of printhead operations as well as different substrates and varying manufacturing conditions.

Another source of disruption is arising out of sustainability initiatives, regulatory concerns, and integration of printing machinery. Printers are being compelled by brand owners to use inks that reduce VOCs, such as water-based, latex, low migration inks, and LED UV-cured inks in their printing process. On the other hand, printer OEMs and ink suppliers are coming closer due to ink systems with validated color management, AI-enabled quality controls, and application-driven ink solutions. This trend creates a more concentrated market for ink manufacturers as formulary excellence, regulatory compliance, regional sourcing capacity, and technical service capabilities become important to win premium contracts.

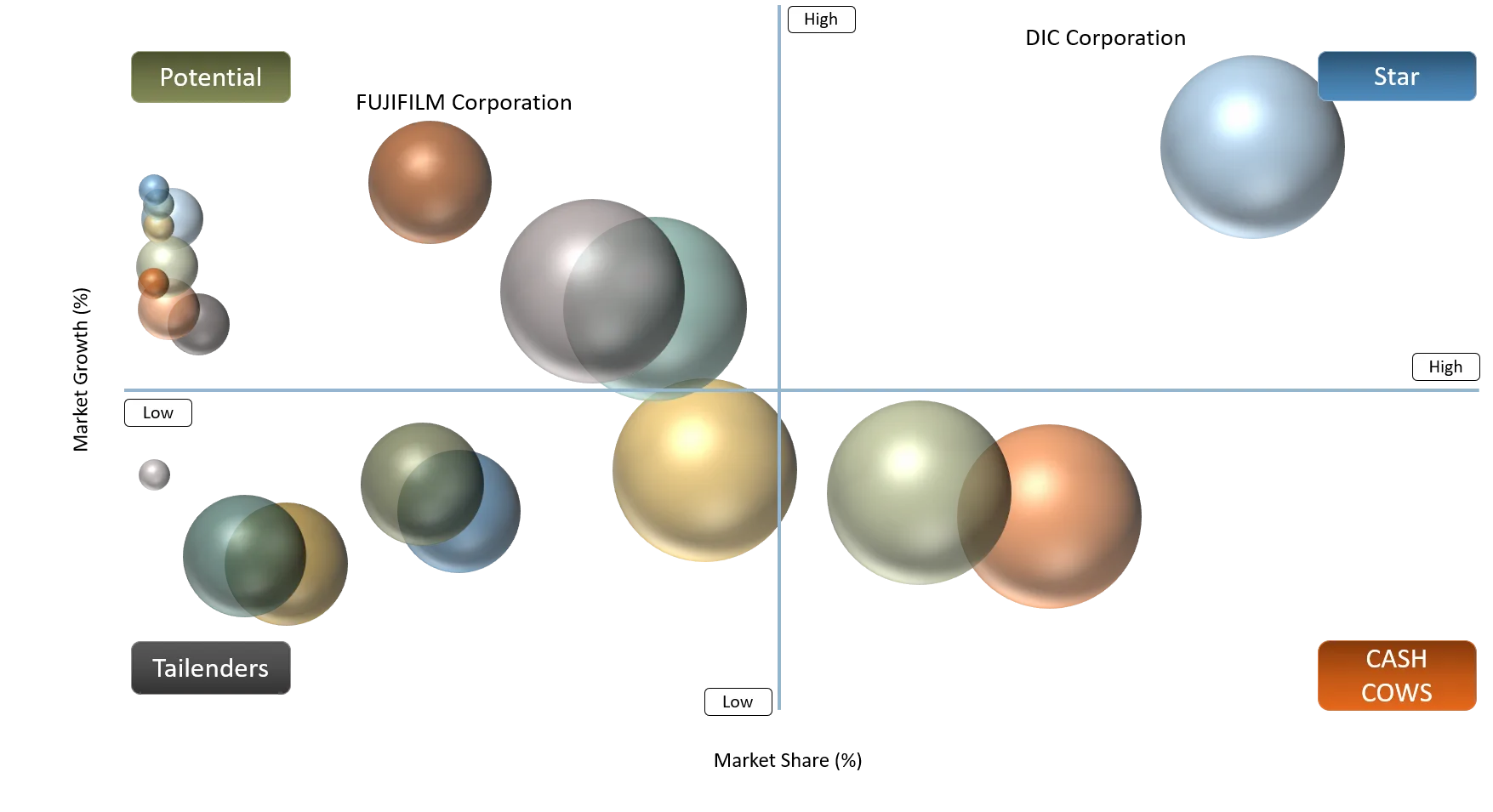

BCG Matrix: Company Evaluation

As for the BCG matrix, For Global Digital Inks Market, Stars can be defined as firms that have strong international presence, diverse range of digital inks, formulation expertise, solid OEM/converter partnerships and distinct positioning in packaging, labels, textiles, wide format printing and industrial digital printing segment. The list includes DIC Corporation, SAKATA INX CORPORATION, artience Co., Ltd., Siegwerk Druckfarben AG & Co. KGaA, Flint Group and FUJIFILM Corporation because of their strong foundation in ink technology, solid presence in packaging and industrial printing markets, sustainability-driven innovations and high-performance capabilities for digital printing applications.

The Cash Cows include firms with proven digital ink expertise, high levels of client loyalty and sustainable position in mature and specialized segments. Agfa-Gevaert Group, Nazdar Company, Marabu GmbH & Co. KG, DuPont and Archroma can be included here because of their strong wide format inks, textile inks, industrial inkjet inks, specialty substrates and application-specific digital ink formulations. These companies occupy commercially critical niches and can boast of technical performance, substrate compatibility, color consistency and strong client support capabilities.

Question Marks include firms which have considerable relevance in the digital printing ecosystem, but where their position within the ink market is directly connected with the printer hardware platform that they use, their proprietary system or application segment. Seiko Epson Corporation, HP Inc., Electronics For Imaging, Inc. and Kornit Digital Ltd. are examples of question marks. While they have tremendous growth potential, considering the increasing applications for digital textile printing, digital packaging printing, digital signage and digital industrial printing, their future market share is contingent upon growth in the number of printers sold.

Digital ink Market Dynamics

Acceleration of Short-Run, Variable Data and Personalized Digital Printing Demand

There is an increase in momentum within the Global Digital Inks Market owing to packaging converters, label printers, textile printers, and commercial print houses switching to short runs. Seasonal packs, regional SKU offerings, exclusive label prints, customized packaging and promotional packaging, among other trends, call for shorter artwork changeover times and reduced minimum quantity orders, a scenario where digital printing becomes an ideal choice, allowing for high-quality images, color accuracy, faster drying or curing and consistent ink performance on high-speed printing systems.

This trend affects such applications as packaging, labeling, e-commerce packaging, DTG Printing, and industrial coding/Marking more than others as speed, customizing capabilities, and design agility become crucial determinants of customer competitiveness. Digital inks are thus becoming essential for the implementation of variable data printing, QR code prints, product serializing and unique graphics on product SKUs. Manufacturers that can provide ink solutions optimized for specific printheads, substrates and applications will benefit most from rising consumer demands.

High Formulation Complexity and Printhead Compatibility Challenges Across Digital Printing Platforms

The Global Digital Inks Market is bound by the challenge of technical difficulties encountered in designing ink systems that can perform reliably with varying digital printing technologies. Digital inks must be formulated with precise standards for viscosity, surface tension, pigment suspension, particle size, drying characteristics, reaction to curing and chemical stability. Any slight variance in formulation can impact nozzle functionality, droplet creation, color output, adhesion and longevity. The process is harder than developing conventional inks, particularly when it comes to textiles, flexible packaging, labels, ceramics, décor and industrial surfaces.

Another challenge is Printhead Compatibility, which adds another layer of difficulty in using digital inks. The ink system should be tailored to a particular type of piezoelectric, thermal inkjet and electrophotographic platform and should be designed not to clog the nozzles, form mist, create satellite droplets, cure unevenly and ensure consistent jetting despite fast speeds. Such a challenge means more qualification periods and higher switching cost for customers and increased research and development effort for suppliers.

Segmentation Analysis

The Global Digital Inks Market is segmented based on the ink type, curing type, VOC level, bio-based content, printing technology, resin type, application/use case, substrate, and end-use industry, and region.

Solvent-Based Ink Strength and On-Demand Textile Printing Creating Segment Momentum

Solvent-based inks remained the dominant segment in 2025, with an estimated market value of US$ 1.42 billion, representing approximately 32.6% of the global market. The segment’s leadership is supported by strong adoption in wide-format graphics, outdoor signage, plastic films, flexible packaging and durable substrate printing, where adhesion strength, weather resistance, drying speed and print durability remain critical buyer requirements. Solvent-based inks continue to serve applications that require long-lasting image quality, strong surface bonding and reliable performance across challenging print environments.

Digital textile printing is expected to be the fastest-growing segment during 2026-2035, with an estimated CAGR of 9.3%. Growth is driven by rising demand for on-demand apparel production, fashion customization, direct-to-garment printing, short-run fabric design and reduced inventory-led textile manufacturing. The segment is also benefiting from increased adoption of pigment-based, water-based and low-impact digital textile ink systems, as textile producers and fashion brands shift toward flexible, faster and more sustainable production models.

Geographical Penetration

Asia-Pacific Dominance Anchored in High-Volume Packaging, Textile and Industrial Digital Printing Demand

The Asia-Pacific digital inks market was forecast to hold a market share of around 38.5%, which made it the largest regional market. The leading position of the market is underpinned by extensive packaging conversion, textile printing, label printing, consumer goods production and increased penetration of digital printing solutions in countries such as China, India, Japan, South Korea and Southeast Asian countries. High demand for flexible packaging applications, e-commerce packaging, apparel printing, signs printing, electronics marking, and other applications drives continued growth in digital ink usage in the region.

Sustainability, customization and technology migration have become drivers of growth in the Asia-Pacific market. Packaging converters and textile printers utilize water-based, UV-curable, LED-UV curable, latex and low-VOC digital inks, in order to facilitate short runs, fast turnarounds, customization and greener production processes. The use of water-based and eco-friendly digital inks in the region helps companies to reduce costs and improve efficiencies. Japan and South Korea add value via advanced printheads, electronic and precise printing technology ecosystems, while India and Southeast Asia are driven by the development of packaging, textile and graphics markets.

U.S Digital Inks Market Trends

The U.S. Digital Inks Market is being shaped by the rapid shift toward e-commerce packaging, digital labels, signage, and short-run commercial printing. U.S. Census Bureau data shows that e-commerce sales accounted for 16.9% of total retail sales in Q1 2026, while the Q1 2026 e-commerce estimate increased 9.8% year-on-year, creating stronger demand for variable graphics, SKU-level packaging, barcodes, QR codes, and customized labels. This supports higher consumption of digital inks that offer color consistency, fast drying, substrate adhesion, and compatibility with high-speed inkjet and wide-format printing platforms.

Technology migration is also accelerating as U.S. print service providers invest in UV, LED UV, latex, solvent, and water-based digital ink systems for faster turnaround and lower-emission production. Epson’s newer SureColor eco-solvent platform uses an 11-color ink set, including red, orange, and green, to improve color gamut and signage output quality, reflecting the premiumization of digital graphics workflows. Demand is increasingly concentrated around sustainable inks, low-odor formulations, printhead reliability, and application-specific performance across packaging, labels, textiles, display graphics, and industrial marking.

Japan Digital Inks Market Outlook

The Japan Digital Inks Market is positioned as a high-value, precision-led market supported by advanced inkjet technology, digital label production, packaging innovation, commercial graphics and industrial printing applications. Demand is shaped by Japan’s strong manufacturing base, quality-sensitive brand owners and established printing ecosystem, where buyers prioritize color consistency, printhead reliability, substrate adhesion, low-odor performance and compliance-ready ink systems. Digital inks are increasingly relevant across packaging, labels, signage, textiles, electronics marking and specialty industrial printing, where short-run flexibility and high-definition output are becoming more important.

Japan’s digital inks market is further supported by expanding digital commerce and packaging requirements. METI reported that Japan’s domestic B-to-C e-commerce market reached 26.1 trillion yen in 2024, while B-to-B e-commerce reached 514.4 trillion yen, reinforcing demand for digitally printed packaging, variable labels, QR-enabled branding and customized product identification. Suppliers offering water-based, UV-curable, LED UV-curable, low-VOC and high-precision inkjet formulations are well-positioned as Japanese converters and print providers focus on sustainability, traceability, flexible production and premium print quality.

Competitive Landscape

The Global Digital Inks Market is moderately consolidated, with competition led by global ink specialists, digital printing technology companies and application-focused textile and industrial ink providers. Key players such as DIC Corporation, SAKATA INX CORPORATION, artience Co., Ltd., Siegwerk Druckfarben AG & Co. KGaA, Flint Group and FUJIFILM Corporation hold strong positions through broad formulation capabilities, packaging and label ink portfolios, regional manufacturing networks and technical support for high-speed digital printing systems. These companies are competing on printhead compatibility, color consistency, curing efficiency, adhesion performance, low-migration compliance and sustainability-led ink innovation.

The competitive intensity is also increasing from specialized and equipment-linked players such as Agfa-Gevaert Group, Nazdar Company, Marabu GmbH & Co. KG, DuPont, Seiko Epson Corporation, HP Inc., Electronics for Imaging, Inc., Kornit Digital Ltd. and Archroma. Their strength lies in wide-format graphics, textile digital printing, latex inks, pigment inks, UV inks, printer-integrated ink systems and specialty substrate applications. Going forward, market leadership will depend on customized digital ink development, OEM partnerships, low-VOC and water-based platforms, regional supply reliability and the ability to support packaging, labels, textiles and industrial printing with application-specific performance.

Recent Developments

- April 2026: Kornit Digital Ltd. launched Atlas MATRIX powered by Karbon Shield technology, strengthening digital textile printing for cotton, polyester and blended fabrics while supporting on-demand apparel production.

- February 2026: Mutoh America, Inc. launched the HydrAton 1642 printer using FUJIFILM Corporation’s AQUAFUZE ink technology, supporting low-VOC, low-odor and hazard-free wide-format digital printing applications.

- February 2026: Agfa-Gevaert Group showcased its Jeti Tauro H3300 UHS at FESPA 2026, reinforcing UV inkjet adoption across high-speed wide-format graphics, display and industrial digital printing.

- October 2025: Sun Chemical Corporation, a member of the DIC Group, showcased Streamline Toccata aqueous inks for poster printing and corrugated display applications, supporting water-based digital ink adoption in sustainable graphics and display printing.

- September 2024: DuPont showcased its Artistri PN1000 ink series, a low-viscosity, water-based pigment inkjet ink for commercial printing, supporting broader adoption of water-based digital ink systems.

- September 2024: Seiko Epson Corporation introduced the SureColor S9170 solvent printer with an advanced 11-color ink set, improving color gamut and print quality for signage and graphics applications.

- March 2024: Kornit Digital Ltd. introduced NeoPigment Vivido ink, designed to deliver deeper blacks and richer colors in pigment-based digital textile printing.

AI Impact Analysis

The introduction of AI technologies into the market is transforming the Global Digital Inks Market through improved formulation, color management, print quality monitoring, and production processes. Ink providers are deploying AI technologies in pigment dispersion, viscosity analysis, curing mechanism, adhesion properties, and nozzle compatibility in order to enhance their ink formulas and to develop water-based, UV-curable, low migration, latex and specialty digital inks. This results in minimizing waste of time and resources during product development and enables rapid innovation of such products in the market.

AI solutions are being applied by printers to streamline downstream operations, including automatic color correction, defect detection, predictive maintenance, and workflow optimization. Digital printers can decrease ink consumption, ensure batch consistency, minimize machine idle times, and optimize short-run and variable data print projects. For consumers, AI-driven ink and print systems provide more reliable and sustainable services. For providers, AI offers an edge in the market through customized product design, high standards of technical services, and performance-driven sales in high-speed digital printing.

White Space Opportunities

Opportunities in the Global Digital Inks Market exist in sustainable ink systems and application-specific ink systems, especially in water-based digital inks, low VOC digital inks, latex digital inks, low migration digital packaging inks, and bio-based digital inks. As end users transition to green production methods, ink manufacturers have an opportunity to differentiate based on ink systems offering both compliance, versatile substrates, superior color reproduction, and lower environmental footprint. Opportunities are developing in digital packaging due to the demand for short-run production, variable data printing, personalized SKUs, and e-commerce packaging.

There are further opportunities in the development of custom formulations for specialty digital inks in the fields of industrial printing, security printing, decoration, electronics, ceramics, and high-performance textiles. Specialty digital inks require specialized characteristics, including scratch-resistant inks, chemical resistance, conductivity, anti-counterfeiting capabilities, wash resistance, and non-traditional substrates. Ink manufacturers that invest in developing customized inks, optimizing ink-jet printers, utilizing AI in color control, and forming partnerships with OEMs will have access to niche opportunities outside commodity printing inks.

DMI Opinion

Based on the DataM analysis, the Global Digital Inks Market is evolving from a volumetric consumption-driven product line into one dominated by performance-based specialty materials. The highest growth potential exists in areas where print quality and speed in addition to regulatory compliance, become key determinants for brand competition. The sectors where this holds true include packaging, labels, flexible packaging, food & beverage, pharmaceuticals, personal care, and e-commerce packaging. The buyer evaluation process in these categories is evolving away from pricing considerations to include considerations related to printhead compatibility, substrate compatibility, drying/curing time, color accuracy, migration, VOCs, durability, and technical assistance.

DMI forecasts sustainability and digitization to be the drivers of competitive success through 2030. Water-based, low-VOC, bio-based, UV-curable, LED UV-curable, low-migration and specialty digital ink systems are gaining relevance as converters and brand owners respond to recyclability goals, food-contact requirements, shorter production runs and personalized packaging demand. Companies with strong formulation capabilities, regional supply reliability, application-specific technical service and advanced color management support will be better positioned to capture long-term value in the evolving digital inks ecosystem.

Why This Report Matters in 2026?

Strategically, 2026 will see the rise in importance of the Global Digital Inks Market since printers involved in packaging conversion, textile printing, labels and digital industrial printing are moving away from long-run conventional printing processes to short-run fast-printing operations. The rising demand for personalized packaging, variable data printing, digital labels, e-commerce packaging and on-demand textile printing is boosting the demand for ink systems which ensure compatibility with printheads, stability of colors, curing time, substrate adhesion and uniform performance during high-speed printing through digital technology.

This report is essential since buyers have started judging inks in terms of performance, compliance and environmental sustainability rather than their prices alone. Water-based inks, VOC-free inks, UV and LED curable inks, low migration packaging inks and textile pigment inks are taking significance in light of increased emphasis on safer packaging materials, reduced carbon footprint and adaptable manufacturing processes. This report provides insight to companies that manufacture digital inks, converters and even investors by highlighting the areas of potential business opportunity and competitive advantages.

Why Choose DataM?

- Value Chain Analysis of Digital Inks: Extensive analysis of the digital inks value chain that includes pigments, dyes, resins, solvents, additives, ink formulation, printhead compatibility, ink cure systems, substrates, digital ink OEMs, converters, package makers, textile printers and label manufacturers.

- Digital Ink Technology Assessment: Comprehensive analysis of various digital ink technologies, such as water-based inks, solvent-based inks, oil-based inks, latex inks, UV curable inks, LED UV inks, electron beam inks, pigment ink for textiles, low migration ink technology and specialty inkjet ink.

- Applications and Use Case Analysis: Analyzing digital ink use case and application potential for packaging and labels & tags, commercial printing applications, publication printing, decorative printing, textile printing, security printing and industrial printing, especially for short-run and variable-data printing.

- Substrate Suitability Testing: Assessing digital ink performance and capability on substrates such as paper and paperboard, films, textiles, glass and ceramic, metal and wood substrates, including adhesion, dry time, print quality, rub resistance, print durability and nozzle stability.

- Regulatory, Sustainability and Compliance Evaluation: Evaluation of the impact of regulatory factors including food contact safety, low migration, VOC emissions reduction, odor, recyclability, solvents reduction, hazardous substances reduction and sustainability-driven branding on the usage of digital ink.

- Competitive Strategy Benchmarking: Benchmarking of key competitors including DIC Corporation, SAKATA INX CORPORATION, artience Co., Ltd., Siegwerk Druckfarben AG & Co. KGaA, Flint Group and FUJIFILM Corporation using criteria of portfolio breadth, digital ink technology, sustainability, market presence, customer service capabilities and the ability to serve packaging, label, textile and industrial digital printing needs.

- Procurement and Supplier Evaluation: Prioritization of procurement criteria based on printhead compatibility, batch uniformity, substrate capability, curing, color, technical assistance, equipment compatibility, supply chain integrity, price stability and supplier evaluation and qualification.

- Growth Opportunities and Product Development: Identification of areas for growth in digital ink products such as water based digital inks, UV and LED UV digital inks, Latex inks, Textile Pigment inks, low migration inks for packaging applications, sustainability focused inks, label inks, packaging inks, industrial inkjet inks and specialty inks for premium substrates.

Key Procurement Priorities and Buyer Evaluation Criteria

- Buyers in the Global Digital Inks Market are prioritizing ink formulations that deliver high-resolution print quality, color stability, strong substrate adhesion, printhead compatibility, fast drying or curing, rub resistance, low odor and consistent performance across high-speed digital printing systems.

- Procurement decisions are increasingly centered on digital ink systems that support inkjet, electrophotography, digital textile, digital label and digital packaging printing, enabling converters and print service providers to manage short runs, variable data printing, personalization and faster design changeovers.

- Packaging converters, label printers, textile printers, commercial print providers and industrial printing users evaluate suppliers based on ink chemistry, viscosity control, droplet formation, nozzle reliability, curing efficiency, substrate compatibility, food-contact safety, low-migration compliance, VOC profile and batch-to-batch consistency.

- Vendors with strong portfolios in water-based digital inks, UV-curable inks, LED UV-curable inks, latex inks, textile pigment inks, low-migration packaging inks and customized digital ink formulations are better positioned to secure long-term supply contracts as buyers shift toward quality-driven, sustainable and equipment-compatible printing solutions.

Related Reports

The digital inks market is closely linked to developments in packaging, printing technologies, specialty chemicals, labeling solutions, and industrial manufacturing. As businesses increasingly adopt digital printing for customization, sustainability, and operational efficiency, understanding adjacent markets becomes essential for identifying new growth opportunities and competitive advantages. Explore the following related reports to gain deeper insights into the technologies and industries shaping the future of digital printing.

Packaging Inks Market

Packaging inks play a critical role in food packaging, consumer goods, pharmaceuticals, and e-commerce packaging applications. Growing demand for sustainable packaging and high-quality print solutions continues to drive innovation across the packaging inks industry.

Printing Inks Market

The printing inks industry encompasses commercial printing, publication printing, packaging, labels, and industrial applications. Advancements in ink formulations, color technologies, and digital printing systems are creating new opportunities for ink manufacturers worldwide.

Textile Printing Market

Digital textile printing is revolutionizing apparel and fashion manufacturing by enabling on-demand production, mass customization, and reduced environmental impact. The increasing adoption of digital textile printing technologies is driving demand for specialized digital inks.

Flexible Packaging Market

Flexible packaging continues to gain market share due to its lightweight design, convenience, and sustainability benefits. Digital printing technologies are increasingly used in flexible packaging production to support short-run printing, personalization, and faster product launches.

Labels Market

The labels industry is rapidly evolving with growing demand for smart labeling, variable data printing, product authentication, and track-and-trace technologies. Digital inks enable high-resolution label production across food, beverage, pharmaceutical, and logistics sectors.

Specialty Chemicals Market

Digital ink manufacturing relies heavily on advanced pigments, resins, additives, and specialty chemical formulations. Innovations in specialty chemicals continue to improve print quality, durability, sustainability, and substrate compatibility across digital printing applications.

Industrial Printing Market

Industrial printing applications are expanding across automotive, electronics, construction materials, ceramics, and product decoration. Advanced digital inks are enabling manufacturers to improve production flexibility, customization, and operational efficiency.