Water Proofing Membrane Market Overview

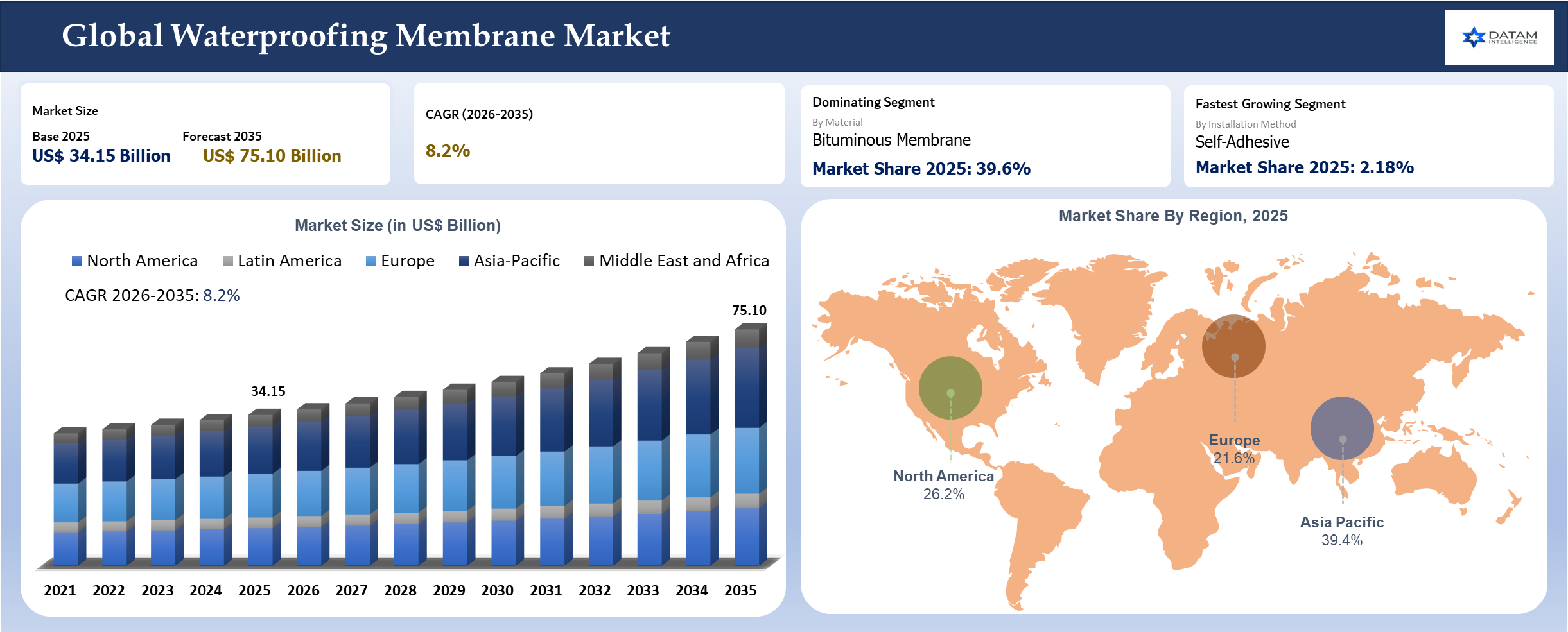

The global waterproofing membrane market reached US$ 34.15 billion in 2025 and is expected to reach US$ 75.10 billion by 2035, growing with a CAGR of 8.2% during the forecast period 2026-2035. The waterproofing membrane market is moving away from broad category selling and toward more exact specification decisions. Buyers are comparing solutions against operating pain points that can be measured in quality drift, downtime exposure, crop outcome, logistics damage, route stability or project delay. Premium suppliers are winning when they can show how their offer removes a visible bottleneck rather than simply adding another product option to a crowded market.

Commercial logic in this market is becoming more selective. Procurement teams, technical teams and operating teams are not valuing the same thing at the same time. Strong suppliers, therefore, need a proposition that works on more than one level. Product capability still matters. Service support, documentation quality, application fit and future adaptability now matter almost as much because the cost of getting the decision wrong is rising.

As per our analysis, the market is also becoming more segmented by consequence rather than by volume alone. High-value pockets are forming where performance variation creates immediate financial impact. Niche subsegments that once looked too small to matter are now influencing margin, customer retention and capital allocation because they attract the strictest buying criteria and the strongest switching barriers.

Revenue formation is therefore strongest where specification intensity is high and where underperformance is expensive. A solution that protects uptime, quality, traceability, premium crop output, safer grid connection or lower load damage can hold pricing better than a generic alternative. Commercial winners in this market will be the suppliers that connect product architecture to practical field outcomes and can still scale that advantage through dependable delivery.

Waterproofing Membrane Industry Trends and Strategic Insights

- Highest-value demand is forming in technically demanding pockets where switching risk is high and performance failure is expensive.

- Supplier advantage is shifting toward application fit, service depth and documentation quality rather than broad portfolio size alone.

- Future share gains will come from markets and use cases where buyers can price the operational payoff more clearly than the initial premium.

Market Scope

| Metrics | Details | |

| 2025 Market Size | US$ 34.15 Billion | |

| 2035 Projected Market Size | US$ 75.10 Billion | |

| CAGR (2026-2035) | 8.2% | |

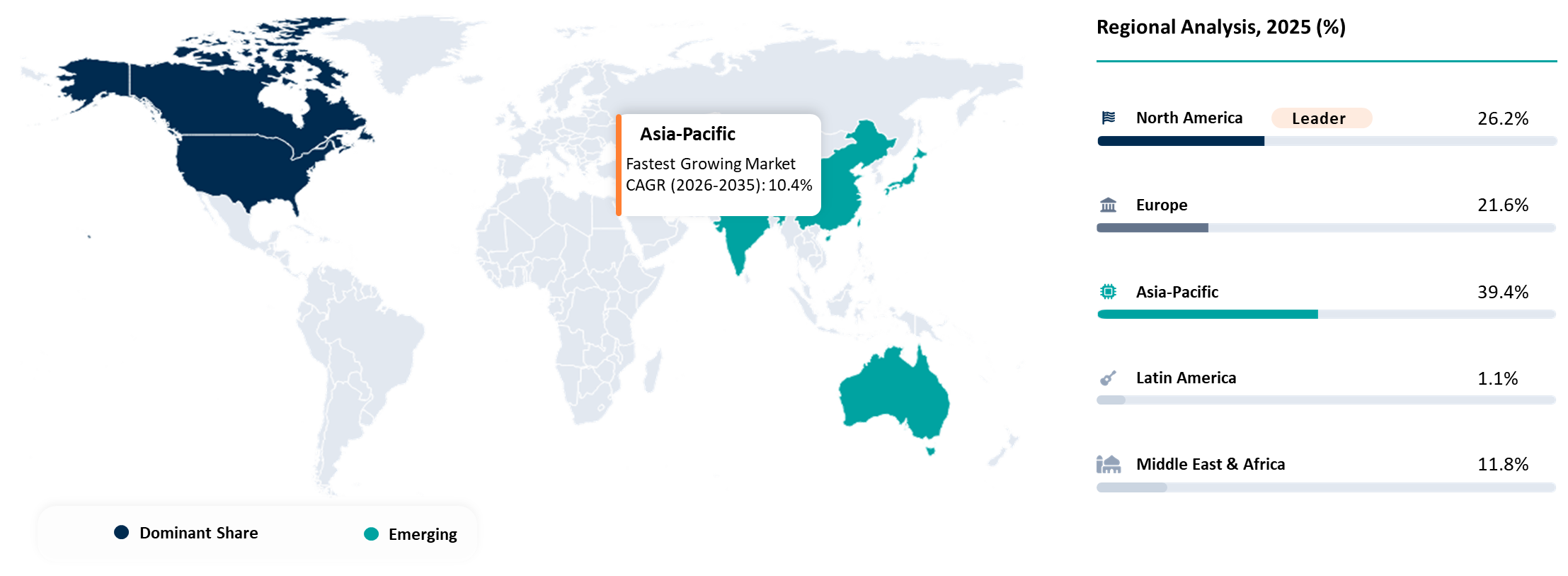

| Largest Market | Asia-Pacific | |

| Fastest Growing Market | Asia-Pacific | |

| By Material | Bituminous Membranes, PVC Membranes, TPO Membranes, EPDM Membranes, HDPE Specialty Membranes, LDPE Membranes, CPE Membranes, PU Liquid-Applied Membranes, Acrylic Liquid-Applied Membranes, Cementitious Waterproofing Membranes, Reinforced Liquid-Applied Systems and Others | |

| By Membrane Type | Sheet-Based Membranes, Liquid-Applied Membranes, Hybrid Waterproofing Systems and Others | |

| By Installation Method | Torch Applied, Self-Adhesive, Mechanically Fastened, Fully Adhered, Loose Laid Systems, Spray Applied, Roller Applied, Brush Applied, Heat Welded and Others | |

| By Project Cycle | New Build, Refurbishment, Reroofing, Infrastructure Rehabilitation, Long-Life Asset Protection, Repair and Maintenance and Others | |

| By Structure Type | Buildings, Transport Infrastructure, Water Infrastructure, Energy and Industrial Facilities, Environmental Containment Structures and Others | |

| By Performance Requirement | UV Resistant Membranes, Chemical Resistant Membranes, Root Resistant Membranes, High Puncture Resistance Membranes, High Flexibility Membranes, High Temperature Resistant Membranes and Others | |

| By Application | Roofing, Below Grade, Walls and Facades, Wet Areas, Podium Decks and Plaza Decks, Balconies and Terraces, Tunnels and Civil Infrastructure, Bridges and Highways, Water and Wastewater Structures, Landfills and Containment Structures and Others | |

| By End-User | Residential, Commercial, Industrial, Infrastructure and Institutional | |

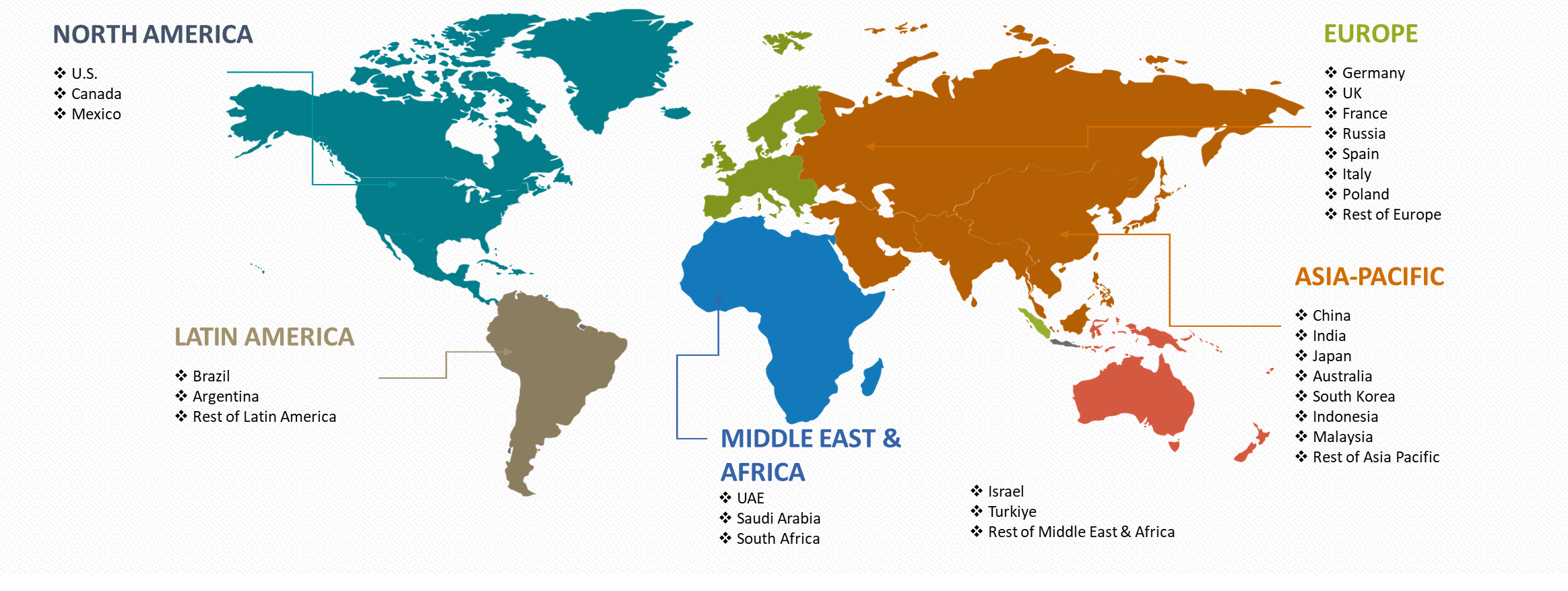

| By Region | North America | USA, Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

AI Is Improving Waterproofing Decisions Through Predictive Project Intelligence

AI is beginning to influence the waterproofing membrane market through decision support rather than through marketing language. Data-rich operating environments are giving buyers better ways to spot drift, predict service needs and compare how one specification choice affects total performance. Sites that already generate process or usage data can now translate more of that data into practical commercial choices.

Predictive planning is the most immediate value layer. Maintenance schedules, quality deviations, crop-response models, route optimization or formulation drift can all be evaluated earlier when analytics sit closer to the operating process. Faster visibility lowers the hidden cost of failure and improves confidence in premium decisions that once looked harder to justify.

A second impact sits in commercial positioning. Suppliers that combine physical product with stronger insight can defend premium pricing more effectively because they are not selling hardware, chemistry or ingredients alone. Buyers can see how the offer lowers waste, protects throughput, reduces callouts or supports auditable compliance in real conditions. The best AI opportunities are concentrated in repetitive, measurable decisions. Markets in this workbook do not need digital theater. Buyers need a clearer path from signal to action. AI tools that shorten that path will create real value, while superficial dashboard layers will struggle to hold attention.

Disruption Analysis

Outcome-Based Selling Is Reshaping Waterproofing Membrane Competition

The biggest disruption in the waterproofing membrane market is the move from product-led competition to outcome-led competition. Buyers want a clearer line between specification choice and a commercial result they can defend. Product quality still matters, yet it is no longer enough when implementation complexity, service burden or integration risk can erase the apparent advantage of a superior option.

Procurement behavior is also changing. Technical teams, sustainability teams, finance leaders and operators now influence the same decisions in many projects. A supplier can lose even with strong core performance if the offer introduces route risk, weakens supply continuity or makes future expansion harder. Multi-stakeholder evaluation is raising the bar for market entry and helping disciplined suppliers protect their share.

Channel structure is shifting as well. Digital discovery, advisory selling and service-linked contracts are moving value away from one-time transactions. Optimization support, retrofit programs, co-development and monitoring layers are becoming more important because buyers increasingly want lower implementation risk and clearer lifetime economics.

As per our analysis, disruption will favor companies that understand where the market is getting more technical and where it is getting more service-led. Volume-led vendors that remain dependent on generic category language are likely to face weaker pricing power as buyers become more selective and more evidence-driven.

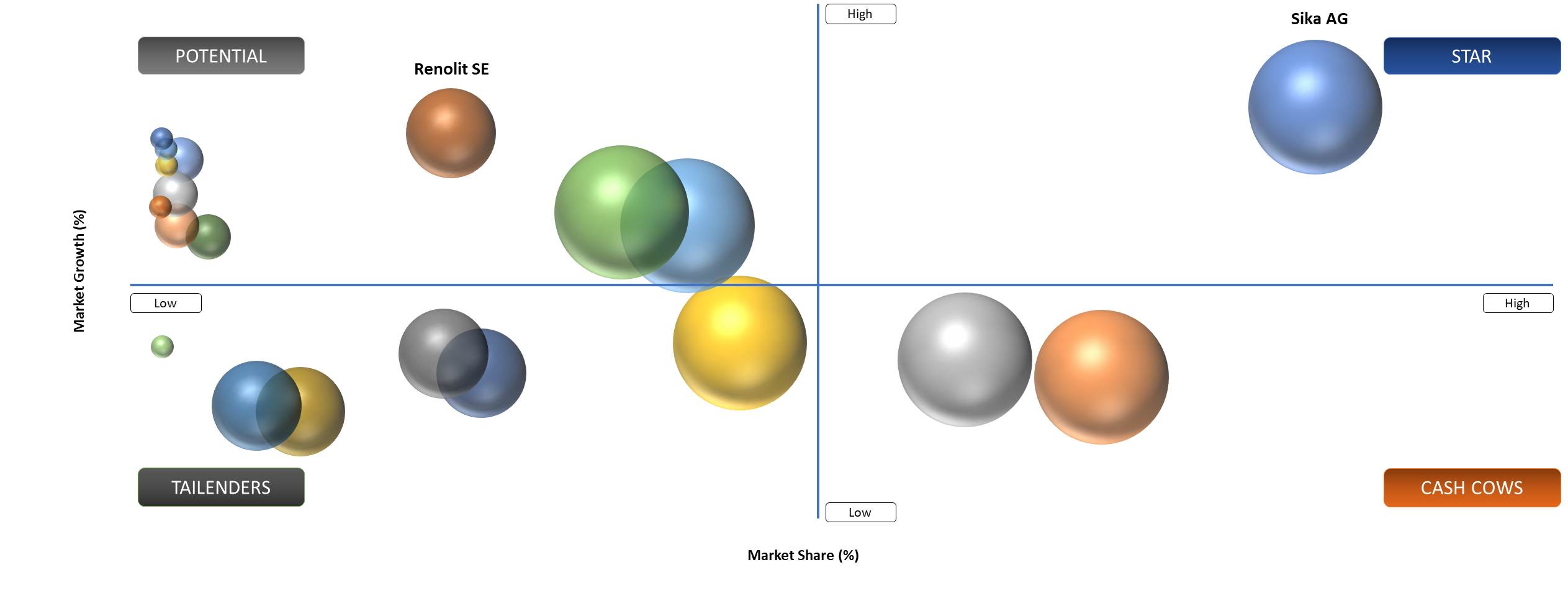

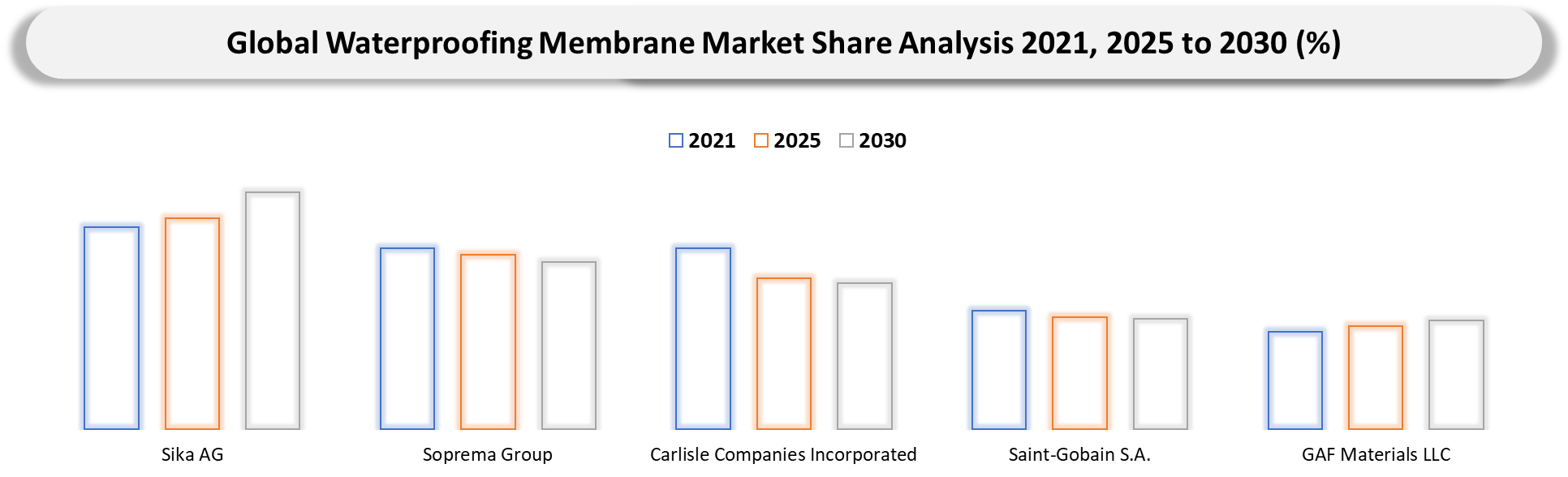

BCG Matrix: Company Evaluation

Stars in the waterproofing membrane market are Sika AG and Soprema Group because both companies combine scale with credible technical positioning in the part of the market where revenue quality is strongest. Leadership is not only about size. Leadership in this market depends on whether a supplier can support demanding specifications, keep delivery dependable and remain relevant when customers move from trial use to multi-year commercial rollout.

Potential players include Oriental Yuhong Waterproof Technology Co., Ltd. and Renolit SE because both are linked to narrower high-value niches or faster-moving regional opportunities. Share gains are possible when niche players offer sharper specialization, stronger local alignment or a better technical answer to a new use case. Scale, validation depth and longer customer relationships still need to be strengthened before these companies can move into the strongest leadership band.

Market Dynamics

Specific operating pain points

Buyers are not moving toward better solutions because the category is fashionable. They are moving because hidden losses from quality inconsistency, supply volatility, downtime, leakage, poor fitment, crop damage or project delay have become harder to absorb. A higher-spec option becomes commercially attractive when the current choice is already creating measurable waste elsewhere in the chain.

Operating complexity is also changing what buyers call value. Teams that once optimized purely for upfront purchase price are now comparing maintenance demand, quality risk, throughput effect, traceability, installation difficulty and future expandability. Better decisions are being justified by fewer disruptions rather than by lower ticket prices. The shift is especially important where one failure can damage an export program, a construction schedule, a logistics network or a critical infrastructure asset.

Market demand is further supported by the fact that many legacy systems and legacy buying habits are no longer well aligned with present operating realities. Higher standards, tighter labor availability, cleaner-label pressure, energy-transition needs, faster customization and stronger sustainability reporting are all increasing the value of products that solve a clearly defined commercial problem. Buyers do not need more options. Buyers need lower failure risk and stronger predictability.

As per our analysis, the strength of this driver will continue because it is tied to structural change rather than temporary sentiment. Markets shaped by traceability, quality control, route stability or capital efficiency tend to reward solutions that remove operational friction. Suppliers that can prove this payoff with evidence, customer examples or measurable service outcomes will keep widening the gap from generic competitors.

Execution complexity

Commercial logic may look strong on paper, while conversion still slows at the point of rollout. Many projects involve more than one decision-maker and more than one process step. A buyer may support the technical case but still hesitate when installation disruption, validation work, process tuning or supply continuity looks difficult to manage at the same time.

Qualification risk deepens the problem. Premium solutions often require stronger documentation, species-specific validation, route studies, installer quality, fitment confidence, feed trial evidence or performance testing before adoption can scale. Approval cycles, therefore, stretch longer than expected and some customers postpone change even when they agree that the current setup is underperforming.

Commercial restraint is stronger when the surrounding ecosystem is not ready. Utilities may need upgrades. Installers may lack training. Procurement teams may still value the category through commodity logic. Regional supply may be too narrow. Each of these factors can slow a market that looks fundamentally attractive from a high level.

Progress is therefore usually fastest when suppliers reduce uncertainty rather than simply restating the business case. Pilot support, phased deployment, application guidance, better documentation and stronger after-sales service can remove friction. Vendors that fail to close that execution gap will continue to lose deals even when product merit is obvious.

White Space Opportunities

High-Value Waterproofing Applications Are Creating Untapped Growth Pockets

The most potent white space opportunities lie in EV battery cases, crash management solutions and lightweight chassis parts. EV producers must keep their vehicles light, yet safe, thermally controlled and manufacturable. While aluminum is ready for immediate use, magnesium and advanced alloys could be further developed in certain applications where reduced weight justifies increased engineering investment.

Another white space opportunity lies in low-carbon aluminum and recycled aluminum. The automotive, packaging and construction markets face strong demands to minimize carbon footprints. As such, recycled content aluminum and low-carbon primary aluminum offer significant commercial potential. Providers who can verify their low carbon footprint and supply consistent mechanical properties will get preferred contracts.

A third white space exists in titanium for medical, aerospace and defense localization. Supply security has become more important for high-performance Materials. Regional titanium processing, qualified inventory programs and specialty mill products can gain traction where customers want reduced geopolitical and logistics risk. A fourth white space is in magnesium alloys used in structural parts for electronic equipment and transport. The lighter housing of laptops, cameras, drones, electric vehicles and even defense mechanisms leave spaces for magnesium alloy suppliers to fill in their difficulties.

DMI Opinion

Waterproofing Membrane Growth Will Depend on Performance, Proof and Application Suppor

According to the DataM analysis, the global market for waterproofing membrane is not something that can be compared against a generic materials market. The business models for aluminum, magnesium and titanium Materials are different due to their revenue logic. For instance, aluminum is the best choice for the largest market opportunity due to its wide use in automotive vehicles, electric cars, food packaging, building constructions and various industries. Titanium is the best choice for creating high-value-added products in aerospace, military, medical and corrosion-resistant applications. Magnesium offers an opportunity with high risks and high potential rewards in electric cars, electronics and advanced lightweight components.

The future of the market belongs to companies that offer more than Material supply. Customers prefer waterproofing membrane that are available in the required form, approved for specific purposes, documented properly and sustainable.

As per DataM, the future growth of the market will be driven by consumers who consider waterproofing membrane not just materials, but performance enhancers. Demand will be influenced by automotive lightweighting, range enhancement for EVs, aircraft efficiency, medical implants’ performance, electronics miniaturization and carbon-free construction. Aluminum will continue to lead the pack in terms of volume, titanium will remain the performance Material of choice, while magnesium will remain pivotal in watch technology.

Segment Analysis

Aluminum Dominates Volume, While Magnesium and Titanium Define High-Value Growth Pockets in the Waterproofing Membrane Market

Bituminous membranes continue to be commercially relevant as they are tied very tightly with the most significant and quantifiable demand pool in the market. The use of bituminous membranes by contractors and purchasers is preferred for waterproofing efficacy, ease of installation and integration with the existing workflow of projects. Good performance by suppliers in this market segment hinges on consistent product offerings, good contractor cooperation, strong project execution abilities and ability to prove efficacy in roofing, basement, bridge and tunnel projects.

PVC membranes are aimed at buyers looking for specialty and higher-end waterproofing membranes. This product category enjoys more demand in situations were flexibility, chemical resistance, durability, lightweight design or roof membrane properties matter. Customer buying behavior is generally quite selective in this market segment as they carefully examine technical documents, quality of installation, warranty conditions and lifetime performance before changing suppliers. It may not provide higher volumes than bituminous membranes but offers some margin potential depending on the project needs.

Application-based segmentation adds another layer of commercial understanding because membrane choice is strongly influenced by project conditions, substrate type, exposure level, installation environment and expected service life. Roofing applications generally favor products that can deliver weather resistance, thermal stability and installation efficiency across large surface areas. Below-grade applications require stronger resistance to hydrostatic pressure, soil movement, moisture ingress and long-term structural protection. As a result, suppliers must position products not only by material type but also by how each membrane performs under specific real-world construction conditions.

Roofing and below-grade applications are therefore more than technical categories. Both reflect different commercial priorities within the market. For roofing uses, most materials will be those that offer weatherproofing and stability along with ease of application in extensive coverage. Below grade applications will have requirements for greater resistance to pressure, movement, water entry and structural integrity. Thus, product positioning should include both what the membrane material is and how it performs in specific construction situations.

Geographical Penetration

Asia-Pacific Leads Volume Demand, While North America and Europe Drive Premium Lightweight Material Specification

Asia-Pacific will retain the leading position in terms of commercial significance within the waterproofing membranes industry as construction activities, infrastructural development, industrialization and real estate development will continue to drive substantial demand from the region. In recent years, there has been a trend towards the selection of products that provide better economic value in the course of their lifecycles rather than the initial purchase cost alone. An improvement in revenue quality can be observed in projects wherein all the stakeholders understand the cost of water leakage, the associated repairs and failures of the membranes.

China Waterproofing Membrane Market Outlook

In China, construction activities, infrastructural development and the adoption of high-performing waterproofing materials are key reasons for the country's importance in the industry. Local project standards and purchasing behavior can influence nearby Asian markets, making China strategically important beyond its direct revenue contribution.

India Waterproofing Membrane Market Trends

India is also becoming a major growth market because demand is supported by infrastructure development, urban housing, commercial construction, metro projects, industrial facilities and modernization of building practices. Practical deployment speed, contractor training and application support are especially important in India because project conditions vary widely across climate zones, building formats and construction quality levels. Suppliers that adapt product positioning and technical support to local project realities can gain share faster than companies using a uniform global approach.

Regional demand will continue to favor suppliers that localize execution without weakening their core product platform. The technical support available, distribution capabilities, installation competencies, project engineering expertise and specification processes may vary considerably from one country to another. The firms that recognize this and adapt their products, pricing and services will be more successful than their rivals who see Asia-Pacific as homogenous.

Competitive Landscape

- The competitive landscape is split between scale leaders with broader portfolios and specialist players that hold technical credibility in narrower pockets. Scale still matters because buyers want continuity, stronger service coverage and confidence that a supplier can support future expansion. Specialist players remain relevant where application depth, faster response or sharper localization solves a problem better than global breadth.

- Competition is becoming more layered because buyers no longer evaluate the product in isolation. Documentation quality, retrofit support, installation discipline, formulation guidance, channel control, digital visibility or validation support all shape the final decision. A supplier with a slightly smaller portfolio can still win if the customer believes execution risk will be lower after purchase.

- Another important shift is that recurring revenue and service-linked value are becoming more strategic. Maintenance, optimization, co-development, monitoring and upgrade work are influencing market share more strongly than before. Sellers that remain dependent on one-time transactions will struggle to defend premium pricing in segments where customers want a longer commercial relationship.

- As per our analysis, the strongest competitors in this workbook are the firms that can convert technical credibility into lower customer risk. Strong products open the door. Strong execution keeps the door from closing.

Key Developments

- May 2026: Carlisle Companies Incorporated reinforced its role through a launch collaboration or segment-specific initiative tied to more selective demand pockets. Market impact is meaningful because premium projects increasingly favor suppliers that can pair product depth with stronger support.

- March 2026: Soprema Group highlighted market activity linked to premium segments and commercially demanding customers. Strategic importance comes from the way such moves signal where capital and technical effort are being directed as buying criteria become stricter.

- January 2026: Sika AG strengthened its strategic position through product capacity or program activity that improved visibility in higher-value specifications. Commercial relevance is high because buyers are rewarding suppliers that remove operating risk and can scale without service disruption.

- November 2025: BASF SE showcased capability enhancements relevant to more selective buying criteria. Market significance is tied to the growing premium on implementation confidence and practical field performance.

- September 2025: GAF Materials LLC advanced commercial reach through project modernization, technical support or channel activity linked to customer requirements in this market. Importance lies in stronger access to recurring and defensible demand pools.

- July 2025: Saint-Gobain S.A. reported progress that improved competitiveness in targeted programs, specialty applications or lifecycle-driven work. Development matters because revenue quality is shifting toward segments where validation and service matter more than simple volume.

- February 2025: Johns Manville expanded regional or segment activity in a way that improved its standing with customers looking for local support and faster response. Strategic value comes from the fact that regional execution now affects supplier choice more strongly.

- October 2024: Renolit SE signaled stronger competitive intent through capability-building channel expansion or targeted project engagement. Market importance rests in the shift toward differentiated and high-fit opportunities.

- August 2024: Oriental Yuhong Waterproof Technology Co., Ltd. increased visibility in emerging or specialized subsegments that are drawing stronger buyer interest. Such moves matter because small premium niches often shape future share gains before they become large-volume categories.

- June 2024: MAPEI S.p.A. strengthened its offering through product refinement, digital support or route-to-market action aligned with present customer pain points. Development is notable because established players are defending their share through deeper value delivery.

Why Choose DataM?

- Data-Driven insights: Dive into detailed analyses with granular insights such as pricing, market shares and value chain evaluations, enriched by interviews with industry leaders and disruptors.

- Post-Purchase Support and Expert Analyst Consultations: As a valued client, gain direct access to our expert analysts for personalized advice and strategic guidance, tailored to your specific needs and challenges.

- White Papers and Case Studies: Benefit quarterly from our in-depth studies related to your purchased titles, tailored to refine your operational and marketing strategies for maximum impact.

- Annual Updates on Purchased Reports: As an existing customer, enjoy the privilege of annual updates to your reports, ensuring you stay abreast of the latest market insights and technological advancements. Terms and conditions apply.

- Specialized Focus on Emerging Markets: DataM differentiates itself by delivering in-depth, specialized insights specifically for emerging markets, rather than offering generalized geographic overviews. The approach equips our clients with a nuanced understanding and actionable intelligence that are essential for navigating and succeeding in high-growth regions.

- Value of DataM Reports: Our reports offer specialized insights tailored to the latest trends and specific business inquiries. The personalized approach provides a deeper, strategic perspective, ensuring you receive the precise information necessary to make informed decisions. The insights complement and go beyond what is typically available in generic databases.

Target Audience 2026

- Manufacturers and OEMs: Companies producing systems, materials, ingredients or components linked to waterproofing membrane market and evaluating product strategy expansion priorities and competitive positioning.

- Distributors and Channel Partners: Firms managing regional sales specification support dealer networks or value-added services in this market.

- Asset Owners and Commercial Buyers: Operators, processors, building owners, utilities, farms or industrial users procuring solutions based on lifecycle economics, uptime quality or compliance needs.

- Engineering and Technical Teams: Consultants, plant managers, formulation experts, project developers or maintenance leads responsible for validating performance and implementation fit.

- Investors and Private Equity Firms: Financial stakeholders assessing margin structure consolidation potential and growth pockets in premium or underpenetrated subsegments.

- Government Regulators and Standards Bodies: Institutions shaping safety, environmental, trade, building, agricultural or quality frameworks that affect demand formation.

- Technology and Service Providers: Companies offering analytics testing retrofit support, digital tools or system-integration capabilities that complement the core market.

- Strategic Procurement and Supply Chain Leaders: Decision-makers monitoring sourcing resilience, feedstock risk, regional supply concentration and long-term supplier reliability.