Refinery Catalyst Market Overview

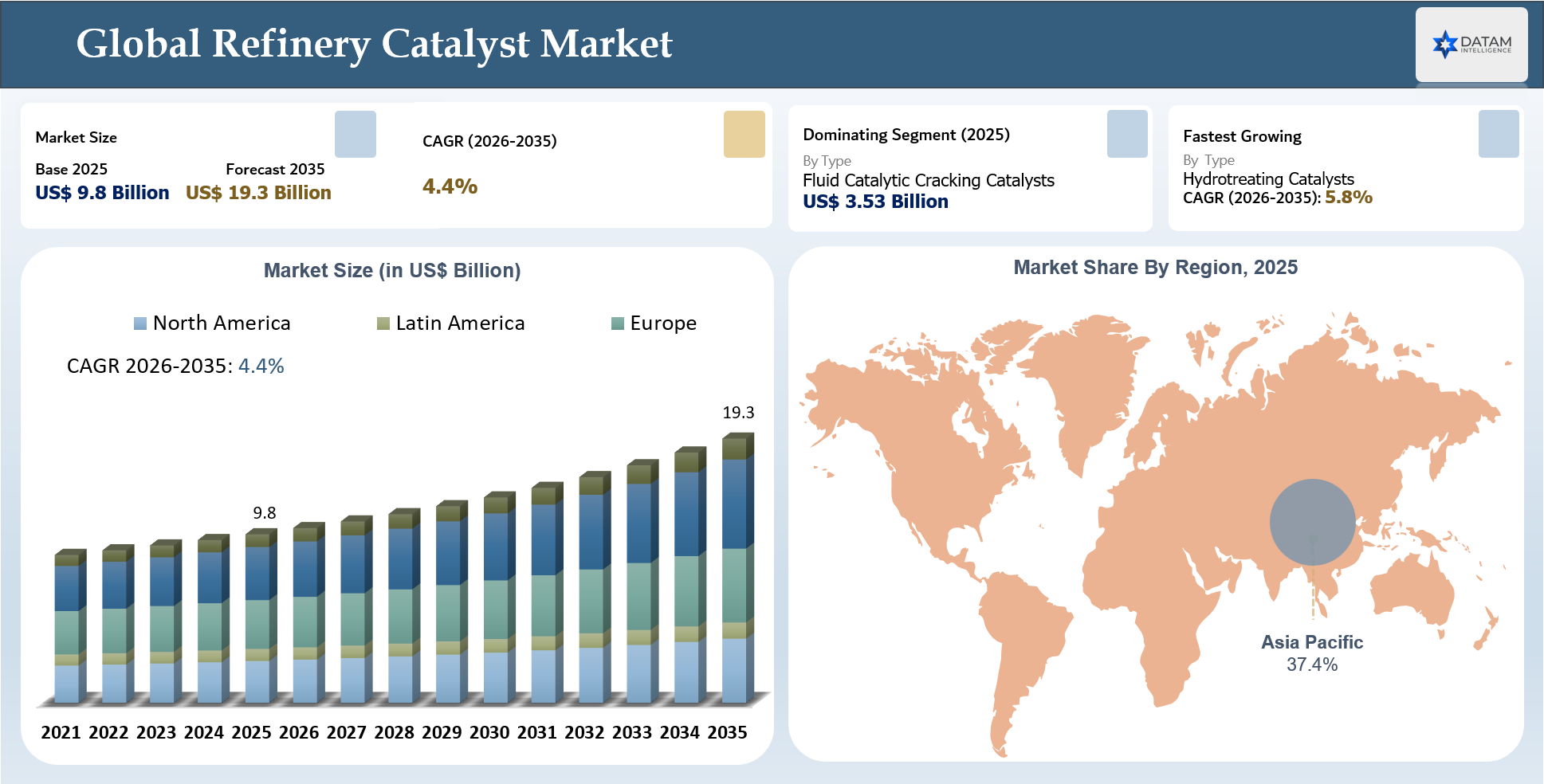

The Global Refinery Catalyst Market stood at US$ 9.8 billion in 2025 and is expected to reach US$ 19.3 billion by 2035, growing with a CAGR of 4.4% during the forecast period 2026-2035.

The Global Refinery Catalyst Market is being reshaped by the regulatory shift toward cleaner fuels, especially low-sulfur gasoline, diesel and marine fuels. This is moving catalyst procurement beyond routine replacement and making it a strategic refinery performance decision. Refiners must reduce sulfur, nitrogen, metals and aromatics while maintaining throughput, product yield and operating reliability. As a result, demand is strengthening for advanced hydrotreating, hydrocracking, FCC and sulfur recovery catalysts that can help refiners meet cleaner fuel specifications without compromising margins.

This shift is more critical for refineries processing heavier, sour and opportunity crude streams, where higher contaminant levels increase catalyst deactivation, coke formation and operational risk. Buyers are increasingly evaluating catalyst suppliers on cycle life, hydrogen efficiency, sulfur removal performance, feedstock flexibility, technical service capability and proven refinery references. The market is therefore moving toward performance-led catalyst programs, where suppliers that can improve yield, extend operating cycles, lower lifecycle cost and support compliance-driven refinery optimization are better positioned to secure long-term contracts.

Key Takeaways

- The Global Refinery Catalyst Market was valued at US$ 9.8 billion in 2025 and is projected to reach US$ 19.3 billion by 2035.

- The market is expected to grow at a CAGR of 4.4% during 2026-2035, supported by refinery modernization, cleaner fuel mandates, heavier crude processing and demand for higher-value fuel yields.

- Asia-Pacific held the highest market share at 37.4% in 2025, supported by large refinery capacity, high crude processing intensity and strong refinery-petrochemical integration across China, India, South Korea, Japan and Southeast Asia.

- Asia-Pacific is also expected to be the fastest-growing region, driven by new refining capacity additions, rising fuel demand, downstream investments and increasing adoption of FCC, hydrotreating and hydrocracking catalysts.

- Fluid Catalytic Cracking Catalysts were the largest type segment in 2025, accounting for approximately 36% of the market, valued at around US$ 3.53 billion, supported by strong use in gasoline, LPG and propylene production.

- Hydrotreating Catalysts are projected to be the fastest-growing type segment, expanding at an estimated 5.8% CAGR during 2026-2035, driven by low-sulfur fuel requirements and diesel quality improvement.

- Refiners are increasingly prioritizing catalysts that improve conversion efficiency, sulfur removal, hydrogen utilization, coke reduction, contaminant tolerance and cycle life.

- Catalyst procurement is shifting from price-based buying toward performance-led evaluation, where lifecycle cost, refinery references, technical service and yield improvement are becoming critical buyer criteria.

- The market has strong competitive concentration, with major players including BASF, Grace, Honeywell UOP, Ketjen, Shell Catalysts & Technologies, Topsoe, Axens Group, Clariant Catalysts, Johnson Matthey and Sinopec Catalyst Co., Ltd.

Market Scope

| Metrics | Details | |

| 2025 Market Size | US$ 9.8 Billion | |

| 2035 Projected Market Size | US$ 19.3 Billion | |

| CAGR (2026-2035) | 4.4% | |

| Largest Market | Asia-Pacific | |

| Fastest Growing Market | Asia-Pacific | |

| By Type | Fluid Catalytic Cracking Catalysts, Hydrotreating Catalysts, Hydrocracking Catalysts, Catalytic Reforming Catalysts, Alkylation Catalysts, Isomerization Catalysts, Sulfur Recovery Catalysts and Others | |

| By Material | Zeolites, Metals, Chemical Compounds, Alumina, Silica Alumina and Others | |

| By Feedstock | Crude Oil, Vacuum Gas Oil, Naphtha, Diesel, Heavy Oils, Residue Oil and Others | |

| By Form | Powder, Pellets, Granules, Extrudates, Beads and Others | |

| By Application/Use Cases | Gasoline Production, Diesel Production, Jet Fuel Production, LPG Production, Petrochemical Feedstock Production, Sulfur Removal, Heavy Oil Upgrading and Others | |

| By End-User | Oil Refineries, Integrated Refining and Petrochemical Complexes, National Oil Companies, Independent Refiners and Others | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

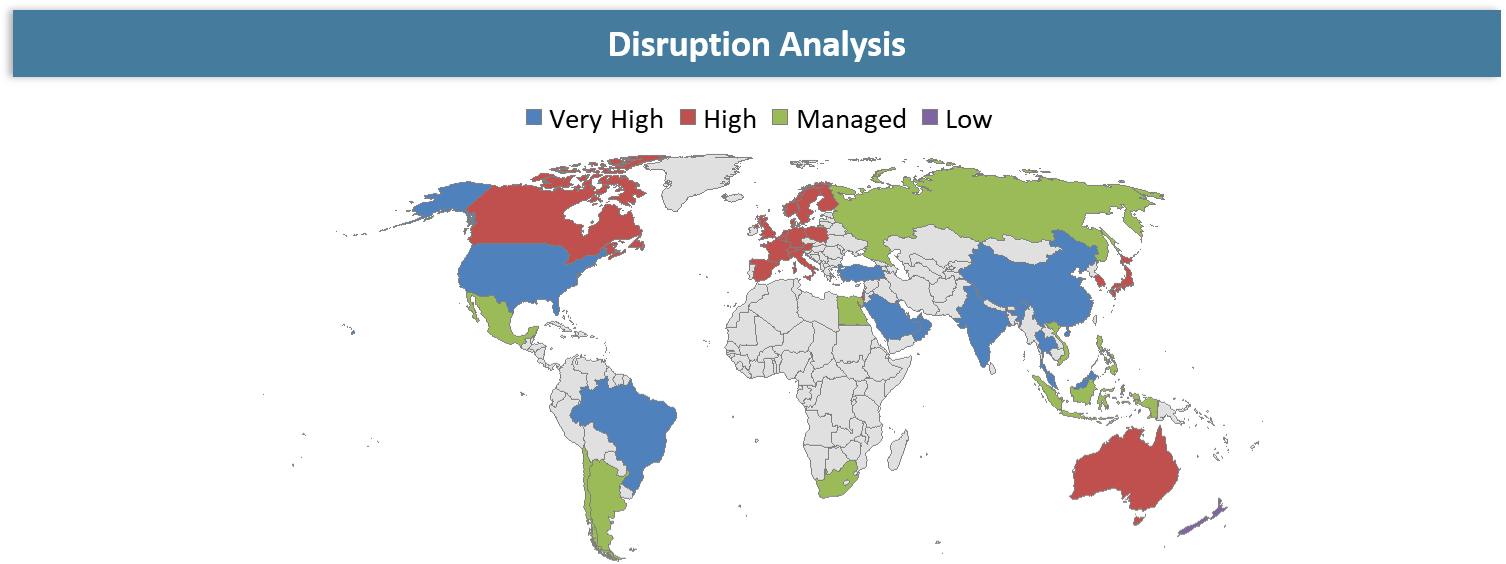

Disruption Analysis

Performance-Led Catalysts Are Redefining Refinery Profitability, Compliance and Feedstock Flexibility

Disruption in the Global Refinery Catalyst Market is resulting from the transition from volume-based refining operations to performance-based operations, where choosing a particular catalyst is responsible for affecting the yield, the quality of fuel products, their emission performance, and margin improvement. As more complex types of oil slates are processed, such as heavy and sour crudes, refiners have a greater need for catalysts that possess enhanced contaminant tolerance, cycle life, and efficiency in conversion. This is leading companies to expand beyond their offerings of catalysts to provide tailored solutions for units such as FCC, hydrotreating, hydrocracking, reforming, and sulfur recovery.

Other disruptions come through refinery-petrochemical integration, renewable fuel co-processing, catalyst regeneration, and AI-based process optimization. Refineries require catalysts that enable low sulfur fuel production, petrochemical product maximization, reduce coke formation, and improve hydrogen efficiency. As buying decisions become results-based, suppliers with strong expertise in services, process optimization through digital platforms, lifecycle cost efficiencies, and experience working in refiner settings will have a competitive advantage.

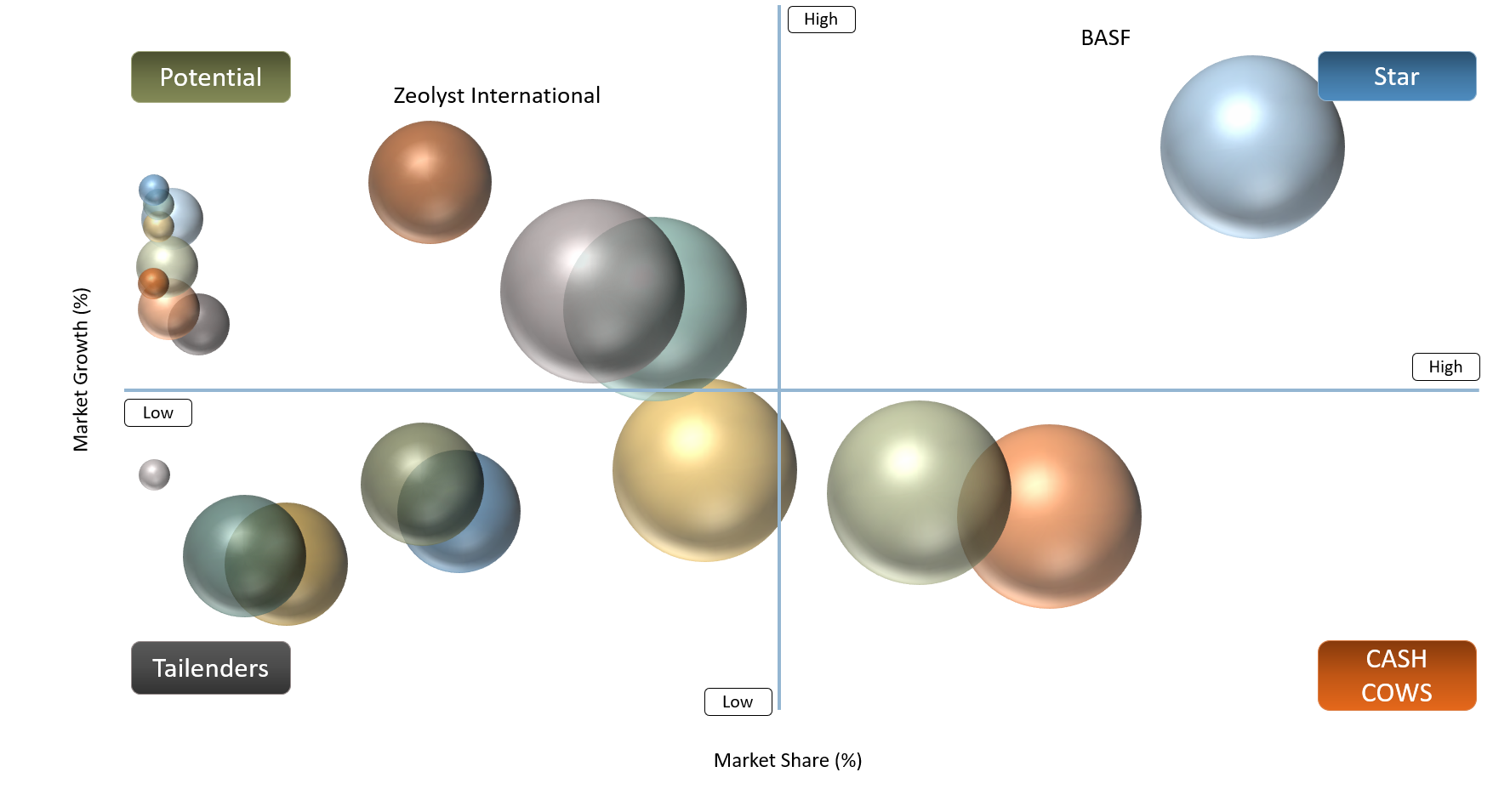

BCG Matrix: Company Evaluation

As for the BCG matrix, Star companies are those with excellent global refinery linkages, extensive range of catalysts, technical excellence and performance in FCC, hydrotreating, hydrocracking, reforming and sulfur recovery. Examples of Star companies include BASF, Grace, Honeywell UOP, Ketjen and Shell Catalysts & Technologies because of their global refinery clients, state-of-the-art catalyst technology, process expertise and excellent replacement demand, among others. The key characteristics of such firms include a robust portfolio of catalysts and refinery demand for products, high technical expertise and strong involvement in certain refinery catalyst categories.

Cash Cows are companies that have a strong position in catalyst manufacturing, good demand from refineries, high technical service capability and good participation in certain refinery catalysts. The leading companies that can be classified under the category of Cash Cows include Topsoe, Axens Group, Clariant Catalysts, Johnson Matthey and Sinopec Catalyst Co., Ltd. These companies are recognized for their experience in the manufacturing of catalysts and refinery operations.

The Question Marks are companies with relevant catalyst technologies or material capabilities but comparatively narrower refinery catalyst coverage, regional concentration or limited positioning across the full refinery process chain. JGC Catalysts and Chemicals Ltd., Zeolyst International and Evonik can be positioned as Question Marks in this market. Their future growth will depend on stronger geographic expansion, deeper integration with refinery process applications, technical partnerships, and the ability to scale catalyst solutions across high-growth areas such as hydroprocessing, FCC optimization, residue upgrading, sulfur recovery and catalyst regeneration.

Market Dynamics

Refiners Are Upgrading Catalyst Systems to Protect Margins Amid Heavier and More Variable Crude Slates

With increasing complexity and inconsistency in the quality of crude being used, there is a rise in the upgrades of catalytic systems by refineries. Many refineries use heavy, sour and opportunity crudes to lower their input expenses, yet such crudes have higher amounts of sulfur, nitrogen, metal content and Conradson carbon. This puts the FCC units, hydro-treatment, hydro-cracking and residual upgrading units under strain. Refinery catalysts assist in ensuring conversion efficiency, less coke production, higher resistance to contaminants and product output despite difficult feedstocks.

In terms of business, the performance of the catalyst will soon be tied directly to margin protection at the refining facility. The ability of the catalyst to increase cycle length, improve yields of gasoline or diesel, cut hydrogen usage, or avoid downtime due to unscheduled maintenance can add value that exceeds the initial cost of the catalyst. With margins being more volatile and with stricter regulations, refineries are less inclined to procure catalysts based on price but rather on their performance. This is creating strong demand for customized catalyst systems supported by technical service, unit optimization and lifecycle performance validation.

High Catalyst Replacement Costs and Performance Validation Requirements Are Slowing Procurement Decisions

High cost of catalyst replacement continues to pose a significant challenge to the growth of the Global Refinery Catalyst Market, especially with refineries operating under slim margins due to uncertainties of crude spreads and turnaround restrictions. The selection of the appropriate catalysts by the buyer is not just a matter of purchasing consumables. It requires technical and compatibility considerations. Where high-cost process equipment like FCC, hydrotreater, hydrocracker, and catalytic reformer are involved, the buyer must exercise caution before changing from one catalyst supplier to another, or trying out different catalyst technology.

The demands for performance validation further discourage acceptance by requiring pilot testing, reference sites, simulation studies, and field-proven experience from the refiner. Underperformance means lower output, sub-standard quality fuels, unscheduled downtime, or increased cost per barrel. For that reason, purchasing cycles tend to be long, particularly among independent refineries and government-owned operators with stringent technical qualification procedures. This restraint benefits established suppliers with proven refinery references but creates barriers for newer catalyst technologies and emerging vendors.

Segmentation Analysis

The Global Refinery Catalyst Market is segmented based on type, material, feedstock, form, application/use cases, end-user, and region.

Fluid Catalytic Cracking (FCC) Catalysts Dominate, While Hydrotreating Catalysts Show Strong Growth

Fluid Catalytic Cracking catalysts constitute a majority share in the Global Refinery Catalysts market, making up about 36% of the market value in 2025 and worth US$ 3.53 billion. The significance of FCC catalysts in refineries lies in their ability to convert vacuum gas oil and heavier feeds to gasoline and other valuable products such as LPG and propylene. The use of FCC catalysts is continuous due to several reasons including high operating temperatures, deposition of coke, presence of metals, and frequent changes of the catalyst. For refiners, FCC catalyst performance directly affects conversion efficiency, product selectivity, octane quality, coke yield and overall refinery margins.

The hydrotreating catalysts market is forecasted to record significant growth over the period of 2026-2035, with a projected growth rate of 5.8% CAGR, which will be significantly higher than the growth trend of the entire market. The increased investment by refineries in producing low-sulfur fuels is driving growth in the segment, along with other applications such as fuel quality enhancement and compliance with clean fuel standards. Growth is also supported by heavier crude processing, renewable fuel co-processing and stricter transportation fuel specifications, making hydrotreating catalysts a critical upgrade area for refiners focused on compliance, operational reliability and long-term margin protection.

Geographical Penetration

Asia-Pacific Refinery Expansion and Petrochemical Integration Are Driving Advanced Catalyst Adoption

The Asia-Pacific Refinery Catalyst Market is expected to remain the leading regional market, accounting for approximately 37.4% of the Global Refinery Catalyst Market in 2025, supported by large refinery capacity, high crude processing intensity and continued refinery-petrochemical integration across China, India, South Korea, Japan and Southeast Asia. The region is structurally important because refiners are upgrading FCC, hydrotreating, hydrocracking and sulfur recovery units to process heavier crude, meet cleaner fuel specifications and maximize gasoline, diesel, jet fuel and petrochemical feedstock yields. OPEC’s World Oil Outlook 2024 indicates that around 5.8 million barrels per day of new refining capacity is expected during 2024–2030, with Asia-Pacific accounting for the largest share at nearly 3.2 million barrels per day, reinforcing the region’s long-term importance for refinery catalyst demand.

From a catalyst demand perspective, Asia-Pacific benefits from both scale and refinery complexity. China and India continue to influence global refining additions, while mature refining hubs such as South Korea and Japan remain catalyst-intensive due to advanced refinery configurations and export-oriented product quality requirements. Refineries across the region are prioritizing catalyst systems that improve sulfur removal, conversion efficiency, hydrogen utilization and feedstock flexibility. This positions Asia-Pacific as the strongest demand center for FCC catalysts, hydrotreating catalysts and hydrocracking catalysts.

U.S Refinery Catalyst Market Trends

The U.S. Refinery Catalyst Market is shaped by high refinery complexity, strong FCC capacity, advanced hydro processing intensity and strict fuel-quality compliance. U.S. refiners are prioritizing catalyst systems that improve gasoline yield, ultra-low sulfur diesel production, hydrogen efficiency and feedstock flexibility, especially across Gulf Coast and Midwest refinery networks. According to EIA data, U.S. operable refinery capacity was around 18.16 million barrels per day in early 2026, while U.S. crude distillation gross input reached more than 17.2 million barrels per day in December 2025, indicating strong utilization of catalyst-intensive refining assets.

A key trend is the shift toward performance-led catalyst procurement rather than standard replacement buying. Refineries are evaluating FCC catalysts, hydrotreating catalysts and hydrocracking catalysts based on cycle life, contaminant tolerance, sulfur reduction, coke control and product yield uplift. The U.S. also remains highly exposed to clean fuel specifications, with gasoline sulfur limits at 10 ppm under Tier 3 standards, which increases the importance of advanced hydrotreating and FCC gasoline treatment catalysts. As refiners process opportunity crudes and optimize margins, catalyst suppliers with strong technical service, refinery troubleshooting and performance benchmarking capabilities are gaining stronger commercial relevance.

Japan Refinery Catalyst Market Outlook

The Japan Refinery Catalyst Market is expected to remain mature but highly specialized, supported by complex refinery configurations, strict product-quality standards and continued focus on operational efficiency. Japan’s refining sector is no longer capacity-expansion led; instead, catalyst demand is increasingly tied to refinery optimization, sulfur reduction, residue handling, hydrogen efficiency and yield improvement. According to the Petroleum Association of Japan, Japan had 19 refineries with total crude oil processing capacity of 3,110,400 barrels per day as of March 2025, highlighting a sizable but consolidating refining base.

Japan’s catalyst demand is also shaped by declining domestic petroleum consumption, refinery rationalization and the need to maintain high product quality despite lower throughput growth. EIA noted that Japan’s petroleum product consumption was expected to fall to 3.3 million barrels per day in 2024, reflecting long-term demand pressure from demographic and economic shifts. As a result, refiners are likely to prioritize high-performance FCC, hydrotreating, hydrocracking and sulfur recovery catalysts that improve unit reliability, extend cycle life and support export-grade fuel production rather than broad capacity-driven catalyst volume growth.

Competitive Landscape

The Global Refining Catalyst market is very technology-driven, with competition revolving around catalyst performance, refinery process know-how, feedstock versatility and technical service longevity. BASF, Grace, Honeywell-UOP, Ketjen and Shell Catalysts & Technologies are well-established players based on their diversified refinery catalyst product range and established connections with refiners worldwide and expertise in FCC, hydrotreatment, hydrocracking, reforming and refinery optimization processes. These organizations differentiate themselves through their ability to assist refiners achieve higher fuel yields, reduced sulfur contents, extended catalyst lifespan, minimized coke generation and margin protection amid changing feed stocks.

Topsoe, Axens Group, Clariant Catalysts, Johnson Matthey, Sinopec Catalyst Co., Ltd., JGC Catalysts and Chemicals Ltd., Zeolyst International, and Evonik offer more competition by offering catalyst chemistry, hydro processing products, zeolite technology, absorbents, licensing, and refinery ties in various geographical locations. Competitive advantage has moved from just the availability of catalysts to catalyst programs where vendors provide not only their products but also technical assistance, cost reduction throughout the catalyst life cycle, regeneration, emissions, and performance benchmarks. Vendors with proven refinery references, reliable supply chains and application-specific catalyst solutions are better positioned to win long-term refinery contracts.

Recent Developments

- May 2026: BASF opened a new R&D center for refinery catalyst innovation at its Attapulgus, Georgia site, co-located with its largest global refinery catalyst production facility. The move strengthens BASF’s applied research capability for next-generation FCC catalysts and shortens the pathway from lab-scale development to commercial refinery deployment.

- March 2026: Albemarle completed the sale of a controlling stake in Ketjen to KPS Capital Partners, while retaining a minority stake. The transaction gives Ketjen a more focused ownership structure for refinery catalyst growth, with KPS holding operational control and Albemarle retaining its Performance Catalyst Solutions business separately.

- February 2026: Honeywell entered into an amended agreement to acquire Johnson Matthey’s Catalyst Technologies business, reducing the consideration to £1.325 billion and extending the long stop date. The deal is strategically relevant because it can strengthen Honeywell UOP’s catalyst and process technology position across refining, petrochemicals and energy transition applications.

- February 2026: Axens completed the acquisition of 100% of Eurecat, strengthening its global catalyst services, catalyst circularity, ex situ activation and metals reuse capabilities. This positions Axens more strongly in lifecycle catalyst management, an increasingly important area as refiners focus on cost control and sustainability.

- October 2025: Ketjen and Axens reached a new Eurecat relationship and collaboration agreement, under which Axens planned to become the sole owner of Eurecat following the acquisition of Ketjen’s shares. The development reinforces the growing strategic importance of catalyst regeneration, metals recovery and circular catalyst services in refinery operations.

- October 2025: Albemarle announced the sale of a 51% stake in Ketjen’s refining catalyst solutions business to KPS Capital Partners. The transaction reflected Albemarle’s portfolio reshaping while creating a more dedicated growth platform for Ketjen’s global refining catalyst business.

- May 2025: Honeywell announced an agreement to acquire Johnson Matthey’s Catalyst Technologies business for £1.8 billion. The acquisition was positioned to expand Honeywell’s catalyst and process technology portfolio, including refining and petrochemical catalyst capabilities under its energy and sustainability solutions platform.

- August 2024: BASF launched Fourtiva, a new FCC catalyst for gasoil to mild resid feedstock. The catalyst was designed to improve butylene yields, naphtha octane and LPG olefinicity while reducing coke and dry gas formation, supporting refinery margin improvement and lower carbon intensity in FCC operations.

AI Impact Analysis

AI technologies are revolutionizing the Global Refining Catalysts Market through improved monitoring and optimization of catalytic performance in fluid catalytic cracking, hydrotreatment, hydrocracking, reforming, and sulfur recovery units. Rather than depending on periodic laboratory analysis and operational experience to manage catalyst activity and effectiveness, refineries are turning to process analytics enabled by AI technologies to predict catalyst deactivation, optimize reaction parameters, reduce coke formation, enhance yield selectivity, and increase catalyst longevity.

For catalyst suppliers, AI is becoming a strategic differentiator in product development and customer support. Advanced modeling can accelerate catalyst formulation, simulate feedstock behavior, identify performance gaps and support refinery-specific recommendations. Vendors that combine catalyst chemistry with digital advisory tools, predictive maintenance, process optimization and performance benchmarking are likely to gain stronger buyer preference. As refiners prioritize margin protection, lower emissions, feedstock flexibility and operational reliability, AI-enabled catalyst optimization will increasingly influence procurement decisions and long-term supplier relationships.

White Space Opportunities

The Global Refinery Catalyst Market contains several avenues to explore when it comes to white space opportunities. These include high-performance hydro processing catalysts, residue upgrading catalysts, sulfur recovery catalysts, and catalyst solutions for heavy, sour, and opportunity crude oil. Refineries are in search of catalysts that will enhance their conversion efficiencies, cut down sulfur and nitrogen levels, take care of metal problems, minimize coke deposits, and increase cycle lengths. In this respect, there is an opportunity for those companies that supply custom-made refinery catalysts instead of generic catalysts.

There are also excellent growth opportunities within the co-processing of renewable fuels, catalyst regeneration, reducing refinery emissions, and utilizing AI for optimal catalyst design. In their search for renewable bio-feedstocks, oil wastes, and reduced carbon footprint fuels, the suppliers can create innovative solutions related to feedstock flexibility, efficiency in hydrogen utilization, and product quality management. Those catalyst vendors who will provide not only products but also their own services, including cost-lifecycle analysis, digital monitoring, and performance-oriented contracts, can be truly unique. The newly formed markets of refineries within the Asia-Pacific, Middle East, and Africa regions can become a valuable source of growth.

DMI Opinion

As per the findings of DataM, there is a shift in the Global Refining Catalyst industry from a traditional consumables industry to one focused on performance optimization. The refiners are not merely buying catalysts just to continue operations; they are considering their ability to increase margins, increase cycle time, process heavy crudes, reduce sulfur content and adhere to fuel specifications. The choice of catalyst in this case becomes extremely important in areas such as FCC, hydrotreating, hydrocracking, and sulfur recovery processes where performance impacts yields, costs and standards.

Catalyst suppliers who have strong chemistry in combination with engineering services for troubleshooting, catalyst regeneration services, and digital performance optimization will outperform their price-focused competitors. There will be the most growth opportunities when there are high levels of feed variability, cleaner fuels requirements, refinery-integrated petrochemistry operations, and increasing asset efficiency pressures at refineries. The next stage of competition is based on customized catalyst systems, total cost savings, field-proven results, and helping refiners achieve profitability, emission control, and feed flexibility.

Why This Report Matters in 2026?

The Global Refinery Catalysts Market is important in 2026 because refineries need to maintain profitability despite increasing pressure to meet clean fuel requirements, process more challenging crudes, and achieve higher conversion rates within FCC, hydrotreating, hydrocracking, and sulfur removal units. Catalyst choice is not just another purchasing decision anymore, but has an immediate bearing on the yields, cycle time, hydrogen use, sulfur content, coke production, and value addition of the refinery.

This study helps stakeholders understand where catalyst demands are rising, what new technology trends are emerging, and how purchasing priorities are evolving for national oil companies, fully integrated refiners, and independents. It provides a systematic assessment of catalyst type, composition, feedstocks used, applications, refinery configurations, and regional opportunities, thus allowing suppliers, investors, and strategists to target high growth processes, analyze their competition, and ensure that their portfolio matches market needs.

Why Choose DataM?

- Refinery Catalyst Ecosystem End-to-End Assessment: Examines the entire ecosystem of refinery catalysts from the perspective of fluid catalytic cracking catalysts, hydrotreating catalysts, hydrocracking catalysts, reforming catalysts, alkylation catalysts, isomerization catalysts, sulfur recovery catalysts, as well as additives.

- Product & Technology Assessment: Identifies the leading catalysts through assessing their performance on the metrics of conversion efficiency, selectivity, contaminant tolerance, cycle life, coke reduction, performance in sulfur removal, hydrogenation and stability in refinery operations.

- Application & Use Case Assessment: Monitors catalyst application trends and growth drivers in gasoline production, diesel upgrade processes, production of jet fuel, liquefied petroleum gas, petrochemical feedstock, sulfur removal, heavy oil upgrading, residue processing and renewable fuels co-processing.

- Refinery Process & Feedstock Assessment: Evaluates catalyst usage trends in hydro skimming refineries, conversion refineries, deep conversion refineries and integrated refining/petrochemical plants, while also assessing the needs for crude oil, vacuum gas oil, naphtha, diesel, heavy oils and residue feeds.

- Regulatory and Sustainability Assessment: Assesses the effect of policies related to low-sulfur fuels requirements, refinery emissions, clean fuel specifications, carbon reductions, catalyst waste management and other sustainability measures on the development of the region’s market.

- Competitive Strategy Benchmarking: Reviews competition between BASF, Grace, Honeywell UOP, Ketjen, Shell Catalysts & Technologies, Topsoe, Axens Group, Clariant Catalysts, Johnson Matthey and Sinopec Catalyst Co., Ltd. in terms of the quality of catalyst product line, alliances, customer references, technical services, regional coverage, etc.

- Pricing, Procurement and Market Entry Analysis: Analyzes catalyst pricing, bidding processes at refineries, catalyst replacement intervals, regeneration economics, catalyst life-cycle costs and procurement approaches used.

- Market Opportunities and Business Strategies: Pinpoints white spaces that could be targeted in terms of FCC catalyst optimization, hydroprocessing catalyst improvement, residue upgrading, sulfur removal, catalyst regeneration, renewable fuels co-processing, refinery-petrochemical complex operation, new refinery markets and other areas of potential growth.

Key Procurement Priorities and Buyer Evaluation Criteria

- Buyers in the Global Refinery Catalyst Market are increasingly prioritizing catalysts that deliver higher conversion efficiency, stronger selectivity, longer cycle life, improved contaminant tolerance, lower coke formation and better operating stability under variable crude quality.

- Procurement decisions are shifting toward process-specific catalyst solutions that support FCC, hydrotreating, hydrocracking, catalytic reforming, alkylation, isomerization and sulfur recovery units, enabling refiners to improve product yield, fuel quality and compliance performance.

- Oil refineries, integrated refining and petrochemical complexes, national oil companies and independent refiners are evaluating vendors based on catalyst performance, technical service support, process optimization capability, regeneration potential, feedstock flexibility, supply reliability, lifecycle cost and proven refinery references.

- Vendors with strong capabilities in FCC catalysts, hydro processing catalysts, residue upgrading, sulfur reduction, catalyst additives, regeneration support and refinery troubleshooting are better positioned to win long-term refinery contracts as buyers move toward margin-focused, compliance-driven and performance-based catalyst procurement.