Portable Diagnostics Devices Market Size

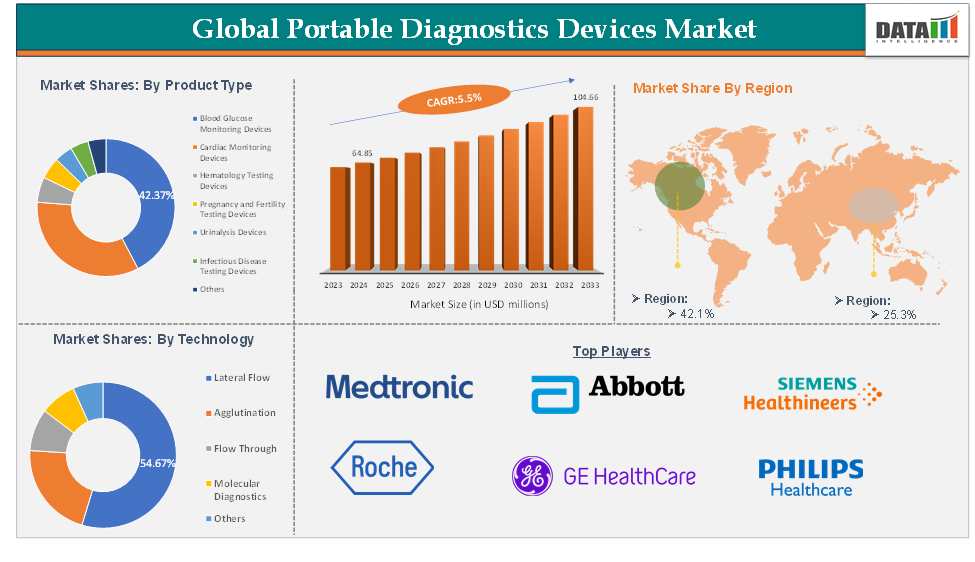

The Portable Diagnostics Devices Market reached US$ 68.42 million in 2025 and is expected to reach US$ 104.66 million in 2033, growing at a CAGR of 5.5% during the forecast period (2026–2033).

Portable diagnostic devices are miniature, lightweight medical testing instruments that perform diagnostic tests at or near the point of care, except instead of laboratory space or hospitals, proper testing can be done. The testing procedures are fast in monitoring various health issues, including, for example, measuring sugar levels in the blood, blood pressure, infection, or heart activity. Due to their nature, these devices proved quite handy for use in remote locations, emergencies, or home care.

The global portable diagnostics market is driven by growing demand for point-of-care testing, rising prevalence of chronic diseases, and other factors. Followed by the market faces different challenges, limited accuracy and reliability in some devices, regulatory and reimbursement challenges, which hinder the market during the forecast period.

Executive Summary

For more details on this report, Request for Sample

Portable Diagnostics Devices Market Dynamics: Drivers & Restraints

Growing Demand for Point-of-Care Testing is Driving the Market Growth

The increasing demand for POCT is among key factors fueling market growth for portable diagnostic devices, which facilitate rapid diagnosis and consequent clinical decision-making outside conventional clinical settings.

Therefore, meeting that requirement is essentially due to portable diagnostic devices that empower the healthcare workforce and patients to conduct tests at the bedside, in outpatient facilities, or even at their home setups while minimising their dependence on centralised laboratories. This provides the utmost convenience to patients while also allowing clinical intervention to be even faster, something that becomes critical, especially in chronic conditions such as diabetes mellitus, hypertension, and cardiovascular disorders.

Moreover, in developing countries and in rural areas that remain devoid of proper healthcare infrastructure, these devices act as conduits for essential testing where conventional laboratory support is absent. Technological progress involving wireless connectivity, smartphone integration, and AI-powered data interpretation has enhanced the ability and reliability of portable diagnostic tools, thereby making them a key element of modern-day and patient-centric healthcare models.

Limited Accuracy and Reliability in Some Devices Restraining the Market Growth

One crucial hindrance to the mass adoption of portable diagnostic devices is their continual concern regarding accuracy, sensitivity, and, more so, their reliability compared to traditional methods of testing performed in a laboratory or clinic. While convenience and quickness remain synonymous with such portable solutions, sometimes they are lacking in delivering consistent results with precision and reliability, mainly when applied in environments other than a clinically controlled one. For example, a scenario might exist where a user's error or environmental conditions, such as temperature and humidity, play a role in affecting the outcome of a test.

Furthermore, the efficacy of such tests could be subject to issues arising from a lack of adequate device calibrations or differences in the quality of samples collected for testing. To cite another example, the use of point-of-care testing kits at home may yield variably accurate results because of improper use or lack of professional oversight, which can lead to misdiagnosis or delayed treatment.

Market Scope

| Metrics | Details | |

| CAGR | 5.5% | |

| Market Size Available for Years | 2023-2033 | |

| Estimation Forecast Period | 2026-2033 | |

| Revenue Units | Value (US$ Mn) | |

| Segments Covered | Product Type | Blood Glucose Monitoring Devices, Cardiac Monitoring Devices, Hematology Testing Devices, Pregnancy and Fertility Testing Devices, Urinalysis Devices, Infectious Disease Testing Devices, Others |

| Technology | Lateral Flow, Agglutination, Flow Through, Molecular Diagnostics, Others | |

| Application | Cardiology, Infectious Diseases, Diabetes, Oncology Pregnancy Testing, Hematology, Others | |

| End-User | Hospitals & Clinics, Home Healthcare, Diagnostic Centers, Ambulatory Surgical Centers (ASCs) | |

| Regions Covered | North America, Europe, Asia-Pacific, South America, and the Middle East & Africa | |

Portable Diagnostics Devices Market Segment Analysis

The global portable diagnostics devices market is segmented based on product type, technology, application, end-user, and region.

Product Type:

The blood glucose monitoring segment is expected to hold 42.3% of the portable diagnostics devices market

Blood glucose monitoring tools are medical devices that determine the amount of glucose in a person's blood to help with controlling and monitoring diabetes. They provide real-time data about the person's glucose levels; therefore, the patient, with the help of a healthcare provider, can make decisions about food, drugs, and lifestyle changes. There are mainly two types: one being the traditional BGMs that require a blood drop from a finger prick, while the other is CGMs, where sensors are placed under the skin to record the glucose change throughout the day. Progress in technology has enabled many such devices to now have smartphone compatibility, cloud data storage, and predictive alerts to further ease the usage of the device while increasing clinical utility.

The demand for the blood glucose monitoring devices segment is driven due to factors such as sedentary lifestyles, poor diets, obesity, and aging populations. Millions of new diabetes cases are diagnosed annually, putting a strain on healthcare systems. Effective self-monitoring tools are needed to manage blood glucose levels and prevent complications like kidney failure and heart disease. The demand for accessible, user-friendly, and accurate devices is rising. Increased awareness of early diagnosis and continuous management, along with government and private sector initiatives, has led to higher adoption rates. Continuous glucose monitors (CGMs) are popular due to their real-time data and convenience.

Portable Diagnostics Devices Market Geographical Analysis

North America is expected to hold a 42.1% of share in the portable diagnostics devices market

North America marks a pivotal region in the global portable diagnostic devices market on account of several factors that underscore its front-running position. The presence of a high patient incidence of chronic diseases such as diabetes, cardiovascular diseases, and respiratory conditions requires constant monitoring and management of patients. Also, FDA clearance, advanced healthcare infrastructure, and other factors help the region to grow during the forecast period.

Moreover, backed by advanced healthcare infrastructure, the region is supported by highly advanced medical facilities and a dense network of medical professionals who are conversant with cutting-edge diagnostic technologies. Further technological evolutions position North America at the forefront as well, witnessing the highest development and application of AI-based health monitoring systems and medical devices integrated with IoT aimed at bettering the accuracy and accessibility of diagnostics.

Asia-Pacific is expected to hold a 25.3% of share in the portable diagnostics devices market

The Asia-Pacific portable diagnostic devices market is driven by factors such as rising healthcare expenditure, chronic and infectious diseases, and demand for point-of-care testing in remote areas. The growing geriatric population, early disease detection awareness, and advanced technologies like IoT and AI are also contributing to market growth. Government initiatives and telemedicine adoption further accelerate the demand for these diagnostic tools.

For instance, in December 2025, Nippon Avionics has introduced Japan's first portable medical thermography system, the "F50ME". This device consists of a tablet and a lightweight camera head, designed for medical professionals and patients. It is compatible with load testing and can be used in any location and posture, aiming to reduce patient burden and improve operational efficiency.

Portable Diagnostics Devices Market Key Players

The major global players in the portable diagnostics devices market include Abbott, F. Hoffmann-La Roche Ltd, Siemens Healthineers, GE HealthCare, Philips Healthcare, Medtronic, LifeScan, Inc., Nova Biomedical, Becton, Dickinson and Company (BD), and Axxin, among others.

Recent Developments

In March 2026, Abbott Laboratories expanded its portable diagnostic portfolio with handheld devices for rapid testing and real-time results. The innovation focuses on accessibility and point-of-care efficiency. This supports decentralized healthcare delivery.

In February 2026, Roche Diagnostics introduced advanced portable diagnostic systems with improved connectivity and data integration. The development enhances remote patient monitoring and diagnostics. This benefits healthcare providers and patients.

In January 2026, Siemens Healthineers strengthened its portable diagnostic solutions with compact and high-precision devices. The focus is on improving diagnostic accuracy and mobility. This supports point-of-care applications.

Why Purchase the Report?

- Technological Innovations: Reviews ongoing clinical trials, Product Type pipelines, and forecasts upcoming advancements in medical devices and pharmaceuticals.

- Product Type Performance & Market Positioning: Analyzes Product Type performance, market positioning, and growth potential to optimize strategies.

- Real-World Evidence: Integrates patient feedback and data into Product Type development for improved outcomes.

- Physician Preferences & Health System Impact: Examines healthcare provider behaviors and the impact of health system mergers on adoption strategies.

- Market Updates & Industry Changes: Covers recent regulatory changes, new policies, and emerging technologies.

- Competitive Strategies: Analyzes competitor strategies, market share, and emerging players.

- Pricing & Market Access: Reviews pricing models, reimbursement trends, and market access strategies.

- Market Entry & Expansion: Identifies optimal strategies for entering new markets and partnerships.

- Regional Growth & Investment: Highlights high-growth regions and investment opportunities.

- Supply Chain Optimization: Assesses supply chain risks and distribution strategies for efficient Product Type delivery.

- Sustainability & Regulatory Impact: Focuses on eco-friendly practices and evolving regulations in healthcare.

- Post-market Surveillance: Uses post-market data to enhance Product Type safety and access.

- Pharmacoeconomics & Value-Based Pricing: Analyzes the shift to value-based pricing and data-driven decision-making in R&D.

The global portable diagnostics devices market report delivers a detailed analysis with 62 key tables, more than 56 visually impactful figures, and 200 pages of expert insights, providing a complete view of the market landscape.

Target Audience

- Manufacturers: Pharmaceutical, Medical Device, Biotech Companies, Contract Manufacturers, Distributors, Hospitals.

- Regulatory & Policy: Compliance Officers, Government, Health Economists, Market Access Specialists.

- End-User & Innovation: AI/Robotics Providers, R&D Professionals, Clinical Trial Managers, Pharmacovigilance Experts.

- Investors: Healthcare Investors, Venture Fund Investors, Pharma Marketing & Sales.

- Consulting & Advisory: Healthcare Consultants, Industry Associations, Analysts.

- Supply Chain: Distribution and Supply Chain Managers.

- Consumers & Advocacy: Patients, Advocacy Groups, Insurance Companies.

- Academic & Research: Academic Institutions.