Lung Stents Market Size

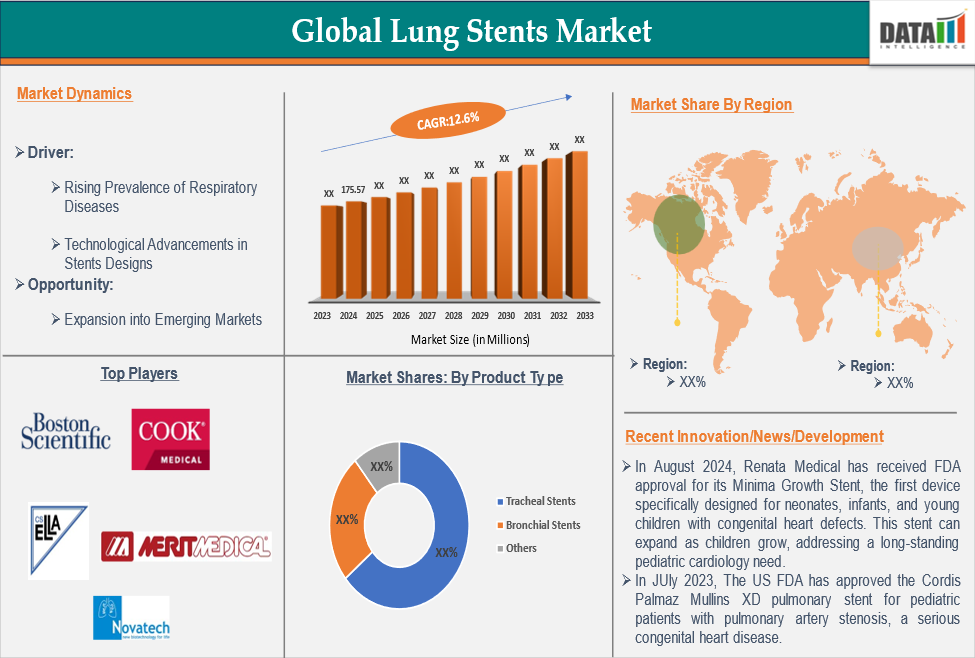

Global Lung Stents Market reached US$ 175.57 million in 2024 and is expected to reach US$ 579.98 million by 2033, growing at a CAGR of 12.6% during the forecast period 2025-2033.

Lung stents are medical devices used to maintain airway patency in patients with obstructed or narrowed airways due to conditions like lung cancer, tracheobronchial stenosis, or COPD. These tubular-shaped implants prevent airway collapse and facilitate normal breathing. Made from metal, silicone, or hybrid combinations, they offer flexibility, durability, and ease of removal. They are commonly used in minimally invasive procedures via bronchoscopy, providing relief for respiratory complications and improving lung function.

Executive Summary

Source : DataM Intelligence

For more details on this report – Request for Sample

Market Dynamics: Drivers & Restraints

Rising Prevalence of Respiratory Diseases

The global lung stents market is growing due to the rise in respiratory diseases like lung cancer, COPD and tracheobronchial stenosis. These conditions cause airway obstruction and breathing difficulties, making stents crucial for maintaining airway patency and improving respiratory function. The aging population, environmental pollutants, and high smoking rates contribute to the surge in respiratory cases worldwide. The demand for minimally invasive treatments like stent placements is boosting market expansion. Advancements in stent Material, including drug-eluting and biodegradable stents, further enhance treatment outcomes.

For instance, in 2020, COPD prevalence was 10.6% globally, resulting in 480 million cases. By 2050, it is projected to increase by 112 million to 592 million, a 23.3% increase from 2020 to 2050. This rise is primarily due to the rising COPD burden among females and in low- and middle-income countries (LMICs). Hence, the rise in the respiratory diseases indeed the need for lung stents demand are raised which helps the overall market to grow during the forecast period.

Complications and Risk of Stent-Related Infections

Lung stents, despite their benefits, carry risks like stent migration, granulation tissue formation, and infections, which can hinder their widespread use. Prolonged stent placement can cause airway irritation, obstruction, or bacterial infections, necessitating additional medical intervention. The complexity of stent removal and replacement procedures adds to healthcare professionals' challenges.

Market Segment Analysis

The global lung stents market is segmented based on product type, material, end-user and region.

Product Type:

The tracheal stents from product type segment is expected to dominate the lung stents market

The tracheal stents holds is a significant position in the global lung stents market, providing life-saving solutions for patients with tracheal obstructions. These stents maintain airway patency, improving patient quality of life. Demand for tracheal stents is growing due to respiratory diseases and minimally invasive procedures. Innovations in stent materials, such as self-expanding metal and bioresorbable stents, have enhanced their effectiveness. Focusing on patient-specific customization and improved biocompatibility, tracheal stents drive market growth in emergency and long-term respiratory care.

For instance, in March 2022, Micro-Tech Endoscopy has introduced the first self-expanding tracheobronchial nitinol y-stent, the Y-Shaped Tracheal Stent System, designed for flexible and compliant treatment of malignant neoplasms at the tracheobronchial carina. Hence, the above solution helps for complex tracheobronchial obstructions, improving patient outcomes and procedural flexibility. This product also drives market growth by increasing the adoption of self-expanding nitinol stents in airway management.

Market Geographical Share

North America is expected to hold a significant position in the lung stents market with the highest market share

North America dominates the global lung stents market due to high prevalence of respiratory diseases like COPD and lung cancer, advanced healthcare infrastructure, increased healthcare spending, and widespread adoption of minimally invasive procedures. Strong research and development initiatives, favorable reimbursement policies, and the presence of leading medical device companies support market expansion. Government funding for respiratory disease management and technological advancements in stent designs further enhance treatment outcomes, making North America a dominant player in this sector.

Additionally, rise in number of product launches, approvals also drive this region to dominate during the forecast period. For instance, in October 2024, The FDA has approved a new stent designed to open airways in patients with growing cancers. The minimally invasive AMStent system, developed by Peytant Solutions, uses a metal frame encased in human amnion, a pliable membrane that forms the amniotic sac. Amnion has been used in various medical specialties for years, including treating chronic wounds, burns, and skin ulcers.

Major Global Players

The major global players in the lung stents market include Boston Scientific Corporation, Cook Medical, ELLA-CS, s.r.o, Merit Medical Systems, Inc., Novatech SA, Micro-Tech (Nanjing) Co., Ltd., S&G Biotech Inc., Medorah Meditek Pvt. Ltd, Mitrai Industries and E. Benson Hood Laboratories, Inc among others.

Market Scope

| Metrics | Details | |

| CAGR | 12.6% | |

| Market Size Available for Years | 2022-2033 | |

| Estimation Forecast Period | 2025-2033 | |

| Revenue Units | Value (US$ Mn) | |

| Segments Covered | Product Type | Tracheal Stents, Bronchial Stents, Others |

| Material | Metal Stents, Silicone Stents, Hybrid Stents | |

| End-User | Hospitals, Ambulatory Surgical Centers, Specialty Clinics, Others | |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America and Middle East & Africa | |

Why Purchase the Report?

- Technological Innovations: Reviews ongoing clinical trials, product pipelines, and forecasts upcoming advancements in medical devices and pharmaceuticals.

- Product Performance & Market Positioning: Analyzes product performance, market positioning, and growth potential to optimize strategies.

- Real-World Evidence: Integrates patient feedback and data into product development for improved outcomes.

- Physician Preferences & Health System Impact: Examines healthcare provider behaviors and the impact of health system mergers on adoption strategies.

- Market Updates & Industry Changes: Covers recent regulatory changes, new policies, and emerging technologies.

- Competitive Strategies: Analyzes competitor strategies, market share, and emerging players.

- Pricing & Market Access: Reviews pricing models, reimbursement trends, and market access strategies.

- Market Entry & Expansion: Identifies optimal strategies for entering new markets and partnerships.

- Regional Growth & Investment: Highlights high-growth regions and investment opportunities.

- Supply Chain Optimization: Assesses supply chain risks and distribution strategies for efficient product delivery.

- Sustainability & Regulatory Impact: Focuses on eco-friendly practices and evolving regulations in healthcare.

- Post-market Surveillance: Uses post-market data to enhance product safety and access.

- Pharmacoeconomics & Value-Based Pricing: Analyzes the shift to value-based pricing and data-driven decision-making in R&D.

The global lung stents market report delivers a detailed analysis with 70 key tables, more than 65 visually impactful figures and 159 pages of expert insights, providing a complete view of the market landscape.

Target Audience 2025

- Manufacturers: Pharmaceutical, Medical Device, Biotech Companies, Contract Manufacturers, Distributors, Hospitals.

- Regulatory & Policy: Compliance Officers, Government, Health Economists, Market Access Specialists.

- Material & Innovation: AI/Robotics Providers, R&D Professionals, Clinical Trial Managers, Pharmacovigilance Experts

- Investors: Healthcare Investors, Venture Fund Investors, Pharma Marketing & Sales.

- Consulting & Advisory: Healthcare Consultants, Industry Associations, Analysts.

- Supply Chain: Distribution and Supply Chain Managers.

- Consumers & Advocacy: Patients, Advocacy Groups, Insurance Companies.

- Academic & Research: Academic Institutions.