Market Size

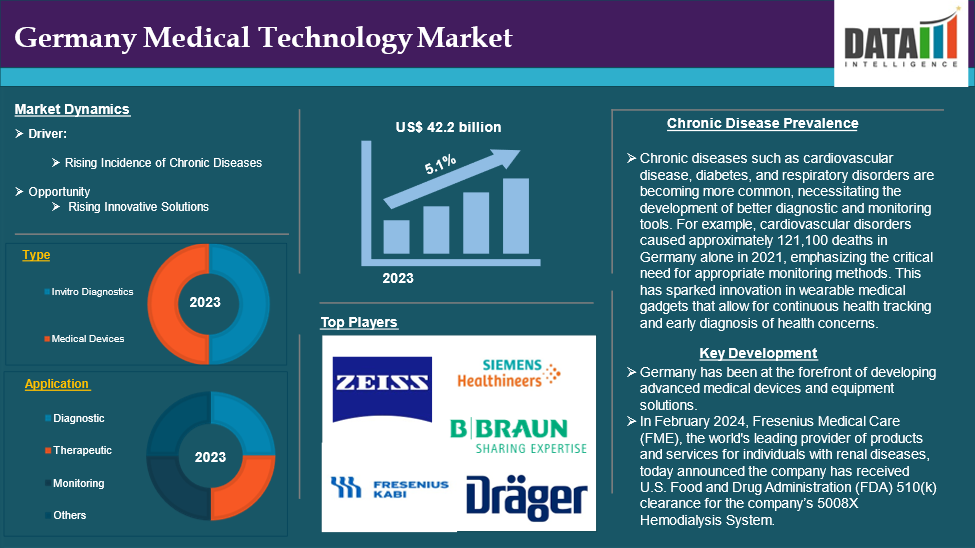

Germany Medical Technology Market reached US$ 46.6 billion in 2025 and is expected to reach US$ 69.2 billion by 2033, growing at a CAGR of 5.1% during the forecast period 2026-2033.

Medical technology encompasses many products, services, and approaches focusing on diagnosing, treating, and improving health and well-being. This field includes a wide range of devices, from simple thermometers to complicated systems like MRI machines.

The fundamental objective of medical technology is to assist healthcare practitioners in providing accurate diagnoses and treatments, hence improving patient outcomes and quality of life. It is essential throughout the healthcare process, from prevention and early identification to treatment and rehabilitation.

Executive Summary

Source:- DataM Intelligence

Market Dynamics: Drivers & Restraints

Rising incidence of chronic diseases

Chronic diseases such as cardiovascular disease, diabetes, and respiratory disorders are becoming more common, necessitating the development of better diagnostic and monitoring tools.

The rise in chronic illnesses has accelerated the use of remote patient monitoring solutions. These technologies enable healthcare providers to monitor patients' health problems without requiring regular in-person visits, increasing patient convenience and healthcare efficiency. The demand for such treatments is likely to increase dramatically, particularly among the elderly, who are more vulnerable to chronic illnesses.

With the rising chronic diseases, companies are developing advanced medical devices by integrating advanced technologies. Companies in the country are receiving approvals from regulatory bodies by meeting their safety guidelines.

High developmental costs

High developmental costs are expected to hinder the Germany medical technology market. Developing medical technologies involves significant investment in research and development (R&D). From the initial concept design to clinical trials, manufacturing, and post-market monitoring, each stage requires considerable financial resources. In Germany, where there is a high demand for top-quality, innovative medical devices, small and medium-sized enterprises (SMEs) may struggle to manage the substantial costs associated with these processes.

Due to strict regulatory requirements, such as the European Union's Medical Device Regulation (MDR), it often takes several years to develop, test, and gain approval for new medical technologies. This delays the return on investment, putting additional financial pressure on companies, particularly smaller ones with limited resources. The MDR has introduced more stringent requirements for medical devices, including extensive clinical trials, detailed documentation, and third-party certifications, which further increase development costs. The greater the complexity of the device, the more rigorous the regulatory scrutiny, resulting in higher costs and longer time-to-market.

For more details on this report – Request for Sample

Segment Analysis

The Germany medical technology market is segmented based on type, application, and end-user.

Product Type:

The medical devices segment is expected to dominate the Germany medical technology market share

The growing preference for minimally invasive procedures is significantly driving the demand for advanced medical devices, which are essential in contemporary healthcare settings due to their ability to enhance diagnostic accuracy and therapeutic outcomes. Innovations such as robotic-assisted surgery and sophisticated imaging techniques exemplify the evolution of medical devices to meet clinical needs.

Furthermore, continuous advancements in technologies, including artificial intelligence (AI), predictive analytics, and telemedicine solutions are transforming patient care by enabling early detection and improved treatment outcomes, which are vital for effectively managing chronic diseases. The integration of smart technologies into these devices also enhances capabilities for patient monitoring and management.

Additionally, rising healthcare expenditures in developed economies like Germany are facilitating greater investment in advanced medical technologies, thereby improving the quality of patient care and operational efficiency within healthcare facilities.

Key Industry Developments

- March 2026: InEK released the finalized 2026 NUB list approving innovation funding for advanced medtech in cardiovascular, endoscopy, neuromodulation, and peripheral vascular categories, including endovascular tricuspid valve replacements and wireless left ventricular stimulation systems to accelerate hospital adoption of cutting-edge implants.

- January 2026: German Government launched the new Pharma & MedTech Dialogue to develop regulatory reforms and policies strengthening medtech innovation, alongside InEK's early NUB approvals for technologies like hemodynamically effective aneurysm implants and gastric pacemakers.

- November 2025: InEK published the 2026 DRG catalog introducing five new DRGs in diagnostic imaging, men's health, nephrology, urology, and radiotherapy, plus 13 new reimbursement categories to support advanced medical technologies and procedures.

Competitive Landscape

The major players in the Germany medical technology market include Siemens Healthineers AG, Carl Zeiss Meditec AG, B. Braun SE, Fresenius Kabi AG, Drägerwerk AG & Co. KGaA, Eppendorf AG, KARL STORZ SE & Co. KG, Olympus Europa SE & Co. KG, Roche Diagnostics GmbH and bioMérieux SA among others.

| Metrics | Details | |

| CAGR | 5.1% | |

| Market Size Available for Years | 2023-2033 | |

| Estimation Forecast Period | 2026-2033 | |

| Revenue Units | Value (US$ Bn) | |

| Segments Covered | Type | Invitro Diagnostics, Medical Devices |

| Application | Diagnostic, Therapeutic, Monitoring, Others | |

| End-User | Pharmaceutical Companies, Research Laboratories, Diagnostic Centers, Others | |

Why Purchase the Report?

- Pipeline & Innovations: Reviews ongoing clinical trials, product pipelines, and forecasts upcoming advancements in medical devices and pharmaceuticals.

- Product Performance & Market Positioning: Analyzes product performance, market positioning, and growth potential to optimize strategies.

- Real-World Evidence: Integrates patient feedback and data into product development for improved outcomes.

- Physician Preferences & Health System Impact: Examines healthcare provider behaviors and the impact of health system mergers on adoption strategies.

- Market Updates & Industry Changes: Covers recent regulatory changes, new policies, and emerging technologies.

- Competitive Strategies: Analyzes competitor strategies, market share, and emerging players.

- Pricing & Market Access: Reviews pricing models, reimbursement trends, and market access strategies.

- Market Entry & Expansion: Identifies optimal strategies for entering new markets and partnerships.

- Regional Growth & Investment: Highlights high-growth regions and investment opportunities.

- Supply Chain Optimization: Assesses supply chain risks and distribution strategies for efficient product delivery.

- Sustainability & Regulatory Impact: Focuses on eco-friendly practices and evolving regulations in healthcare.

- Post-market Surveillance: Uses post-market data to enhance product safety and access.

- Pharmacoeconomics & Value-Based Pricing: Analyzes the shift to value-based pricing and data-driven decision-making in R&D.

The Germany Medical Technology market report delivers a detailed analysis with 60+ key tables, more than 50 visually impactful figures, and 176 pages of expert insights, providing a complete view of the market landscape.

Target Audience 2026

- Manufacturers: Pharmaceutical, Medical Device, Biotech Companies, Contract Manufacturers, Distributors, Hospitals.

- Regulatory & Policy: Compliance Officers, Government, Health Economists, Market Access Specialists.

- Technology & Innovation: AI/Robotics Providers, R&D Professionals, Clinical Trial Managers, Pharmacovigilance Experts.

- Investors: Healthcare Investors, Venture Fund Investors, Pharma Marketing & Sales.

- Consulting & Advisory: Healthcare Consultants, Industry Associations, Analysts.

- Supply Chain: Distribution and Supply Chain Managers.

- Consumers & Advocacy: Patients, Advocacy Groups, Insurance Companies.

- Academic & Research: Academic Institutions