Antipeptic Ulcer Drugs Market Size & Industry Outlook

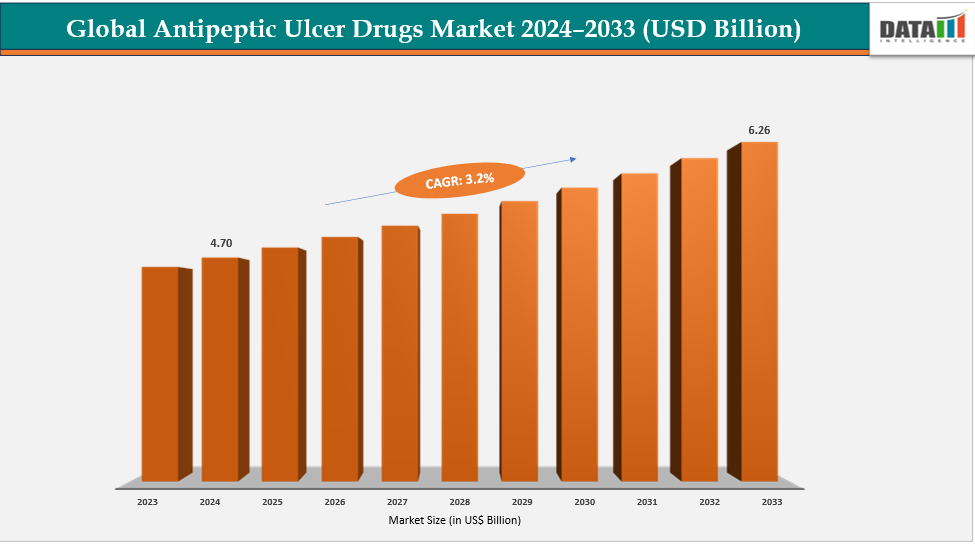

The global antipeptic ulcer drug market size reached US$ 4.56 Billion in 2023 with a rise of US$ 4.70 Billion in 2024 and is expected to reach US$ 6.26 Billion by 2033, growing at a CAGR of 3.2% during the forecast period 2025-2033.

The antipeptic ulcer drug market is witnessing significant growth due to OTC availability, patient self-care, and widespread use of proton pump inhibitors (PPIs). Patients can get PPIs over-the-counter (OTC) without a prescription, which improves convenience and grows the customer base. Regular intake is driven by rising health consciousness, which motivates people to self-manage diseases including acid reflux, heartburn, and recurrent ulcers. Both patients and doctors choose PPIs because of their high effectiveness in lowering stomach acid and their long-term use for chronic illnesses including GERD and ulcers brought on by NSAIDs.

Key Highlights

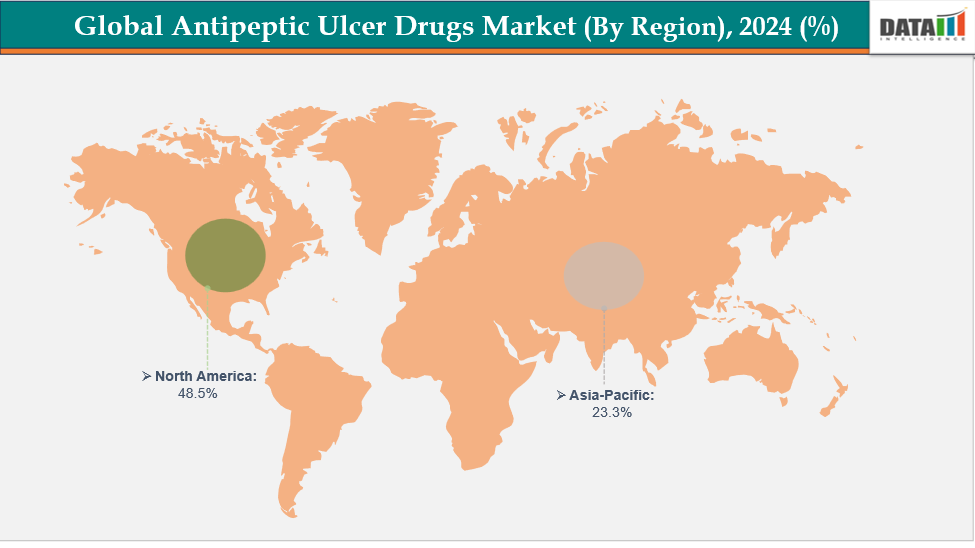

- North America is dominating the global antipeptic ulcer drugs market with the largest revenue share of a 48.5% in 2024

- The Asia Pacific region is the fastest-growing region in the global with a CAGR of 7.5% in 2024

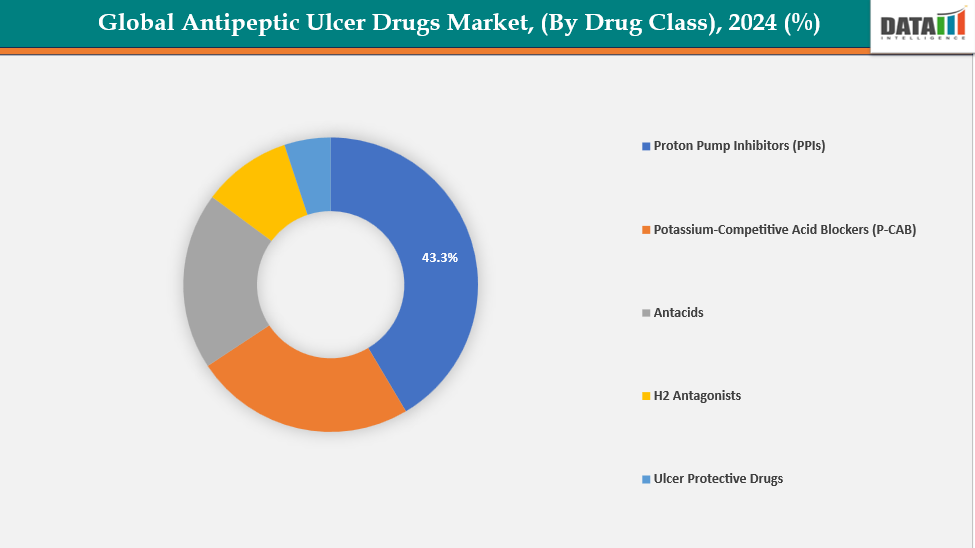

- The proton pump inhibitors segment from drug class is dominating the antipeptic ulcer drugs market with a 43.3% share in 2024.

- The gastroesophageal reflux disease (GERD) segment form application is dominating the antipeptic ulcer drugs market with a 42.5% share in 2024.

- Top companies in the antipeptic ulcer drug market include AstraZeneca, Sun Pharmaceutical Industries Ltd., Takeda Pharmaceuticals America, Inc., Pfizer Inc., Torrent Pharmaceuticals Ltd., Glenmark Pharmaceuticals Inc., USA, Medtech Products Inc., Teva Pharmaceuticals USA, Inc., Zydus Healthcare Limited, And Lupin among others.

Market Dynamics

Drivers: High and persistent prevalence of H. pylori and related GI disorders is significantly driving the antipeptic ulcer drugs market growth

The high and persistent prevalence of Helicobacter pylori infection, a primary cause of gastric and duodenal ulcers, is a major factor propelling the antipeptic ulcer drugs market. Since almost half of the world's population is afflicted with H. pylori, especially in poorer nations, there is a greater need for proton pump inhibitors, antibiotics, and combination treatments to eradicate the infection.

Additionally, the rising prevalence of GI conditions including peptic ulcers, GERD, and gastritis brought on by a poor diet, stress, and the widespread use of NSAIDs also contributes to drug use. Prescription volumes are increasing as a result of education campaigns encouraging early treatment and rising diagnostic rates.

Restraints: Safety concerns with long-term PPI use are hampering the growth of the antipeptic ulcer drugs market

Proton pump inhibitors (PPIs) such as omeprazole, pantoprazole, and esomeprazole are the mainstay treatment for peptic ulcers. However, cautious prescribing practices have been brought about by mounting evidence of negative effects linked to long-term use. In several studies, chronic PPI therapy has been associated with a higher incidence of gastrointestinal cancers, vitamin B12 deficiency, bone fractures, kidney illness, hypomagnesemia, and Clostridium difficile infections.

For instance, according to Yale Medicine, long-term PPI use was associated with increased risks of bone fractures, infections such as pneumonia and C. difficile, and nutritional deficiencies, including magnesium, iron, and vitamin B12, likely due to reduced stomach acid production.

For more details on this report, see Request for Sample

Segmentation Analysis

The global antipeptic ulcer drugs market is segmented based on drug class, application, route of administration, distribution channel and region

By Drug class: The proton pump inhibitors segment from drug class is dominating the antipeptic ulcer drugs market with a 43.3% share in 2024

Proton Pump Inhibitors (PPIs) are the market leader for antipeptic ulcer medications because they are more effective at suppressing acid, which allows GERD and peptic ulcers to heal more quickly and completely than with H2 antagonists or antacids. Prescription PPIs including omeprazole, pantoprazole, and esomeprazole are frequently used as first-line treatments for ulcers and H. pylori elimination programs.

Additionally, the dominance of the proton pump inhibitors is further reinforced by recent regulatory approvals and market development, and their availability in both prescription and OTC forms further expands patient access. For instance, in March 2025, Eisai Co., Ltd. announced that it had obtained manufacturing and marketing authorization in Japan for the proton pump inhibitor Pariet S, approving its RX-to-OTC switch for treating stomach pain, heartburn, and bloating.

By Application: The gastroesophageal reflux disease (GERD) segment form application is dominating the antipeptic ulcer drugs market with a 42.5% share in 2024

The GERD segment dominates the antipeptic ulcer drug market due to its high and increasing global prevalence, driven by lifestyle factors such as obesity, unhealthy diets, smoking, and stress. Acid-suppressive medications, especially PPIs and the more recent PCABs, are in high demand since patients with GERD frequently need long-term or maintenance therapy to control chronic symptoms including heartburn and acid reflux. The treatment of GERD primarily depends on pharmaceutical therapy rather than curative measures, in contrast to duodenal or gastric ulcers, which are on the decline in many areas as a result of H. pylori eradication. the biggest portion of antipeptic ulcer medication sales and prescriptions.

Additionally, the dominance of gastroesophageal reflux disease is further reinforced by recent regulatory approvals and market development. For in November 2023, Phathom Pharmaceuticals announced that the U.S. FDA approved VOQUEZNA (vonoprazan) tablets, a novel potassium-competitive acid blocker (PCAB), for adults. The approval allowed treatment and maintenance of all grades of erosive GERD, providing heartburn relief and marking the first major U.S. innovation in over 30 years.

Geographical Analysis

North America is dominating the global antipeptic ulcer drugs market with a 48.5% in 2024

North America dominates the global antipeptic ulcer drug market due to high healthcare expenditure, advanced healthcare infrastructure, and widespread awareness of gastrointestinal disorders. Due to the region's high prevalence of GERD, peptic ulcers, and associated disorders, there is a steady need for acid-suppressive treatments, especially potassium-competitive acid blockers (P-CABs) and proton pump inhibitors (PPIs).

Additionally, continuous research, innovation, and regulatory approvals in North America further strengthen market penetration. For instance, in August 2025, Christopher C. Thompson, MD, MSc, at Brigham and Women's Hospital, initiated an interventional clinical trial to evaluate marginal ulcer healing using low-thermal argon plasma endoscopic treatment (AMULET).

Europe is the second region after North America which is expected to dominate the global antipeptic ulcer drugs market with a 34.5% in 2024

Europe’s antipeptic ulcer drug market growth is driven by high awareness of gastrointestinal disorders and well-established healthcare systems. Easy access to hospitals, clinics, and pharmacies, along with supportive government policies and public health initiatives, has boosted adoption of acid-suppressive therapies across adult and at-risk populations.

Germany’s antipeptic ulcer drug market is driven by advanced healthcare infrastructure, supportive regulations, and high public awareness of gastrointestinal disorders. Hospitals, clinics, pharmacies, and digital platforms provide widespread access, while government initiatives and public health campaigns promote early diagnosis and treatment, ensuring robust market growth nationwide.

The Asia Pacific region is the fastest-growing region in the global with a CAGR of 7.5% in 2024

The Asia-Pacific antipeptic ulcer drug market, including Japan, China, India, and South Korea, is growing due to rising awareness of gastrointestinal disorders, urbanization, and improved healthcare access. Public health programs, government initiatives, and pharmaceutical company advancements encourage early diagnosis, treatment uptake, and improved illness management throughout the region.

Japan and India are experiencing rising demand for antipeptic ulcer drugs, driven by pharmaceutical partnerships, non-exclusive patent licensing agreements, increased awareness of gastrointestinal disorders, and expanding healthcare infrastructure supporting broader access and treatment adoption. For instance, in July 2024, Zydus and Sun Pharma entered into non-exclusive patent licensing agreements with Takeda Pharmaceutical Company to market the novel potassium-competitive acid blocker Vonoprazan in India. Zydus marketed it as Vault, while Sun Pharma introduced it as Voltapraz, targeting reflux esophagitis and other acid-peptic disorders.

Competitive Landscape

Top companies in the antipeptic ulcer drug market include AstraZeneca, Sun Pharmaceutical Industries Ltd., Takeda Pharmaceuticals America, Inc., Pfizer Inc., Torrent Pharmaceuticals Ltd., Glenmark Pharmaceuticals Inc., USA, Medtech Products Inc., Teva Pharmaceuticals USA, Inc., Zydus Healthcare Limited, and Lupin, among others.

AstraZeneca:AstraZeneca is a global biopharmaceutical company actively involved in the development and commercialization of antipeptic ulcer drugs. With a strong focus on gastrointestinal therapies, the company offers proton pump inhibitors and acid-suppressive treatments, leveraging research, innovation, and a broad distribution network to address peptic ulcer disease and related gastrointestinal disorders worldwide.

Key Developments:

- In June 2024, Yunovia and Daewon Pharmaceutical entered into a co-development and licensing agreement for a novel potassium-competitive acid blocker (P-CAB) for peptic ulcer. Under the agreement, Daewon Pharmaceutical conducted clinical development of Yunovia’s drug candidate ID120040002 and obtained full rights to seek approval, manufacture, and commercialize the therapy in South Korea.

Market Scope

| Metrics | Details | |

| CAGR | 3.2% | |

| Market Size Available for Years | 2022-2033 | |

| Estimation Forecast Period | 2025-2033 | |

| Revenue Units | Value (US$ Bn) | |

| Segments Covered | By Drug Class | Proton Pump Inhibitors, Potassium-Competitive Acid Blockers, Antacids, H2 Antagonists, Ulcer Protective Drugs |

| By Application | Gastroesophageal Reflux Disease, Duodenal Ulcers, Gastritis, Gastric Ulcers | |

| By Route of Administration | Oral, Intravenous, Intramuscular | |

| By Distribution Channel | Retail Pharmacies, Hospital Pharmacies, Online Pharmacies | |

| Regions Covered | North America, Europe, Asia-Pacific, South America and the Middle East & Africa | |

The Global Antipeptic Ulcer Drugs Market report delivers a detailed analysis with 62 key tables, more than 52 visually impactful figures, and 159 pages of expert insights, providing a complete view of the market landscape.

Suggestions for Related Report

For more pharmaceutical-related reports, please click here